Neurointerventional Devices Market Overview - Definition, scope, and significance

The neurointerventional devices market encompasses a specialized segment of medical devices designed for minimally invasive treatment of neurological conditions affecting the brain, spine, and peripheral nervous system. These devices include neurovascular thrombectomy devices, stents, embolic protection devices, intrasaccular devices, embolic coils, flow diverters, liquid embolics, balloons, and stent retrievers. The market serves critical applications in treating cerebrovascular diseases such as aneurysms, arteriovenous malformations, ischemic strokes, and other neurovascular disorders. This sector holds significant importance in modern healthcare as it enables less invasive procedures with reduced recovery times, lower complication rates, and improved patient outcomes compared to traditional open surgical approaches. The growing prevalence of neurological disorders, aging global population, and technological advancements in interventional techniques continue to drive market expansion and innovation.

Neurointerventional Devices Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The neurointerventional devices market is primarily driven by the increasing incidence of neurological disorders, particularly stroke and brain aneurysms, coupled with the rising geriatric population globally. Technological advancements in device design, such as improved navigability, enhanced visualization, and better material biocompatibility, are accelerating market growth. The shift toward minimally invasive procedures, which offer reduced hospital stays and faster recovery, further propels demand. However, the market faces significant restraints including the high cost of devices and procedures, stringent regulatory approval processes, and the need for specialized training for healthcare professionals. Challenges include reimbursement complexities across different healthcare systems and the risk of complications during procedures. Despite these obstacles, substantial opportunities exist in emerging markets, particularly in Asia-Pacific and Latin America, where improving healthcare infrastructure and rising awareness about advanced treatment options are creating new growth avenues. Additionally, the development of next-generation devices with improved efficacy and safety profiles presents significant market potential.

Neurointerventional Devices Market Growth Trends - Current and emerging trends shaping the market

The neurointerventional devices market is experiencing several transformative trends that are reshaping the industry landscape. One prominent trend is the increasing adoption of flow diversion technology for treating complex aneurysms, which offers a less invasive alternative to traditional surgical clipping. Another significant development is the integration of advanced imaging technologies with interventional devices, enabling real-time visualization and enhanced procedural precision. The market is also witnessing a shift toward personalized medicine approaches, with devices being tailored to individual patient anatomy and pathology. Emerging trends include the development of bioresorbable stents and the incorporation of artificial intelligence for improved treatment planning and device navigation. Additionally, there is growing emphasis on developing devices that can be used in acute stroke treatment, particularly mechanical thrombectomy devices that can rapidly restore blood flow to affected brain regions. The convergence of robotics and neurointerventional procedures represents another frontier, potentially enabling remote procedures and improved access to specialized care in underserved regions.

COVID-19 Impact on the Neurointerventional Devices Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly disrupted the neurointerventional devices market, creating both immediate challenges and long-term implications. During the peak pandemic periods, many elective neurointerventional procedures were postponed or canceled as healthcare resources were redirected to manage COVID-19 patients, resulting in temporary market contraction. Supply chain disruptions affected device manufacturing and distribution, while lockdowns and travel restrictions hindered clinical training and device demonstrations. However, the pandemic also accelerated certain trends, including the adoption of telemedicine for pre- and post-procedure consultations and the increased use of disposable devices to minimize infection risks. As healthcare systems recover, the market is experiencing a rebound driven by pent-up demand for deferred procedures and the resumption of regular screening and treatment protocols. The pandemic has also heightened awareness about the importance of maintaining healthcare infrastructure for neurological emergencies, potentially leading to increased investment in neurointerventional capabilities. Looking forward, the market is expected to return to its pre-pandemic growth trajectory, with some segments potentially experiencing accelerated growth due to lessons learned during the pandemic.

Neurointerventional Devices Market Competitive Landscape - Major competitors and market consolidation

The neurointerventional devices market features a competitive landscape characterized by both established medical device giants and specialized companies focusing exclusively on neurovascular interventions. Major players such as Medtronic, Boston Scientific, Stryker, and Johnson & Johnson dominate the market with comprehensive product portfolios spanning multiple device categories. These companies leverage their extensive research and development capabilities, global distribution networks, and strong brand recognition to maintain market leadership. The market also includes specialized companies like Penumbra, Terumo, and MicroPort Scientific Corporation, which have carved out significant market shares through innovative technologies and focused expertise in specific device segments. Recent years have witnessed strategic consolidation through mergers and acquisitions, as larger companies acquire innovative startups to expand their technological capabilities and market presence. This consolidation trend is expected to continue as companies seek to strengthen their competitive positions and capture emerging opportunities in the growing neurointerventional space. The competitive dynamics are further shaped by ongoing product innovations, regulatory approvals, and strategic partnerships aimed at expanding geographic reach and enhancing clinical outcomes.

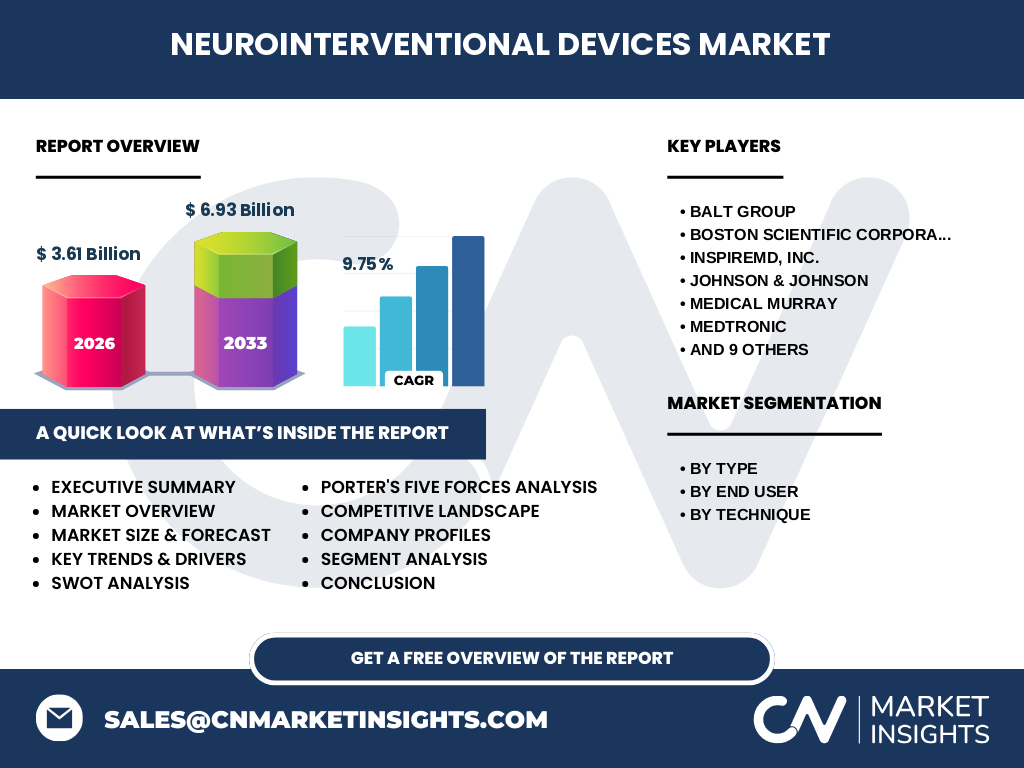

Executive Summary - High-level overview and key findings about Neurointerventional Devices Market

The neurointerventional devices market represents a dynamic and rapidly evolving sector within the medical device industry, characterized by technological innovation and increasing clinical adoption. With a market size of $3.61 billion in 2026 and projected growth to $6.93 billion by 2033, the market demonstrates robust expansion potential with a CAGR of 9.75%. The market encompasses a diverse range of devices categorized by type, including thrombectomy devices, stents, embolic protection devices, and various specialized tools for neurovascular interventions. Key growth drivers include the rising prevalence of neurological disorders, particularly among aging populations, technological advancements enabling less invasive procedures, and expanding healthcare infrastructure in emerging markets. The market serves multiple end-user segments, with hospitals representing the primary customer base, followed by ambulatory surgical centers. Geographically, the market exhibits varied growth patterns across regions, with developed markets maintaining technological leadership while emerging economies present significant growth opportunities. The competitive landscape features a mix of global medical device leaders and specialized neurointerventional companies, with ongoing consolidation through strategic acquisitions and partnerships shaping the industry structure.

Neurointerventional Devices Market Forecast - Projections for 2025-2032 period

The neurointerventional devices market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating a market value of $6.93 billion by 2033, up from $3.61 billion in 2026. This represents a compound annual growth rate of 9.75%, reflecting the market's robust expansion trajectory. The forecast period is expected to be characterized by several key developments, including the introduction of next-generation devices with enhanced capabilities, expanded indications for existing technologies, and increased adoption across emerging markets. The thrombectomy devices segment is anticipated to maintain strong growth momentum, driven by the increasing incidence of acute ischemic stroke and the proven efficacy of mechanical thrombectomy in clinical trials. Stenting and coiling procedures will continue to represent significant market segments, with innovations focusing on improved deliverability and reduced complications. The ambulatory surgical center segment is expected to witness accelerated growth as these facilities increasingly adopt neurointerventional capabilities. Regional growth will vary, with Asia-Pacific projected to exhibit the highest growth rates, followed by Latin America and the Middle East, while North America and Europe will maintain their positions as the largest market segments in absolute terms.

Neurointerventional Devices Market Size and Share by Segmentation - Breakdown by {segmentData}

The neurointerventional devices market exhibits a diverse segmentation structure across multiple dimensions, reflecting the varied applications and technologies within this specialized field. By device type, neurovascular thrombectomy devices currently represent a significant market share, driven by the growing incidence of acute ischemic stroke and the proven clinical benefits of mechanical thrombectomy. Neurovascular stents and embolic coils constitute substantial segments, with flow diverters emerging as a rapidly growing category due to their effectiveness in treating complex aneurysms. The market is also segmented by end-user, with hospitals accounting for the largest share due to their comprehensive neurointerventional capabilities and ability to handle complex cases. Ambulatory surgical centers represent an increasingly important segment as these facilities expand their neurointerventional offerings. By technique, neurothrombectomy procedures dominate the market, followed by stenting and coiling procedures, reflecting the prevalence of stroke and aneurysm treatments. Cerebral angiography remains a fundamental diagnostic and therapeutic technique, while flow disruption represents an evolving approach for treating challenging vascular malformations. This segmentation analysis highlights the market's complexity and the diverse opportunities across different device categories, clinical applications, and healthcare settings.

Global Neurointerventional Devices Market Size and Share by Region - Geographic distribution

The global neurointerventional devices market demonstrates distinct regional patterns in terms of market size, growth rates, and adoption dynamics. North America currently represents the largest regional market, driven by advanced healthcare infrastructure, high healthcare expenditure, favorable reimbursement policies, and early adoption of innovative technologies. The region benefits from a well-established ecosystem of device manufacturers, research institutions, and specialized neurointerventional centers. Europe follows as the second-largest market, characterized by strong technological capabilities and comprehensive regulatory frameworks, with countries like Germany, France, and the UK leading in adoption rates. The Asia-Pacific region is emerging as the fastest-growing market, fueled by expanding healthcare infrastructure, increasing healthcare spending, rising awareness about neurological disorders, and a large patient population. Countries such as China, Japan, and India are witnessing rapid market growth, supported by government initiatives to improve neurological care access. Latin America and the Middle East & Africa regions, while currently representing smaller market shares, are experiencing steady growth driven by improving healthcare systems and increasing investment in neurointerventional capabilities. The regional distribution reflects varying levels of market maturity, with developed regions focusing on advanced technologies and emerging markets prioritizing access to basic neurointerventional procedures.

Regional Analysis of the Neurointerventional Devices Market - Detailed regional market performance

Regional analysis of the neurointerventional devices market reveals distinct characteristics and growth dynamics across different geographical areas. In North America, the market benefits from a sophisticated healthcare ecosystem, with the United States leading in both adoption rates and technological innovation. The region's strong reimbursement environment, high prevalence of neurological disorders, and concentration of specialized neurovascular centers contribute to its market leadership. Europe demonstrates a mature market with well-established regulatory frameworks and high standards of care, particularly in Western European countries. The region is characterized by collaborative research initiatives and a strong emphasis on clinical evidence, driving the adoption of proven technologies. Asia-Pacific presents a dynamic growth landscape, with China and India emerging as key markets due to their large populations and improving healthcare infrastructure. Japan, with its aging population and advanced medical technology sector, represents a significant market with unique growth characteristics. Latin America shows steady market development, with Brazil and Mexico leading adoption, supported by increasing healthcare investments and growing awareness about advanced treatment options. The Middle East & Africa region, while currently representing a smaller market share, is experiencing gradual growth driven by healthcare modernization initiatives and increasing focus on specialized neurological care, particularly in Gulf Cooperation Council countries.

Leading Company Profiles in the Neurointerventional Devices Market - Industry players and strategies

The neurointerventional devices market features a diverse array of companies ranging from global medical device conglomerates to specialized neurovascular technology firms. Medtronic stands out as a market leader with a comprehensive portfolio spanning multiple device categories and a strong global presence. The company's strategy focuses on continuous innovation and strategic acquisitions to expand its technological capabilities. Stryker has established itself as a key player through its significant investments in mechanical thrombectomy technology, particularly following its acquisition of Covidien's neurovascular business. Boston Scientific leverages its extensive experience in interventional medicine to offer a broad range of neurointerventional solutions, with a strategy emphasizing clinical evidence and physician training. Terumo Corporation has built a strong position in the Japanese market and is expanding globally through strategic partnerships and product development. Penumbra has emerged as a specialized leader in mechanical thrombectomy, with a strategy centered on continuous innovation and a comprehensive stroke care ecosystem. Johnson & Johnson, through its DePuy Synthes division, offers a range of neurointerventional solutions with a focus on integrated care approaches. These companies, along with other notable players like MicroPort Scientific Corporation and BALT Group, shape the competitive landscape through their technological innovations, strategic partnerships, and global expansion initiatives.

Porter's Five Forces Analysis of the Neurointerventional Devices Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the neurointerventional devices market. The threat of new entrants remains moderate due to the high barriers to entry, including substantial R&D requirements, stringent regulatory approval processes, and the need for extensive clinical validation. However, the market does attract new players, particularly in emerging technologies and niche segments. The bargaining power of buyers, primarily hospitals and healthcare systems, is significant given their ability to negotiate on price and demand comprehensive clinical evidence. This power is somewhat mitigated by the specialized nature of neurointerventional devices and the critical importance of these technologies in treating life-threatening conditions. Suppliers of raw materials and components have moderate bargaining power, though this varies depending on the specific materials required for device manufacturing. The threat of substitute products exists but is limited, as neurointerventional procedures often represent the most effective treatment options for many neurological conditions. The intensity of competitive rivalry is high, characterized by numerous established players, continuous technological innovation, and strategic consolidation through mergers and acquisitions. This competitive environment drives ongoing product development and market expansion efforts as companies seek to differentiate their offerings and capture market share.

SWOT Analysis of the Neurointerventional Devices Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the neurointerventional devices market reveals key factors influencing its current position and future trajectory. Strengths of the market include continuous technological innovation leading to improved patient outcomes, a strong clinical evidence base supporting device efficacy, and the growing acceptance of minimally invasive procedures among both physicians and patients. The market also benefits from a well-established regulatory framework in developed regions and increasing healthcare expenditure globally. However, weaknesses exist in the form of high device and procedure costs, which can limit accessibility, particularly in emerging markets. The market also faces challenges related to the need for specialized training for healthcare professionals and the complexity of some procedures. Significant opportunities are emerging from the expanding applications of neurointerventional technologies, particularly in acute stroke treatment, and the growing healthcare infrastructure in developing regions. The increasing prevalence of neurological disorders globally presents a substantial market opportunity. Threats to the market include potential regulatory changes that could impact approval timelines and market access, reimbursement challenges in certain regions, and the ongoing risk of device-related complications that could affect market confidence. Additionally, economic uncertainties and healthcare budget constraints in some regions pose potential threats to market growth.

Neurointerventional Devices Market Value Chain Analysis - Industry structure and value flow

The neurointerventional devices market value chain encompasses a complex network of activities and stakeholders, from initial research and development through to end-user delivery and post-market support. The value chain begins with raw material suppliers providing specialized components and materials essential for device manufacturing, including biocompatible metals, polymers, and advanced coatings. Device manufacturers then transform these materials into sophisticated neurointerventional products through advanced engineering processes, quality control systems, and regulatory compliance measures. Research and development activities form a critical upstream component, driving innovation in device design, materials science, and clinical applications. Distribution channels, including direct sales forces and specialized medical distributors, facilitate the movement of devices from manufacturers to healthcare providers. Healthcare providers, primarily hospitals and specialized neurovascular centers, represent the key customers who integrate these devices into their clinical practices. End-users, including interventional neurologists, neurosurgeons, and neuroradiologists, utilize these devices in treating patients with neurological conditions. Post-market surveillance and support activities ensure ongoing product safety and effectiveness, while clinical education and training programs help disseminate knowledge about optimal device utilization. This value chain structure highlights the collaborative nature of the neurointerventional ecosystem and the multiple touchpoints where value is created and delivered to patients.

Key Investment Insights in the Neurointerventional Devices Market - Strategic investment recommendations

The neurointerventional devices market presents compelling investment opportunities driven by strong growth projections, technological innovation, and expanding clinical applications. Strategic investments should focus on companies demonstrating robust R&D capabilities and a track record of successful product launches, particularly in high-growth segments such as mechanical thrombectomy devices and flow diverters. The market's strong growth trajectory, with a projected CAGR of 9.75% through 2033, suggests that investments in established players with comprehensive product portfolios could yield substantial returns. However, the market also offers opportunities for investments in innovative startups developing next-generation technologies, particularly those addressing unmet clinical needs or improving upon existing solutions. Geographic diversification represents another strategic consideration, with emerging markets in Asia-Pacific and Latin America offering significant growth potential as healthcare infrastructure improves and awareness increases. Investors should also consider the impact of regulatory trends and reimbursement landscapes on market dynamics, as these factors can significantly influence company performance. Additionally, investments in companies with strong intellectual property portfolios and strategic partnerships may provide competitive advantages in this rapidly evolving market. The increasing focus on acute stroke treatment and the growing adoption of neurointerventional procedures in ambulatory surgical centers represent specific areas warranting investment attention.

Neurointerventional Devices Market Conclusion - Summary and key takeaways

The neurointerventional devices market represents a dynamic and rapidly growing sector within the medical device industry, characterized by technological innovation, expanding clinical applications, and strong growth projections. With a market size of $3.61 billion in 2026 and expected to reach $6.93 billion by 2033, the market demonstrates robust expansion potential driven by the increasing prevalence of neurological disorders, particularly among aging populations, and the proven clinical benefits of minimally invasive neurointerventional procedures. The market encompasses a diverse range of devices and techniques, with thrombectomy devices, stents, and coiling procedures representing key segments. While North America currently leads the market, significant growth opportunities exist in emerging regions, particularly Asia-Pacific. The competitive landscape features a mix of global medical device leaders and specialized companies, with ongoing consolidation through strategic acquisitions shaping the industry structure. Despite challenges related to high costs and regulatory complexities, the market's strong fundamentals and continuous innovation suggest a positive long-term outlook. Key investment opportunities exist across established players, innovative startups, and emerging markets, with particular emphasis on technologies addressing acute stroke treatment and expanding applications in ambulatory surgical centers.

Research Methodology - How this research was conducted

The research methodology employed for this neurointerventional devices market analysis combines comprehensive primary and secondary research approaches to ensure accurate and reliable findings. Primary research involved extensive interviews with industry experts, including medical device manufacturers, healthcare providers, regulatory authorities, and academic researchers, to gather firsthand insights into market dynamics, technological trends, and clinical applications. Secondary research encompassed a thorough review of industry reports, scientific publications, company financial statements, regulatory databases, and market intelligence sources to validate and supplement primary findings. The analysis incorporated both top-down and bottom-up approaches to estimate market size and growth projections, triangulating data from multiple sources to ensure accuracy. Market segmentation was conducted based on device types, end-users, techniques, and geographic regions, with each segment analyzed for its contribution to overall market dynamics. The research also included competitive analysis through company profiling, patent analysis, and assessment of recent developments in the industry. Data validation processes were implemented throughout the research cycle, including cross-verification of findings with multiple sources and expert review of key conclusions. This rigorous methodology ensures that the market insights presented are based on credible data and comprehensive analysis.

Research Scope - Coverage and limitations

The research scope for this neurointerventional devices market analysis encompasses a comprehensive examination of the global market, including detailed segmentation by device type, end-user, technique, and geographic region. The study covers the period from 2026 to 2033, with specific focus on market size, growth trends, competitive landscape, and key industry developments. The analysis includes all major device categories such as neurovascular thrombectomy devices, stents, embolic protection devices, intrasaccular devices, embolic coils, flow diverters, liquid embolics, balloons, and stent retrievers. End-user segments covered include hospitals and ambulatory surgical centers, while techniques analyzed encompass neurothrombectomy, stenting, coiling procedures, cerebral angiography, and flow disruption. The geographic scope spans North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed regional analysis for each area. Limitations of the research include potential variations in data availability across different regions and the inherent challenges in forecasting long-term market trends in a rapidly evolving technological landscape. The study also acknowledges that market dynamics may be influenced by unforeseen factors such as regulatory changes, economic conditions, and emerging technologies not currently accounted for in the analysis. Despite these limitations, the research provides a comprehensive overview of the market based on available data and expert insights.

Key Companies and Recent Developments in the Neurointerventional Devices Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The neurointerventional devices market features several key companies that are driving innovation and shaping the industry through their technological advancements and strategic initiatives. Medtronic continues to strengthen its market position through continuous product development and strategic acquisitions, most recently expanding its flow diversion portfolio with innovative solutions for complex aneurysm treatments. Stryker has made significant strides in mechanical thrombectomy technology, with recent announcements focusing on next-generation devices offering improved navigability and clot retrieval efficiency. Boston Scientific has been actively expanding its neurovascular offerings through both internal development and strategic partnerships, with recent product launches emphasizing enhanced visualization and precision in neurointerventional procedures. Terumo Corporation has strengthened its presence in the Japanese market while expanding globally, with recent developments including advanced liquid embolic systems and innovative flow diverter technologies. Penumbra has maintained its leadership in mechanical thrombectomy through continuous innovation, recently announcing expanded indications for its flagship devices and introducing new technologies for comprehensive stroke care. Johnson & Johnson, through its DePuy Synthes division, has been focusing on integrated care solutions, with recent developments including advanced embolic protection devices and next-generation neurovascular stents. These companies, along with other notable players like MicroPort Scientific Corporation and BALT Group, continue to shape the market through their technological innovations, strategic partnerships, and global expansion initiatives, reflecting the dynamic nature of the neurointerventional devices industry.