Branded Generics Market Overview - Definition, scope, and significance

Branded generics represent a unique segment within the pharmaceutical industry, combining the cost-effectiveness of generic medications with the brand recognition and marketing strategies typically associated with innovator drugs. These products are essentially generic versions of off-patent medications that are marketed under a brand name, distinguishing them from unbranded generics that are sold under their chemical names. The branded generics market occupies a strategic position in the pharmaceutical landscape, offering healthcare providers and patients a middle ground between expensive branded innovator drugs and basic unbranded generics. This market segment has gained significant traction globally, particularly in emerging economies where brand trust and quality assurance play crucial roles in medication selection. The significance of branded generics extends beyond mere cost savings, as they often provide enhanced formulations, improved delivery systems, and additional therapeutic benefits while maintaining the bioequivalence standards required of all generic medications.

Branded Generics Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The branded generics market is propelled by several key drivers, including increasing healthcare costs worldwide, growing demand for affordable medications, and the expiration of numerous drug patents. The rising prevalence of chronic diseases and aging populations in both developed and developing nations creates sustained demand for cost-effective treatment options. Additionally, the expanding middle class in emerging markets, coupled with improving healthcare infrastructure, presents significant growth opportunities. However, the market faces several restraints, including stringent regulatory requirements for bioequivalence and quality standards, intense competition from both branded and unbranded generics, and pricing pressures from healthcare systems and insurance providers. Challenges include maintaining brand differentiation in a crowded marketplace, navigating complex patent landscapes, and addressing concerns about medication adherence and patient education. Opportunities exist in developing innovative formulations, expanding into underserved therapeutic areas, leveraging digital health technologies for patient engagement, and exploring strategic partnerships for market expansion.

Branded Generics Market Growth Trends - Current and emerging trends shaping the market

The branded generics market is experiencing several transformative trends that are reshaping the competitive landscape. One prominent trend is the increasing focus on combination therapies and fixed-dose combinations, which offer enhanced therapeutic benefits and improved patient compliance. Another significant trend is the growing emphasis on value-added services, such as patient support programs, adherence monitoring, and digital health integration, which differentiate branded generics from their unbranded counterparts. The market is also witnessing a shift towards personalized medicine approaches, with manufacturers developing branded generics tailored to specific patient populations or genetic profiles. Additionally, there is a rising trend of vertical integration, with pharmaceutical companies expanding their presence across the value chain from manufacturing to distribution. The adoption of advanced manufacturing technologies, such as continuous manufacturing and 3D printing, is enabling the production of more sophisticated and customized branded generic formulations. Furthermore, the increasing focus on sustainability and environmental responsibility is driving the development of eco-friendly packaging and manufacturing processes in the branded generics sector.

COVID-19 Impact on the Branded Generics Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the branded generics market, presenting both challenges and opportunities for industry stakeholders. During the initial phases of the pandemic, supply chain disruptions and manufacturing delays affected the production and distribution of many pharmaceutical products, including branded generics. However, the crisis also highlighted the critical importance of affordable and accessible medications, leading to increased demand for branded generics as healthcare systems sought cost-effective treatment options. The pandemic accelerated the adoption of digital health technologies and telemedicine, creating new avenues for patient engagement and medication adherence support for branded generic products. Additionally, the focus on respiratory health and immune system support during the pandemic opened up new therapeutic areas for branded generic manufacturers. As the world recovers from the pandemic, the branded generics market is expected to benefit from the lessons learned, with increased emphasis on supply chain resilience, digital integration, and the development of treatments for emerging health challenges.

Branded Generics Market Competitive Landscape - Major competitors and market consolidation

The branded generics market is characterized by a highly competitive landscape, with a mix of large multinational pharmaceutical companies, specialized generic manufacturers, and regional players vying for market share. The market has witnessed significant consolidation in recent years, with major acquisitions and mergers reshaping the competitive dynamics. Large pharmaceutical companies are increasingly focusing on their branded generic portfolios as a strategy to maintain revenue streams following patent expirations of their blockbuster drugs. This has led to intense competition in key therapeutic areas and geographic markets. The competitive landscape is further complicated by the presence of local and regional manufacturers who often have a strong foothold in their respective markets, particularly in emerging economies. Companies are differentiating themselves through various strategies, including the development of innovative formulations, expansion into niche therapeutic areas, and the provision of value-added services. The market also sees competition from unbranded generics, which offer lower prices but lack the brand recognition and additional services provided by branded generics.

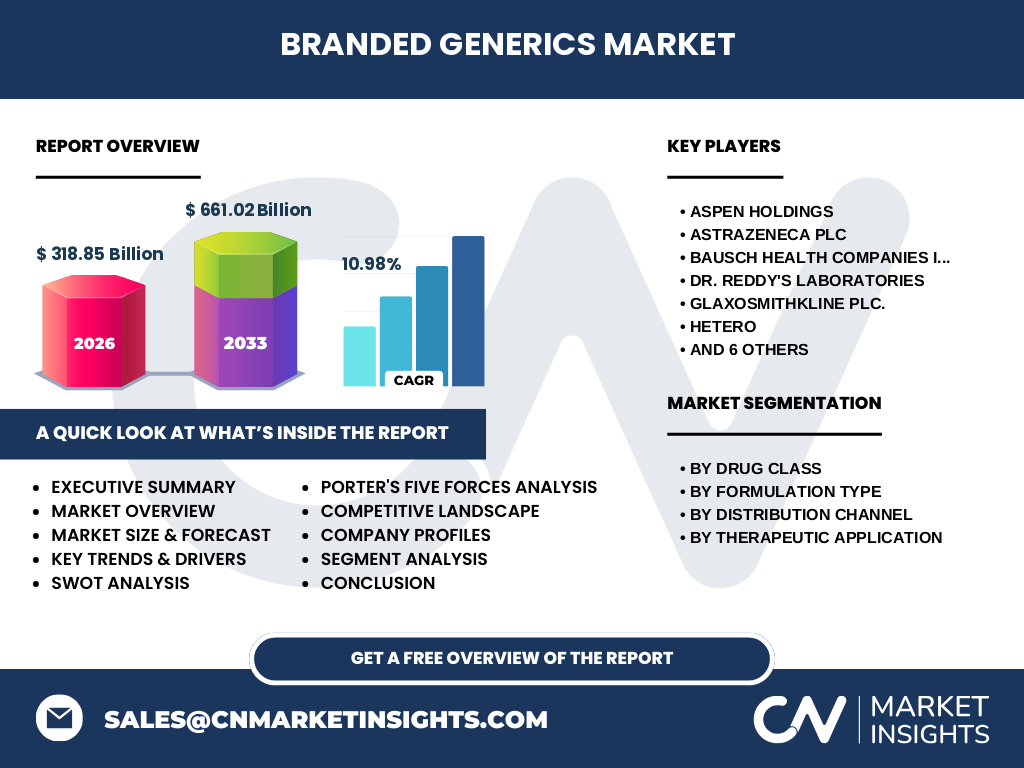

Executive Summary - High-level overview and key findings about Branded Generics Market

The branded generics market represents a dynamic and rapidly evolving segment of the pharmaceutical industry, offering a unique value proposition that combines the affordability of generic medications with the brand recognition and additional services typically associated with innovator drugs. With a market size of 318.85 Billion in 2026 and a projected growth to 661.02 Billion by 2033, representing a CAGR of 10.98%, the market demonstrates robust expansion potential. This growth is driven by factors such as increasing healthcare costs, patent expirations, and the rising prevalence of chronic diseases globally. The market is characterized by diverse segmentation across drug classes, formulation types, distribution channels, and therapeutic applications, catering to a wide range of healthcare needs. Key therapeutic areas include oncology, cardiovascular diseases, and diabetes, reflecting the global burden of these conditions. The competitive landscape is marked by both consolidation among major players and the presence of specialized manufacturers, creating a complex ecosystem of innovation and market dynamics. As the market continues to evolve, it presents significant opportunities for investment and growth, particularly in emerging markets and through the development of innovative formulations and value-added services.

Branded Generics Market Forecast - Projections for 2025-2032 period

The branded generics market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating a market size of 661.02 Billion by 2033, up from 318.85 Billion in 2026. This represents a compound annual growth rate (CAGR) of 10.98%, reflecting the strong momentum and potential of the market. The forecast period is expected to be characterized by several key trends and developments that will shape the market's trajectory. These include the continued expiration of blockbuster drug patents, driving the development of new branded generic products; increasing demand from emerging markets as healthcare infrastructure improves and middle-class populations expand; and the growing focus on complex generics and biosimilars, which offer higher value propositions. The market is also likely to see increased investment in research and development, particularly in areas such as combination therapies and personalized medicine approaches. Additionally, the integration of digital health technologies and the expansion of value-added services are expected to play a significant role in driving market growth and differentiation among competitors.

Branded Generics Market Size and Share by Segmentation - Breakdown by {segmentData}

The branded generics market exhibits a complex segmentation structure, reflecting the diverse needs of patients and healthcare systems across different therapeutic areas and geographies. By drug class, the market encompasses a wide range of therapeutic categories, including Alkylating Agents, Antimetabolites, Hormones, Antihypertensive, Lipid-Lowering Drugs, Antidepressants, Antipsychotics, and Antiepileptic medications. Each of these segments presents unique growth opportunities and challenges, with some experiencing faster growth due to factors such as aging populations or increasing disease prevalence. In terms of formulation type, the market is divided into Oral, Parenteral, and Topical formulations, each catering to different patient needs and administration preferences. The distribution channel segmentation includes Hospitals, Retail Pharmacies, Online Pharmacies, and Drug Stores, reflecting the evolving landscape of pharmaceutical distribution and the growing importance of digital platforms. The therapeutic application segmentation covers major disease areas such as Oncology, Cardiovascular Diseases, Diabetes, Neurology, Gastrointestinal Diseases, Dermatology Diseases, and Analgesics & Anti-Inflammatory treatments, highlighting the broad scope of the branded generics market in addressing diverse healthcare needs.

Global Branded Generics Market Size and Share by Region - Geographic distribution

The global branded generics market exhibits significant regional variations in terms of market size, growth rates, and competitive dynamics. While specific regional market share data is not provided, it is evident that the market is influenced by factors such as healthcare infrastructure, regulatory environments, economic development, and disease prevalence across different regions. Developed markets, such as North America and Europe, continue to be major contributors to the global branded generics market, driven by high healthcare expenditure, advanced regulatory frameworks, and a strong emphasis on cost containment in healthcare systems. However, emerging markets, particularly in Asia-Pacific, Latin America, and Africa, are experiencing rapid growth in the branded generics sector. This growth is fueled by factors such as expanding middle-class populations, improving healthcare infrastructure, and increasing awareness of the benefits of branded generics. The Asia-Pacific region, in particular, is expected to witness significant growth due to the large patient populations, rising healthcare expenditure, and the presence of major generic manufacturing hubs in countries like India and China. The regional dynamics of the branded generics market are further influenced by local regulatory policies, patent laws, and the strategies of multinational pharmaceutical companies in establishing a presence in these markets.

Regional Analysis of the Branded Generics Market - Detailed regional market performance

The branded generics market demonstrates distinct regional characteristics and performance metrics across different geographic areas. In North America, the market is characterized by a mature pharmaceutical industry, stringent regulatory frameworks, and a strong emphasis on cost containment in healthcare systems. The region benefits from advanced healthcare infrastructure and high levels of generic drug utilization, driving demand for branded generics that offer additional value propositions. Europe presents a diverse landscape, with varying market dynamics across different countries. The region is marked by a strong focus on biosimilars and complex generics, driven by patent expirations and healthcare cost pressures. The Asia-Pacific region emerges as a high-growth market for branded generics, fueled by large patient populations, rising healthcare expenditure, and the presence of major generic manufacturing hubs. Countries like India and China are particularly significant, with their large domestic markets and growing export capabilities. Latin America and the Middle East & Africa regions show promising growth potential, driven by improving healthcare infrastructure, expanding middle-class populations, and increasing awareness of the benefits of branded generics. These regions also present opportunities for market expansion due to their large underserved populations and growing healthcare needs.

Leading Company Profiles in the Branded Generics Market - Industry players and strategies

The branded generics market is dominated by a mix of large multinational pharmaceutical companies and specialized generic manufacturers, each employing distinct strategies to capture market share and drive growth. Major players in the market include Aspen Holdings, AstraZeneca PLC, Bausch Health Companies Inc., Dr. Reddy's Laboratories, GlaxoSmithKline plc., Hetero, Lupin, Mylan N.V, Par Pharmaceuticals, INC, Sandoz International GMBH, Sanofi, and Teva Pharmaceutical Industries Ltd. These companies have established strong market positions through various strategies, including extensive product portfolios, global distribution networks, and significant investments in research and development. Many of these players focus on developing innovative formulations and value-added services to differentiate their branded generic offerings from unbranded alternatives. Additionally, these companies often engage in strategic partnerships, mergers, and acquisitions to expand their market presence and enhance their product pipelines. The competitive strategies of these leading companies are characterized by a balance between cost leadership in generic production and differentiation through branding, quality assurance, and patient support services.

Porter's Five Forces Analysis of the Branded Generics Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the branded generics market. The threat of new entrants in the market is moderate to high, particularly in emerging markets where regulatory barriers may be lower and manufacturing capabilities are developing. However, established players benefit from economies of scale, strong brand recognition, and extensive distribution networks, which create significant barriers to entry. The bargaining power of buyers, including healthcare providers and insurance companies, is relatively high due to the commoditized nature of many generic products and the emphasis on cost containment in healthcare systems. This pressure often leads to price negotiations and the demand for additional value-added services. The bargaining power of suppliers, primarily raw material manufacturers, is moderate, with some suppliers holding significant positions in the supply chain. The threat of substitute products, including unbranded generics and alternative therapies, is high, necessitating continuous innovation and differentiation by branded generic manufacturers. Competitive rivalry within the market is intense, driven by the presence of numerous players, price competition, and the constant pressure to develop new products and expand into emerging markets.

SWOT Analysis of the Branded Generics Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the branded generics market reveals a complex landscape of strengths, weaknesses, opportunities, and threats. The market's key strengths include the ability to offer cost-effective alternatives to expensive branded drugs, the potential for high-volume sales due to widespread disease prevalence, and the flexibility to develop innovative formulations and delivery systems. Additionally, the established regulatory frameworks for generic drugs provide a level of market stability and predictability. However, the market also faces several weaknesses, including intense price competition, the challenge of maintaining brand differentiation in a crowded marketplace, and the potential for quality concerns that can impact the entire generic sector. Opportunities in the market are abundant, including the expansion into emerging markets with growing healthcare needs, the development of complex generics and biosimilars, and the integration of digital health technologies to enhance patient engagement and adherence. Threats to the market include increasing regulatory scrutiny, potential changes in patent laws that could affect market exclusivity, and the risk of supply chain disruptions. Additionally, the market faces challenges from the growing trend of personalized medicine, which may reduce the applicability of traditional generic approaches.

Branded Generics Market Value Chain Analysis - Industry structure and value flow

The value chain of the branded generics market encompasses a complex network of activities and stakeholders, from drug discovery and development to manufacturing, distribution, and patient access. The primary activities in the value chain include research and development, where companies focus on developing bioequivalent formulations and innovative delivery systems; manufacturing, which involves large-scale production of generic drugs with stringent quality control measures; marketing and sales, where companies differentiate their products through branding and value-added services; and distribution, which ensures the efficient delivery of products to various healthcare settings. Support activities in the value chain include procurement of raw materials, technology development for manufacturing processes, human resource management, and infrastructure development. The value chain is characterized by significant outsourcing, particularly in manufacturing and research activities, allowing companies to focus on their core competencies and reduce costs. The integration of digital technologies throughout the value chain is becoming increasingly important, enabling better supply chain management, improved patient engagement, and enhanced data analytics for market insights.

Key Investment Insights in the Branded Generics Market - Strategic investment recommendations

The branded generics market presents numerous investment opportunities across various segments and geographies, driven by the market's strong growth trajectory and evolving dynamics. Key investment insights suggest focusing on emerging markets, particularly in Asia-Pacific and Latin America, where rapid urbanization, expanding middle-class populations, and improving healthcare infrastructure create significant growth potential. Investments in research and development, particularly in complex generics, biosimilars, and innovative delivery systems, are likely to yield high returns as these areas offer opportunities for differentiation and premium pricing. The integration of digital health technologies and patient support services represents another attractive investment area, as these elements become increasingly important in driving brand loyalty and improving patient outcomes. Strategic acquisitions and partnerships can provide access to new markets, technologies, and product pipelines, offering a faster route to market expansion compared to organic growth. Additionally, investments in sustainable manufacturing practices and eco-friendly packaging align with growing environmental concerns and regulatory trends, potentially offering long-term competitive advantages.

Branded Generics Market Conclusion - Summary and key takeaways

The branded generics market represents a dynamic and rapidly evolving segment of the pharmaceutical industry, offering a unique value proposition that combines the affordability of generic medications with the brand recognition and additional services typically associated with innovator drugs. With a projected market size of 661.02 Billion by 2033 and a CAGR of 10.98%, the market demonstrates robust growth potential driven by factors such as increasing healthcare costs, patent expirations, and the rising prevalence of chronic diseases globally. The market is characterized by diverse segmentation across drug classes, formulation types, distribution channels, and therapeutic applications, catering to a wide range of healthcare needs. Key therapeutic areas include oncology, cardiovascular diseases, and diabetes, reflecting the global burden of these conditions. The competitive landscape is marked by both consolidation among major players and the presence of specialized manufacturers, creating a complex ecosystem of innovation and market dynamics. As the market continues to evolve, it presents significant opportunities for investment and growth, particularly in emerging markets and through the development of innovative formulations and value-added services. The future of the branded generics market will likely be shaped by advancements in personalized medicine, the integration of digital health technologies, and the increasing focus on sustainability and environmental responsibility.

Research Methodology - How this research was conducted

The research methodology employed for this branded generics market analysis combines both primary and secondary research approaches to ensure comprehensive and accurate insights. Primary research involved extensive interviews with industry experts, including pharmaceutical company executives, regulatory affairs specialists, and healthcare providers, to gather firsthand information on market trends, competitive dynamics, and future outlook. Secondary research encompassed a thorough review of industry reports, company financial statements, regulatory filings, and scientific publications to validate and supplement the primary data. Market size and growth projections were derived using a combination of top-down and bottom-up approaches, considering factors such as disease prevalence, treatment patterns, and pricing dynamics across different regions and therapeutic areas. The segmentation analysis was conducted based on detailed examination of product portfolios, distribution channels, and therapeutic applications, supported by data from industry databases and market intelligence platforms. Competitive landscape analysis involved assessing company profiles, product offerings, and strategic initiatives of key market players. The research also incorporated an analysis of macroeconomic factors, regulatory environments, and technological advancements to provide a holistic view of the market dynamics.

Research Scope - Coverage and limitations

The research scope for this branded generics market analysis encompasses a comprehensive examination of the global market, covering key segments such as drug classes, formulation types, distribution channels, and therapeutic applications. The study focuses on major geographic regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, providing insights into regional market dynamics and growth opportunities. The analysis includes a detailed examination of leading companies in the branded generics market, their product portfolios, strategic initiatives, and competitive positioning. The research also explores key trends shaping the market, including technological advancements, regulatory changes, and evolving patient needs. However, it is important to note certain limitations in the research scope. The analysis primarily focuses on branded generics as a distinct category within the broader generic pharmaceutical market, and does not extensively cover unbranded generics or innovator drugs. Additionally, while the research provides insights into market size and growth projections, specific regional market share data and detailed financial metrics for individual companies are not included in this overview. The study also does not delve into granular patent expiration data or specific pricing information for individual products, which may be available in more specialized reports or through direct engagement with industry stakeholders.

Key Companies and Recent Developments in the Branded Generics Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The branded generics market is characterized by the presence of several major pharmaceutical companies, each contributing to the market's growth through innovative products, strategic partnerships, and expansion initiatives. Key players in the market include Aspen Holdings, AstraZeneca PLC, Bausch Health Companies Inc., Dr. Reddy's Laboratories, GlaxoSmithKline plc., Hetero, Lupin, Mylan N.V, Par Pharmaceuticals, INC, Sandoz International GMBH, Sanofi, and Teva Pharmaceutical Industries Ltd. These companies have been actively involved in recent developments that are shaping the market landscape. For instance, many of these players have focused on expanding their presence in emerging markets, recognizing the significant growth potential in regions such as Asia-Pacific and Latin America. Strategic partnerships and collaborations have been a common theme, with companies joining forces to enhance their product portfolios, improve manufacturing capabilities, and strengthen distribution networks. Several companies have also invested in the development of complex generics and biosimilars, recognizing the higher value propositions these products offer. Additionally, there has been a growing emphasis on digital health integration and patient support programs, with companies leveraging technology to improve medication adherence and patient outcomes. While specific recent announcements and product launches are not detailed in this overview, it is evident that the leading companies in the branded generics market are continuously innovating and adapting their strategies to maintain competitive advantages and capitalize on emerging opportunities in the global pharmaceutical landscape.