Automotive Infotainment SoC Market Overview - Definition, scope, and significance

System-on-Chip (SoC) technology for automotive infotainment represents a critical advancement in vehicle electronics, integrating multiple functions into a single semiconductor platform. These specialized chips combine processing power, graphics capabilities, audio processing, connectivity features, and control systems into compact integrated circuits designed specifically for automotive applications. The automotive infotainment SoC market encompasses the development, manufacturing, and deployment of these sophisticated semiconductor solutions that power modern vehicle entertainment, navigation, communication, and information systems. This market segment is significant because it serves as the technological backbone for connected vehicles, enabling advanced driver interfaces, real-time navigation, multimedia streaming, vehicle diagnostics, and integration with smartphones and other devices. As vehicles become increasingly software-defined and connected, automotive infotainment SoCs play a pivotal role in delivering the computing power and functionality required for next-generation mobility experiences while meeting stringent automotive quality, reliability, and safety standards.

Automotive Infotainment SoC Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The automotive infotainment SoC market is driven by several powerful forces including the rapid adoption of connected vehicles, increasing consumer demand for advanced in-car entertainment and information systems, and the automotive industry's shift toward electric and autonomous vehicles. Growing consumer expectations for smartphone-like experiences in vehicles, coupled with regulatory requirements for advanced driver assistance systems (ADAS), creates substantial demand for more powerful and capable SoCs. However, the market faces significant restraints including high development costs, complex certification requirements for automotive applications, and supply chain vulnerabilities that became particularly evident during recent global disruptions. Major challenges include managing thermal constraints in increasingly compact vehicle designs, ensuring cybersecurity for connected systems, and maintaining long-term supply commitments required by automotive manufacturers. Despite these obstacles, substantial opportunities exist in emerging markets, particularly in developing regions where vehicle ownership is expanding rapidly, and in the growing commercial vehicle segment where fleet management and telematics applications are driving SoC adoption. The transition toward software-defined vehicles also presents opportunities for over-the-air update capabilities and continuous feature enhancement through SoC platforms.

Automotive Infotainment SoC Market Growth Trends - Current and emerging trends shaping the market

The automotive infotainment SoC market is experiencing transformative growth trends driven by technological convergence and changing consumer expectations. One prominent trend is the integration of artificial intelligence and machine learning capabilities directly into SoC architectures, enabling advanced voice recognition, personalized user experiences, and predictive maintenance features. Another significant trend is the shift toward centralized computing architectures where multiple vehicle functions consolidate onto fewer, more powerful SoCs rather than distributed systems. The market is also witnessing increased adoption of 5G connectivity integration within SoCs, enabling real-time cloud services, high-bandwidth streaming, and vehicle-to-everything (V2X) communication. Additionally, there is growing emphasis on cybersecurity features embedded directly into SoC designs to protect against increasingly sophisticated threats to connected vehicles. The rise of digital cockpits and e-cockpit platforms represents another major trend, where single SoCs power multiple displays and control interfaces throughout the vehicle. Furthermore, the market is seeing increased demand for SoCs supporting augmented reality head-up displays and advanced graphics processing for immersive in-vehicle experiences. These trends collectively point toward a future where automotive SoCs become even more powerful, integrated, and central to the overall vehicle architecture.

COVID-19 Impact on the Automotive Infotainment SoC Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly disrupted the automotive infotainment SoC market through multiple channels, creating both immediate challenges and longer-term shifts in market dynamics. During the height of the pandemic, global lockdowns and supply chain interruptions caused severe semiconductor shortages that particularly impacted automotive production, with many manufacturers forced to idle production lines due to insufficient SoC availability. This disruption exposed vulnerabilities in the automotive semiconductor supply chain and accelerated discussions about regional semiconductor manufacturing capabilities and supply chain resilience. Consumer demand for vehicles initially declined sharply during lockdowns but subsequently rebounded strongly, particularly for vehicles with advanced connectivity features as consumers placed greater value on in-car technology for comfort and productivity. The pandemic also accelerated digital transformation trends in the automotive industry, with increased emphasis on over-the-air update capabilities and remote vehicle monitoring features that rely heavily on advanced SoCs. As the market recovers, manufacturers are implementing more robust supply chain strategies, including dual sourcing and increased inventory buffers, while continuing to invest in next-generation SoC technologies to meet evolving consumer expectations for connected and intelligent vehicles.

Automotive Infotainment SoC Market Competitive Landscape - Major competitors and market consolidation

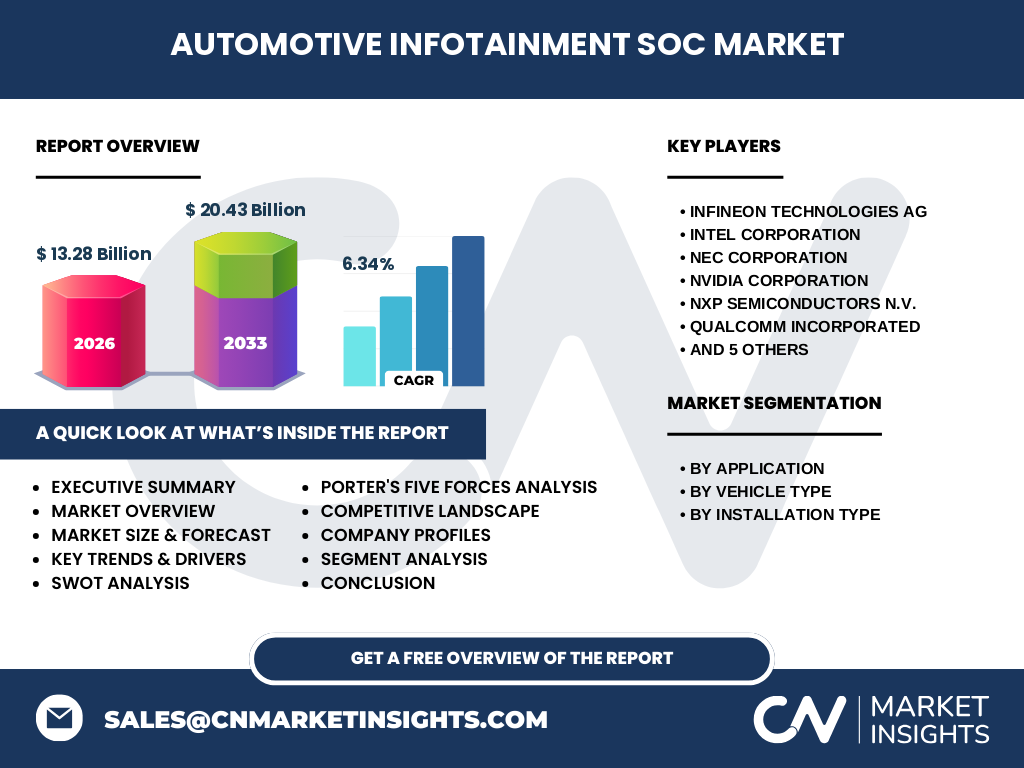

The automotive infotainment SoC market features a competitive landscape characterized by both established semiconductor giants and specialized automotive electronics companies vying for market share in this strategically important segment. Major competitors include Infineon Technologies AG, Intel Corporation, NEC Corporation, NVIDIA Corporation, NXP Semiconductors N.V., Qualcomm Incorporated, Renesas Electronics Corporation, STMicroelectronics N.V., Semiconductor Components Industries (On Semiconductor), Telechips, Inc., and Texas Instruments Incorporated. The competitive dynamics are shaped by significant barriers to entry including the need for automotive-grade certification, long development cycles, and the requirement for extensive testing and validation to meet automotive reliability standards. Market consolidation is evident through strategic partnerships, acquisitions, and collaborative development efforts as companies seek to combine their strengths in areas such as AI processing, connectivity, and automotive expertise. The competitive landscape is further influenced by the growing importance of software capabilities, with companies increasingly focusing on developing comprehensive software ecosystems alongside their hardware offerings. Differentiation strategies include specialization in specific vehicle segments, development of proprietary AI accelerators, and integration of advanced security features. The market also sees competition from integrated solutions provided by Tier-1 automotive suppliers who are increasingly developing their own SoC capabilities to maintain control over the complete user experience.

Executive Summary - High-level overview and key findings about Automotive Infotainment SoC Market

The automotive infotainment SoC market represents a dynamic and rapidly evolving segment of the automotive electronics industry, driven by technological advancement and changing consumer expectations. The market is experiencing robust growth, with the market size projected to increase from 13.28 Billion to 20.43 Billion during the forecast period, representing a compound annual growth rate of 6.34%. This growth is fueled by the automotive industry's transformation toward connected, autonomous, and software-defined vehicles that require increasingly sophisticated computing platforms. Key findings indicate that the market is characterized by strong demand across multiple vehicle segments, with passenger vehicles representing the largest application area while commercial vehicles show the fastest growth rates. The market segmentation reveals distinct opportunities across different applications including head units, e-cockpit systems, and sound systems, as well as varying installation types such as in-dash and rear seat configurations. The competitive landscape is dominated by established semiconductor companies with deep automotive expertise, though new entrants with specialized capabilities are increasingly challenging traditional players. Regional analysis shows varying adoption rates and growth patterns, with developed markets leading in technology adoption while emerging markets present significant growth opportunities. Overall, the market demonstrates strong fundamentals with multiple growth drivers, though challenges related to supply chain resilience and technological complexity must be addressed to sustain long-term growth.

Automotive Infotainment SoC Market Forecast - Projections for 2025-2032 period

The automotive infotainment SoC market is projected to experience steady growth throughout the 2025-2032 period, with the market expanding from 13.28 Billion to 20.43 Billion, representing a compound annual growth rate of 6.34%. This forecast reflects the continued transformation of the automotive industry toward more connected and intelligent vehicles that require increasingly powerful semiconductor solutions. The projection period is expected to be characterized by several key trends that will shape market dynamics, including the widespread adoption of software-defined vehicle architectures, increased integration of AI and machine learning capabilities, and the transition toward centralized computing platforms. Growth will be particularly strong in emerging markets where vehicle ownership is expanding rapidly and consumers are demanding advanced connectivity features. The commercial vehicle segment is expected to show accelerated growth rates compared to passenger vehicles, driven by fleet management applications and regulatory requirements for connected commercial vehicles. Regional variations in growth rates will reflect differences in vehicle production volumes, technology adoption rates, and economic conditions, with Asia-Pacific markets likely showing the strongest growth while North America and Europe maintain leadership in technology innovation. The forecast also accounts for potential market disruptions from emerging technologies such as solid-state batteries and new mobility paradigms that could influence SoC requirements and adoption patterns.

Automotive Infotainment SoC Market Size and Share by Segmentation - Breakdown by {segmentData}

The automotive infotainment SoC market demonstrates distinct segmentation patterns across multiple dimensions that reveal important insights about market structure and growth opportunities. By application, the market segments into head unit, e-cockpit, and sound system categories, with head units traditionally representing the largest segment due to their central role in vehicle infotainment systems, while e-cockpit solutions show the fastest growth as vehicles adopt integrated digital cockpit architectures. By vehicle type, the market divides into passenger vehicles and commercial vehicles, with passenger vehicles accounting for the majority of volume due to higher production numbers and consumer demand for advanced features, though commercial vehicles are experiencing rapid growth driven by fleet management and telematics applications. By installation type, the market segments into in-dash and rear seat configurations, with in-dash installations dominating due to their primary role in driver interaction, while rear seat entertainment systems are growing in premium and family vehicles. These segmentation patterns highlight the diverse nature of the market and indicate that different strategies may be required to address various segments effectively. The segmentation also reveals that growth opportunities exist across all segments, though the rate and nature of growth vary significantly depending on the specific application, vehicle type, and installation configuration.

Global Automotive Infotainment SoC Market Size and Share by Region - Geographic distribution

The global automotive infotainment SoC market exhibits significant regional variations in market size, growth rates, and technology adoption patterns, reflecting differences in vehicle production volumes, consumer preferences, and economic conditions across geographic regions. While specific regional market share data is not provided in the available information, general patterns can be observed based on global automotive industry trends. Asia-Pacific represents a substantial portion of the global market, driven by high vehicle production volumes in countries like China, Japan, and South Korea, along with rapidly growing consumer demand for connected vehicle features. China, in particular, shows strong growth potential due to government support for electric vehicles and connected mobility solutions. North America maintains a significant market presence characterized by early adoption of advanced technologies and strong demand for premium vehicle features, with the United States leading in technology innovation and integration. Europe represents another major market region, distinguished by stringent regulatory requirements for vehicle connectivity and safety features, along with strong demand for luxury vehicles with advanced infotainment systems. Other regions including Latin America, the Middle East, and Africa show emerging market potential with varying growth rates depending on economic conditions and vehicle ownership trends. The regional distribution of the market is also influenced by the presence of major automotive manufacturers, semiconductor companies, and the development of local supply chains and technology ecosystems.

Regional Analysis of the Automotive Infotainment SoC Market - Detailed regional market performance

Regional analysis of the automotive infotainment SoC market reveals distinct performance patterns and growth trajectories across different geographic areas, shaped by local automotive industry dynamics, regulatory environments, and consumer preferences. In Asia-Pacific, the market demonstrates robust growth driven by the region's position as the world's largest automotive manufacturing hub, particularly in China, Japan, and South Korea. This region benefits from strong domestic demand for connected vehicles, government initiatives supporting electric and intelligent transportation, and the presence of major automotive and electronics manufacturers. China's market performance is particularly noteworthy, with rapid adoption of advanced infotainment features and strong government support for connected vehicle technologies. North America shows steady market performance characterized by high technology adoption rates, strong consumer demand for premium features, and significant investment in autonomous vehicle development. The United States leads regional performance with its concentration of technology companies and automotive innovation hubs. Europe demonstrates stable market growth influenced by stringent regulatory requirements for vehicle connectivity and safety, along with strong demand for luxury vehicles with advanced infotainment systems. Germany, as Europe's automotive manufacturing center, plays a particularly important role in regional market dynamics. Other regions including Latin America, the Middle East, and Africa show emerging market potential with growth rates varying based on economic conditions, vehicle ownership trends, and infrastructure development. Regional performance is also affected by factors such as trade policies, semiconductor supply chain localization efforts, and the development of local technology ecosystems.

Leading Company Profiles in the Automotive Infotainment SoC Market - Industry players and strategies

The automotive infotainment SoC market features several leading companies that have established strong positions through technological innovation, strategic partnerships, and deep automotive industry expertise. Infineon Technologies AG has built a significant presence through its comprehensive portfolio of automotive semiconductors and focus on energy efficiency and security features. Intel Corporation leverages its dominant position in computing technology to provide high-performance SoC solutions, particularly for autonomous driving and connected vehicle applications. NEC Corporation brings extensive experience in system integration and telecommunications to develop advanced infotainment platforms. NVIDIA Corporation has emerged as a key player through its powerful AI computing platforms and graphics processing capabilities, which are increasingly important for advanced vehicle interfaces and autonomous features. NXP Semiconductors N.V. maintains a strong market position through its broad automotive semiconductor portfolio and deep relationships with automotive manufacturers. Qualcomm Incorporated applies its wireless technology expertise to develop connected car solutions with advanced 5G and AI capabilities. Renesas Electronics Corporation focuses on integrated solutions that combine processing power with analog and power management functions. STMicroelectronics N.V. leverages its expertise in MEMS sensors and power electronics to provide comprehensive automotive solutions. Semiconductor Components Industries (On Semiconductor) specializes in energy-efficient solutions for automotive applications. Telechips, Inc. focuses on cost-effective solutions for mass-market vehicles, while Texas Instruments Incorporated brings its extensive analog and embedded processing expertise to automotive applications. These companies employ various strategies including vertical integration, strategic partnerships with automotive manufacturers, investment in software ecosystems, and development of specialized automotive-grade technologies to maintain and expand their market positions.

Porter's Five Forces Analysis of the Automotive Infotainment SoC Market - Competitive forces assessment

Porter's Five Forces analysis of the automotive infotainment SoC market reveals a competitive landscape shaped by several powerful industry forces that influence market dynamics and profitability. The threat of new entrants is relatively moderate due to high barriers to entry including the need for automotive-grade certification, substantial capital requirements for semiconductor fabrication, and the necessity of long-term relationships with automotive manufacturers. However, technology companies with strong financial resources and semiconductor expertise continue to enter the market, particularly those with existing relationships in adjacent markets. The bargaining power of buyers, primarily automotive OEMs and Tier-1 suppliers, is significant due to their large purchase volumes, ability to switch suppliers, and increasing tendency to develop in-house semiconductor capabilities. Supplier bargaining power is moderate, influenced by the consolidation of semiconductor manufacturing capacity and the critical nature of automotive-grade components, though the market faces ongoing challenges related to semiconductor supply constraints. The threat of substitute products is relatively low given the specialized nature of automotive infotainment SoCs and the lack of viable alternatives that can meet automotive reliability and safety requirements. Competitive rivalry is intense among established players, driven by rapid technological advancement, the need for continuous innovation, and the strategic importance of automotive semiconductors to future mobility trends. The analysis indicates that while the market offers significant opportunities, success requires substantial investment in technology development, strong automotive industry relationships, and the ability to navigate complex certification and quality requirements.

SWOT Analysis of the Automotive Infotainment SoC Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the automotive infotainment SoC market reveals important insights about the industry's internal capabilities and external environment. Strengths of the market include strong demand growth driven by the transformation toward connected and autonomous vehicles, the presence of established semiconductor companies with deep automotive expertise, and continuous technological advancement enabling increasingly sophisticated vehicle features. The market also benefits from the strategic importance of automotive semiconductors to the future of mobility and the willingness of automotive manufacturers to invest in advanced infotainment capabilities. Weaknesses include the high cost and complexity of developing automotive-grade SoCs, long development cycles that delay time-to-market, and vulnerability to semiconductor supply chain disruptions. The market also faces challenges related to managing thermal constraints in increasingly compact vehicle designs and ensuring cybersecurity for connected systems. Opportunities abound in emerging markets with growing vehicle ownership, the transition toward software-defined vehicles that enable continuous feature updates, and the integration of AI and machine learning capabilities that enhance user experiences. Additional opportunities exist in commercial vehicle applications, electric vehicle platforms, and the development of digital cockpit architectures. Threats to the market include intense competitive pressure from both established semiconductor companies and new technology entrants, potential regulatory changes affecting connected vehicle technologies, and macroeconomic factors that could impact automotive production volumes. The market also faces threats from rapid technological change that could render existing solutions obsolete and from cybersecurity risks that could undermine consumer confidence in connected vehicle features.

Automotive Infotainment SoC Market Value Chain Analysis - Industry structure and value flow

The automotive infotainment SoC market value chain represents a complex ecosystem of interconnected activities and participants that collectively deliver sophisticated semiconductor solutions to the automotive industry. At the foundation of the value chain are semiconductor foundries and intellectual property providers who supply the basic building blocks including fabrication processes, design IP, and manufacturing capabilities. Above this foundation, semiconductor companies engage in complex SoC design and development activities, integrating multiple functions including processing, graphics, connectivity, and automotive-specific features into unified platforms. These companies then work through rigorous testing, validation, and automotive certification processes to ensure their products meet stringent quality and reliability standards required for automotive applications. The value chain continues with distribution and supply chain management activities that ensure timely delivery of components to automotive manufacturers and Tier-1 suppliers. Automotive OEMs and Tier-1 suppliers represent critical nodes in the value chain, integrating SoCs into complete vehicle systems and user experiences while providing feedback and requirements that drive future SoC development. The value chain also includes software developers who create the operating systems, applications, and user interfaces that run on SoC platforms, as well as testing and validation services that ensure system reliability and safety. Throughout the value chain, various support services including logistics, technical support, and aftermarket services add additional value. The flow of value is characterized by increasing integration and complexity as the industry moves toward centralized computing architectures and software-defined vehicles, requiring closer collaboration and coordination among all participants in the value chain.

Key Investment Insights in the Automotive Infotainment SoC Market - Strategic investment recommendations

The automotive infotainment SoC market presents compelling investment opportunities driven by the fundamental transformation of the automotive industry toward connected, autonomous, and software-defined vehicles. Strategic investment insights indicate that companies should prioritize investments in AI and machine learning capabilities that enable advanced user experiences, predictive maintenance, and autonomous driving features. Investment in 5G and beyond connectivity technologies is crucial as vehicles increasingly rely on high-bandwidth connections for real-time services and cloud integration. The market also warrants significant investment in cybersecurity capabilities, as protecting connected vehicles from increasingly sophisticated threats becomes a critical competitive differentiator. Companies should consider strategic investments in software development capabilities and digital cockpit platforms, as the value proposition shifts from hardware to integrated hardware-software solutions. Investment in supply chain resilience and regional manufacturing capabilities is recommended to mitigate ongoing semiconductor supply constraints and geopolitical risks. The commercial vehicle segment represents an attractive investment opportunity due to growing demand for fleet management and telematics solutions. Emerging markets, particularly in Asia and other developing regions, offer significant growth potential for companies willing to adapt their solutions to local requirements and price points. Investment in partnerships and collaborative development efforts can provide access to complementary technologies and accelerate time-to-market for new solutions. Overall, successful investment strategies should focus on creating comprehensive, integrated solutions that address the evolving needs of automotive manufacturers while maintaining flexibility to adapt to rapid technological change and shifting market demands.

Automotive Infotainment SoC Market Conclusion - Summary and key takeaways

The automotive infotainment SoC market stands at the intersection of two transformative trends: the evolution of the automotive industry toward connected and intelligent vehicles, and the rapid advancement of semiconductor technology. The market demonstrates strong growth fundamentals, with projections showing expansion from 13.28 Billion to 20.43 Billion at a compound annual growth rate of 6.34%, driven by increasing consumer demand for advanced in-vehicle experiences and the automotive industry's shift toward software-defined architectures. Key takeaways from the market analysis include the critical importance of technological innovation in areas such as AI integration, 5G connectivity, and cybersecurity, as well as the need for companies to develop comprehensive hardware-software solutions that deliver compelling user experiences. The competitive landscape remains dynamic, with established semiconductor companies competing alongside new technology entrants, while automotive manufacturers increasingly seek to develop their own semiconductor capabilities. Regional variations in market development reflect differences in vehicle production volumes, technology adoption rates, and economic conditions, creating both challenges and opportunities for market participants. The market faces significant challenges including supply chain vulnerabilities, complex certification requirements, and intense competitive pressure, but these are outweighed by substantial opportunities in emerging markets, commercial vehicle applications, and the transition toward centralized computing architectures. Success in this market requires a combination of technological expertise, deep automotive industry knowledge, strong customer relationships, and the ability to navigate a rapidly evolving technological and competitive landscape.

Research Methodology - How this research was conducted

The research methodology employed for this automotive infotainment SoC market analysis combines multiple approaches to ensure comprehensive and reliable insights. Primary research forms a crucial component, involving interviews with industry experts, semiconductor manufacturers, automotive OEMs, and technology analysts to gather firsthand perspectives on market dynamics, technological trends, and competitive strategies. Secondary research complements primary data collection through extensive review of industry reports, company financial statements, technical publications, patent filings, and market databases to validate findings and provide broader context. The methodology incorporates both quantitative and qualitative analysis techniques, with quantitative methods including market sizing calculations, growth rate projections, and segmentation analysis based on available data points and industry benchmarks. Qualitative analysis focuses on understanding market drivers, challenges, competitive dynamics, and emerging trends through thematic analysis of industry developments and expert insights. The research process also includes careful validation of data through triangulation across multiple sources to ensure accuracy and reliability. Geographic and segment-specific analyses are conducted using a combination of top-down and bottom-up approaches to estimate market sizes and growth rates across different regions and application areas. The methodology acknowledges limitations in available data, particularly regarding specific market share figures and regional breakdowns, while providing reasoned analysis based on industry knowledge and observable trends. Throughout the research process, emphasis is placed on maintaining objectivity and providing balanced insights that reflect the complex and dynamic nature of the automotive infotainment SoC market.

Research Scope - Coverage and limitations

The research scope for this automotive infotainment SoC market analysis encompasses a comprehensive examination of the market's key dimensions, including market size and growth projections, competitive landscape, technological trends, regional variations, and strategic considerations for industry participants. The scope covers the forecast period from 2025 to 2032, with particular focus on the projected market expansion from 13.28 Billion to 20.43 Billion at a compound annual growth rate of 6.34%. The analysis includes examination of major market segments based on application (head unit, e-cockpit, sound system), vehicle type (passenger and commercial vehicles), and installation type (in-dash and rear seat configurations). The research scope encompasses leading companies in the market, including Infineon Technologies AG, Intel Corporation, NEC Corporation, NVIDIA Corporation, NXP Semiconductors N.V., Qualcomm Incorporated, Renesas Electronics Corporation, STMicroelectronics N.V., Semiconductor Components Industries (On Semiconductor), Telechips, Inc., and Texas Instruments Incorporated. Regional analysis covers major geographic markets, though specific market share data for individual regions is not provided within the available scope. The research scope acknowledges several limitations, including the unavailability of detailed regional market share data, specific application segment breakdowns, and granular competitive positioning information. Additionally, the scope recognizes that rapidly evolving technologies and market conditions may affect the accuracy of projections beyond the immediate forecast period. Despite these limitations, the research provides valuable insights into market trends, growth drivers, and strategic considerations based on available data and industry expertise.

Key Companies and Recent Developments in the Automotive Infotainment SoC Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The automotive infotainment SoC market features several key companies that have recently announced significant developments shaping the industry's trajectory. Infineon Technologies AG has focused on expanding its automotive-grade semiconductor portfolio with enhanced security features and energy-efficient designs, while Intel Corporation has leveraged its computing expertise to develop high-performance platforms for autonomous and connected vehicle applications. NVIDIA Corporation continues to strengthen its position through advanced AI computing platforms, particularly with recent announcements regarding enhanced graphics processing capabilities for digital cockpits and driver assistance systems. NXP Semiconductors N.V. has announced strategic partnerships with automotive manufacturers to develop integrated cockpit solutions that combine multiple vehicle functions onto unified SoC platforms. Qualcomm Incorporated has made headlines with its Snapdragon Digital Chassis platform, representing a comprehensive suite of connected car solutions with advanced 5G integration. Renesas Electronics Corporation has recently launched new automotive SoC families with enhanced processing power and functional safety features. STMicroelectronics N.V. has announced developments in MEMS sensor integration with SoC platforms to enable more sophisticated vehicle monitoring and user interface capabilities. Texas Instruments Incorporated has introduced new automotive-grade processors with improved graphics and multimedia capabilities. These companies are increasingly pursuing strategic partnerships, joint ventures, and collaborative development efforts to accelerate innovation and address the complex requirements of modern automotive infotainment systems. Recent developments also include increased focus on over-the-air update capabilities, cybersecurity enhancements, and the integration of AI and machine learning features directly into SoC architectures. These strategic moves reflect the industry's recognition that success in the automotive infotainment SoC market requires not only advanced hardware capabilities but also comprehensive software ecosystems and strong automotive industry relationships.