Subscriber Data Management Market Overview - Definition, scope, and significance

Subscriber Data Management (SDM) refers to the comprehensive process of collecting, storing, managing, and utilizing subscriber information across telecommunications networks. This market encompasses solutions and services that enable service providers to efficiently handle subscriber profiles, preferences, usage patterns, and authentication data. The significance of SDM has grown exponentially as telecommunications networks have evolved from simple voice services to complex ecosystems supporting data, video, and emerging technologies like 5G and IoT. SDM solutions serve as the backbone for delivering personalized services, ensuring network security, and optimizing resource allocation across fixed and mobile networks.

Subscriber Data Management Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Subscriber Data Management market is primarily driven by the rapid proliferation of connected devices, increasing demand for personalized services, and the ongoing rollout of 5G networks globally. The exponential growth in mobile data consumption and the need for real-time subscriber analytics are compelling service providers to invest in advanced SDM solutions. However, the market faces restraints such as data privacy concerns, regulatory compliance challenges, and the complexity of integrating legacy systems with modern SDM platforms. Additionally, the high initial investment costs and the shortage of skilled professionals pose significant challenges. Opportunities abound in the form of AI-driven subscriber analytics, edge computing integration, and the expanding IoT ecosystem, which require sophisticated data management capabilities.

Subscriber Data Management Market Growth Trends - Current and emerging trends shaping the market

The Subscriber Data Management market is witnessing several transformative trends that are reshaping its landscape. Cloud-based SDM solutions are gaining significant traction due to their scalability, flexibility, and cost-effectiveness. The integration of artificial intelligence and machine learning algorithms is enabling predictive analytics and automated subscriber management, enhancing operational efficiency. There is a growing trend towards federated identity management and policy-based control, allowing for more granular and dynamic subscriber data handling. Additionally, the convergence of fixed and mobile networks is driving the demand for unified SDM platforms that can manage subscribers across multiple access technologies. The emergence of edge computing is also influencing SDM trends, with a focus on distributed data management architectures to support low-latency applications and services.

COVID-19 Impact on the Subscriber Data Management Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the Subscriber Data Management market, initially causing disruptions in supply chains and delaying technology deployments. However, the crisis also accelerated digital transformation initiatives across industries, leading to increased demand for robust SDM solutions. The surge in remote work, online education, and digital entertainment resulted in unprecedented network traffic, highlighting the critical need for efficient subscriber data management. Service providers were compelled to rapidly scale their infrastructure and implement advanced SDM capabilities to handle the increased load and ensure service quality. As the world recovers from the pandemic, the market is witnessing a renewed focus on cloud-based solutions, enhanced security features, and the integration of 5G technologies, driving sustained growth in the post-COVID era.

Subscriber Data Management Market Competitive Landscape - Major competitors and market consolidation

The Subscriber Data Management market is characterized by intense competition among established telecommunications equipment vendors and emerging technology companies. The competitive landscape is marked by a mix of global players and regional specialists, each vying for market share through innovation and strategic partnerships. Major competitors are focusing on expanding their product portfolios to offer comprehensive SDM solutions that cater to the evolving needs of service providers. Market consolidation is evident through mergers, acquisitions, and strategic alliances aimed at enhancing technological capabilities and expanding geographic presence. The competition is further intensified by the entry of cloud service providers and software-defined networking specialists, challenging traditional SDM vendors to innovate and adapt to changing market dynamics.

Executive Summary - High-level overview and key findings about Subscriber Data Management Market

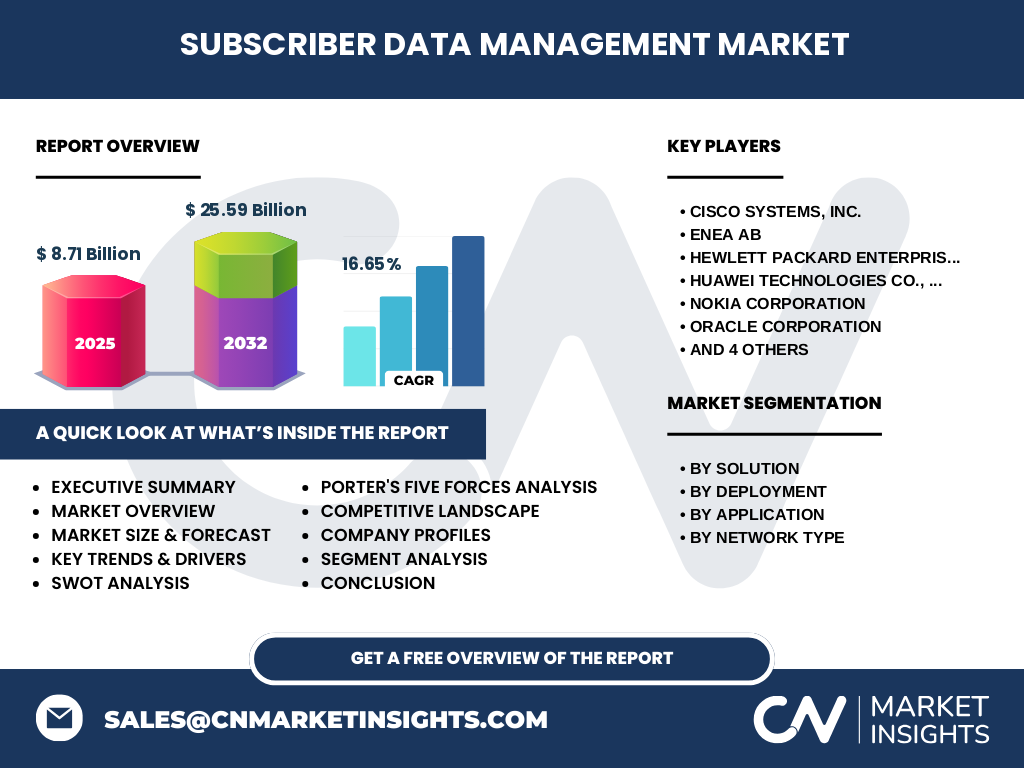

The Subscriber Data Management market is experiencing robust growth, driven by the increasing complexity of telecommunications networks and the demand for personalized services. With a market size of $8.71 billion in 2025 and a projected growth to $25.59 billion by 2032, the market is poised for significant expansion at a CAGR of 16.65%. Key trends shaping the market include the shift towards cloud-based solutions, the integration of AI and machine learning, and the convergence of fixed and mobile networks. The market is segmented by solution type, deployment model, application, and network type, catering to diverse industry needs. Major players such as Cisco Systems, Ericsson, and Huawei are leading innovation, while emerging technologies like 5G and IoT present substantial growth opportunities. The market faces challenges related to data privacy and legacy system integration but continues to evolve rapidly to meet the demands of the digital age.

Subscriber Data Management Market Forecast - Projections for 2025-2032 period

The Subscriber Data Management market is set for substantial growth over the forecast period from 2025 to 2032. Starting from a market size of $8.71 billion in 2025, the market is expected to reach $25.59 billion by 2032, representing a robust compound annual growth rate (CAGR) of 16.65%. This impressive growth trajectory is driven by several factors, including the rapid adoption of 5G networks, the proliferation of IoT devices, and the increasing demand for personalized services. The forecast period will likely see accelerated investment in cloud-based SDM solutions and AI-driven analytics capabilities. Regional markets, particularly in Asia-Pacific and North America, are expected to contribute significantly to this growth, fueled by expanding telecommunications infrastructure and digital transformation initiatives. The market is also anticipated to witness increased consolidation through mergers and acquisitions as companies seek to enhance their technological capabilities and expand their market presence.

Subscriber Data Management Market Size and Share by Segmentation - Breakdown by {segmentData}

The Subscriber Data Management market is segmented across several key dimensions, each contributing uniquely to the overall market dynamics. By solution type, the market is divided into User Data Repository, Subscriber Data Federation, Policy Management, and Identity Management. User Data Repository solutions are expected to hold a significant market share due to their fundamental role in storing and managing subscriber information. The deployment segment, comprising Cloud and On-Premise solutions, is witnessing a shift towards cloud-based offerings, driven by their scalability and cost-effectiveness. In terms of application, the Voice Over IP and Mobile segments are key contributors, with the Mobile segment likely to dominate due to the increasing smartphone penetration and mobile data consumption. The network type segmentation, including Fixed Networks and Mobile Networks, reflects the market's response to the convergence of these technologies, with Mobile Networks expected to show higher growth rates due to the 5G rollout.

Global Subscriber Data Management Market Size and Share by Region - Geographic distribution

The global Subscriber Data Management market exhibits diverse growth patterns across different regions, reflecting varying levels of technological adoption and telecommunications infrastructure development. North America, led by the United States, is expected to maintain a significant market share due to its advanced telecommunications ecosystem and early adoption of 5G technology. Europe, with its strong focus on digital transformation and stringent data protection regulations, represents another key market for SDM solutions. The Asia-Pacific region is anticipated to witness the highest growth rate, driven by rapid urbanization, increasing smartphone penetration, and massive investments in 5G infrastructure, particularly in countries like China, Japan, and South Korea. Latin America and the Middle East & Africa regions are also showing promising growth potential, albeit from a smaller base, as they continue to expand their telecommunications networks and embrace digital technologies.

Regional Analysis of the Subscriber Data Management Market - Detailed regional market performance

The Subscriber Data Management market exhibits distinct characteristics and growth patterns across different regions. In North America, the market is characterized by early adoption of advanced technologies, with a strong focus on cloud-based solutions and AI-driven analytics. The region's mature telecommunications infrastructure and high smartphone penetration drive demand for sophisticated SDM capabilities. Europe presents a unique landscape, where stringent data protection regulations such as GDPR influence the development and deployment of SDM solutions. The region emphasizes privacy-centric approaches and federated identity management. Asia-Pacific emerges as the fastest-growing region, fueled by rapid digitalization, expanding 5G networks, and a large consumer base. Countries like China and India are at the forefront of this growth, with massive investments in telecommunications infrastructure. Latin America and the Middle East & Africa regions are gradually catching up, with increasing government initiatives to improve digital connectivity and a growing demand for mobile services driving SDM adoption.

Leading Company Profiles in the Subscriber Data Management Market - Industry players and strategies

The Subscriber Data Management market is dominated by several key players, each bringing unique strengths and strategies to the competitive landscape. Cisco Systems, Inc. leverages its extensive networking expertise to offer comprehensive SDM solutions, focusing on integration with its broader portfolio of networking products. Enea AB specializes in real-time operating systems and middleware, positioning itself as a provider of high-performance SDM solutions for critical telecommunications infrastructure. Hewlett Packard Enterprise Development LP combines its hardware capabilities with software-defined networking solutions to offer end-to-end SDM platforms. Huawei Technologies Co., Ltd. capitalizes on its strong presence in the Asian market and its expertise in 5G technology to drive SDM innovation. Nokia Corporation emphasizes its Bell Labs research capabilities to develop cutting-edge SDM solutions, particularly for 5G networks. Oracle Corporation leverages its strength in database management and cloud services to offer scalable SDM platforms. R Systems International Limited focuses on providing customized SDM solutions for emerging markets. Sandvine brings expertise in network policy control and traffic management to enhance SDM capabilities. Telefonaktiebolaget LM Ericsson combines its telecommunications heritage with advanced software solutions to offer comprehensive SDM platforms. ZTE Corporation focuses on providing cost-effective SDM solutions, particularly for developing markets.

Porter's Five Forces Analysis of the Subscriber Data Management Market - Competitive forces assessment

The Subscriber Data Management market is influenced by several competitive forces that shape its dynamics and attractiveness. The threat of new entrants is moderate, as the market requires significant technological expertise and established relationships with telecommunications service providers. However, the entry of cloud service providers and software-defined networking specialists is increasing competitive pressure. The bargaining power of buyers, primarily telecommunications service providers, is high due to the availability of multiple solution providers and the critical nature of SDM in their operations. Suppliers, including component manufacturers and technology partners, have moderate bargaining power, as the market relies on a mix of proprietary and standardized technologies. The threat of substitute products or services is relatively low, given the specialized nature of SDM solutions, but the emergence of alternative data management approaches could pose future challenges. Competitive rivalry is intense, with major players competing on technological innovation, pricing, and comprehensive service offerings. The market is also influenced by the threat of forward integration by service providers, who may develop in-house SDM capabilities.

SWOT Analysis of the Subscriber Data Management Market - Strengths, weaknesses, opportunities, threats

The Subscriber Data Management market exhibits several strengths, including its critical role in enabling personalized services and network optimization, the growing demand for data-driven insights in telecommunications, and the increasing adoption of cloud-based solutions. The market's ability to support emerging technologies like 5G and IoT represents a significant strength. However, weaknesses exist in the form of complex integration challenges with legacy systems, high initial investment costs, and concerns about data privacy and security. Opportunities abound in the form of expanding 5G networks, the proliferation of IoT devices, and the increasing demand for real-time analytics and policy management. The market can also capitalize on the trend towards edge computing and the convergence of fixed and mobile networks. Threats to the market include stringent data protection regulations, the potential for disruptive technologies to emerge, and the risk of economic downturns affecting telecommunications investments. Additionally, the market faces challenges from cybersecurity threats and the need for continuous technological innovation to stay relevant in a rapidly evolving telecommunications landscape.

Subscriber Data Management Market Value Chain Analysis - Industry structure and value flow

The Subscriber Data Management market value chain encompasses several interconnected stages, each contributing to the delivery of comprehensive SDM solutions. At the foundation of the value chain are component manufacturers and technology providers who supply the hardware and software building blocks for SDM platforms. These include semiconductor companies, database management system providers, and cloud infrastructure vendors. The next stage involves solution developers and system integrators who design and implement SDM platforms, incorporating various technologies and customizing them to meet specific client requirements. Telecommunications equipment vendors and software companies then package these solutions into comprehensive SDM offerings, often bundling them with their broader product portfolios. Value-added resellers and managed service providers play a crucial role in distributing these solutions and providing implementation and support services to end-users. At the top of the value chain are the telecommunications service providers who deploy SDM solutions to manage their subscriber data and deliver enhanced services to end consumers. The value flow in this chain is driven by the increasing demand for personalized services, network optimization, and data-driven insights, with each stage adding value through technological innovation, customization, and service delivery.

Key Investment Insights in the Subscriber Data Management Market - Strategic investment recommendations

The Subscriber Data Management market presents several compelling investment opportunities for stakeholders looking to capitalize on the growing demand for advanced data management solutions. Strategic investments in cloud-based SDM platforms are particularly promising, given the industry's shift towards scalable and flexible infrastructure. Investors should consider opportunities in companies developing AI and machine learning capabilities for predictive analytics and automated subscriber management, as these technologies are becoming increasingly critical for competitive differentiation. The convergence of fixed and mobile networks presents investment opportunities in unified SDM solutions that can manage subscribers across multiple access technologies. Additionally, the expansion of 5G networks and the proliferation of IoT devices create a strong case for investing in SDM solutions that can handle massive data volumes and support diverse use cases. Investors should also explore opportunities in companies focusing on edge computing integration, as this trend is likely to reshape the SDM landscape in the coming years. Given the market's growth trajectory, investments in research and development to enhance security features and ensure regulatory compliance could yield significant returns.

Subscriber Data Management Market Conclusion - Summary and key takeaways

The Subscriber Data Management market is poised for significant growth, driven by the increasing complexity of telecommunications networks and the demand for personalized services. With a projected CAGR of 16.65% from 2025 to 2032, the market presents substantial opportunities for stakeholders across the value chain. Key trends shaping the market include the shift towards cloud-based solutions, the integration of AI and machine learning, and the convergence of fixed and mobile networks. While the market faces challenges related to data privacy, legacy system integration, and regulatory compliance, its critical role in enabling advanced telecommunications services ensures continued investment and innovation. The competitive landscape is characterized by intense rivalry among established players and emerging technology companies, driving rapid technological advancements. As the market evolves, stakeholders must focus on developing scalable, secure, and flexible SDM solutions to capitalize on the growing demand for data-driven insights and personalized services in the telecommunications industry.

Research Methodology - How this research was conducted

This comprehensive market research on the Subscriber Data Management industry was conducted using a robust methodology that combines both primary and secondary research approaches. The study involved extensive data collection from a wide range of sources, including industry reports, company annual reports, regulatory filings, and interviews with key industry stakeholders. Primary research included in-depth interviews with executives from leading SDM solution providers, telecommunications service providers, and industry experts to gather insights on market trends, technological advancements, and competitive dynamics. Secondary research involved analyzing data from reputable market intelligence databases, industry publications, and government sources to validate and supplement primary findings. The research methodology also incorporated a thorough analysis of patent filings, product launches, and strategic partnerships to understand the innovation landscape and competitive strategies in the SDM market. Market size and forecast estimates were derived using a combination of top-down and bottom-up approaches, considering factors such as technological trends, regulatory environment, and macroeconomic indicators. The research team employed advanced data triangulation techniques to ensure the accuracy and reliability of the findings presented in this report.

Research Scope - Coverage and limitations

This research report on the Subscriber Data Management market provides a comprehensive analysis of the industry, covering key aspects such as market size, growth trends, competitive landscape, and regional dynamics. The scope of the research encompasses the period from 2025 to 2032, with a particular focus on the base year of 2025 and the forecast period extending to 2032. The study covers various market segments, including solutions (User Data Repository, Subscriber Data Federation, Policy Management, Identity Management), deployment models (Cloud, On-Premise), applications (Voice Over IP, Mobile), and network types (Fixed Networks, Mobile Networks). The research also includes an analysis of key geographic regions, namely North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. While the report provides detailed insights into the market's current state and future projections, it is important to note that the research is subject to certain limitations. These include the rapidly evolving nature of the telecommunications industry, which may lead to unforeseen technological disruptions, and the potential impact of regulatory changes on market dynamics. Additionally, the report's findings are based on available data and expert opinions at the time of research, and actual market conditions may vary due to unforeseen global events or economic factors.

Key Companies and Recent Developments in the Subscriber Data Management Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Subscriber Data Management market is characterized by the presence of several key players who are driving innovation and shaping the industry's future. Cisco Systems, Inc. has recently announced advancements in its Intent-Based Networking platform, integrating enhanced SDM capabilities to support 5G network deployments. Enea AB unveiled its latest uCPE (Universal Customer Premises Equipment) solution, which includes advanced SDM features for edge computing environments. Hewlett Packard Enterprise Development LP introduced a new line of software-defined infrastructure solutions with built-in SDM functionalities, targeting hybrid cloud deployments. Huawei Technologies Co., Ltd. launched its next-generation SDM platform, emphasizing AI-driven subscriber analytics and real-time policy management for 5G networks. Nokia Corporation announced a strategic partnership with a major cloud service provider to enhance its SDM offerings with cloud-native capabilities. Oracle Corporation expanded its Communications Broadband Network Gateway portfolio with new SDM modules designed for IoT and 5G use cases. R Systems International Limited introduced a specialized SDM solution for emerging markets, focusing on cost-effective deployment and scalability. Sandvine unveiled its latest network policy control solution, integrating advanced SDM features for improved subscriber experience management. Telefonaktiebolaget LM Ericsson announced the acquisition of a software-defined networking startup to bolster its SDM capabilities in the 5G era. ZTE Corporation launched a new line of SDM solutions optimized for small and medium-sized telecommunications operators, emphasizing ease of deployment and management. These developments reflect the industry's focus on 5G readiness, cloud integration, and AI-driven capabilities to meet the evolving demands of telecommunications service providers.