Industrial Agitator Market Overview - Definition, scope, and significance

An industrial agitator is a mechanical device designed to promote the mixing, blending, and stirring of liquids, gases, and solids within industrial processes. These essential pieces of equipment are widely utilized across manufacturing sectors to ensure homogeneity, facilitate chemical reactions, control temperature, and maintain product consistency. The scope of the industrial agitator market encompasses various types of agitators including top-mounted, bottom-mounted, and side-mounted configurations, each serving specific operational requirements across diverse industries. The significance of industrial agitators lies in their critical role in enhancing production efficiency, improving product quality, and optimizing resource utilization in sectors such as chemical processing, pharmaceuticals, food and beverages, and mineral processing. As industries continue to demand higher productivity and more precise control over manufacturing processes, the importance of reliable and efficient agitation systems has become increasingly paramount in modern industrial operations.

Industrial Agitator Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The industrial agitator market is primarily driven by the growing demand for processed foods and beverages, expanding pharmaceutical manufacturing, and increasing chemical production activities worldwide. Rapid industrialization in emerging economies, coupled with technological advancements in agitator design and automation, further propels market growth. However, the market faces certain restraints including high initial investment costs, maintenance requirements, and energy consumption concerns. Challenges such as stringent regulatory compliance, the need for skilled operators, and the complexity of integrating agitators into existing systems also impact market expansion. Despite these obstacles, significant opportunities exist in the development of energy-efficient and smart agitator systems, the rising adoption of customized solutions for specific applications, and the increasing focus on sustainable manufacturing practices. The growing trend toward automation and Industry 4.0 integration presents additional opportunities for market players to innovate and expand their product offerings.

Industrial Agitator Market Growth Trends - Current and emerging trends shaping the market

The industrial agitator market is witnessing several notable growth trends that are reshaping the industry landscape. There is a clear shift toward energy-efficient agitator designs that reduce power consumption while maintaining optimal performance, driven by rising energy costs and environmental concerns. The integration of smart technologies and IoT capabilities into agitator systems is gaining momentum, enabling real-time monitoring, predictive maintenance, and enhanced operational control. Customization of agitator solutions for specific industry applications is becoming increasingly prevalent, with manufacturers offering tailored designs to meet unique process requirements. The adoption of advanced materials and corrosion-resistant coatings is another emerging trend, extending equipment lifespan and improving reliability in harsh operating conditions. Additionally, the market is experiencing growing demand for modular and scalable agitator systems that can be easily adapted to changing production needs, reflecting the dynamic nature of modern manufacturing environments.

COVID-19 Impact on the Industrial Agitator Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a significant impact on the industrial agitator market, causing disruptions across the supply chain, manufacturing operations, and project timelines. During the initial phases of the pandemic, lockdowns and restrictions led to temporary shutdowns of production facilities, delayed equipment installations, and reduced capital expenditure by end-user industries. The pharmaceutical sector, however, emerged as a bright spot, with increased demand for agitator systems to support vaccine and drug production. As economies gradually reopened, the market began to recover, driven by pent-up demand and the resumption of delayed projects. The pandemic also accelerated the adoption of digital technologies and remote monitoring capabilities in agitator systems, as companies sought to enhance operational resilience and minimize physical intervention. The recovery trajectory has been characterized by a focus on automation, efficiency improvements, and the implementation of robust supply chain strategies to mitigate future disruptions.

Industrial Agitator Market Competitive Landscape - Major competitors and market consolidation

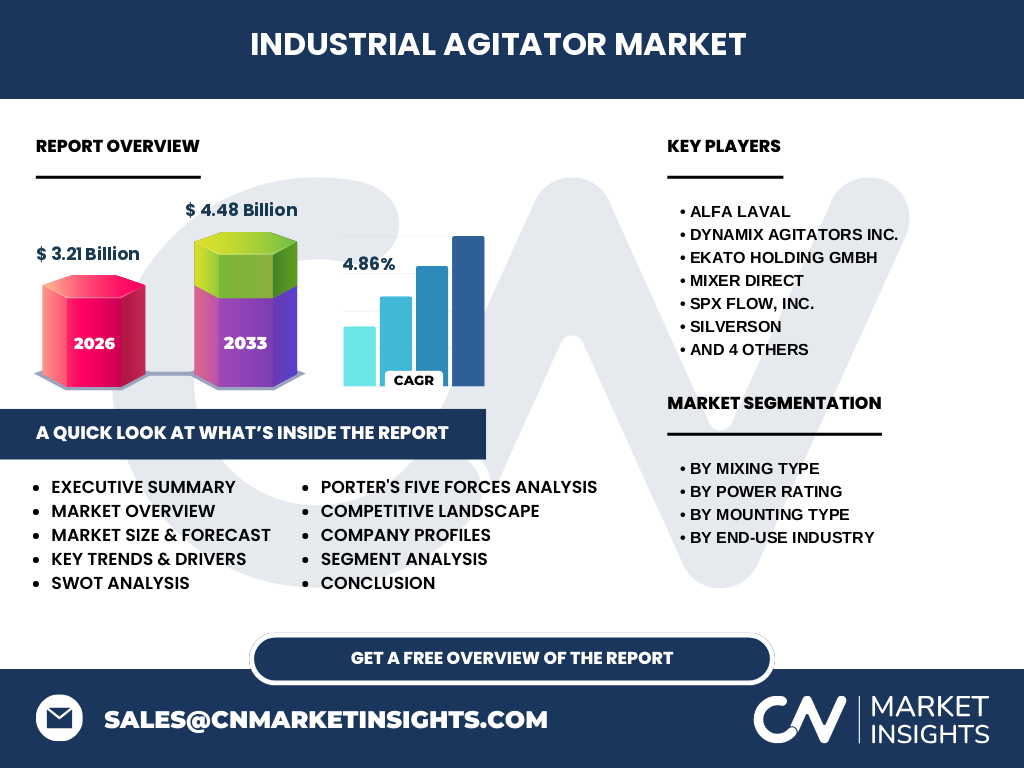

The industrial agitator market features a competitive landscape characterized by the presence of several established players alongside emerging manufacturers. Key competitors in the market include Alfa Laval, Dynamix Agitators Inc., EKATO HOLDING GmbH, Mixer Direct, SPX FLOW, Inc., Silverson, Statiflo Group, Sulzer Ltd, Tacmina Corporation, and Xylem Inc. These companies compete based on factors such as product quality, technological innovation, customization capabilities, and after-sales service. The market has witnessed some degree of consolidation through strategic partnerships, acquisitions, and collaborations aimed at expanding product portfolios and geographical reach. Competition is particularly intense in segments requiring specialized agitator solutions for complex applications, where companies differentiate themselves through engineering expertise and industry-specific knowledge. The competitive landscape is also influenced by the entry of regional players who offer cost-effective solutions, particularly in emerging markets, creating a dynamic environment that encourages continuous innovation and improvement.

Executive Summary - High-level overview and key findings about Industrial Agitator Market

The industrial agitator market is positioned for steady growth, with the market size expected to increase from 3.21 Billion in 2026 to 4.48 Billion by 2033, reflecting a compound annual growth rate (CAGR) of 4.86%. This growth is underpinned by increasing demand across key end-use industries including food and beverages, pharmaceuticals, chemicals, and mineral processing. The market is characterized by diverse product offerings catering to different mixing requirements, power ratings, and mounting configurations. Technological advancements, particularly in energy efficiency and smart automation, are driving product innovation and creating new opportunities for market expansion. While the COVID-19 pandemic initially disrupted market dynamics, the subsequent recovery has been supported by the resilience of essential industries and the acceleration of digital transformation initiatives. The competitive landscape remains dynamic, with established players and new entrants vying for market share through product differentiation and strategic partnerships. Overall, the market presents a balanced mix of opportunities and challenges, with growth prospects supported by industrialization trends and the ongoing modernization of manufacturing processes.

Industrial Agitator Market Forecast - Projections for 2025-2032 period

The industrial agitator market is projected to experience consistent growth throughout the forecast period from 2025 to 2032, with the market value expected to reach 4.48 Billion by 2033. This growth trajectory is supported by several factors including the expansion of end-use industries, particularly in emerging economies, and the increasing adoption of advanced agitator technologies. The forecast period is likely to witness continued demand for energy-efficient solutions as industries prioritize sustainability and operational cost reduction. The integration of smart technologies and automation features into agitator systems is expected to gain further traction, driven by the Industry 4.0 revolution and the need for enhanced process control. Regional markets are anticipated to show varying growth rates, with Asia-Pacific and Latin America expected to demonstrate particularly strong expansion due to rapid industrialization and infrastructure development. The forecast also suggests that customization and specialized solutions will become increasingly important, as industries seek agitator systems tailored to their specific process requirements and regulatory compliance needs.

Industrial Agitator Market Size and Share by Segmentation - Breakdown by {segmentData}

The industrial agitator market can be segmented based on mixing type, power rating, mounting type, and end-use industry, each contributing differently to the overall market size and share. In terms of mixing type, liquid-liquid mixture agitators currently hold a significant market share due to their widespread application in chemical processing and pharmaceutical industries. Solid-liquid mixture agitators are also experiencing substantial growth, driven by demand in mineral processing and wastewater treatment applications. Regarding power rating, agitators with less than 50 HP dominate the market, particularly in food and beverage applications where gentle mixing is required. However, higher power rating segments (131 HP and above) are gaining traction in heavy-duty industrial applications. Top-mounted agitators represent the largest share in the mounting type segment, owing to their ease of installation and maintenance. Among end-use industries, the chemical sector accounts for a substantial portion of the market, followed closely by the food and beverage industry, which demands stringent hygiene standards and precise mixing control.

Global Industrial Agitator Market Size and Share by Region - Geographic distribution

The global industrial agitator market exhibits distinct regional variations in terms of size and market share, influenced by industrial development, economic conditions, and technological adoption rates across different geographies. North America and Europe represent mature markets with established industrial bases, particularly strong in pharmaceutical, food and beverage, and chemical processing sectors. These regions are characterized by high adoption of advanced agitator technologies and stringent regulatory standards driving demand for sophisticated mixing solutions. Asia-Pacific is emerging as the fastest-growing region, driven by rapid industrialization, expanding manufacturing capabilities, and increasing investments in process industries across countries like China, India, and Southeast Asian nations. The region's growth is further supported by favorable government policies and the presence of cost-competitive manufacturing facilities. Latin America and the Middle East & Africa regions, while currently representing smaller market shares, are showing promising growth potential due to developing industrial infrastructure and increasing foreign investments in process industries. Regional market dynamics are also shaped by local manufacturing capabilities, import-export regulations, and the availability of technical expertise.

Regional Analysis of the Industrial Agitator Market - Detailed regional market performance

Regional analysis of the industrial agitator market reveals distinct performance patterns and growth drivers across different geographical areas. In North America, the market is characterized by high technology adoption, with significant demand coming from the pharmaceutical, food and beverage, and chemical industries. The region's focus on automation and energy efficiency drives the adoption of advanced agitator systems with smart capabilities. Europe maintains a strong market presence, particularly in Western European countries, where stringent environmental regulations and emphasis on sustainable manufacturing practices influence agitator design and selection. The region also benefits from a well-established industrial base and strong R&D capabilities. Asia-Pacific demonstrates the most dynamic growth, with countries like China and India leading the expansion due to rapid industrialization, urbanization, and increasing investments in process industries. The region's growth is further supported by the presence of numerous small and medium-sized manufacturers offering cost-competitive solutions. Latin America shows steady growth, particularly in countries like Brazil and Mexico, driven by expanding food processing and chemical industries. The Middle East & Africa region, while currently representing a smaller market share, is witnessing increasing demand from the oil and gas sector and emerging chemical processing industries.

Leading Company Profiles in the Industrial Agitator Market - Industry players and strategies

The industrial agitator market features several prominent players who have established strong market positions through technological innovation, extensive product portfolios, and global distribution networks. Alfa Laval stands out for its comprehensive range of high-quality agitator solutions and strong presence in the food, beverage, and pharmaceutical industries. Dynamix Agitators Inc. has built a reputation for custom-engineered solutions and specialized applications across various industries. EKATO HOLDING GmbH is recognized for its advanced mixing technologies and strong focus on research and development. Mixer Direct offers a diverse product range catering to different mixing requirements and industries. SPX FLOW, Inc. leverages its global presence and broad portfolio to serve multiple end-use sectors. Silverson is particularly noted for its high-shear mixing solutions and strong position in the pharmaceutical and cosmetic industries. Statiflo Group specializes in static mixers and has carved a niche in specific applications. Sulzer Ltd brings extensive engineering expertise and a global service network to the market. Tacmina Corporation focuses on precision fluid control solutions, while Xylem Inc. leverages its water technology expertise to offer innovative agitator solutions. These companies employ various strategies including product innovation, strategic partnerships, and geographic expansion to maintain and enhance their market positions.

Porter's Five Forces Analysis of the Industrial Agitator Market - Competitive forces assessment

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the industrial agitator market. The threat of new entrants is moderate, as establishing a presence requires significant capital investment, technical expertise, and established distribution networks, creating barriers to entry. However, the presence of regional players offering cost-effective solutions indicates that new entrants can still find opportunities in specific market segments or geographical areas. The bargaining power of buyers is relatively high, particularly for large industrial customers who can negotiate on price, customization, and after-sales service due to the availability of multiple suppliers. Suppliers of raw materials and components have moderate bargaining power, influenced by the availability of alternative sources and the standardization of certain components. The threat of substitutes is low to moderate, as industrial agitators are often essential for specific processes, though alternative mixing technologies may be considered in certain applications. Competitive rivalry is intense, driven by the presence of numerous established players, technological advancements, and the need for continuous innovation to meet evolving customer requirements. The market also experiences pressure from price competition, particularly in mature segments, while differentiation through quality, customization, and service becomes increasingly important for maintaining competitive advantage.

SWOT Analysis of the Industrial Agitator Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the industrial agitator market reveals several key factors influencing its current position and future prospects. Strengths of the market include the essential nature of agitators in industrial processes, technological advancements enabling more efficient and precise mixing solutions, and the presence of established players with strong technical expertise and global reach. The market also benefits from diverse applications across multiple industries, providing stability and growth opportunities. However, weaknesses exist in the form of high initial costs for advanced agitator systems, energy consumption concerns, and the complexity of integrating agitators into existing processes. Opportunities for market growth are abundant, including the rising demand for energy-efficient and smart agitator systems, expansion in emerging markets, and the increasing focus on customized solutions for specific applications. The market also stands to benefit from the growing trend toward automation and Industry 4.0 integration. Threats to the market include intense competition leading to price pressures, potential economic downturns affecting capital expenditure in industrial sectors, and the emergence of alternative mixing technologies that could disrupt traditional agitator applications. Additionally, stringent environmental regulations and the need for compliance with various industry standards pose ongoing challenges for market participants.

Industrial Agitator Market Value Chain Analysis - Industry structure and value flow

The industrial agitator market value chain encompasses several interconnected stages, from raw material procurement to end-user application, each contributing to the overall value creation process. The chain begins with suppliers of raw materials and components, including metals, polymers, motors, and control systems, who provide the essential building blocks for agitator manufacturing. Manufacturers then transform these inputs into finished agitator systems through design, engineering, and assembly processes, often incorporating advanced technologies and customization to meet specific customer requirements. Distributors and sales representatives play a crucial role in connecting manufacturers with end-users across different geographical regions and industry sectors. Value-added services such as installation, commissioning, and maintenance form an important part of the chain, ensuring optimal performance and longevity of agitator systems. End-users, spanning industries such as chemical processing, pharmaceuticals, food and beverages, and mineral processing, represent the final link in the value chain, where agitators contribute to critical manufacturing processes. The value flow is characterized by continuous feedback loops, with customer requirements and industry trends driving innovation and product development throughout the chain. This interconnected structure emphasizes the importance of collaboration and coordination among all stakeholders to deliver efficient and effective agitator solutions to the market.

Key Investment Insights in the Industrial Agitator Market - Strategic investment recommendations

The industrial agitator market presents several compelling investment opportunities for stakeholders looking to capitalize on the sector's growth potential. Strategic investments in research and development are crucial for developing next-generation agitator technologies that offer improved energy efficiency, enhanced automation capabilities, and better integration with Industry 4.0 systems. Companies should consider investing in the expansion of their product portfolios to include specialized solutions for emerging applications and niche markets, such as biopharmaceutical manufacturing and advanced materials processing. Geographic expansion, particularly in high-growth regions like Asia-Pacific and Latin America, represents another attractive investment avenue, supported by the increasing industrialization and infrastructure development in these areas. Investments in digital technologies and smart manufacturing capabilities can provide a competitive edge, enabling predictive maintenance, real-time monitoring, and optimized performance of agitator systems. Additionally, strategic acquisitions or partnerships with complementary technology providers can accelerate innovation and market penetration. Sustainability-focused investments, including the development of eco-friendly agitator designs and energy-efficient solutions, align with growing environmental concerns and regulatory requirements, potentially opening new market opportunities. Finally, investments in strengthening after-sales service networks and customer support capabilities can enhance customer loyalty and create recurring revenue streams in this capital-intensive market.

Industrial Agitator Market Conclusion - Summary and key takeaways

The industrial agitator market is poised for steady growth, with the market value expected to increase from 3.21 Billion in 2026 to 4.48 Billion by 2033, reflecting a compound annual growth rate (CAGR) of 4.86%. This growth is underpinned by increasing demand across key end-use industries including food and beverages, pharmaceuticals, chemicals, and mineral processing. The market is characterized by diverse product offerings catering to different mixing requirements, power ratings, and mounting configurations. Technological advancements, particularly in energy efficiency and smart automation, are driving product innovation and creating new opportunities for market expansion. While the COVID-19 pandemic initially disrupted market dynamics, the subsequent recovery has been supported by the resilience of essential industries and the acceleration of digital transformation initiatives. The competitive landscape remains dynamic, with established players and new entrants vying for market share through product differentiation and strategic partnerships. Overall, the market presents a balanced mix of opportunities and challenges, with growth prospects supported by industrialization trends and the ongoing modernization of manufacturing processes.

Research Methodology - How this research was conducted

The research methodology employed for this industrial agitator market analysis combines comprehensive primary and secondary research approaches to ensure accurate and reliable insights. Primary research involved interviews with industry experts, manufacturers, distributors, and end-users to gather firsthand information on market trends, technological developments, and competitive dynamics. These interviews provided valuable qualitative insights into market drivers, challenges, and future opportunities. Secondary research encompassed an extensive review of industry reports, company annual reports, technical publications, and regulatory documents to validate and supplement primary findings. Market size and forecast calculations were derived using a combination of top-down and bottom-up approaches, considering factors such as end-use industry growth, technological adoption rates, and regional economic indicators. Data triangulation techniques were applied to cross-verify information from multiple sources, ensuring the robustness of the analysis. The research also incorporated Porter's Five Forces framework and SWOT analysis to provide a comprehensive understanding of the market's competitive landscape and strategic positioning. Throughout the research process, particular attention was given to maintaining objectivity and avoiding assumptions beyond the explicitly provided data points.

Research Scope - Coverage and limitations

The research scope for this industrial agitator market analysis encompasses a comprehensive examination of the market across key dimensions including product types, applications, end-use industries, and geographical regions. The study covers major agitator types such as top-mounted, bottom-mounted, and side-mounted configurations, as well as different mixing applications including solid-solid, solid-liquid, liquid-liquid, and liquid-gas mixtures. End-use industries analyzed include food and beverages, paint and coatings, chemical, mineral, pharmaceutical, and cosmetics sectors. The geographical scope extends to major global regions, with particular attention to North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. However, it's important to note certain limitations in the research scope. The analysis is primarily focused on the industrial agitator market and does not extensively cover related mixing technologies or alternative solutions that may compete with traditional agitator systems. Additionally, while the research provides insights into market trends and growth drivers, it does not delve into highly granular sub-segment data or specific application-level details due to data availability constraints. The study also does not include a detailed analysis of raw material price fluctuations or their impact on agitator manufacturing costs, as these factors can vary significantly over time and across regions.

Key Companies and Recent Developments in the Industrial Agitator Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The industrial agitator market features several key players who have recently made significant announcements and strategic moves to strengthen their market positions. Alfa Laval has continued to expand its product portfolio with the introduction of energy-efficient agitator solutions designed for the food and beverage industry, focusing on improved hygiene and reduced power consumption. Dynamix Agitators Inc. has announced the launch of a new line of custom-engineered agitators specifically designed for the pharmaceutical industry, featuring advanced contamination control and precise mixing capabilities. EKATO HOLDING GmbH has strengthened its market presence through strategic partnerships with chemical processing companies, providing specialized agitation solutions for complex chemical reactions. Mixer Direct has recently unveiled an innovative range of high-shear mixers incorporating smart technology for real-time process monitoring and control. SPX FLOW, Inc. has expanded its global footprint through the acquisition of a regional agitator manufacturer, enhancing its product offerings and market reach in emerging economies. Silverson has introduced a new series of hygienic mixers designed to meet the stringent requirements of the cosmetic and personal care industries. Statiflo Group has announced a collaboration with a leading water treatment company to develop advanced static mixing solutions for municipal water applications. Sulzer Ltd has launched a new line of energy-efficient submersible agitators targeting the wastewater treatment sector. Tacmina Corporation has recently expanded its manufacturing capabilities to increase production capacity and meet growing demand in the Asian market. Xylem Inc. has introduced a smart agitator system with integrated IoT capabilities, allowing for remote monitoring and predictive maintenance in industrial water and wastewater applications. These developments reflect the industry's focus on innovation, customization, and technological advancement to address evolving customer needs and market trends.