Australia and New Zealand Data Protection as a Service Market Overview - Definition, scope, and significance

The Australia and New Zealand Data Protection as a Service (DPaaS) market represents a rapidly evolving segment of the cloud computing industry, providing organizations with comprehensive data protection solutions delivered through cloud-based infrastructure. This market encompasses services such as Backup as a Service (BaaS), Disaster Recovery as a Service (DRaaS), and Storage as a Service (STaaS), enabling businesses to safeguard critical data without the need for extensive on-premises infrastructure. The significance of this market lies in its ability to address the growing data protection needs of organizations across Australia and New Zealand, particularly as businesses increasingly adopt digital transformation strategies and face mounting cybersecurity threats. DPaaS solutions offer scalable, cost-effective, and flexible alternatives to traditional data protection methods, making them particularly attractive to small and medium enterprises (SMEs) as well as large enterprises seeking to optimize their data management strategies.

Australia and New Zealand Data Protection as a Service Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Australia and New Zealand DPaaS market is driven by several key factors, including the increasing adoption of cloud technologies, growing data volumes, and stringent regulatory requirements such as the Australian Privacy Principles and New Zealand's Privacy Act. Organizations are recognizing the need for robust data protection strategies to mitigate risks associated with data breaches and system failures. However, the market faces restraints such as concerns over data sovereignty, particularly in industries with strict compliance requirements, and the challenge of integrating DPaaS solutions with existing IT infrastructure. Additionally, the complexity of managing hybrid cloud environments and the potential for vendor lock-in pose significant challenges. Opportunities in this market include the rising demand for hybrid cloud solutions, advancements in artificial intelligence and machine learning for predictive analytics, and the growing focus on disaster recovery capabilities to ensure business continuity in the face of increasing cyber threats.

Australia and New Zealand Data Protection as a Service Market Growth Trends - Current and emerging trends shaping the market

The Australia and New Zealand DPaaS market is witnessing several notable growth trends, including the increasing adoption of hybrid cloud deployment models, which combine the benefits of private and public cloud environments. This trend is driven by organizations seeking to balance data security with scalability and cost-efficiency. Another emerging trend is the integration of advanced technologies such as artificial intelligence and machine learning into DPaaS solutions, enabling predictive analytics and automated threat detection. Additionally, there is a growing emphasis on disaster recovery as a service, as businesses prioritize resilience and continuity in the face of natural disasters and cyber incidents. The market is also seeing a shift towards managed service providers (MSPs) offering tailored DPaaS solutions to meet the specific needs of SMEs, which often lack the resources to implement comprehensive data protection strategies independently.

COVID-19 Impact on the Australia and New Zealand Data Protection as a Service Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic has had a profound impact on the Australia and New Zealand DPaaS market, accelerating the adoption of cloud-based data protection solutions as organizations rapidly transitioned to remote work models. The pandemic underscored the importance of robust disaster recovery and business continuity plans, driving increased demand for DPaaS offerings. However, the initial disruption caused by lockdowns and economic uncertainty temporarily slowed market growth as businesses prioritized immediate operational needs over long-term IT investments. As the region recovers, the market is expected to rebound strongly, with organizations investing in scalable and resilient data protection solutions to support hybrid work environments and mitigate future disruptions. The pandemic has also highlighted the need for enhanced cybersecurity measures, further boosting the adoption of DPaaS solutions that offer advanced threat detection and mitigation capabilities.

Australia and New Zealand Data Protection as a Service Market Competitive Landscape - Major competitors and market consolidation

The competitive landscape of the Australia and New Zealand DPaaS market is characterized by the presence of both global technology giants and regional players, creating a dynamic and competitive environment. Major competitors such as Amazon Web Services, IBM Corporation, and VMware, Inc. dominate the market with their extensive cloud infrastructure and comprehensive service offerings. These companies are leveraging their global reach and technological expertise to capture significant market share. Meanwhile, regional players like Acronis International GmbH and Commvault are focusing on tailored solutions to address the specific needs of local businesses, particularly in highly regulated industries. The market is also witnessing consolidation through strategic partnerships, mergers, and acquisitions, as companies seek to expand their service portfolios and enhance their competitive positioning. This consolidation is expected to drive innovation and improve service quality, benefiting end-users across the region.

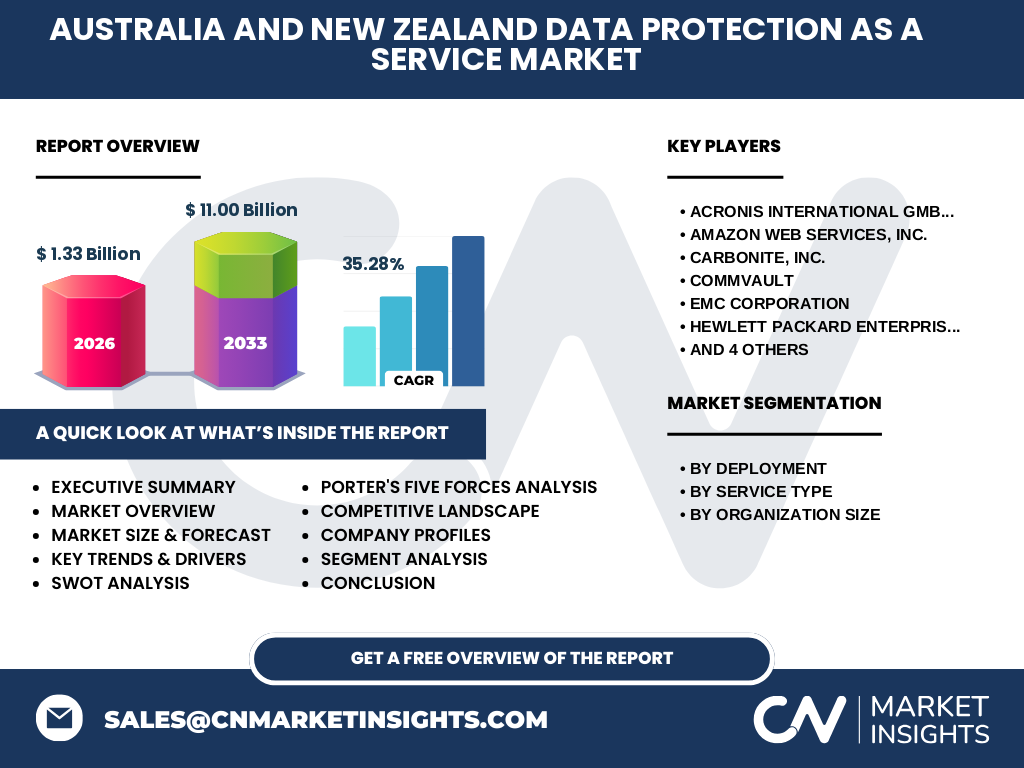

Executive Summary - High-level overview and key findings about Australia and New Zealand Data Protection as a Service Market

The Australia and New Zealand DPaaS market is poised for significant growth, driven by the increasing adoption of cloud technologies, rising data protection needs, and the growing emphasis on disaster recovery and business continuity. The market is expected to grow from a size of 1.33 billion in 2026 to 11.00 billion by 2033, reflecting a robust compound annual growth rate (CAGR) of 35.28%. Key trends shaping the market include the adoption of hybrid cloud deployment models, the integration of advanced technologies such as AI and machine learning, and the rising demand for managed service providers. While challenges such as data sovereignty concerns and integration complexities persist, the market presents substantial opportunities for innovation and growth. The competitive landscape is dominated by global players, but regional providers are gaining traction by offering tailored solutions to meet local needs.

Australia and New Zealand Data Protection as a Service Market Forecast - Projections for 2025-2032 period

The Australia and New Zealand DPaaS market is projected to experience substantial growth over the forecast period from 2025 to 2032, with the market size expected to increase from 1.33 billion in 2026 to 11.00 billion by 2033. This growth trajectory reflects a compound annual growth rate (CAGR) of 35.28%, underscoring the rapid adoption of DPaaS solutions across the region. The forecast period is expected to be characterized by increased investment in cloud infrastructure, advancements in data protection technologies, and a growing focus on disaster recovery capabilities. The adoption of hybrid cloud deployment models is anticipated to drive significant demand, as organizations seek to balance scalability with data security. Additionally, the integration of AI and machine learning into DPaaS solutions is expected to enhance predictive analytics and threat detection, further fueling market growth.

Australia and New Zealand Data Protection as a Service Market Size and Share by Segmentation - Breakdown by {segmentData}

The Australia and New Zealand DPaaS market is segmented by deployment type, service type, and organization size, each contributing to the overall market dynamics. In terms of deployment, the hybrid cloud segment is expected to dominate, as organizations increasingly adopt a mix of private and public cloud environments to optimize cost and security. By service type, Backup as a Service (BaaS) is projected to hold the largest share, driven by the growing need for reliable data backup solutions. Disaster Recovery as a Service (DRaaS) is also expected to witness significant growth, as businesses prioritize resilience and continuity. In terms of organization size, large enterprises are likely to account for the majority of the market share, owing to their substantial data protection requirements and greater financial resources. However, the SME segment is anticipated to grow rapidly, as managed service providers offer cost-effective and scalable DPaaS solutions tailored to their needs.

Global Australia and New Zealand Data Protection as a Service Market Size and Share by Region - Geographic distribution

The Australia and New Zealand DPaaS market is geographically concentrated in two primary regions: Australia and New Zealand. Australia is expected to dominate the market, driven by its larger economy, higher adoption of cloud technologies, and the presence of major technology hubs such as Sydney and Melbourne. The country's robust digital infrastructure and favorable regulatory environment further support the growth of the DPaaS market. New Zealand, while smaller in market size, is also witnessing significant growth, particularly in sectors such as finance, healthcare, and government, where data protection is critical. The geographic distribution of the market is influenced by factors such as internet penetration, digital transformation initiatives, and the level of cybersecurity awareness. As both countries continue to invest in cloud infrastructure and data protection capabilities, the regional market is expected to expand further.

Regional Analysis of the Australia and New Zealand Data Protection as a Service Market - Detailed regional market performance

The regional analysis of the Australia and New Zealand DPaaS market reveals distinct performance patterns in each country. Australia, with its advanced digital economy and higher concentration of large enterprises, is the dominant market, accounting for the majority of the region's DPaaS adoption. The country's strong focus on cybersecurity and data protection regulations, such as the Australian Privacy Principles, drives demand for comprehensive DPaaS solutions. Key industries driving growth in Australia include finance, healthcare, and government, where data protection is paramount. New Zealand, while smaller in market size, is experiencing rapid growth, particularly in sectors such as agriculture, tourism, and education. The country's emphasis on innovation and digital transformation, coupled with its stringent data protection laws, is fostering the adoption of DPaaS solutions. Both countries are expected to see increased investment in hybrid cloud deployment models and advanced data protection technologies, further boosting regional market performance.

Leading Company Profiles in the Australia and New Zealand Data Protection as a Service Market - Industry players and strategies

The Australia and New Zealand DPaaS market is characterized by the presence of several leading companies, each employing distinct strategies to capture market share. Amazon Web Services (AWS) leverages its extensive global cloud infrastructure and comprehensive service portfolio to dominate the market, offering scalable and cost-effective DPaaS solutions. IBM Corporation focuses on integrating advanced technologies such as AI and machine learning into its DPaaS offerings, enhancing predictive analytics and threat detection capabilities. VMware, Inc. emphasizes hybrid cloud solutions, enabling organizations to seamlessly manage data across private and public cloud environments. Regional players like Acronis International GmbH and Commvault are gaining traction by offering tailored solutions that address the specific needs of local businesses, particularly in highly regulated industries. These companies are also investing in strategic partnerships and acquisitions to expand their service portfolios and strengthen their competitive positioning.

Porter's Five Forces Analysis of the Australia and New Zealand Data Protection as a Service Market - Competitive forces assessment

The Porter's Five Forces analysis of the Australia and New Zealand DPaaS market reveals a competitive landscape shaped by several key forces. The threat of new entrants is moderate, as the market requires significant investment in cloud infrastructure and technological expertise, creating barriers to entry. However, the growing demand for DPaaS solutions presents opportunities for innovative startups to disrupt the market. The bargaining power of buyers is relatively high, as organizations have multiple options for DPaaS providers and can negotiate pricing and service terms. The bargaining power of suppliers is moderate, as key components such as cloud infrastructure and advanced technologies are provided by a few dominant players. The threat of substitutes is low, as traditional data protection methods are increasingly being replaced by cloud-based solutions. Finally, the intensity of competitive rivalry is high, with global giants and regional players competing on price, innovation, and service quality.

SWOT Analysis of the Australia and New Zealand Data Protection as a Service Market - Strengths, weaknesses, opportunities, threats

The SWOT analysis of the Australia and New Zealand DPaaS market highlights several key factors influencing its growth and development. Strengths include the increasing adoption of cloud technologies, the presence of a robust digital infrastructure, and the growing emphasis on data protection regulations. Weaknesses include concerns over data sovereignty, the complexity of integrating DPaaS solutions with existing IT infrastructure, and the potential for vendor lock-in. Opportunities in the market include the rising demand for hybrid cloud solutions, advancements in AI and machine learning, and the growing focus on disaster recovery capabilities. Threats include the increasing sophistication of cyber threats, regulatory challenges, and the potential for economic downturns to impact IT spending. Overall, the market presents significant opportunities for growth, but companies must navigate challenges related to security, compliance, and competition.

Australia and New Zealand Data Protection as a Service Market Value Chain Analysis - Industry structure and value flow

The value chain analysis of the Australia and New Zealand DPaaS market reveals a complex ecosystem involving multiple stakeholders and processes. At the core of the value chain are service providers, including global cloud giants like AWS and IBM, as well as regional players like Acronis and Commvault, who develop and deliver DPaaS solutions. These providers rely on cloud infrastructure providers for the underlying technology and storage capabilities. Managed service providers (MSPs) play a crucial role in the value chain by offering tailored DPaaS solutions to SMEs, which often lack the resources to implement comprehensive data protection strategies independently. Additionally, technology partners and system integrators contribute to the value chain by enhancing DPaaS solutions with advanced features such as AI-driven analytics and automation. The value chain is further supported by regulatory bodies, which establish data protection standards, and end-users, who drive demand for secure and scalable data protection solutions.

Key Investment Insights in the Australia and New Zealand Data Protection as a Service Market - Strategic investment recommendations

The Australia and New Zealand DPaaS market presents several key investment opportunities for stakeholders seeking to capitalize on the region's growing demand for data protection solutions. Investors should focus on companies that are leveraging advanced technologies such as AI and machine learning to enhance their DPaaS offerings, as these innovations are expected to drive significant market growth. Additionally, investments in hybrid cloud deployment models are recommended, as organizations increasingly seek to balance scalability with data security. The SME segment also represents a lucrative investment opportunity, as managed service providers offer cost-effective and scalable DPaaS solutions tailored to their needs. Furthermore, investors should consider companies that are expanding their presence in highly regulated industries such as finance and healthcare, where data protection is critical. Strategic partnerships and acquisitions are also likely to yield strong returns, as companies seek to enhance their service portfolios and competitive positioning.

Australia and New Zealand Data Protection as a Service Market Conclusion - Summary and key takeaways

The Australia and New Zealand DPaaS market is poised for significant growth, driven by the increasing adoption of cloud technologies, rising data protection needs, and the growing emphasis on disaster recovery and business continuity. The market is expected to grow from 1.33 billion in 2026 to 11.00 billion by 2033, reflecting a robust CAGR of 35.28%. Key trends shaping the market include the adoption of hybrid cloud deployment models, the integration of advanced technologies such as AI and machine learning, and the rising demand for managed service providers. While challenges such as data sovereignty concerns and integration complexities persist, the market presents substantial opportunities for innovation and growth. The competitive landscape is dominated by global players, but regional providers are gaining traction by offering tailored solutions to meet local needs. Overall, the market offers significant potential for stakeholders seeking to capitalize on the region's growing demand for data protection solutions.

Research Methodology - How this research was conducted

The research methodology for this report on the Australia and New Zealand DPaaS market involved a comprehensive analysis of primary and secondary data sources. Primary research included interviews with industry experts, key stakeholders, and decision-makers to gather insights into market trends, competitive dynamics, and growth opportunities. Secondary research involved the analysis of industry reports, company publications, regulatory documents, and market databases to validate and supplement primary findings. The research also incorporated a detailed examination of market segmentation, regional performance, and competitive landscape to provide a holistic view of the market. Data triangulation was employed to ensure the accuracy and reliability of the findings, and the report was structured to align with the specific requirements of stakeholders seeking actionable insights into the DPaaS market.

Research Scope - Coverage and limitations

The research scope of this report on the Australia and New Zealand DPaaS market encompasses a detailed analysis of market size, growth trends, competitive landscape, and key investment opportunities. The report covers the period from 2025 to 2033, with a focus on the forecast period from 2025 to 2032. The scope includes an examination of market segmentation by deployment type, service type, and organization size, as well as a regional analysis of Australia and New Zealand. The report also provides insights into the impact of COVID-19 on the market, key company profiles, and strategic recommendations for stakeholders. However, the research is limited to the Australia and New Zealand region and does not include a global analysis. Additionally, the report does not provide detailed financial data for individual companies, as this information was not available within the scope of the research.

Key Companies and Recent Developments in the Australia and New Zealand Data Protection as a Service Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Australia and New Zealand DPaaS market is characterized by the presence of several key companies, each driving innovation and competition through recent developments. Amazon Web Services (AWS) has continued to expand its cloud infrastructure in the region, launching new data centers and enhancing its DPaaS offerings with advanced features such as AI-driven analytics. IBM Corporation has announced strategic partnerships with local technology providers to strengthen its presence in the market and offer tailored solutions to industries such as finance and healthcare. VMware, Inc. has introduced new hybrid cloud solutions designed to simplify data management across private and public cloud environments, addressing the growing demand for flexible and scalable DPaaS offerings. Acronis International GmbH has launched a series of product updates focused on improving disaster recovery capabilities, while Commvault has expanded its managed service provider (MSP) program to better serve the SME segment. These developments highlight the dynamic nature of the market and the ongoing efforts of key players to meet the evolving needs of organizations in Australia and New Zealand.