North America Electronic Design Automation Market Overview - Definition, scope, and significance

Electronic Design Automation (EDA) refers to a category of software tools used for designing electronic systems such as integrated circuits and printed circuit boards. The North America EDA market encompasses the United States and Canada, serving as a critical enabler for semiconductor innovation and electronic system development. This market plays a pivotal role in supporting the region's technological leadership in areas like artificial intelligence, 5G communications, automotive electronics, and consumer devices. EDA tools facilitate the design, simulation, verification, and testing of complex electronic components, significantly reducing time-to-market and development costs for electronics manufacturers.

North America Electronic Design Automation Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The North America EDA market is driven by several key factors including the increasing complexity of semiconductor designs, growing demand for advanced consumer electronics, and the proliferation of Internet of Things (IoT) devices. The automotive industry's shift toward electric and autonomous vehicles creates substantial opportunities for EDA tools. However, the market faces challenges such as high initial costs for EDA software licenses, the need for continuous upskilling of design engineers, and intellectual property protection concerns. Opportunities exist in emerging technologies like quantum computing, advanced packaging techniques, and the integration of artificial intelligence into EDA workflows to enhance design optimization and automation.

North America Electronic Design Automation Market Growth Trends - Current and emerging trends shaping the market

Current trends in the North America EDA market include the increasing adoption of cloud-based EDA solutions, which offer scalability and collaborative design capabilities. There is a growing emphasis on design for manufacturability (DFM) and design for testability (DFT) to improve yield and reduce production costs. The integration of machine learning algorithms into EDA tools is emerging as a significant trend, enabling faster design iterations and improved optimization. Additionally, the market is witnessing increased demand for tools that support advanced node designs below 7nm, as well as solutions for heterogeneous integration and 3D packaging technologies.

COVID-19 Impact on the North America Electronic Design Automation Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the North America EDA market through supply chain interruptions and delayed semiconductor projects. However, the crisis also accelerated digital transformation initiatives, leading to increased demand for EDA tools in sectors such as telecommunications, healthcare electronics, and remote work infrastructure. The market demonstrated resilience as companies adapted to remote work environments, with EDA vendors enhancing their cloud-based offerings and collaborative features. As the economy recovers, the EDA market is experiencing renewed growth driven by pent-up demand for advanced semiconductor designs and the expansion of 5G networks and IoT applications.

North America Electronic Design Automation Market Competitive Landscape - Major competitors and market consolidation

The North America EDA market features a mix of established players and innovative startups competing for market share. Major companies such as Cadence Design Systems, Synopsys, and Mentor Graphics dominate the market with comprehensive tool suites covering various design stages. The competitive landscape is characterized by strategic partnerships, acquisitions, and continuous innovation to address evolving design challenges. Companies are increasingly focusing on developing integrated solutions that combine multiple design capabilities and leveraging artificial intelligence to enhance tool performance. The market has seen consolidation through mergers and acquisitions, with larger players acquiring specialized technology providers to expand their product portfolios.

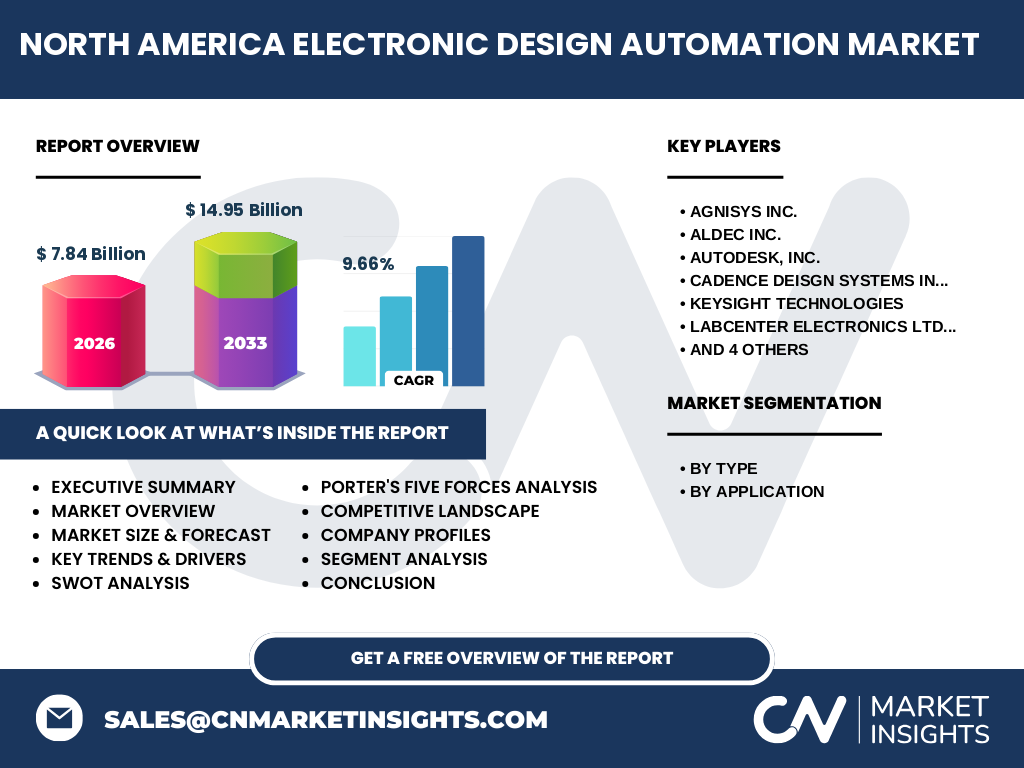

Executive Summary - High-level overview and key findings about North America Electronic Design Automation Market

The North America Electronic Design Automation market is positioned for substantial growth, driven by technological advancements and increasing demand for sophisticated electronic systems. With a projected market size of $7.84 billion in 2026 and expected to reach $14.95 billion by 2033, the market demonstrates strong growth potential with a CAGR of 9.66%. The market's expansion is fueled by the region's leadership in semiconductor innovation, the proliferation of connected devices, and the automotive industry's transformation. Key segments include CAE, SIP, IC Physical Design & Verification, and PCB & MCM, serving applications across aerospace & defense, consumer electronics, telecom, automotive, and industrial sectors. The competitive landscape features established players investing in R&D to maintain technological edge and address emerging design challenges.

North America Electronic Design Automation Market Forecast - Projections for 2025-2032 period

The North America Electronic Design Automation market is forecasted to experience robust growth between 2025 and 2032, with the market expanding from $7.84 billion in 2026 to $14.95 billion by 2033. This growth trajectory reflects a compound annual growth rate of 9.66%, indicating strong market momentum. The forecast period is expected to be characterized by increasing adoption of advanced node designs, growing demand for automotive electronics, and the expansion of 5G infrastructure. The market will likely see continued investment in cloud-based EDA solutions and AI-enhanced design tools. Segmentation by type and application will continue to evolve, with CAE and IC Physical Design & Verification segments maintaining significant market share due to their critical role in complex semiconductor designs.

North America Electronic Design Automation Market Size and Share by Segmentation - Breakdown by {segmentData}

The North America EDA market is segmented by type and application, each contributing differently to the overall market size. By type, the market includes Computer-Aided Engineering (CAE), Semiconductor Intellectual Property (SIP), IC Physical Design & Verification, and Printed Circuit Board & Multi-Chip Module (PCB & MCM) segments. Among these, CAE and IC Physical Design & Verification are expected to hold significant market share due to their essential role in complex semiconductor design processes. By application, the market serves aerospace & defense, consumer electronics, telecom, automotive, and industrial sectors. The consumer electronics and automotive segments are projected to show strong growth, driven by increasing demand for advanced electronic devices and the transformation of the automotive industry toward electric and autonomous vehicles.

Global North America Electronic Design Automation Market Size and Share by Region - Geographic distribution

While this report focuses specifically on the North American EDA market, it's important to note that North America represents a significant portion of the global EDA market. The United States, being home to major semiconductor companies and EDA tool providers, dominates the regional market share. Canada contributes through its growing semiconductor design industry and research institutions. The region's strong position is supported by substantial investments in semiconductor research and development, a robust ecosystem of electronics manufacturers, and government initiatives to maintain technological leadership. North America's market share is expected to remain strong relative to other regions, driven by continuous innovation in semiconductor technologies and the presence of leading EDA companies headquartered in the region.

Regional Analysis of the North America Electronic Design Automation Market - Detailed regional market performance

The North American EDA market exhibits varying dynamics across different regions within the continent. The United States accounts for the majority of the market share, driven by the concentration of semiconductor foundries, design houses, and EDA companies in regions like Silicon Valley, Texas, and Arizona. The U.S. market benefits from strong government support for semiconductor manufacturing through initiatives like the CHIPS Act. Canada's EDA market, while smaller, is growing steadily, supported by its expertise in wireless technologies and a strong academic research base. Regional variations in market growth are influenced by factors such as the presence of electronics manufacturing clusters, availability of skilled workforce, and local government policies supporting technological innovation and semiconductor development.

Leading Company Profiles in the North America Electronic Design Automation Market - Industry players and strategies

The North American EDA market features several leading companies that shape the industry landscape. Cadence Design Systems and Synopsys are prominent players offering comprehensive EDA tool suites covering various design stages. Mentor Graphics, now part of Siemens, provides specialized solutions for complex system designs. Keysight Technologies focuses on electronic design and test solutions, while Autodesk brings expertise in PCB design and simulation. Companies like Agnisys, Aldec, Labcenter Electronics, Silvaco, and Zuken offer niche solutions and specialized tools. These companies employ strategies such as continuous product innovation, strategic acquisitions to expand capabilities, and partnerships with semiconductor companies to maintain their competitive edge. They are increasingly focusing on integrating artificial intelligence and cloud technologies into their offerings to address evolving design challenges.

Porter's Five Forces Analysis of the North America Electronic Design Automation Market - Competitive forces assessment

Applying Porter's Five Forces analysis to the North American EDA market reveals several key insights. The threat of new entrants is moderate due to high barriers to entry, including the need for substantial R&D investment and established customer relationships. Bargaining power of buyers is relatively high as large semiconductor companies can influence pricing and demand customized solutions. The bargaining power of suppliers is low as EDA companies primarily rely on their in-house technology and expertise. The threat of substitute products is low as EDA tools are essential for semiconductor design with no direct alternatives. Competitive rivalry is intense among established players, driving continuous innovation and leading to frequent product updates and feature enhancements. The analysis suggests that success in this market requires strong technological capabilities, comprehensive product portfolios, and effective customer relationships.

SWOT Analysis of the North America Electronic Design Automation Market - Strengths, weaknesses, opportunities, threats

The North American EDA market exhibits several strengths including technological leadership, a robust ecosystem of semiconductor companies, and strong intellectual property protection. The region's weaknesses include high costs associated with EDA tools and the need for continuous upskilling of design engineers. Opportunities abound in emerging technologies such as AI-enhanced design tools, cloud-based solutions, and advanced packaging techniques. However, the market faces threats from global competition, particularly from Asia-Pacific regions investing heavily in semiconductor capabilities, and potential economic downturns affecting electronics demand. The market's ability to capitalize on opportunities while mitigating threats will be crucial for sustained growth, with companies needing to balance innovation investments with cost considerations and adapt to changing technological landscapes.

North America Electronic Design Automation Market Value Chain Analysis - Industry structure and value flow

The value chain in the North American EDA market encompasses several key stages, starting with research and development of design tools and algorithms. This is followed by software development, testing, and validation processes. The distribution stage involves direct sales to large semiconductor companies and indirect channels for smaller customers. Value is added through continuous innovation in design methodologies, integration of artificial intelligence for enhanced tool performance, and provision of comprehensive support and training services. The end-users, primarily semiconductor companies and electronics manufacturers, derive value through improved design efficiency, reduced time-to-market, and enhanced product performance. The value chain is characterized by close collaboration between EDA companies and their customers to address specific design challenges and optimize tool performance for emerging technologies.

Key Investment Insights in the North America Electronic Design Automation Market - Strategic investment recommendations

Investment opportunities in the North American EDA market are driven by several key factors. Investors should consider companies that are leading in the development of AI-enhanced design tools, as this represents a significant growth area. Cloud-based EDA solutions present another attractive investment avenue, given the industry's shift towards scalable and collaborative design environments. Companies focusing on advanced node designs and heterogeneous integration technologies are well-positioned for growth as semiconductor manufacturing continues to push technological boundaries. Additionally, investments in startups offering innovative solutions for specific design challenges or emerging applications like quantum computing design could yield significant returns. However, investors should be mindful of the cyclical nature of the semiconductor industry and the high R&D costs associated with EDA tool development.

North America Electronic Design Automation Market Conclusion - Summary and key takeaways

The North American Electronic Design Automation market presents a compelling growth story, with the market projected to expand from $7.84 billion in 2026 to $14.95 billion by 2033, representing a robust CAGR of 9.66%. This growth is underpinned by the region's technological leadership, increasing complexity of semiconductor designs, and the proliferation of advanced electronic systems across various industries. The market's segmentation by type and application reflects the diverse needs of the electronics industry, with CAE and IC Physical Design & Verification tools playing crucial roles. While facing challenges such as high costs and intense competition, the market offers significant opportunities in emerging technologies and applications. Companies that can innovate continuously, integrate AI and cloud technologies, and address specific industry needs are likely to thrive in this dynamic market landscape.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research sources. Primary research involved interviews with industry experts, EDA tool users, and company representatives to gather insights on market trends, challenges, and growth drivers. Secondary research included analysis of company annual reports, industry publications, and market databases to validate findings and gather quantitative data. The research methodology employed both top-down and bottom-up approaches to estimate market size and forecast future growth. Segmentation analysis was performed based on type and application, with careful consideration of regional dynamics within North America. The research team cross-validated findings through multiple sources to ensure accuracy and reliability of the market projections and insights presented in this report.

Research Scope - Coverage and limitations

This research report covers the Electronic Design Automation market in North America, focusing on the United States and Canada. The scope includes analysis of market size, growth trends, competitive landscape, and segmentation by type and application. The report examines key market drivers, restraints, and opportunities, providing insights into the impact of COVID-19 and future growth projections from 2025 to 2032. While the report offers comprehensive coverage of the market, it has certain limitations. The analysis is primarily focused on commercial EDA tools and may not fully capture open-source alternatives. Additionally, the report's scope is limited to North America, and while it provides context for the global market, detailed analysis of other regions is not included. The research also focuses on mainstream EDA applications and may not extensively cover highly specialized or emerging use cases.

Key Companies and Recent Developments in the North America Electronic Design Automation Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The North American EDA market features several key players driving innovation and competition. Cadence Design Systems has been focusing on AI-driven design solutions and recently announced advancements in computational software for chip design. Synopsys continues to strengthen its position with new product launches in verification and simulation tools, along with strategic acquisitions to expand its IP portfolio. Mentor Graphics, under Siemens, has been enhancing its system design capabilities and announced partnerships to improve automotive electronics design workflows. Keysight Technologies has been expanding its 5G design and test solutions, with recent product launches targeting emerging wireless technologies. Autodesk has been strengthening its PCB design offerings and announced cloud-based collaboration features. Companies like Agnisys, Aldec, and Zuken have been focusing on specialized solutions, with recent developments in register automation and FPGA design tools. These companies are continuously innovating to address the increasing complexity of semiconductor designs and emerging application requirements.