Fuel Cell Market Overview - Definition, scope, and significance

Fuel cells are electrochemical devices that convert chemical energy from a fuel, typically hydrogen, into electricity through a reaction with oxygen or another oxidizing agent. Unlike conventional combustion-based power generation, fuel cells produce electricity through an electrochemical process that is cleaner and more efficient. The fuel cell market encompasses various types of fuel cell technologies including Proton Exchange Membrane Fuel Cells (PEMFC), Phosphoric Acid Fuel Cells (PAFC), and Solid Oxide Fuel Cells (SOFC), serving applications across transportation, portable power, and stationary power generation. The significance of this market lies in its potential to address global energy challenges by providing a sustainable alternative to fossil fuels, reducing greenhouse gas emissions, and enabling energy security through diverse fuel sources.

Fuel Cell Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The fuel cell market is driven by several key factors including increasing environmental concerns and stringent emission regulations worldwide, growing demand for clean energy solutions, and technological advancements that have improved fuel cell efficiency and reduced costs. Government initiatives and incentives supporting hydrogen infrastructure development and fuel cell adoption also serve as major drivers. However, the market faces restraints such as high initial costs, limited hydrogen refueling infrastructure, and competition from other clean energy technologies like batteries. Challenges include hydrogen production and storage complexities, durability issues, and the need for specialized materials. Opportunities exist in expanding applications across various sectors, particularly in heavy-duty transportation, backup power systems, and integration with renewable energy sources for energy storage solutions.

Fuel Cell Market Growth Trends - Current and emerging trends shaping the market

The fuel cell market is experiencing several notable growth trends, including the increasing adoption of fuel cell electric vehicles (FCEVs) in the automotive sector, particularly for commercial and heavy-duty applications where battery limitations are more pronounced. There is a growing trend toward the development of green hydrogen production through electrolysis powered by renewable energy sources, which enhances the environmental benefits of fuel cells. The market is also witnessing increased integration of fuel cells in microgrids and distributed power generation systems, providing reliable backup power and grid stability. Additionally, technological innovations are driving trends toward smaller, more efficient fuel cell systems for portable and consumer electronics applications, while advancements in materials science are improving durability and reducing costs across all fuel cell types.

COVID-19 Impact on the Fuel Cell Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic initially disrupted the fuel cell market through supply chain interruptions, project delays, and reduced investments as industries focused on immediate survival rather than long-term clean energy transitions. Manufacturing facilities faced temporary closures, and the deployment of fuel cell projects experienced setbacks due to lockdowns and social distancing measures. However, the pandemic also highlighted the importance of resilient and sustainable energy systems, potentially accelerating interest in fuel cell technologies as part of green recovery initiatives. The recovery trajectory shows positive momentum as governments worldwide incorporate hydrogen and fuel cell technologies into their economic stimulus packages and climate action plans. The market is gradually recovering with renewed focus on building more sustainable and resilient energy infrastructure for the future.

Fuel Cell Market Competitive Landscape - Major competitors and market consolidation

The fuel cell market features a competitive landscape with both established industrial giants and specialized fuel cell companies vying for market share. Major competitors include Ballard Power Systems, known for its leadership in PEM fuel cell technology for transportation and stationary applications; Bloom Energy, a prominent player in solid oxide fuel cells for stationary power generation; and Plug Power, which has established a strong presence in hydrogen fuel cell solutions for material handling and logistics. The market is witnessing increasing consolidation as larger companies acquire specialized fuel cell technology providers to strengthen their positions. Strategic partnerships between fuel cell manufacturers, automotive companies, and energy providers are becoming more common, creating integrated ecosystems for hydrogen production, distribution, and utilization. This competitive environment is driving innovation and scale economies while also creating barriers to entry for new players.

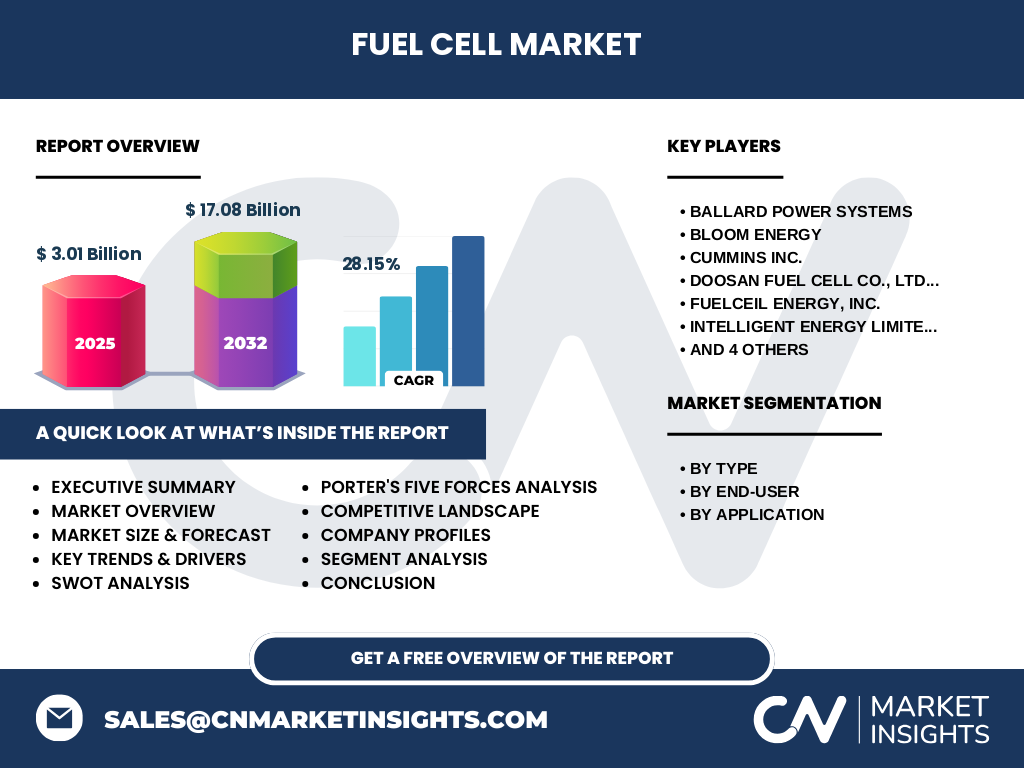

Executive Summary - High-level overview and key findings about Fuel Cell Market

The global fuel cell market is positioned for substantial growth, with projections indicating expansion from $3.01 billion in 2025 to $17.08 billion by 2032, representing a robust CAGR of 28.15%. This growth is underpinned by increasing environmental regulations, technological advancements, and growing recognition of fuel cells as a viable clean energy solution. The market is segmented by type, end-user, and application, with Proton Exchange Membrane Fuel Cells leading the technology segment due to their versatility and efficiency. Key applications span transportation, particularly in fuel cell vehicles, utilities for stationary power generation, and defense applications. The competitive landscape features both established industrial players and specialized fuel cell companies, with strategic partnerships and consolidation shaping the market dynamics. Despite challenges related to infrastructure and costs, the market presents significant opportunities for investors and stakeholders committed to the clean energy transition.

Fuel Cell Market Forecast - Projections for 2025-2032 period

The fuel cell market is projected to experience remarkable growth over the 2025-2032 period, expanding from a market size of $3.01 billion in 2025 to an estimated $17.08 billion by 2032. This represents a compound annual growth rate (CAGR) of 28.15%, indicating strong market momentum and increasing adoption across various applications. The forecast period will likely see accelerated growth driven by declining technology costs, expanding hydrogen infrastructure, and supportive government policies worldwide. Key growth drivers during this period include the commercialization of fuel cell vehicles, particularly in heavy-duty transportation, increased deployment of stationary fuel cells for backup power and grid services, and growing demand for clean energy solutions in industrial applications. The market is expected to witness regional variations in growth rates, with Asia-Pacific potentially leading due to strong government support in countries like Japan, South Korea, and China.

Fuel Cell Market Size and Share by Segmentation - Breakdown by {segmentData}

The fuel cell market segmentation reveals distinct patterns in technology adoption and application preferences. By type, Proton Exchange Membrane Fuel Cells (PEMFC) currently dominate the market due to their versatility, quick startup times, and suitability for both transportation and stationary applications. Phosphoric Acid Fuel Cells (PAFC) hold a significant share in the stationary power generation segment, particularly for commercial and industrial applications requiring reliable baseload power. Solid Oxide Fuel Cells (SOFC) are gaining traction in high-efficiency stationary applications and are expected to capture increasing market share due to their fuel flexibility and high electrical efficiency. By end-user, the utilities segment represents a substantial portion of the market, driven by the need for clean, reliable power generation. The transportation segment, particularly fuel cell vehicles, is emerging as a high-growth area, while the defense sector utilizes fuel cells for portable power and unmanned systems. Application-wise, the stationary segment currently leads due to established deployments, followed by the growing transport segment and the emerging portable applications.

Global Fuel Cell Market Size and Share by Region - Geographic distribution

The global fuel cell market exhibits distinct regional patterns in adoption and growth, influenced by varying policy frameworks, infrastructure development, and industrial capabilities. Asia-Pacific currently leads the global market, driven by strong government support in countries like Japan, South Korea, and China, which have implemented comprehensive hydrogen strategies and invested heavily in fuel cell technology development. North America represents the second-largest market, with the United States showing significant growth in fuel cell vehicle adoption and stationary power applications, supported by federal and state-level incentives. Europe is rapidly emerging as a key market, with the European Union's hydrogen strategy and various national hydrogen roadmaps driving investments in fuel cell technology and infrastructure. The region is expected to witness accelerated growth during the forecast period as countries work toward their carbon neutrality goals. Other regions, including Latin America and the Middle East & Africa, are in earlier stages of fuel cell adoption but present growing opportunities as infrastructure develops and costs decline.

Regional Analysis of the Fuel Cell Market - Detailed regional market performance

Regional analysis of the fuel cell market reveals distinct performance patterns and growth drivers across different geographies. In Asia-Pacific, Japan has been a pioneer in fuel cell adoption, with extensive deployments of residential fuel cell systems (ENE-FARM) and ambitious targets for hydrogen utilization. South Korea has emerged as a leader in fuel cell manufacturing and deployment, with companies like Doosan Fuel Cell establishing significant production capacity and the government targeting leadership in the global hydrogen economy. China is rapidly scaling up its fuel cell industry, focusing on commercial vehicles and establishing large-scale production facilities. In North America, the United States shows strong growth in material handling applications, with companies like Plug Power dominating the forklift market, while California leads in fuel cell vehicle deployment and hydrogen station development. Canada leverages its abundant hydrogen production capabilities and has established itself as a center for fuel cell technology development, particularly in British Columbia. Europe's regional performance is characterized by Germany's leadership in automotive fuel cell development, France's focus on hydrogen production and industrial applications, and the Nordic countries' emphasis on green hydrogen production through electrolysis powered by renewable energy.

Leading Company Profiles in the Fuel Cell Market - Industry players and strategies

The fuel cell market features several leading companies with distinct strategic approaches and technological specializations. Ballard Power Systems has established itself as a global leader in PEM fuel cell technology, focusing on heavy-duty transportation applications including buses, trucks, and trains, while also serving the material handling and backup power markets. Bloom Energy specializes in solid oxide fuel cell technology for stationary power generation, targeting commercial, industrial, and data center applications with its Energy Server platform. Cummins Inc. has expanded its portfolio through strategic acquisitions in the fuel cell space, positioning itself as a comprehensive provider of hydrogen and fuel cell solutions across multiple applications. Doosan Fuel Cell Co., Ltd. focuses on PAFC technology for stationary power generation, particularly in South Korea and expanding internationally. FuelCell Energy, Inc. develops carbonate fuel cell technology for utility-scale power generation and carbon capture applications. Plug Power Inc. has built a strong position in hydrogen fuel cell solutions for material handling and is expanding into on-road vehicles and green hydrogen production. These companies employ various strategies including vertical integration, strategic partnerships, and geographic expansion to strengthen their market positions.

Porter's Five Forces Analysis of the Fuel Cell Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the fuel cell market. The threat of new entrants is moderate to high, as the market requires significant capital investment and technical expertise, creating barriers to entry, but growing demand and technological advancements are attracting new players. The bargaining power of suppliers is relatively high due to the specialized materials required for fuel cell production, including platinum catalysts and membrane electrode assemblies, though this is gradually decreasing as supply chains mature and alternative materials are developed. The bargaining power of buyers is increasing as the market grows and more alternatives become available, particularly in the transportation sector where fuel cells compete with batteries. The threat of substitutes is significant, with battery electric vehicles and other renewable energy technologies serving as alternatives in many applications, though fuel cells offer distinct advantages in certain use cases such as long-range transportation and continuous power generation. Competitive rivalry is intense among existing players, driving innovation and cost reduction efforts, with companies competing on technology performance, cost, and application-specific solutions.

SWOT Analysis of the Fuel Cell Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the fuel cell market reveals several key factors influencing its development. Strengths include the technology's high efficiency compared to conventional power generation, zero emissions at point of use, fuel flexibility allowing operation on various hydrogen sources, and modular scalability across different power ranges. Weaknesses encompass high initial costs, limited hydrogen infrastructure, durability challenges particularly for automotive applications, and sensitivity to fuel impurities. Opportunities abound in the growing demand for clean energy solutions, expanding applications in heavy-duty transportation where batteries face limitations, integration with renewable energy for energy storage, and government initiatives supporting hydrogen economies worldwide. Threats include intense competition from alternative technologies particularly batteries, potential delays in hydrogen infrastructure development, regulatory uncertainties, and the challenge of reducing costs to achieve parity with conventional technologies. The market's ability to leverage its strengths and opportunities while addressing weaknesses and threats will determine its long-term success and adoption rate.

Fuel Cell Market Value Chain Analysis - Industry structure and value flow

The fuel cell market value chain encompasses multiple stages from raw material sourcing to end-user applications, with distinct players and value-adding activities at each level. The upstream segment includes suppliers of critical materials such as platinum catalysts, membrane electrode assemblies, bipolar plates, and other specialized components essential for fuel cell stack manufacturing. The midstream segment comprises fuel cell system integrators and manufacturers who assemble stacks into complete systems, incorporating balance of plant components including fuel processors, power conditioners, and control systems. This segment also includes hydrogen production and delivery infrastructure providers, ranging from industrial gas companies to electrolysis equipment manufacturers. The downstream segment consists of system integrators who incorporate fuel cell systems into specific applications, distributors and dealers who bring these solutions to market, and end-users across various sectors including transportation, utilities, and industrial applications. Value flows through this chain as technological innovations reduce costs, scale economies improve competitiveness, and integration across the value chain creates more comprehensive solutions for end-users.

Key Investment Insights in the Fuel Cell Market - Strategic investment recommendations

The fuel cell market presents compelling investment opportunities driven by its projected high growth rate and increasing role in the clean energy transition. Strategic investment recommendations include focusing on companies with strong technological differentiation and intellectual property portfolios, particularly those developing next-generation fuel cell technologies with improved efficiency and reduced costs. Investors should consider opportunities across the value chain, from upstream material suppliers developing alternative catalysts to reduce dependency on platinum, to midstream system manufacturers achieving scale economies, to downstream application developers targeting high-growth segments like heavy-duty transportation and stationary power. Geographic diversification is recommended, with particular attention to regions with strong policy support such as Asia-Pacific and Europe. Investments in hydrogen infrastructure development, including production, storage, and distribution, represent strategic opportunities as this remains a key enabler for fuel cell adoption. Additionally, companies integrating fuel cells with renewable energy systems for energy storage applications present attractive investment prospects as the market for grid-scale energy storage expands.

Fuel Cell Market Conclusion - Summary and key takeaways

The fuel cell market stands at a pivotal juncture, characterized by strong growth projections, technological advancements, and increasing recognition of its role in the clean energy transition. With the market expected to grow from $3.01 billion in 2025 to $17.08 billion by 2032 at a CAGR of 28.15%, the industry demonstrates significant potential for expansion across multiple applications and regions. Key takeaways include the dominance of PEM fuel cell technology, the growing importance of transportation applications particularly for heavy-duty vehicles, and the leadership of Asia-Pacific in market adoption driven by strong government support. While challenges related to costs and infrastructure remain, opportunities in renewable hydrogen production, energy storage integration, and expanding applications present pathways for continued growth. The competitive landscape features both established industrial players and specialized fuel cell companies, with strategic partnerships and consolidation shaping market dynamics. Success in this market will depend on continued technological innovation, cost reduction efforts, and the development of comprehensive hydrogen ecosystems that address infrastructure limitations.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches to ensure accuracy and reliability. Secondary research involved extensive analysis of industry reports, company financial statements, technical publications, patent databases, and government policy documents to establish baseline market data and trends. Primary research included interviews with industry experts, fuel cell manufacturers, technology developers, and end-users across different applications and regions to validate findings and gain insights into market dynamics. Market size and forecast calculations were based on bottom-up analysis of individual market segments, considering factors such as technology adoption rates, application-specific requirements, and regional policy frameworks. Data triangulation was employed to cross-verify information from multiple sources, while assumptions and limitations were clearly documented. The research methodology prioritized data accuracy and relevance, with particular attention to emerging trends and technological developments that could impact future market trajectories.

Research Scope - Coverage and limitations

This research scope encompasses a comprehensive analysis of the global fuel cell market, covering major fuel cell technologies including Proton Exchange Membrane Fuel Cells (PEMFC), Phosphoric Acid Fuel Cells (PAFC), and Solid Oxide Fuel Cells (SOFC). The study examines key applications across transportation (fuel cell vehicles), utilities (stationary power generation), and defense sectors, with geographic coverage spanning North America, Europe, Asia-Pacific, and the rest of the world. The research timeframe extends from historical data through 2025 to forecasts through 2032, providing both retrospective analysis and forward-looking projections. Limitations of the research include the inherent challenges in forecasting emerging technologies, potential variations in regional policy implementation that could affect adoption rates, and the difficulty in quantifying certain market drivers such as consumer acceptance and infrastructure development timelines. The scope focuses on commercial and near-commercial fuel cell technologies, excluding experimental or conceptual applications that lack clear commercialization pathways within the forecast period.

Key Companies and Recent Developments in the Fuel Cell Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The fuel cell market features several key companies driving technological innovation and market expansion through strategic developments. Ballard Power Systems recently announced expanded production capacity for its fuel cell engines to meet growing demand in heavy-duty transportation applications, while also securing new partnerships with major automotive manufacturers for fuel cell vehicle development. Bloom Energy launched its next-generation solid oxide fuel cell platform with improved efficiency and expanded fuel flexibility, targeting data center and microgrid applications. Cummins Inc. made strategic acquisitions in the fuel cell space to strengthen its hydrogen technology portfolio and announced plans for large-scale fuel cell system manufacturing facilities. Doosan Fuel Cell Co., Ltd. expanded its stationary fuel cell business with new projects in South Korea and international markets, focusing on utility-scale power generation. FuelCell Energy, Inc. announced advancements in its carbonate fuel cell technology for carbon capture applications, securing partnerships with utilities for demonstration projects. Plug Power Inc. made significant progress in its green hydrogen production initiatives, announcing multiple electrolyzer projects and expanding its ecosystem approach to include hydrogen production, distribution, and fueling infrastructure. These developments reflect the industry's focus on scaling production, expanding applications, and creating integrated hydrogen solutions to drive market growth.