What is the Dairy Starter Culture Market and why is it significant?

Dairy starter cultures are carefully selected microorganisms, primarily bacteria, used in the production of fermented dairy products to initiate and control the fermentation process. These cultures are essential for transforming milk into products like yogurt, cheese, buttermilk, sour cream, and ripened butter. The significance of this market lies in its critical role in food preservation, flavor development, texture enhancement, and nutritional improvement of dairy products. Starter cultures not only ensure consistent product quality and safety by inhibiting harmful bacteria but also contribute to the distinctive characteristics that consumers expect from fermented dairy products. As global dairy consumption continues to rise and consumer preferences shift toward probiotic-rich and artisanal dairy products, the dairy starter culture market has become increasingly important in meeting both industrial-scale production needs and specialized artisanal requirements.

What are the key drivers, restraints, challenges, and opportunities in the Dairy Starter Culture Market?

The dairy starter culture market is driven by several factors including the growing global demand for fermented dairy products, increasing consumer awareness of probiotic health benefits, technological advancements in culture development, and the expansion of the dairy industry in emerging markets. The rising popularity of functional foods and the trend toward natural and clean-label products further accelerate market growth. However, the market faces restraints such as stringent regulatory requirements for microbial cultures, the high cost of research and development, and the need for specialized storage and transportation conditions. Challenges include maintaining culture viability throughout the supply chain and meeting diverse consumer taste preferences across different regions. Opportunities exist in developing novel strains with enhanced functionalities, expanding into plant-based dairy alternatives, and leveraging biotechnology to create cultures with improved fermentation efficiency and health benefits.

What are the current and emerging growth trends in the Dairy Starter Culture Market?

The dairy starter culture market is experiencing several notable growth trends. There is a significant shift toward multi-strain cultures that offer enhanced flavor complexity and functional benefits compared to single-strain options. The market is also witnessing increased demand for thermophilic bacteria cultures used in yogurt and Italian cheese production, driven by the popularity of these products globally. Another emerging trend is the development of cultures specifically designed for reduced fermentation time, which helps manufacturers improve production efficiency. The industry is also moving toward cultures with enhanced probiotic properties to meet growing consumer health consciousness. Additionally, there is a trend toward customized starter cultures tailored to regional taste preferences and specific product requirements. The integration of digital technologies for culture monitoring and quality control is also gaining traction, enabling more precise fermentation management.

How did the COVID-19 pandemic impact the Dairy Starter Culture Market?

The COVID-19 pandemic had a mixed impact on the dairy starter culture market. Initially, the market experienced disruptions in supply chains, production facilities, and distribution networks due to lockdowns and restrictions. The closure of restaurants, cafes, and food service establishments temporarily reduced demand for certain dairy products, indirectly affecting starter culture consumption. However, the pandemic also led to increased at-home consumption of dairy products, particularly yogurt and other fermented foods perceived as healthy and immune-boosting. This shift partially offset the decline in food service demand. The market demonstrated resilience as dairy manufacturers adapted to new safety protocols and shifted production to meet changing consumer preferences. Looking forward, the pandemic has accelerated trends toward health-conscious eating and increased interest in fermented foods, which is expected to support market recovery and growth in the post-pandemic period.

What is the competitive landscape of the Dairy Starter Culture Market?

The dairy starter culture market is characterized by a mix of global players and regional specialists, creating a moderately consolidated competitive landscape. Major international companies dominate the market with their extensive product portfolios, global distribution networks, and significant research and development capabilities. These leading players compete on factors such as product quality, innovation, technical support, and price. The market has seen strategic activities including mergers and acquisitions, partnerships, and collaborations aimed at expanding product offerings and geographic presence. Competition is intensifying as companies focus on developing specialized cultures for niche applications and differentiated products with enhanced functionalities. Regional players maintain their position by offering customized solutions and leveraging their understanding of local market preferences. The competitive environment is further shaped by the entry of biotechnology firms bringing innovative microbial solutions to the market.

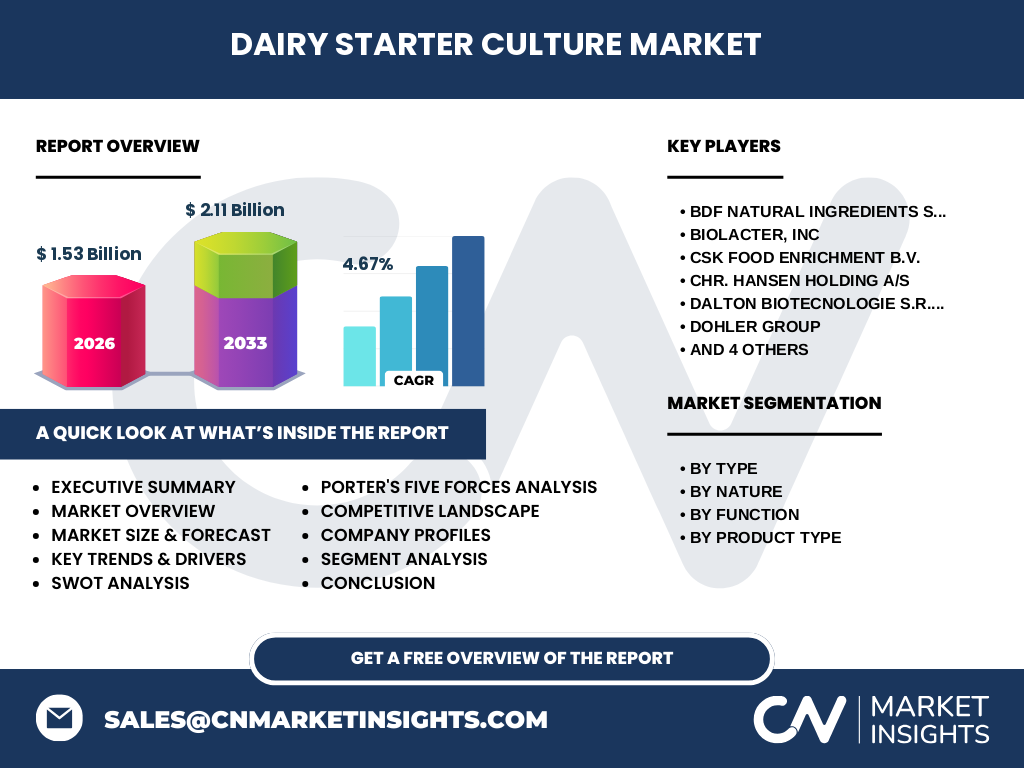

What are the key findings and high-level overview of the Dairy Starter Culture Market?

The dairy starter culture market presents a promising growth trajectory with a projected CAGR of 4.67% from 2027 to 2033, reaching an estimated value of 2.11 billion by 2033. The market demonstrates robust fundamentals driven by the essential role of starter cultures in dairy fermentation and the continuous innovation in microbial strains. Key findings indicate strong demand across various product segments, with cheese and yogurt applications leading consumption. The market shows healthy segmentation with both mesophilic and thermophilic bacteria cultures finding significant applications, while multi-strain cultures are gaining preference over single-strain options for their enhanced functional benefits. Geographically, the market exhibits diverse growth patterns with developed regions focusing on premium and specialized cultures while emerging markets drive volume growth. The competitive landscape remains dynamic with established players and innovative entrants contributing to market evolution through technological advancements and strategic initiatives.

What is the market forecast for the Dairy Starter Culture Market from 2025 to 2032?

The dairy starter culture market is projected to experience steady growth throughout the forecast period of 2025-2032, with the market expected to reach 2.11 billion by 2033, growing at a CAGR of 4.67%. This growth trajectory reflects the increasing global demand for fermented dairy products, technological advancements in culture development, and expanding applications across various dairy segments. The forecast period is expected to witness significant opportunities in emerging markets where dairy consumption is rising, coupled with growing awareness of probiotic benefits. The market is likely to see continued innovation in culture strains offering improved fermentation efficiency, enhanced flavor profiles, and additional health benefits. Challenges such as regulatory compliance and maintaining culture viability during storage and transportation may influence the growth rate, but overall market fundamentals remain strong. The forecast also indicates potential for market expansion through the development of cultures for plant-based dairy alternatives and specialized applications.

How is the Dairy Starter Culture Market segmented by type, nature, function, and product type?

The dairy starter culture market is segmented across multiple dimensions to provide a comprehensive understanding of its structure. By type, the market is divided into mesophilic bacteria and thermophilic bacteria, with mesophilic cultures typically used in products like buttermilk and sour cream, while thermophilic cultures are essential for yogurt and certain cheese varieties. By nature, the market distinguishes between single strain types, which contain one bacterial strain, and multi-strain types, which combine multiple strains for enhanced functionality and flavor complexity. By function, cultures are categorized based on their primary purpose: acid production cultures that lower pH for preservation and texture, and flavor production cultures that develop distinctive taste profiles. By product type, the market encompasses buttermilk, cheese, ripened butter, sour cream, and yogurt applications, with cheese representing one of the largest segments due to the diverse range of cheese varieties requiring specific cultures.

How is the global Dairy Starter Culture Market distributed across different regions?

The global dairy starter culture market exhibits distinct regional patterns influenced by dairy consumption habits, production capabilities, and economic development levels. Developed regions such as North America and Europe represent mature markets with high per capita dairy consumption and sophisticated production techniques, driving demand for premium and specialized cultures. These regions are characterized by strong innovation capabilities and stringent quality standards. The Asia-Pacific region is emerging as a high-growth market, driven by increasing dairy consumption, rising disposable incomes, and growing awareness of fermented food benefits, particularly in countries like China, India, and Southeast Asian nations. Latin America shows steady growth potential with its established dairy traditions and expanding production capacity. The Middle East and Africa region, while currently smaller in market size, presents opportunities for growth as dairy infrastructure develops and consumption patterns evolve. Regional differences in taste preferences and regulatory environments significantly influence market dynamics across geographies.

What is the detailed regional analysis of the Dairy Starter Culture Market?

Regional analysis reveals distinct market characteristics and growth drivers across different geographies. In North America, the market benefits from advanced dairy processing infrastructure, high consumer awareness of probiotic benefits, and strong demand for Greek yogurt and artisanal cheeses, driving innovation in culture development. Europe, with its rich cheese-making traditions and strict quality standards, represents a mature market focused on premium cultures and specialized strains for traditional products. The Asia-Pacific region shows the fastest growth rate, fueled by changing dietary habits, urbanization, and increasing Western influence on food preferences, particularly in China and India where yogurt consumption is rising rapidly. Latin America demonstrates steady growth supported by its established dairy industry and growing middle class, with particular emphasis on cheese production. The Middle East and Africa region, though currently smaller, shows potential for expansion as dairy consumption increases and production capabilities improve, with a focus on meeting local taste preferences and religious dietary requirements.

Who are the leading companies in the Dairy Starter Culture Market and what are their strategies?

The dairy starter culture market features several prominent players with distinct strategic approaches. Chr. Hansen Holding A/S stands out as a global leader with its extensive portfolio of microbial solutions and strong focus on research and development, particularly in developing cultures with enhanced functional properties. Lallemand Inc. has established itself through its comprehensive range of cultures and strategic acquisitions to expand its market presence. Dohler Group leverages its expertise in natural ingredients to offer innovative culture solutions, while The Dow Chemical Company brings its technological capabilities to enhance culture stability and performance. BDF Natural Ingredients S.L. and Biolacter, Inc focus on specialized and natural culture solutions, catering to niche market segments. Sacco System and Dalton Biotecnologie S.R.L. emphasize their Italian heritage and expertise in cheese-making cultures. These companies employ strategies including product innovation, strategic partnerships, geographic expansion, and investments in biotechnology to strengthen their market positions and meet evolving customer needs.

What does Porter's Five Forces analysis reveal about the Dairy Starter Culture Market?

Porter's Five Forces analysis provides valuable insights into the competitive dynamics of the dairy starter culture market. The threat of new entrants is moderate due to the specialized knowledge required for culture development, regulatory requirements, and the need for significant R&D investments, though opportunities exist for biotechnology startups with innovative approaches. The bargaining power of buyers is relatively high, particularly for large dairy manufacturers who can switch suppliers and demand customized solutions, though this is somewhat balanced by the technical expertise required to effectively utilize cultures. Suppliers of raw materials and equipment have moderate bargaining power due to the specialized nature of inputs required for culture production. The threat of substitute products is low as starter cultures are essential for traditional fermented dairy production, though emerging plant-based alternatives present a potential long-term consideration. Competitive rivalry is intense among established players, driven by product differentiation, technological innovation, and the need to meet diverse customer requirements across different dairy applications.

What are the strengths, weaknesses, opportunities, and threats in the Dairy Starter Culture Market?

A SWOT analysis of the dairy starter culture market reveals several key factors. Strengths include the essential nature of starter cultures in dairy fermentation, continuous technological advancements enabling improved culture performance, and the growing consumer demand for fermented and probiotic-rich products. The market also benefits from established distribution networks and strong relationships between culture suppliers and dairy manufacturers. Weaknesses include the high costs associated with research and development, the complexity of maintaining culture viability throughout the supply chain, and vulnerability to fluctuations in raw material prices. Opportunities exist in expanding into emerging markets with growing dairy consumption, developing cultures for plant-based alternatives, and leveraging biotechnology for enhanced functionality. Threats include stringent regulatory requirements across different regions, potential contamination risks affecting product quality, and increasing competition from both established players and innovative startups. The market also faces challenges from changing consumer preferences and the need to continuously adapt to evolving dairy industry trends.

How does the value chain operate in the Dairy Starter Culture Market?

The dairy starter culture value chain encompasses several interconnected stages from raw material sourcing to end-user application. The process begins with the sourcing of high-quality raw materials including milk substrates and specialized growth media necessary for culture cultivation. Culture development and production involve sophisticated fermentation processes, strain selection, and quality control measures to ensure consistent performance. The supply chain includes specialized storage and transportation requirements to maintain culture viability, with cold chain logistics playing a critical role. Distribution channels involve direct sales to large dairy manufacturers, partnerships with dairy equipment suppliers, and distribution through specialized food ingredient distributors. Technical support and application services form an important part of the value chain, with suppliers providing expertise in culture selection and fermentation optimization. The value chain is characterized by close collaboration between culture suppliers and dairy manufacturers to develop customized solutions that meet specific product requirements and quality standards.

What are the key investment insights for the Dairy Starter Culture Market?

The dairy starter culture market presents several compelling investment opportunities driven by its essential role in the growing dairy industry and continuous innovation potential. Strategic investments in research and development are crucial for developing next-generation cultures with enhanced functionalities, improved fermentation efficiency, and additional health benefits. There is significant potential in expanding production capacity to serve emerging markets where dairy consumption is rising rapidly. Investments in biotechnology and genetic engineering could yield cultures with superior performance characteristics and novel applications. The market also offers opportunities for vertical integration, particularly in cold chain logistics and technical support services. Investors should consider the growing trend toward natural and clean-label products, which favors cultures with minimal processing and clear consumer benefits. Strategic acquisitions of regional players or specialized culture developers could provide market access and technological capabilities. However, investments should be balanced against regulatory challenges and the need for specialized expertise in microbial cultivation and quality control.

What are the key takeaways and summary of the Dairy Starter Culture Market?

The dairy starter culture market represents a vital and growing segment of the global food industry, driven by the essential role of cultures in dairy fermentation and the continuous evolution of consumer preferences. With a projected market value of 2.11 billion by 2033 and a healthy CAGR of 4.67%, the market demonstrates strong fundamentals and promising growth potential. Key takeaways include the increasing demand for multi-strain cultures, the growing importance of thermophilic cultures for yogurt and cheese production, and the expanding applications across various dairy segments. The market is characterized by a mix of global leaders and regional specialists, with competition centered on innovation, quality, and technical support. Regional dynamics show mature markets in developed regions driving premiumization while emerging markets offer volume growth opportunities. The market's future will be shaped by technological advancements, regulatory developments, and changing consumer preferences toward healthier and more natural dairy products.

How was the research for this Dairy Starter Culture Market conducted?

The research methodology for this dairy starter culture market analysis employed a comprehensive and multi-faceted approach to ensure accuracy and reliability. Primary research involved interviews with industry experts, including culture manufacturers, dairy processors, and food scientists, to gather firsthand insights into market dynamics, technological developments, and future trends. Secondary research encompassed extensive review of industry reports, academic publications, company financial statements, and regulatory documents to build a robust database of market information. Data triangulation techniques were applied to validate findings across multiple sources, ensuring consistency and reliability. Market size and forecast calculations were based on both top-down and bottom-up approaches, considering factors such as dairy production volumes, culture consumption rates, and regional market characteristics. The research also incorporated analysis of patent filings, new product launches, and strategic corporate activities to identify innovation trends and competitive positioning. Special attention was given to understanding regional variations in market structure, regulatory environments, and consumer preferences to provide a comprehensive global perspective.

What is the scope and coverage of this Dairy Starter Culture Market research?

This research provides comprehensive coverage of the global dairy starter culture market, encompassing all major segments, regions, and market dynamics. The scope includes detailed analysis of market segmentation by type (mesophilic and thermophilic bacteria), nature (single strain and multi-strain types), function (acid production and flavor production), and product type (buttermilk, cheese, ripened butter, sour cream, and yogurt). Geographic coverage extends to all major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed analysis of country-level markets where significant. The research examines key market drivers, restraints, opportunities, and challenges, along with impact analysis of external factors such as the COVID-19 pandemic. Coverage includes competitive landscape analysis of major players, their strategies, and recent developments. The research also explores technological trends, regulatory frameworks, and future market projections. Limitations of the research include potential variations in regional data availability and the challenge of accurately quantifying certain market segments due to the specialized nature of some culture applications.

Who are the key companies in the Dairy Starter Culture Market and what are their recent developments?

The dairy starter culture market features several key players with significant market presence and ongoing strategic initiatives. Chr. Hansen Holding A/S has been focusing on expanding its probiotic culture portfolio and strengthening its position in emerging markets through strategic partnerships. Lallemand Inc. has recently invested in expanding its production capacity and launched new culture solutions for specialty cheese applications. Dohler Group has been active in acquiring complementary businesses to enhance its natural ingredient offerings, including specialized culture solutions. The Dow Chemical Company has been leveraging its material science expertise to develop innovative carrier systems for improved culture stability. BDF Natural Ingredients S.L. has introduced new natural culture solutions targeting the growing clean-label market segment. Biolacter, Inc has focused on developing customized culture solutions for artisanal dairy producers. CSK Food Enrichment B.V. has expanded its presence in the European market through strategic distribution agreements. Sacco System has launched new cultures specifically designed for reduced fermentation time applications. Dalton Biotecnologie S.R.L. has strengthened its position in the Italian cheese culture market through product innovation. These companies continue to invest in research and development, pursue strategic partnerships, and expand their geographic presence to maintain competitive advantage in the evolving market landscape.