Managed Network Services Market Overview - Definition, scope, and significance

Managed Network Services refer to the practice of outsourcing network management and monitoring to third-party service providers who handle the day-to-day operations, maintenance, and optimization of an organization's network infrastructure. This includes services such as network design, implementation, security management, performance monitoring, and troubleshooting across various network components including LAN, WAN, VPN, and wireless networks. The market encompasses both cloud-based and on-premise deployment models, serving diverse industry verticals from BFSI and government to manufacturing, retail, and telecommunications. The significance of this market has grown substantially as organizations increasingly seek to reduce operational complexity, lower costs, and focus on core business functions while leveraging expert network management capabilities. With the global market size projected to reach $82.83 billion in 2025 and expected to grow at a CAGR of 10.61% through 2032, managed network services have become a critical component of modern enterprise IT strategies, enabling digital transformation and supporting the growing demands of cloud computing, IoT, and remote workforce requirements.

Managed Network Services Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The managed network services market is primarily driven by the increasing complexity of network infrastructures, the growing adoption of cloud computing, and the need for enhanced security in an era of rising cyber threats. Organizations are seeking cost-effective solutions to manage their expanding network requirements while ensuring optimal performance and security. The shift towards digital transformation across industries and the proliferation of remote work have further accelerated demand for managed services. However, the market faces restraints such as concerns over data privacy and security when outsourcing critical network functions, potential loss of control over network operations, and the challenge of integrating managed services with existing legacy systems. Key challenges include maintaining service quality across distributed networks, addressing skill gaps in network management, and ensuring compliance with evolving regulatory requirements. Despite these challenges, significant opportunities exist in emerging markets, the growing demand for specialized services like network security and monitoring, and the potential for service providers to offer value-added solutions that incorporate AI and automation technologies to enhance network performance and reliability.

Managed Network Services Market Growth Trends - Current and emerging trends shaping the market

The managed network services market is experiencing several transformative trends that are reshaping its growth trajectory. One of the most prominent trends is the increasing adoption of cloud-based managed services, driven by the need for scalability, flexibility, and cost-efficiency. The integration of artificial intelligence and machine learning into network management is another significant trend, enabling predictive maintenance, automated troubleshooting, and enhanced network optimization. The rise of 5G technology is creating new opportunities for managed services, particularly in supporting the increased bandwidth and low-latency requirements of next-generation applications. There is also a growing trend towards managed security services as organizations prioritize cybersecurity in their network management strategies. Additionally, the market is witnessing increased demand for end-to-end managed services that cover the entire network lifecycle, from design and implementation to ongoing monitoring and optimization. The convergence of IT and operational technology (OT) networks is creating new service opportunities, particularly in manufacturing and industrial sectors. Furthermore, the emphasis on sustainability and energy-efficient networking is driving innovation in managed services that optimize network performance while reducing environmental impact.

COVID-19 Impact on the Managed Network Services Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the managed network services market, initially causing disruptions in service delivery and implementation due to lockdowns and remote working conditions. However, the pandemic ultimately accelerated the adoption of managed network services as organizations rapidly shifted to remote work models, creating unprecedented demand for secure, scalable, and reliable network infrastructure. The crisis highlighted the critical importance of robust network management capabilities, leading many businesses to accelerate their digital transformation initiatives and outsource network management to experienced providers. While some sectors like retail and hospitality experienced temporary slowdowns, others such as healthcare, e-commerce, and remote collaboration tools saw significant growth in managed service requirements. The pandemic also emphasized the need for enhanced network security and monitoring capabilities to protect against the increased cyber threats associated with distributed workforces. As the market recovers, the long-term effects of COVID-19 are expected to drive sustained growth in managed network services, with organizations continuing to prioritize network reliability, security, and scalability to support hybrid work models and digital business operations.

Managed Network Services Market Competitive Landscape - Major competitors and market consolidation

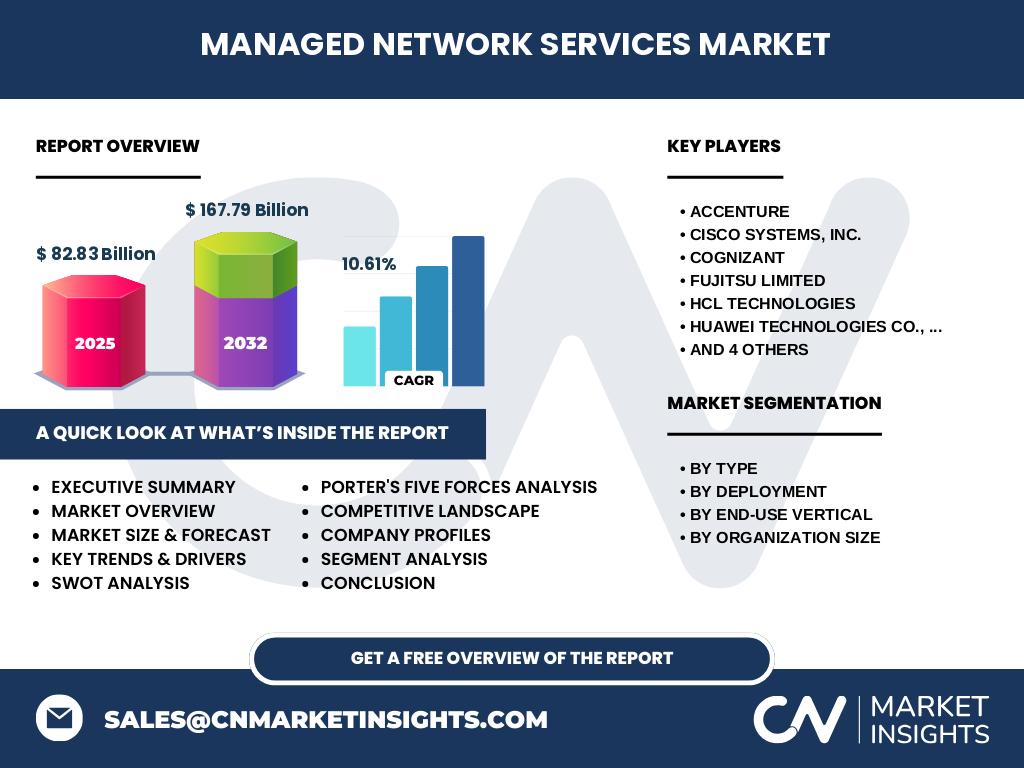

The managed network services market features a competitive landscape characterized by a mix of global technology giants, specialized managed service providers, and regional players. Major competitors include Accenture, Cisco Systems, Cognizant, Fujitsu Limited, HCL Technologies, Huawei Technologies, Kyndryl Holdings, NTT Limited, Tata Consultancy Services, and Verizon, each bringing unique strengths and capabilities to the market. The competitive environment is marked by continuous innovation, strategic partnerships, and mergers and acquisitions as companies seek to expand their service portfolios and geographic reach. Large technology companies leverage their extensive infrastructure and technological expertise, while specialized providers focus on niche services and industry-specific solutions. The market is witnessing increasing consolidation as larger players acquire smaller, specialized firms to enhance their capabilities in areas such as network security, cloud integration, and IoT management. Competition is intensifying around service quality, technological innovation, and the ability to provide comprehensive, end-to-end network management solutions. Service providers are also differentiating themselves through their expertise in emerging technologies, their global service delivery capabilities, and their ability to offer customized solutions that address specific industry requirements and regulatory compliance needs.

Executive Summary - High-level overview and key findings about Managed Network Services Market

The managed network services market is experiencing robust growth, with the global market size reaching $82.83 billion in 2025 and projected to expand to $167.79 billion by 2032, representing a strong CAGR of 10.61%. This growth is driven by the increasing complexity of network infrastructures, the rapid adoption of cloud technologies, and the growing need for enhanced security measures across organizations of all sizes. The market is characterized by diverse service offerings including managed LAN, network security, monitoring, VPN, WAN, and Wi-Fi services, deployed through both cloud and on-premise models. Key industry verticals driving demand include BFSI, government, IT & telecommunications, manufacturing, media & entertainment, and retail & e-commerce, with both large enterprises and SMEs increasingly adopting managed services. The competitive landscape features major global players such as Accenture, Cisco Systems, and Verizon, alongside specialized providers, creating a dynamic environment of innovation and strategic partnerships. Despite challenges related to data security concerns and integration complexities, the market presents significant opportunities in emerging technologies, particularly in AI-driven network management, 5G integration, and enhanced security services. The COVID-19 pandemic has further accelerated market growth by highlighting the critical importance of reliable, secure, and scalable network infrastructure for business continuity and digital transformation initiatives.

Managed Network Services Market Forecast - Projections for 2025-2032 period

The managed network services market is poised for substantial growth over the forecast period from 2025 to 2032, with projections indicating expansion from $82.83 billion to $167.79 billion, representing a robust CAGR of 10.61%. This growth trajectory is underpinned by several key factors, including the continued digital transformation across industries, the increasing adoption of cloud-based services, and the growing complexity of network infrastructures that require specialized management expertise. The forecast period is expected to see accelerated demand for advanced managed services, particularly those incorporating artificial intelligence and machine learning for enhanced network optimization and predictive maintenance. The proliferation of 5G networks and the Internet of Things (IoT) will create new opportunities for managed service providers to offer specialized solutions that address the unique requirements of these technologies. Regional markets are expected to show varying growth rates, with emerging economies in Asia-Pacific and Latin America demonstrating particularly strong expansion due to increasing digitalization and infrastructure development. The forecast also indicates growing demand for managed security services as cybersecurity concerns continue to escalate. Service providers that can offer comprehensive, integrated solutions combining network management, security, and emerging technology support are expected to capture the largest market share during this period.

Managed Network Services Market Size and Share by Segmentation - Breakdown by {segmentData}

The managed network services market exhibits distinct segmentation patterns across various dimensions, reflecting the diverse needs of different customer segments and deployment scenarios. By service type, managed network security services are expected to capture a significant market share due to increasing cybersecurity concerns, followed by managed WAN and VPN services that support distributed enterprise operations. Managed LAN services continue to represent a substantial portion of the market, particularly in enterprise environments, while managed monitoring services are gaining traction as organizations prioritize network performance optimization. In terms of deployment, cloud-based managed services are experiencing faster growth compared to on-premise solutions, driven by the scalability and flexibility benefits of cloud infrastructure. The end-use vertical segmentation reveals that the IT & telecommunications sector currently holds the largest market share, followed closely by BFSI and government sectors, which have stringent network management and security requirements. The manufacturing sector is showing rapid growth in managed service adoption, particularly with the integration of Industry 4.0 technologies. By organization size, large enterprises continue to dominate the market due to their complex network infrastructures, but the SME segment is experiencing the fastest growth rate as smaller organizations increasingly recognize the cost benefits and expertise advantages of managed services.

Global Managed Network Services Market Size and Share by Region - Geographic distribution

The global managed network services market demonstrates varied geographic distribution, with North America currently holding the largest market share due to its advanced technological infrastructure, high adoption rates of managed services, and the presence of major service providers. The region benefits from strong digital transformation initiatives across industries and significant investments in cloud technologies and cybersecurity. Europe represents the second-largest market, driven by stringent regulatory requirements, particularly in data protection and privacy, which necessitate sophisticated network management solutions. The Asia-Pacific region is experiencing the fastest growth rate, fueled by rapid digitalization, expanding IT infrastructure, and increasing adoption of cloud services across emerging economies such as China, India, and Southeast Asian countries. Latin America shows promising growth potential, particularly in countries like Brazil and Mexico, where digital transformation initiatives are gaining momentum. The Middle East and Africa region, while currently representing a smaller market share, is witnessing increasing adoption of managed network services, particularly in Gulf Cooperation Council (GCC) countries that are investing heavily in digital infrastructure. Regional variations in market share are influenced by factors such as technological maturity, regulatory environments, economic conditions, and the level of digital transformation across different industries within each geographic area.

Regional Analysis of the Managed Network Services Market - Detailed regional market performance

Regional analysis of the managed network services market reveals distinct performance characteristics and growth drivers across different geographic areas. North America, particularly the United States, demonstrates strong market performance driven by technological leadership, high digital maturity, and substantial investments in network infrastructure. The region benefits from a mature ecosystem of service providers and early adoption of emerging technologies such as AI and 5G. Europe shows steady growth, with Western European countries leading in adoption rates, while Eastern Europe presents emerging opportunities. The region's performance is influenced by strict data protection regulations like GDPR, which drive demand for specialized managed security services. The Asia-Pacific region exhibits the most dynamic growth, with countries like China, India, and Singapore showing particularly strong performance due to rapid digital transformation, expanding cloud adoption, and increasing IT spending. Japan and South Korea demonstrate mature markets with high technology adoption rates. Latin America's market performance varies significantly by country, with Brazil and Mexico showing the strongest growth due to economic development and digital initiatives. The Middle East and Africa region shows mixed performance, with Gulf countries investing heavily in digital infrastructure while other regions face challenges related to infrastructure development and economic conditions. Regional performance is also influenced by local competitive landscapes, with varying degrees of presence from global and regional service providers.

Leading Company Profiles in the Managed Network Services Market - Industry players and strategies

The managed network services market features several leading companies that have established strong market positions through comprehensive service offerings and strategic capabilities. Accenture stands out for its broad consulting expertise combined with managed services, offering end-to-end network solutions that integrate business strategy with technical implementation. Cisco Systems leverages its extensive networking hardware and software portfolio to provide integrated managed services, with a particular strength in enterprise network management and security solutions. Cognizant has built a strong position through its digital transformation capabilities and industry-specific managed services, particularly in financial services and healthcare. Fujitsu Limited brings its extensive experience in telecommunications and enterprise IT to offer comprehensive managed network services with a focus on innovation and sustainability. HCL Technologies has differentiated itself through its Mode 1-2-3 strategy, combining traditional infrastructure management with digital and cognitive services. Huawei Technologies, despite facing some market challenges, continues to be a significant player, particularly in emerging markets, with its comprehensive network equipment and managed services portfolio. Kyndryl Holdings, as a recent spin-off from IBM, is positioning itself as a dedicated managed infrastructure services provider with a strong focus on hybrid cloud and network management. NTT Limited leverages its global telecommunications infrastructure to offer comprehensive managed services with strong capabilities in managed security and network optimization. Tata Consultancy Services combines its IT services expertise with network management capabilities, particularly strong in serving enterprise clients across multiple industries. Verizon brings its telecommunications infrastructure and enterprise services experience to offer managed network solutions with particular strength in connectivity and security services.

Porter's Five Forces Analysis of the Managed Network Services Market - Competitive forces assessment

Porter's Five Forces analysis of the managed network services market reveals a competitive landscape shaped by several key forces. The threat of new entrants is moderate, as establishing a presence in this market requires significant capital investment, technical expertise, and established customer relationships, though cloud-based service models have lowered some barriers to entry. The bargaining power of buyers is increasing as organizations become more knowledgeable about managed services and demand customized solutions, though the complexity of network management often limits their ability to switch providers easily. The bargaining power of suppliers is relatively low for major service providers who have developed their own technology platforms, though specialized technology vendors can exert some influence, particularly in emerging technology areas. The threat of substitute products or services is moderate, with in-house network management serving as the primary alternative, though the growing complexity of networks makes this option increasingly challenging for most organizations. Competitive rivalry is intense, characterized by price competition, service differentiation, and the continuous need for innovation. Service providers compete on multiple dimensions including service quality, technological capabilities, industry expertise, and geographic coverage. The analysis indicates that while the market presents significant opportunities, success requires substantial investment in technology, talent, and customer relationships to maintain competitive advantage.

SWOT Analysis of the Managed Network Services Market - Strengths, weaknesses, opportunities, threats

A comprehensive SWOT analysis of the managed network services market reveals several key factors influencing its growth and development. Strengths of the market include the increasing complexity of network infrastructures that necessitate specialized expertise, the cost-effectiveness of outsourcing compared to in-house management, and the ability of managed service providers to offer 24/7 monitoring and support. The market also benefits from strong demand across multiple industry verticals and the continuous evolution of technology that creates new service opportunities. However, weaknesses exist in the form of potential security concerns when outsourcing critical network functions, the challenge of integrating managed services with existing legacy systems, and the dependency on service provider performance. Significant opportunities are emerging from the growing adoption of cloud technologies, the increasing focus on network security, the proliferation of IoT devices, and the expansion of 5G networks. The market also presents opportunities in emerging economies where digital transformation is accelerating. Threats to the market include intense competition leading to price pressures, the potential for technological disruption from new networking paradigms, and evolving regulatory requirements that may increase compliance costs. Additionally, economic uncertainties and budget constraints in certain sectors could impact spending on managed services. The analysis suggests that while the market faces challenges, its fundamental strengths and the significant opportunities presented by technological advancement position it for continued growth.

Managed Network Services Market Value Chain Analysis - Industry structure and value flow

The managed network services market value chain encompasses a complex network of activities and stakeholders that create and deliver value to end customers. At the foundation of the value chain are technology providers and equipment manufacturers who supply the hardware and software infrastructure essential for network management. These include networking equipment vendors, cloud service providers, and security technology companies whose products form the technological backbone of managed services. Network service providers and system integrators then build upon this foundation, offering specialized expertise in network design, implementation, and management. Managed service providers (MSPs) represent the core of the value chain, delivering end-to-end network management solutions that encompass monitoring, maintenance, security, and optimization services. Value is added through various stages including service design and customization, integration with customer environments, ongoing management and support, and the application of analytics and automation technologies to enhance service delivery. The value chain also includes consulting firms that help organizations assess their network needs and develop strategies for managed service adoption. Distribution channels include direct sales teams, channel partners, and digital platforms that facilitate service delivery and customer engagement. Finally, end customers across various industries represent the ultimate value recipients, benefiting from improved network performance, enhanced security, and reduced operational complexity. The value chain is characterized by continuous innovation and collaboration among stakeholders to address evolving customer needs and technological advancements.

Key Investment Insights in the Managed Network Services Market - Strategic investment recommendations

The managed network services market presents several compelling investment opportunities driven by strong growth projections and technological evolution. Strategic investments should focus on companies that demonstrate strong capabilities in emerging technologies such as artificial intelligence and machine learning for network optimization and predictive maintenance. Investments in providers with robust cloud-based service offerings are particularly attractive given the accelerating shift toward cloud infrastructure and the scalability advantages it provides. The growing emphasis on network security creates investment opportunities in companies that offer integrated security solutions as part of their managed services portfolio, particularly those with strong capabilities in threat detection and response. Geographic expansion presents another strategic investment consideration, with emerging markets in Asia-Pacific and Latin America showing particularly strong growth potential due to increasing digitalization and infrastructure development. Investors should also consider companies that demonstrate strong vertical market expertise, particularly in high-growth sectors such as healthcare, manufacturing, and financial services where specialized network management requirements create barriers to entry for generalist providers. The trend toward end-to-end managed services represents an investment opportunity in providers that can offer comprehensive solutions covering the entire network lifecycle from design and implementation to ongoing management and optimization. Additionally, investments in companies that demonstrate strong partnerships with technology vendors and cloud providers can provide competitive advantages through access to cutting-edge technologies and integrated solution capabilities.

Managed Network Services Market Conclusion - Summary and key takeaways

The managed network services market is positioned for substantial growth, with the global market size expanding from $82.83 billion in 2025 to an impressive $167.79 billion by 2032, representing a robust CAGR of 10.61%. This growth is driven by the increasing complexity of network infrastructures, the accelerating adoption of cloud technologies, and the growing emphasis on network security across organizations of all sizes. The market's diverse segmentation, encompassing various service types, deployment models, industry verticals, and organization sizes, reflects its broad applicability and the varied needs of different customer segments. While the competitive landscape is intense, featuring major global players and specialized providers, opportunities abound for companies that can offer innovative, integrated solutions that address emerging technological trends such as AI, 5G, and IoT. The COVID-19 pandemic has further accelerated market growth by highlighting the critical importance of reliable, secure, and scalable network infrastructure. Despite challenges related to security concerns and integration complexities, the fundamental drivers of market growth remain strong, supported by continuous digital transformation across industries and the increasing recognition of the cost and expertise benefits of managed services. The market's future appears promising, with significant opportunities for providers that can deliver comprehensive, technology-forward solutions that address the evolving needs of modern enterprises.

Research Methodology - How this research was conducted

The research methodology for this managed network services market analysis employed a comprehensive, multi-faceted approach to ensure accuracy and reliability of findings. Primary research formed the foundation of the study, involving extensive interviews with industry experts, managed service providers, technology vendors, and end-user organizations across various industry verticals. These interviews provided valuable insights into market trends, challenges, and growth drivers from multiple stakeholder perspectives. Secondary research complemented primary findings through analysis of industry reports, company financial statements, press releases, and regulatory filings to validate market size estimates and growth projections. The research methodology incorporated both top-down and bottom-up approaches to market sizing, cross-validating data through multiple estimation techniques to ensure accuracy. Market segmentation analysis was conducted using a combination of quantitative data analysis and qualitative assessment of market dynamics across different service types, deployment models, industry verticals, and geographic regions. The forecast methodology utilized historical growth patterns, technology adoption curves, and macroeconomic indicators to project future market performance. Competitive analysis involved detailed profiling of key market players, assessment of their service portfolios, geographic presence, and strategic initiatives. The research also incorporated analysis of patent filings, technology trends, and regulatory developments to provide a comprehensive understanding of market dynamics and future opportunities.

Research Scope - Coverage and limitations

The research scope for this managed network services market analysis encompasses a comprehensive examination of the global market from 2025 through 2032, with a particular focus on key market segments, regional variations, and competitive dynamics. The study covers major service categories including managed LAN, network security, monitoring, VPN, WAN, and Wi-Fi services, as well as deployment models spanning cloud and on-premise solutions. Industry vertical coverage includes BFSI, government, IT & telecommunications, manufacturing, media & entertainment, and retail & e-commerce sectors, with analysis of both large enterprises and SMEs. Geographic scope encompasses major regions including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with detailed country-level analysis in key markets. The research examines market drivers, restraints, challenges, and opportunities, providing a holistic view of factors influencing market growth. Competitive landscape analysis includes profiling of major market players and assessment of their strategies, service offerings, and market positions. The study also incorporates analysis of emerging trends, technological developments, and regulatory factors impacting the market. Limitations of the research include the availability of certain market data in specific regions, the rapidly evolving nature of technology that may impact future projections, and the challenge of quantifying certain qualitative factors influencing market dynamics. Additionally, the research focuses primarily on commercial managed network services and may not fully capture certain niche or emerging service categories.

Key Companies and Recent Developments in the Managed Network Services Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The managed network services market features several key companies that have recently made significant announcements and strategic moves to strengthen their market positions. Accenture has expanded its managed services portfolio through strategic acquisitions and partnerships, particularly focusing on cloud integration and cybersecurity services. The company recently announced enhanced AI-driven network management capabilities aimed at improving service automation and predictive maintenance. Cisco Systems continues to innovate with new product launches in its managed services offerings, including advanced network security solutions and expanded 5G network management capabilities. The company has also formed strategic partnerships with major cloud providers to enhance its managed cloud networking services. Cognizant has strengthened its position through acquisitions of specialized network security firms and the launch of new industry-specific managed services tailored for financial services and healthcare sectors. Fujitsu Limited has announced expanded partnerships with telecommunications providers to enhance its managed network services in the Asia-Pacific region, along with new sustainability-focused network management solutions. HCL Technologies has recently launched enhanced digital workplace services as part of its managed network portfolio, incorporating advanced analytics and automation capabilities. Huawei Technologies continues to expand its presence in emerging markets with new managed service offerings focused on 5G network deployment and management. Kyndryl Holdings has made significant strides since its spin-off from IBM, announcing new strategic partnerships and expanded service capabilities in hybrid cloud network management. NTT Limited has recently enhanced its managed security services portfolio with new threat detection and response capabilities, along with expanded global service delivery infrastructure. Tata Consultancy Services has launched new managed services focused on IoT network management and has formed strategic alliances with major technology vendors to enhance its service offerings. Verizon has announced expanded managed network services for enterprise customers, including new offerings in edge computing and network-as-a-service solutions. These developments reflect the dynamic nature of the market and the ongoing efforts of key players to innovate and expand their service capabilities to meet evolving customer needs.