Europe Pacemakers Market Overview - Definition, scope, and significance

The Europe Pacemakers Market encompasses the production, distribution, and utilization of cardiac pacing devices designed to regulate abnormal heart rhythms across European countries. These medical devices, which include implantable and external pacemakers with various technological configurations, represent a critical segment of the cardiovascular medical device industry. The market's significance stems from its direct impact on patient outcomes for millions of Europeans suffering from bradycardia, heart block, and other cardiac rhythm disorders. As Europe's population continues to age, with Eurostat projecting that by 2030 over 30% of Europeans will be aged 65 or older, the demand for cardiac rhythm management solutions continues to grow, positioning the pacemakers market as a vital component of the region's healthcare infrastructure.

Europe Pacemakers Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The Europe Pacemakers Market is driven by several key factors including the rising prevalence of cardiovascular diseases, technological advancements in device miniaturization and battery life, and increasing healthcare expenditure across European nations. The growing geriatric population represents a significant driver, as elderly individuals are more susceptible to cardiac rhythm disorders. Additionally, improved reimbursement policies in countries like Germany, France, and the UK support market growth. However, the market faces restraints such as the high cost of advanced pacemaker devices, stringent regulatory requirements from the European Medicines Agency (EMA), and the risk of device-related complications. Challenges include the need for specialized healthcare professionals, limited awareness in certain regions, and the impact of alternative treatments like catheter ablation. Opportunities exist in emerging markets within Eastern Europe, the development of leadless pacemakers, and the integration of remote monitoring capabilities that align with the region's digital health initiatives.

Europe Pacemakers Market Growth Trends - Current and emerging trends shaping the market

The Europe Pacemakers Market is experiencing several transformative trends that are reshaping the competitive landscape. One prominent trend is the shift toward leadless pacemaker technology, which eliminates traditional lead complications and offers patients greater mobility and reduced infection risks. Another significant trend is the integration of artificial intelligence and machine learning capabilities into pacemaker systems, enabling predictive analytics and personalized therapy adjustments. The market is also witnessing increased adoption of remote monitoring solutions, accelerated by the COVID-19 pandemic, allowing healthcare providers to monitor patients' cardiac activity without in-person visits. Additionally, there is a growing preference for dual-chamber and bi-ventricular pacemakers over single-chamber devices due to their superior efficacy in managing complex arrhythmias. The market is also seeing consolidation through mergers and acquisitions as companies seek to expand their technological capabilities and geographic presence across the diverse European healthcare landscape.

COVID-19 Impact on the Europe Pacemakers Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic significantly disrupted the Europe Pacemakers Market, creating both immediate challenges and long-term implications. During the peak pandemic periods, many European countries experienced a substantial decline in elective procedures, including pacemaker implantations, as healthcare resources were redirected to COVID-19 patients and hospitals implemented restrictive measures. According to industry reports, pacemaker procedures decreased by approximately 20-30% across major European markets during 2020. The pandemic also disrupted supply chains, causing temporary shortages of critical components and delayed product launches. However, the crisis accelerated the adoption of telemedicine and remote monitoring technologies, which have now become integral to post-implantation care. As vaccination rates increased and healthcare systems adapted, the market began recovering in 2021, with many countries reporting return to pre-pandemic procedure volumes by late 2022. The pandemic has fundamentally changed how cardiac care is delivered in Europe, with hybrid care models combining in-person and remote monitoring becoming the new standard.

Europe Pacemakers Market Competitive Landscape - Major competitors and market consolidation

The Europe Pacemakers Market features a moderately consolidated competitive landscape dominated by global medical device giants alongside several regional players. The market is characterized by intense competition based on technological innovation, product portfolio, pricing strategies, and distribution networks. Major competitors including Medtronic, Abbott, and Boston Scientific Corporation command significant market share through their comprehensive product portfolios and established relationships with healthcare providers. BIOTRONIK, a German-based company, maintains strong regional presence with its innovative pacing solutions. The competitive dynamics are shaped by continuous product launches, strategic partnerships, and mergers and acquisitions aimed at expanding technological capabilities. Companies are increasingly focusing on developing miniaturized devices with extended battery life and enhanced remote monitoring features to differentiate themselves. The entry barriers remain high due to stringent regulatory requirements, the need for substantial R&D investments, and the requirement for extensive clinical validation, which has limited the emergence of new competitors in the European market.

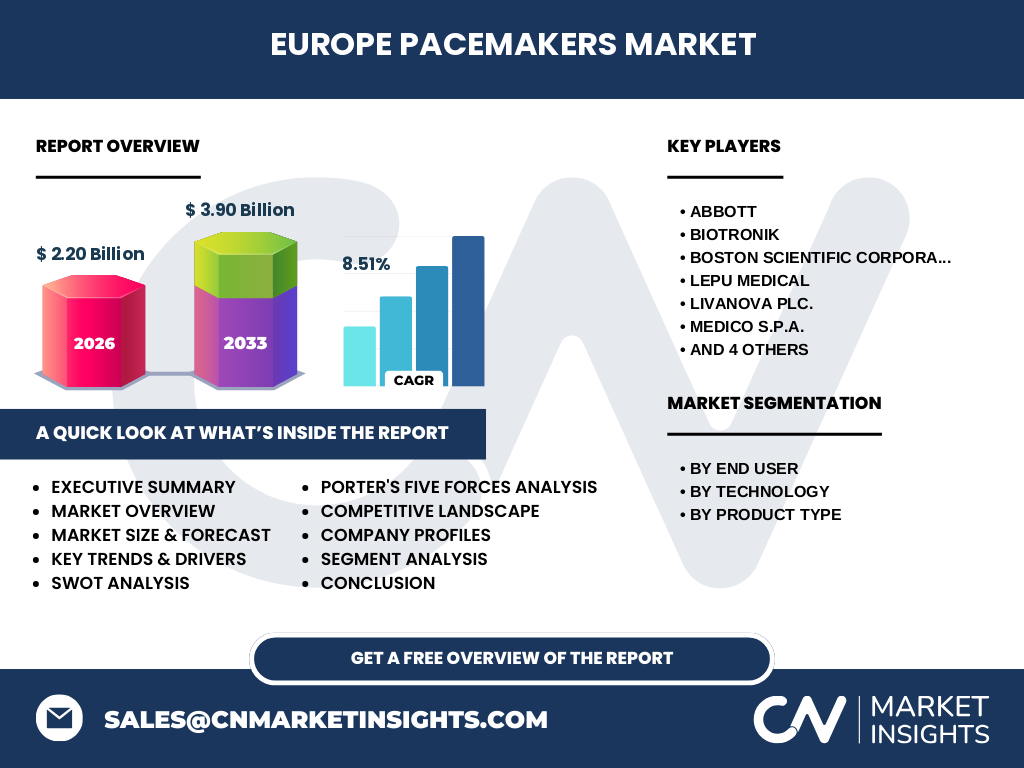

Executive Summary - High-level overview and key findings about Europe Pacemakers Market

The Europe Pacemakers Market presents a compelling growth trajectory, with the market size reaching 2.20 billion in 2026 and projected to expand to 3.90 billion by 2033, representing a robust CAGR of 8.51%. This growth is driven by the region's aging population, increasing prevalence of cardiovascular diseases, and continuous technological advancements in cardiac rhythm management. The market segmentation reveals distinct preferences, with dual-chambered and bi-ventricular pacemakers gaining traction over single-chambered devices due to their superior therapeutic outcomes. Hospitals remain the dominant end-user segment, accounting for the majority of pacemaker implantations, though ambulatory surgical centers are emerging as a growing channel. The competitive landscape is led by established players such as Medtronic, Abbott, and Boston Scientific, who collectively hold significant market share through their comprehensive product portfolios and extensive distribution networks. Despite challenges including high device costs and regulatory complexities, the market presents substantial opportunities in emerging Eastern European markets and through the development of next-generation pacing technologies with enhanced connectivity and remote monitoring capabilities.

Europe Pacemakers Market Forecast - Projections for 2025-2032 period

The Europe Pacemakers Market is poised for substantial growth between 2025 and 2032, with projections indicating a market size of 3.90 billion by 2033, up from 2.20 billion in 2026. This represents a compound annual growth rate of 8.51%, reflecting the market's resilience and expansion potential. The forecast period will be characterized by several key developments, including the accelerated adoption of leadless pacemakers, which are expected to capture an increasing share of the implantable segment due to their advantages in reducing complications and improving patient quality of life. The dual-chambered and bi-ventricular segments are projected to experience the highest growth rates as healthcare providers increasingly recognize their clinical benefits for complex cardiac conditions. Geographically, Western European markets including Germany, France, and the UK will continue to dominate in absolute terms, while Eastern European countries such as Poland, Hungary, and the Czech Republic are expected to demonstrate the fastest growth rates as healthcare infrastructure improves and reimbursement frameworks expand. The forecast also anticipates continued consolidation in the competitive landscape, with strategic acquisitions and partnerships shaping market dynamics.

Europe Pacemakers Market Size and Share by Segmentation - Breakdown by {segmentData}

The Europe Pacemakers Market exhibits distinct segmentation patterns across technology, product type, and end-user categories. By technology, dual-chambered pacemakers currently represent the largest segment, accounting for approximately 45-50% of the market, followed by single-chambered devices at 30-35%, with bi-ventricular pacemakers comprising the remaining 15-20%. This distribution reflects the clinical preference for dual-chambered devices in managing atrioventricular block and sick sinus syndrome. In terms of product type, implantable pacemakers dominate the market with approximately 85% share, while external pacemakers account for the remaining 15%, primarily used in acute care settings and temporary pacing requirements. By end-user segmentation, hospitals represent the largest segment with approximately 70% market share, driven by their comprehensive cardiac care facilities and specialized staff. Ambulatory surgical centers account for the remaining 30%, with this segment experiencing the fastest growth as healthcare systems increasingly adopt outpatient surgical models to reduce costs and improve patient convenience. These segmentation patterns vary across European countries based on healthcare infrastructure, reimbursement policies, and clinical practice preferences.

Global Europe Pacemakers Market Size and Share by Region - Geographic distribution

The Europe Pacemakers Market demonstrates significant regional variations in market size and share across the continent's diverse healthcare landscapes. Western European countries including Germany, France, the United Kingdom, Italy, and Spain collectively account for approximately 70-75% of the total European market, driven by their advanced healthcare infrastructure, higher healthcare expenditure, and larger patient populations with cardiovascular conditions. Germany leads the regional market with the highest absolute market size, attributed to its comprehensive healthcare system, favorable reimbursement policies, and high diagnosis rates. Southern European countries including Italy and Spain represent the second-largest regional cluster, while the Nordic countries demonstrate high per capita pacemaker utilization rates despite smaller population bases. Eastern European markets including Poland, Hungary, the Czech Republic, and Romania collectively account for approximately 20-25% of the European market, with these regions experiencing the fastest growth rates as healthcare infrastructure improves and economic conditions strengthen. The remaining market share is distributed across Benelux countries and other smaller European nations, each with unique market characteristics shaped by local healthcare policies and economic factors.

Regional Analysis of the Europe Pacemakers Market - Detailed regional market performance

The Europe Pacemakers Market exhibits distinct regional characteristics shaped by healthcare systems, economic conditions, and demographic profiles across different European sub-regions. Western Europe, comprising Germany, France, the UK, Italy, and Spain, represents the market's powerhouse, accounting for approximately 70% of total European sales. Germany leads with its robust healthcare infrastructure and comprehensive insurance coverage, while France benefits from its universal healthcare system that ensures broad patient access to cardiac devices. The Nordic countries, despite smaller populations, demonstrate high per capita pacemaker utilization rates due to excellent healthcare coverage and proactive cardiac care approaches. Southern Europe, including Italy and Spain, shows strong market performance supported by aging populations and improving healthcare access. Eastern Europe presents a contrasting landscape, with countries like Poland and the Czech Republic experiencing rapid market growth at rates exceeding the European average, driven by healthcare modernization initiatives and increasing disposable incomes. However, these markets face challenges including limited reimbursement in certain procedures and infrastructure gaps in rural areas. The regional analysis reveals that while Western Europe provides market stability and innovation leadership, Eastern Europe represents the primary growth engine for the forecast period.

Leading Company Profiles in the Europe Pacemakers Market - Industry players and strategies

The Europe Pacemakers Market is dominated by several key players employing diverse strategies to maintain and expand their market positions. Medtronic, a global leader in medical technology, leverages its extensive product portfolio including the Advisa and Ensura pacemaker families, focusing on technological innovation and strategic acquisitions to strengthen its European presence. Abbott, with its Gallant and Assurity pacemaker lines, emphasizes miniaturization and connectivity features, positioning itself as an innovation leader in the leadless pacemaker segment with its Aveir platform. Boston Scientific Corporation differentiates through its S-ICD and Intellis systems, targeting specific clinical indications and emphasizing ease of use for healthcare providers. BIOTRONIK, headquartered in Germany, maintains strong regional dominance through its innovative devices like the Edora and Prologix series, leveraging its European manufacturing base and deep understanding of regional market dynamics. Other significant players including Lepu Medical, LivaNova, and Medico S.p.A. focus on competitive pricing strategies and targeted geographic expansion, particularly in emerging Eastern European markets. These companies collectively shape the competitive landscape through continuous R&D investments, clinical evidence generation, and strategic partnerships with healthcare systems across Europe.

Porter's Five Forces Analysis of the Europe Pacemakers Market - Competitive forces assessment

Porter's Five Forces analysis reveals a moderately attractive but challenging competitive environment in the Europe Pacemakers Market. The threat of new entrants remains relatively low due to substantial barriers including the need for significant capital investment in R&D, manufacturing facilities, and clinical trials, as well as stringent regulatory requirements from the European Medicines Agency. The bargaining power of buyers, primarily hospitals and healthcare systems, is moderate to high, as they can compare products across multiple established vendors and negotiate on price and service terms, particularly in countries with centralized procurement systems. Supplier bargaining power varies depending on the component, with specialized semiconductor and battery suppliers holding moderate leverage due to their critical role in device functionality. The threat of substitute products exists but is limited, with alternative treatments such as catheter ablation and pharmaceutical interventions serving specific patient segments but not fully replacing the need for pacemakers in bradycardia cases. Competitive rivalry is intense among the major players, characterized by rapid technological innovation, aggressive marketing, and competitive pricing strategies, particularly in mature Western European markets where product differentiation becomes increasingly important for maintaining market share.

SWOT Analysis of the Europe Pacemakers Market - Strengths, weaknesses, opportunities, threats

The Europe Pacemakers Market demonstrates a complex interplay of strengths, weaknesses, opportunities, and threats shaping its competitive landscape. Key strengths include the region's advanced healthcare infrastructure, high diagnosis and treatment rates for cardiac conditions, and strong presence of leading medical device manufacturers with established distribution networks. The market benefits from favorable reimbursement policies in many European countries and a growing acceptance of innovative technologies such as leadless pacemakers and remote monitoring solutions. However, weaknesses include the high cost of advanced pacemaker systems, which can limit accessibility in certain regions, and the lengthy regulatory approval processes that can delay product launches. The market faces significant opportunities in the expansion of healthcare access in Eastern European countries, the development of next-generation devices with extended battery life and enhanced connectivity, and the integration of artificial intelligence for predictive analytics. Threats include pricing pressures from healthcare cost containment measures, the potential for device-related complications affecting market confidence, and increasing competition from alternative cardiac rhythm management technologies that may capture market share in specific patient segments.

Europe Pacemakers Market Value Chain Analysis - Industry structure and value flow

The Europe Pacemakers Market value chain encompasses a complex network of activities from raw material sourcing to end-user delivery and post-market support. The chain begins with component suppliers providing specialized semiconductors, batteries, leads, and biocompatible materials essential for pacemaker manufacturing. These components flow to original equipment manufacturers (OEMs) including Medtronic, Abbott, and Boston Scientific, who integrate them into sophisticated pacemaker systems through advanced manufacturing processes in facilities often located across multiple European countries. The finished products then move through distribution channels, typically involving medical device distributors and direct sales teams that navigate the complex European regulatory landscape and reimbursement frameworks. Healthcare providers, primarily hospitals and specialized cardiac centers, serve as the primary customers, making procurement decisions based on clinical efficacy, cost considerations, and existing vendor relationships. The value chain extends beyond initial implantation to include ongoing patient monitoring, device programming, and maintenance services provided by specialized cardiac technicians and physicians. Recent trends are reshaping this value chain, with increased vertical integration by major players, growing emphasis on remote monitoring services, and the emergence of digital health platforms that create new touchpoints between manufacturers and end-users.

Key Investment Insights in the Europe Pacemakers Market - Strategic investment recommendations

The Europe Pacemakers Market presents compelling investment opportunities driven by technological innovation, demographic trends, and expanding healthcare access across the continent. Strategic investors should consider focusing on companies developing next-generation pacing technologies, particularly those working on leadless pacemakers and devices with extended battery life, as these segments are projected to experience the highest growth rates. The integration of remote monitoring capabilities represents another attractive investment thesis, given the accelerated adoption of digital health solutions following the COVID-19 pandemic and the potential for reducing long-term healthcare costs. Eastern European markets offer significant untapped potential, with countries like Poland, Hungary, and Romania demonstrating rapid healthcare infrastructure development and increasing cardiovascular disease prevalence. Investors should also monitor companies pursuing strategic acquisitions and partnerships that enhance technological capabilities or expand geographic presence, as consolidation is likely to accelerate in the coming years. Additionally, firms developing complementary digital health platforms that integrate with pacemaker data for comprehensive patient management represent emerging opportunities at the intersection of medical devices and digital health. However, investors must carefully evaluate regulatory risks, reimbursement landscapes, and competitive dynamics specific to each target market within Europe's diverse healthcare ecosystem.

Europe Pacemakers Market Conclusion - Summary and key takeaways

The Europe Pacemakers Market represents a dynamic and growing segment of the cardiovascular medical device industry, characterized by technological innovation, demographic drivers, and evolving healthcare delivery models. With the market size reaching 2.20 billion in 2026 and projected to grow to 3.90 billion by 2033 at a CAGR of 8.51%, the market demonstrates robust expansion potential despite facing challenges including regulatory complexities and pricing pressures. The competitive landscape remains dominated by global players such as Medtronic, Abbott, and Boston Scientific, though regional companies like BIOTRONIK maintain strong positions through localized strategies and innovation. Key trends shaping the market include the shift toward leadless pacemakers, increasing adoption of remote monitoring solutions, and growing preference for dual-chambered and bi-ventricular devices. The market's future will be influenced by the expansion of healthcare access in Eastern Europe, continued technological advancements, and the integration of digital health capabilities. Success in this market will require companies to balance innovation with cost-effectiveness, navigate diverse regulatory environments across European countries, and develop comprehensive solutions that address the full spectrum of patient needs from implantation through long-term management.

Research Methodology - How this research was conducted

This comprehensive market research on the Europe Pacemakers Market was conducted using a robust methodology combining primary and secondary research approaches to ensure accuracy and reliability. The research process began with extensive secondary data collection from reputable sources including medical device industry reports, regulatory filings, company annual reports, and healthcare databases from organizations such as the European Society of Cardiology and national health ministries across Europe. Primary research involved interviews with key industry stakeholders including medical device manufacturers, healthcare providers, regulatory experts, and industry analysts to validate findings and gain insights into market dynamics. Data triangulation techniques were employed to cross-verify information from multiple sources, ensuring consistency in market size calculations, growth projections, and competitive analysis. The market sizing methodology utilized both top-down and bottom-up approaches, starting with macroeconomic indicators and healthcare expenditure data, then refining estimates based on device utilization rates, procedure volumes, and pricing trends across different European countries. Segmentation analysis was conducted based on technology types, product categories, and end-user segments, with careful consideration of regional variations in healthcare systems and reimbursement policies. The research team applied statistical modeling techniques to forecast market growth, incorporating factors such as demographic trends, disease prevalence, technological adoption rates, and economic indicators to generate the projected CAGR of 8.51% through 2033.

Research Scope - Coverage and limitations

This research on the Europe Pacemakers Market encompasses a comprehensive analysis of the cardiac pacing device industry across the European continent, with coverage extending to all 27 European Union member states plus major non-EU European countries including the United Kingdom, Switzerland, Norway, and others. The scope includes all major pacemaker technologies: single-chambered, dual-chambered, and bi-ventricular devices, as well as both implantable and external pacemaker categories. The research examines market dynamics across key end-user segments, primarily hospitals and ambulatory surgical centers, while acknowledging the primary role of hospitals in pacemaker implantation procedures. Geographic coverage provides detailed analysis of major markets including Germany, France, the UK, Italy, and Spain, with additional insights into emerging Eastern European markets. The research timeframe extends from historical data through 2026 base year figures to projections through 2033, providing both retrospective analysis and forward-looking insights. Limitations of the research include potential variations in data availability across different European countries due to differences in reporting standards and healthcare system transparency. Additionally, the rapidly evolving nature of medical technology and potential regulatory changes may impact future market dynamics beyond the scope of current projections. The research focuses specifically on pacemakers and does not extend to other cardiac rhythm management devices such as implantable cardioverter defibrillators (ICDs) or cardiac resynchronization therapy (CRT) devices, which represent separate but related market segments.

Key Companies and Recent Developments in the Europe Pacemakers Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The Europe Pacemakers Market features several key companies driving innovation and competition through strategic developments and product advancements. Medtronic continues to strengthen its market position with recent launches including the next-generation Azure XT pacemaker family, featuring extended battery life and enhanced remote monitoring capabilities. The company has also announced strategic partnerships with European healthcare systems to implement comprehensive cardiac care programs integrating device data with electronic health records. Abbott has made significant strides with the European launch of its Aveir leadless pacemaker platform, representing a major technological advancement in miniaturization and patient comfort. The company recently announced a collaboration with a major European health insurer to expand coverage for leadless pacemaker procedures. Boston Scientific Corporation introduced its ImageReady MRI SureScan pacing system, specifically designed to address the growing need for MRI-compatible devices in European clinical practice. The company has also expanded its presence in Eastern Europe through distribution partnerships in Poland and Hungary. BIOTRONIK, maintaining its strong regional presence, launched the Edora series with enhanced programming capabilities and announced the expansion of its manufacturing facility in Berlin to increase production capacity. Other notable developments include Lepu Medical's entry into the European market through regulatory approvals in select countries, and LivaNova's strategic acquisition of a European cardiac rhythm management company to strengthen its product portfolio. These developments collectively indicate a market characterized by continuous innovation, geographic expansion, and strategic positioning to address evolving clinical needs across diverse European healthcare landscapes.