Fraud Detection And Prevention Market Overview - Definition, scope, and significance

The Fraud Detection and Prevention (FDP) market encompasses technologies, solutions, and services designed to identify, prevent, and mitigate fraudulent activities across various industries. This market includes software platforms, analytics tools, authentication systems, and consulting services that help organizations protect against financial crimes, identity theft, payment fraud, and other deceptive practices. The scope of the FDP market spans multiple sectors including banking, financial services, insurance, healthcare, retail, telecommunications, and e-commerce. Its significance has grown exponentially as digital transactions have become ubiquitous, with organizations facing increasingly sophisticated fraud schemes that can result in substantial financial losses, reputational damage, and regulatory penalties. The market addresses critical needs for real-time monitoring, risk assessment, compliance management, and incident response capabilities in an interconnected global economy.

Fraud Detection And Prevention Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The primary drivers of the FDP market include the rapid digitalization of financial services, increasing cyber threats, stringent regulatory requirements, and growing adoption of digital payment systems. Organizations face mounting pressure to protect customer data and prevent financial losses, while consumers demand secure transaction experiences. However, the market faces restraints such as high implementation costs, complexity of integration with legacy systems, and shortage of skilled cybersecurity professionals. Key challenges include keeping pace with evolving fraud techniques, managing false positives in detection systems, and ensuring cross-border compliance. Significant opportunities exist in emerging markets with growing digital economies, artificial intelligence and machine learning advancements for predictive analytics, and the expansion of fraud prevention in non-traditional sectors like healthcare and manufacturing. The shift toward cloud-based solutions and the Internet of Things (IoT) also presents new avenues for market growth and innovation.

Fraud Detection And Prevention Market Growth Trends - Current and emerging trends shaping the market

The FDP market is experiencing several transformative trends that are reshaping the industry landscape. Artificial intelligence and machine learning are becoming increasingly central to fraud detection systems, enabling more sophisticated pattern recognition and predictive capabilities. Real-time fraud prevention is emerging as a critical requirement, with organizations moving away from batch processing to instantaneous transaction monitoring. The adoption of cloud-based FDP solutions is accelerating due to their scalability, cost-effectiveness, and ease of deployment. Behavioral analytics and biometrics are gaining prominence for identity verification and anomaly detection. There is also a growing trend toward integrated fraud management platforms that combine multiple detection methods into unified solutions. The market is witnessing increased demand for fraud prevention in mobile payments and digital wallets, while blockchain technology is being explored for its potential to enhance transaction security and transparency. Additionally, the convergence of fraud detection with cybersecurity and risk management functions is creating more holistic approaches to organizational protection.

COVID-19 Impact on the Fraud Detection And Prevention Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a profound impact on the FDP market, initially causing disruptions due to economic uncertainty and reduced business operations. However, the pandemic ultimately accelerated market growth as organizations rapidly shifted to digital channels, creating new vulnerabilities that required enhanced fraud protection. The surge in e-commerce, remote work, and digital banking during lockdowns led to increased fraud attempts across payment systems, account takeovers, and identity theft schemes. This created an urgent need for more robust FDP solutions, driving accelerated adoption and investment. The recovery trajectory has been strong, with organizations recognizing that digital transformation trends accelerated by the pandemic are permanent, necessitating long-term fraud prevention strategies. The market has seen increased focus on cloud-based solutions, API security, and multi-channel fraud detection capabilities. As businesses continue to operate in hybrid environments, the demand for flexible, scalable FDP solutions that can protect both traditional and digital touchpoints remains elevated.

Fraud Detection And Prevention Market Competitive Landscape - Major competitors and market consolidation

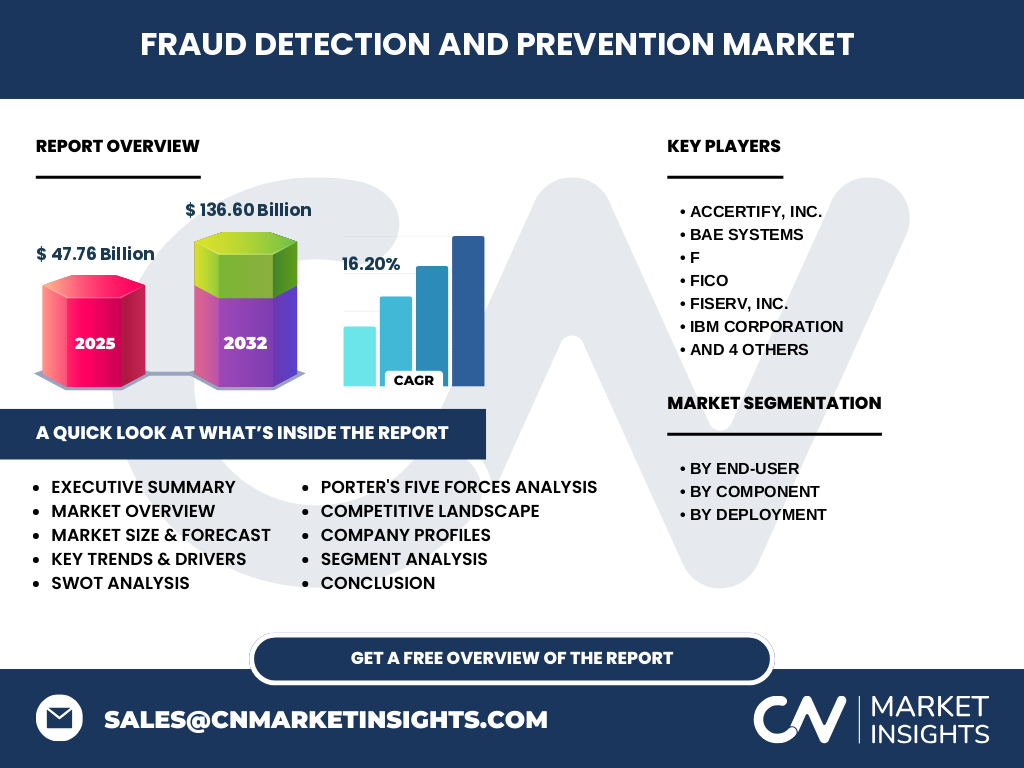

The FDP market features a diverse competitive landscape with a mix of established technology giants, specialized cybersecurity firms, and innovative startups. Major players include IBM Corporation, SAP SE, FICO, SAS Institute Inc., and Fiserv, Inc., which leverage their extensive technological capabilities and global reach. Specialized providers like Accertify, Inc., BAE Systems, Securonix, and PayPal bring deep expertise in specific fraud prevention domains. The market is experiencing consolidation through strategic acquisitions, partnerships, and collaborations as companies seek to expand their capabilities and market presence. Large technology firms are acquiring specialized FDP companies to enhance their security portfolios, while established players are forming strategic alliances to integrate complementary technologies. Competition is intensifying around artificial intelligence capabilities, real-time processing, and cloud-based solutions. Companies are also competing on their ability to provide comprehensive, end-to-end fraud management platforms that can address multiple fraud vectors across different industries and transaction types.

Executive Summary - High-level overview and key findings about Fraud Detection And Prevention Market

The Fraud Detection and Prevention market is experiencing robust growth driven by increasing digital transactions, sophisticated fraud schemes, and stringent regulatory requirements. The market is projected to grow from $47.76 billion in 2025 to $136.60 billion by 2032, representing a strong CAGR of 16.20%. Key segments include BFSI, healthcare, manufacturing, retail, and telecommunications, with solutions and services deployed across both on-premises and cloud environments. The competitive landscape features major technology companies alongside specialized fraud prevention providers, with ongoing consolidation through acquisitions and partnerships. The COVID-19 pandemic accelerated digital transformation, creating both challenges and opportunities for the market. Emerging trends include AI-driven detection, real-time monitoring, behavioral analytics, and integrated fraud management platforms. The market presents significant investment opportunities, particularly in cloud-based solutions and emerging markets, while facing challenges related to implementation complexity and evolving fraud techniques.

Fraud Detection And Prevention Market Forecast - Projections for 2025-2032 period

The FDP market is forecast to experience substantial growth over the 2025-2032 period, expanding from $47.76 billion to $136.60 billion, representing a compound annual growth rate of 16.20%. This growth trajectory reflects increasing digital transaction volumes, rising fraud sophistication, and expanding regulatory requirements across global markets. The forecast period will likely see accelerated adoption of AI and machine learning technologies, with these capabilities becoming standard features in FDP solutions. Cloud-based deployments are expected to dominate market growth, driven by their scalability and cost advantages. The BFSI sector will continue to be the largest market segment, while healthcare and retail are projected to show the fastest growth rates due to increasing digital adoption and fraud vulnerabilities. Geographic expansion will be particularly strong in emerging markets across Asia-Pacific, Latin America, and the Middle East, where digital economies are rapidly developing. The forecast also indicates growing demand for integrated fraud management platforms that can address multiple fraud vectors simultaneously.

Fraud Detection And Prevention Market Size and Share by Segmentation - Breakdown by {segmentData}

The FDP market segmentation reveals distinct patterns across end-users, components, and deployment models. By end-user, the Banking, Financial Services, and Insurance (BFSI) sector represents the largest market share, driven by high transaction volumes and strict regulatory requirements. Healthcare follows as a significant segment, with increasing digital health records and telemedicine creating new fraud vulnerabilities. Retail and telecommunications also represent substantial market segments, particularly with the growth of e-commerce and mobile payments. By component, the solutions segment dominates, encompassing software platforms, analytics tools, and detection systems, while services including consulting, implementation, and managed services form a growing segment. Deployment analysis shows a clear trend toward cloud-based solutions, which offer scalability and cost advantages, though on-premises deployments remain important for organizations with strict data sovereignty requirements or legacy system dependencies. The segmentation data indicates that integrated, multi-channel solutions are increasingly preferred over point solutions.

Global Fraud Detection And Prevention Market Size and Share by Region - Geographic distribution

The global FDP market exhibits distinct regional patterns in terms of market size and adoption rates. North America currently leads the market, driven by advanced technological infrastructure, high digital transaction volumes, and stringent regulatory frameworks. The region benefits from the presence of major technology providers and early adoption of innovative fraud prevention solutions. Europe represents the second-largest market, characterized by comprehensive data protection regulations and a mature financial services sector. The Asia-Pacific region is experiencing the fastest growth, fueled by rapid digitalization, expanding e-commerce, and increasing smartphone penetration. Countries like China, India, and Southeast Asian nations are seeing particularly strong demand as their digital economies mature. Latin America and the Middle East & Africa regions are emerging markets with significant growth potential, though they currently represent smaller market shares. Regional differences in regulatory environments, technological maturity, and fraud sophistication levels create varying demands for FDP solutions across geographic markets.

Regional Analysis of the Fraud Detection And Prevention Market - Detailed regional market performance

Regional market performance in the FDP sector varies significantly based on economic development, regulatory frameworks, and technological adoption rates. North America demonstrates mature market penetration with high adoption of advanced AI-driven solutions, particularly in the United States where regulatory compliance and cybersecurity concerns drive substantial investment. Europe shows strong growth in fraud prevention adoption, with GDPR compliance and PSD2 regulations creating specific requirements for transaction monitoring and customer authentication. The Asia-Pacific region exhibits the most dynamic growth trajectory, with countries like China and India rapidly expanding their digital payment infrastructure and requiring scalable fraud prevention solutions. However, the region also faces challenges with varying regulatory standards across countries. Latin America is experiencing increased FDP adoption due to rising e-commerce and mobile banking, though market fragmentation and economic volatility present challenges. The Middle East and Africa region shows growing interest in fraud prevention, particularly in Gulf Cooperation Council countries investing in financial technology, though overall market maturity remains lower compared to other regions.

Leading Company Profiles in the Fraud Detection And Prevention Market - Industry players and strategies

The FDP market features several prominent players with distinct strategic approaches and competitive advantages. IBM Corporation leverages its extensive AI and analytics capabilities through its Trusteer and Safer Payments solutions, focusing on enterprise-grade fraud prevention platforms. SAP SE offers comprehensive fraud management solutions integrated with its broader enterprise software ecosystem, targeting large organizations with complex needs. FICO brings decades of expertise in predictive analytics and credit risk, applying these capabilities to fraud detection through its Falcon platform. SAS Institute Inc. emphasizes advanced analytics and machine learning for fraud detection across multiple industries. Fiserv, Inc. specializes in financial services fraud prevention with integrated payment security solutions. Specialized providers like Accertify, Inc. focus on e-commerce fraud prevention, while BAE Systems brings cybersecurity expertise to the financial sector. Securonix offers next-generation security analytics with behavioral monitoring capabilities. These companies compete on technological innovation, industry expertise, global reach, and the ability to provide integrated, scalable solutions that address evolving fraud threats.

Porter's Five Forces Analysis of the Fraud Detection And Prevention Market - Competitive forces assessment

Porter's Five Forces analysis reveals the competitive dynamics shaping the FDP market. The threat of new entrants is moderate, as the market requires significant technological expertise, substantial R&D investment, and established customer relationships, though innovative startups can still enter with specialized solutions. Bargaining power of buyers is increasing as organizations become more sophisticated in their procurement and demand integrated, cost-effective solutions. The bargaining power of suppliers is relatively low, as component technologies are widely available, though specialized AI and machine learning capabilities may command premium pricing. The threat of substitutes is moderate, with traditional fraud prevention methods being replaced by more advanced technological solutions, while new fraud techniques constantly emerge requiring updated prevention methods. Competitive rivalry is intense, with numerous established players and specialized providers competing on technological capabilities, pricing, and service quality. The market shows characteristics of both consolidation and fragmentation, with large players acquiring specialized firms while niche providers continue to innovate in specific fraud prevention domains.

SWOT Analysis of the Fraud Detection And Prevention Market - Strengths, weaknesses, opportunities, threats

The FDP market exhibits distinct strengths including strong growth drivers from digital transformation, increasing regulatory requirements, and sophisticated fraud techniques that create sustained demand. The market benefits from technological advancements in AI and machine learning that enable more effective fraud detection. However, weaknesses include high implementation costs, complexity of integration with existing systems, and shortage of skilled professionals to manage advanced FDP solutions. Significant opportunities exist in emerging markets with growing digital economies, the expansion of fraud prevention into new industry sectors, and the development of cloud-based and API-driven solutions. The market also benefits from increasing awareness of fraud risks among organizations of all sizes. Threats include rapidly evolving fraud techniques that can outpace prevention technologies, potential economic downturns affecting IT spending, and regulatory changes that may require costly system modifications. Additionally, the market faces challenges from data privacy concerns and the need to balance security with user experience in fraud prevention implementations.

Fraud Detection And Prevention Market Value Chain Analysis - Industry structure and value flow

The FDP market value chain encompasses multiple interconnected stages that deliver fraud prevention capabilities to end-users. The chain begins with component suppliers providing essential technologies including AI algorithms, data analytics platforms, and security protocols. Technology developers and solution providers then integrate these components into comprehensive fraud detection platforms, incorporating features like real-time monitoring, behavioral analytics, and risk scoring. System integrators play a crucial role in customizing and implementing these solutions within organizational IT environments, ensuring compatibility with existing systems and workflows. Value-added resellers and managed service providers extend market reach, particularly to small and medium enterprises that may lack internal expertise. End-users across various industries including BFSI, healthcare, and retail ultimately consume these solutions to protect against fraud losses. Supporting services such as consulting, training, and ongoing maintenance complete the value chain. The flow of value is increasingly characterized by partnerships and ecosystem approaches, where multiple providers collaborate to deliver comprehensive fraud prevention capabilities rather than competing on isolated solutions.

Key Investment Insights in the Fraud Detection And Prevention Market - Strategic investment recommendations

The FDP market presents compelling investment opportunities driven by strong growth projections and technological innovation. Strategic investors should focus on companies developing AI and machine learning capabilities, as these technologies are becoming essential differentiators in fraud detection effectiveness. Cloud-based FDP solutions represent a particularly attractive investment segment due to their scalability, cost advantages, and growing enterprise adoption. The market also offers opportunities in specialized fraud prevention for emerging sectors such as healthcare, where digital transformation is creating new fraud vulnerabilities. Investors should consider companies with strong intellectual property portfolios and those demonstrating ability to integrate multiple fraud prevention capabilities into unified platforms. Geographic expansion into high-growth markets in Asia-Pacific and Latin America presents additional investment potential, particularly for companies with adaptable solutions that can address varying regulatory environments. Strategic partnerships and acquisitions that enhance technological capabilities or expand market reach should be viewed favorably. However, investors should be mindful of implementation challenges and the need for continuous innovation to address evolving fraud techniques.

Fraud Detection And Prevention Market Conclusion - Summary and key takeaways

The Fraud Detection and Prevention market is positioned for substantial growth over the coming years, driven by digital transformation, increasing fraud sophistication, and expanding regulatory requirements. The market's projected growth from $47.76 billion to $136.60 billion by 2032, at a CAGR of 16.20%, reflects the critical importance of fraud prevention in today's digital economy. Key trends including AI-driven detection, real-time monitoring, and cloud-based solutions are reshaping the competitive landscape, while regional variations in adoption rates create diverse market opportunities. The market benefits from strong demand across multiple industry sectors, with BFSI leading but healthcare and retail showing particularly strong growth potential. Companies that can provide integrated, scalable solutions with advanced analytics capabilities are best positioned to capture market share. While challenges exist in terms of implementation complexity and evolving fraud techniques, the overall market trajectory remains strongly positive, driven by the fundamental need for organizations to protect against financial losses and maintain customer trust in an increasingly digital world.

Research Methodology - How this research was conducted

This market research was conducted using a comprehensive methodology combining primary and secondary research approaches. Primary research involved interviews with industry experts, technology providers, and end-users across multiple sectors to gather firsthand insights into market dynamics, challenges, and opportunities. Secondary research included analysis of company annual reports, financial filings, industry publications, and market databases to validate findings and establish quantitative benchmarks. The research methodology employed both top-down and bottom-up approaches to estimate market size and growth projections, ensuring accuracy through triangulation of multiple data sources. Market segmentation analysis was conducted based on industry verticals, component types, and deployment models, with regional assessments providing geographic context. The research team applied rigorous validation processes to ensure data reliability and consistency across all market estimates. Competitive landscape analysis included assessment of company capabilities, market positioning, and strategic initiatives through public disclosures and industry analyst reports.

Research Scope - Coverage and limitations

This research report covers the global Fraud Detection and Prevention market with comprehensive analysis of market size, growth trends, competitive landscape, and regional dynamics. The scope encompasses all major industry segments including BFSI, healthcare, manufacturing, retail, and telecommunications, with detailed examination of solution and service components deployed across on-premises and cloud environments. The research timeframe extends from 2025 through 2032, with historical context provided for market evolution. Geographic coverage includes North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa regions, with regional market dynamics thoroughly analyzed. The report examines key market drivers, restraints, challenges, and opportunities, along with emerging trends and technological developments. However, the research has limitations in terms of granular company-level financial data for private firms and potential variations in regional data availability. The scope focuses on commercial FDP solutions and does not extensively cover government or defense-specific fraud prevention applications.

Key Companies and Recent Developments in the Fraud Detection And Prevention Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The FDP market features several key companies driving innovation and market evolution through strategic initiatives. IBM Corporation has recently enhanced its Trusteer fraud prevention solutions with advanced AI capabilities and expanded cloud deployment options. SAP SE announced new fraud management modules integrated with its S/4HANA platform, targeting enterprise customers with complex fraud prevention needs. FICO continues to evolve its Falcon platform with machine learning enhancements and real-time detection capabilities, while forming strategic partnerships with payment processors. SAS Institute Inc. launched new behavioral analytics modules and expanded its fraud detection offerings for healthcare and government sectors. Fiserv, Inc. introduced enhanced fraud prevention tools specifically designed for small and medium financial institutions. Accertify, Inc. developed new e-commerce fraud prevention solutions with improved chargeback management capabilities. BAE Systems expanded its financial crime prevention offerings with advanced transaction monitoring systems. Securonix announced next-generation security analytics platforms with enhanced fraud detection features. PayPal continues to innovate in payment fraud prevention while expanding its merchant protection services. These companies are actively pursuing partnerships, acquisitions, and product innovations to strengthen their market positions and address evolving fraud threats.