Terminal Tractor Market Overview - Definition, scope, and significance

Terminal tractors, also known as yard trucks or shunt trucks, are specialized vehicles designed for moving semi-trailers and containers within freight terminals, warehouses, ports, and distribution centers. These vehicles play a crucial role in logistics and material handling operations by efficiently moving heavy loads over short distances. The terminal tractor market encompasses various propulsion types including diesel, electric, hybrid, and CNG-powered vehicles, catering to diverse applications such as material handling, logistics, distribution, airport operations, and container terminals. The market's significance lies in its ability to optimize yard operations, reduce manual labor, improve safety, and enhance overall supply chain efficiency in an increasingly globalized trade environment.

Terminal Tractor Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles

The terminal tractor market is driven by several factors including the rapid growth of e-commerce, increasing international trade volumes, and the need for efficient logistics operations. The expansion of port infrastructure and the growing emphasis on automation in material handling operations are also significant drivers. However, the market faces restraints such as high initial investment costs, particularly for electric and autonomous models, and the need for specialized training for operators. Challenges include the integration of new technologies with existing infrastructure and the regulatory hurdles associated with autonomous vehicles. Opportunities abound in the development of electric and autonomous terminal tractors, driven by environmental regulations and the push for operational efficiency. The market also presents opportunities in emerging economies where infrastructure development is accelerating.

Terminal Tractor Market Growth Trends - Current and emerging trends shaping the market

The terminal tractor market is experiencing several notable growth trends. There is a clear shift towards electric and hybrid propulsion systems, driven by environmental concerns and stricter emission regulations. Automation is another significant trend, with semi-autonomous and fully automated terminal tractors gaining traction in large-scale operations. The integration of IoT and telematics for improved fleet management and predictive maintenance is becoming increasingly common. Additionally, there is a trend towards customization, with manufacturers offering tailored solutions for specific applications such as airport ground support or specialized container handling. The market is also seeing a rise in rental and leasing models, providing flexibility to end-users and reducing capital expenditure barriers.

COVID-19 Impact on the Terminal Tractor Market - Pandemic effects and recovery trajectory

The COVID-19 pandemic had a mixed impact on the terminal tractor market. Initially, the market experienced a slowdown due to supply chain disruptions, reduced manufacturing activities, and economic uncertainties. However, the pandemic also highlighted the importance of resilient and efficient logistics operations, leading to increased investments in automation and modernization of terminal facilities. The e-commerce boom during lockdowns further accelerated the demand for efficient material handling solutions. As economies recover, the terminal tractor market is expected to witness a rebound, with a particular focus on electric and autonomous vehicles to meet new safety and efficiency standards. The recovery trajectory is likely to be steady, with long-term growth prospects remaining strong as global trade volumes recover and expand.

Terminal Tractor Market Competitive Landscape - Major competitors and market consolidation

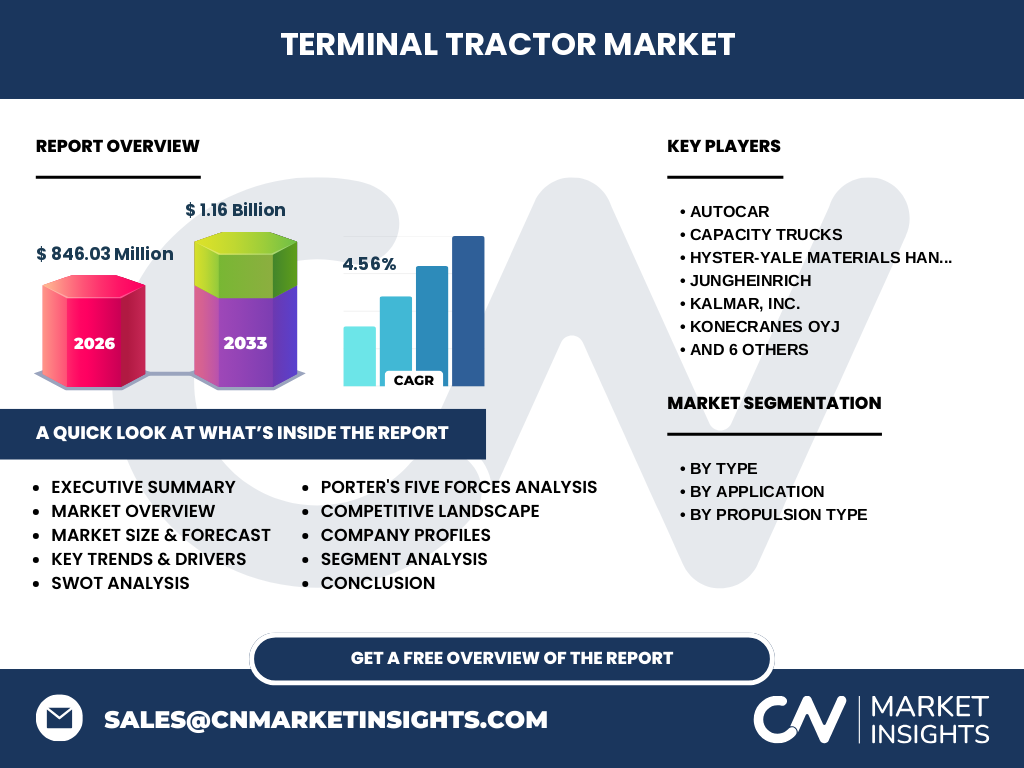

The terminal tractor market features a mix of established players and emerging companies, creating a moderately consolidated competitive landscape. Major competitors include industry giants such as Kalmar, Konecranes, and Hyster-Yale Materials Handling, which leverage their extensive experience in material handling equipment. Specialized terminal tractor manufacturers like Capacity Trucks, TICO Tractors, and Terberg Group BV are also significant players, known for their focused expertise in this niche market. The market has seen some consolidation through strategic partnerships and acquisitions, as larger companies seek to expand their product portfolios and technological capabilities. Competition is primarily based on factors such as product innovation, technological advancements, pricing, and after-sales service. The emergence of electric and autonomous technologies is likely to intensify competition as companies race to establish dominance in these growing segments.

Executive Summary - High-level overview and key findings about Terminal Tractor Market

The terminal tractor market is poised for steady growth, with a projected CAGR of 4.56% from 2027 to 2033, reaching a value of 1.16 billion USD. This growth is driven by the increasing demand for efficient logistics solutions, the expansion of global trade, and the push towards automation and electrification in material handling operations. The market is segmented by type (automated, semi-autonomous, and manual), application (material handling, logistics, distribution, airport, and container terminals), and propulsion type (diesel, electric, hybrid, and CNG). Key players in the market are focusing on technological innovations, particularly in electric and autonomous vehicles, to meet evolving customer needs and regulatory requirements. The market presents significant opportunities in emerging economies and in the development of sustainable, efficient terminal tractor solutions.

Terminal Tractor Market Forecast - Projections for 2025-2032 period

The terminal tractor market is expected to witness steady growth over the forecast period from 2025 to 2032. Starting from a market size of 846.03 million USD in 2026, the market is projected to reach 1.16 billion USD by 2033, representing a compound annual growth rate (CAGR) of 4.56%. This growth trajectory is underpinned by several factors, including the ongoing expansion of global trade, increasing investments in port and terminal infrastructure, and the growing adoption of electric and autonomous terminal tractors. The forecast period is likely to see a gradual shift in market dynamics, with electric and autonomous vehicles gaining a larger market share, particularly in developed economies. The Asia-Pacific region is expected to be a key growth driver, fueled by rapid industrialization and infrastructure development in countries like China and India.

Terminal Tractor Market Size and Share by Segmentation - Breakdown by {segmentData}

The terminal tractor market is segmented by type, application, and propulsion type, each contributing differently to the overall market size and share. In terms of type, manual terminal tractors currently dominate the market due to their lower cost and widespread adoption. However, automated and semi-autonomous tractors are expected to gain significant market share, driven by the push for operational efficiency and safety. By application, material handling and logistics segments are the largest contributors to market size, reflecting the critical role of terminal tractors in these operations. The container terminals segment is also expected to see substantial growth, driven by the expansion of global shipping activities. Regarding propulsion type, diesel-powered terminal tractors currently hold the largest market share due to their established infrastructure and lower initial costs. However, electric and hybrid tractors are gaining traction, particularly in regions with strict emission regulations, and are expected to capture a larger market share in the coming years.

Global Terminal Tractor Market Size and Share by Region - Geographic distribution

The global terminal tractor market exhibits varying growth patterns across different regions. North America and Europe currently hold significant market shares, driven by advanced infrastructure, high adoption of automation technologies, and stringent environmental regulations. These regions are also at the forefront of electric and autonomous terminal tractor adoption. The Asia-Pacific region is expected to witness the highest growth rate during the forecast period, fueled by rapid industrialization, expanding port infrastructure, and increasing foreign investments in countries like China, India, and Southeast Asian nations. Latin America and the Middle East & Africa regions, while currently holding smaller market shares, present substantial growth opportunities due to ongoing infrastructure development and increasing trade activities. The regional distribution of the market is likely to evolve, with emerging economies gradually increasing their share as they invest in modernizing their logistics and material handling capabilities.

Regional Analysis of the Terminal Tractor Market - Detailed regional market performance

Regional analysis of the terminal tractor market reveals distinct performance patterns and growth drivers across different geographies. In North America, the market is characterized by high adoption rates of advanced technologies, including electric and autonomous vehicles, driven by strict emission regulations and a focus on operational efficiency. Europe follows a similar trend, with countries like Germany and the Netherlands leading in the adoption of sustainable terminal tractor solutions. The Asia-Pacific region, particularly China and India, is experiencing rapid market growth due to massive infrastructure investments and the expansion of manufacturing and logistics sectors. This region is also seeing increased demand for electric terminal tractors as governments push for cleaner transportation solutions. Latin America is gradually modernizing its port and terminal operations, presenting opportunities for market growth, while the Middle East & Africa region is focusing on developing its logistics infrastructure to support growing trade activities, particularly in the Gulf Cooperation Council (GCC) countries.

Leading Company Profiles in the Terminal Tractor Market - Industry players and strategies

The terminal tractor market is populated by several key players, each with distinct strategies and market positions. Kalmar, a part of Cargotec Corporation, is a leading provider of terminal tractors, known for its innovative solutions and focus on automation and electrification. Konecranes, another major player, offers a range of terminal tractors with an emphasis on ergonomic design and fuel efficiency. Capacity Trucks specializes in electric and alternative fuel terminal tractors, positioning itself as a sustainable solution provider. TICO Tractors is known for its Pro-Spotter model, which has gained popularity in North American ports. Terberg Group BV, a Dutch company, offers a wide range of terminal tractors with a focus on customization for specific applications. These companies are adopting strategies such as product innovation, strategic partnerships, and expansion into emerging markets to strengthen their market positions and capitalize on growth opportunities.

Porter's Five Forces Analysis of the Terminal Tractor Market - Competitive forces assessment

Porter's Five Forces analysis provides insights into the competitive dynamics of the terminal tractor market. The threat of new entrants is moderate, as the market requires significant capital investment and technical expertise, creating barriers to entry. However, the growing demand for electric and autonomous vehicles may lower these barriers over time. The bargaining power of buyers is relatively high due to the availability of multiple suppliers and the commoditized nature of some terminal tractor models. Suppliers of key components, particularly for electric and autonomous systems, have gained some bargaining power as their technologies become critical to product differentiation. The threat of substitutes is low, as terminal tractors are specialized vehicles with unique capabilities essential for yard operations. Competitive rivalry is intense, with numerous players competing on factors such as price, technology, and after-sales service. The market is also seeing increased competition from technology companies entering the autonomous vehicle space.

SWOT Analysis of the Terminal Tractor Market - Strengths, weaknesses, opportunities, threats

A SWOT analysis of the terminal tractor market reveals several key factors influencing its growth and development. Strengths of the market include the essential role of terminal tractors in efficient logistics operations, ongoing technological advancements, and the growing demand for automation and electrification in material handling. Weaknesses include the high initial costs of advanced models, particularly electric and autonomous vehicles, and the need for specialized infrastructure and training. Opportunities abound in the development of sustainable and smart terminal tractor solutions, expansion into emerging markets, and the integration of IoT and AI technologies for improved fleet management. Threats to the market include economic uncertainties affecting trade volumes, potential supply chain disruptions, and the rapid pace of technological change that may render existing models obsolete. Additionally, regulatory challenges related to autonomous vehicles and varying emission standards across regions pose potential threats to market growth.

Terminal Tractor Market Value Chain Analysis - Industry structure and value flow

The terminal tractor market value chain encompasses several key stages, from raw material suppliers to end-users. At the beginning of the chain, suppliers of raw materials such as steel, electronics, and batteries provide the essential components for terminal tractor manufacturing. Original Equipment Manufacturers (OEMs) then assemble these components into finished products, incorporating various technologies and design features. The distribution network, including dealers and distributors, plays a crucial role in bringing these products to market and providing after-sales support. End-users, primarily logistics companies, ports, and distribution centers, form the final link in the value chain, utilizing terminal tractors for their material handling needs. Value is added at each stage through technological innovations, customization, and service offerings. The growing trend towards electric and autonomous vehicles is reshaping the value chain, with increased emphasis on battery technology and software development, while aftermarket services and fleet management solutions are becoming increasingly important sources of value.

Key Investment Insights in the Terminal Tractor Market - Strategic investment recommendations

The terminal tractor market presents several attractive investment opportunities for both existing players and new entrants. Key investment areas include the development of electric and autonomous terminal tractors, driven by environmental regulations and the push for operational efficiency. Investments in battery technology and charging infrastructure are crucial to support the growing demand for electric vehicles. There are also significant opportunities in software development for fleet management, predictive maintenance, and autonomous driving systems. Strategic partnerships and collaborations between terminal tractor manufacturers and technology companies can accelerate innovation and market penetration. Investments in emerging markets, particularly in Asia-Pacific and Latin America, offer potential for high growth as these regions continue to develop their logistics infrastructure. Additionally, investments in aftermarket services, including maintenance, repair, and fleet management solutions, can provide stable revenue streams and enhance customer loyalty.

Terminal Tractor Market Conclusion - Summary and key takeaways

The terminal tractor market is on a growth trajectory, driven by the increasing demand for efficient logistics solutions, the expansion of global trade, and the push towards automation and electrification. With a projected CAGR of 4.56% from 2027 to 2033, the market is expected to reach 1.16 billion USD by 2033. Key trends shaping the market include the shift towards electric and autonomous vehicles, the integration of IoT and AI technologies, and the growing importance of sustainability in material handling operations. While challenges exist, such as high initial costs and regulatory hurdles, the market presents significant opportunities for innovation and growth, particularly in emerging economies and in the development of smart, sustainable terminal tractor solutions. As the industry continues to evolve, companies that can effectively navigate technological changes, meet diverse customer needs, and capitalize on emerging market opportunities are likely to emerge as leaders in this dynamic sector.

Research Methodology - How this research was conducted

This comprehensive market research on the terminal tractor market was conducted using a robust methodology combining primary and secondary research techniques. Primary research involved interviews with industry experts, including terminal tractor manufacturers, suppliers, end-users, and technology providers. These interviews provided valuable insights into market trends, technological developments, and future outlook. Secondary research encompassed a thorough analysis of industry reports, company annual reports, press releases, and relevant publications. Market data was triangulated using multiple sources to ensure accuracy and reliability. The research also incorporated a detailed analysis of patent filings, product launches, and strategic developments by key market players. Statistical modeling and forecasting techniques were employed to project market growth and segment performance. The research methodology was designed to provide a holistic view of the terminal tractor market, covering all major aspects from market dynamics to competitive landscape and future trends.

Research Scope - Coverage and limitations

The scope of this research on the terminal tractor market encompasses a comprehensive analysis of the global market, including detailed segmentation by type, application, and propulsion type. The research covers key geographic regions, including North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. It provides insights into market size, growth trends, competitive landscape, and future projections up to 2033. The research also delves into specific aspects such as technological advancements, regulatory environment, and investment opportunities. However, it's important to note that while the research aims to provide a thorough analysis, it may not capture every minor player or niche segment in the market. Additionally, the rapidly evolving nature of technology in this sector means that some specific technological developments may not be fully reflected in the current analysis. The research focuses on commercially available terminal tractor solutions and may not extensively cover experimental or prototype technologies still in development.

Key Companies and Recent Developments in the Terminal Tractor Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments

The terminal tractor market features several key players driving innovation and competition. Kalmar, a global leader in cargo and material handling solutions, has been focusing on electric and automated terminal tractors, with recent developments in their ECG50-140 electric forklift range. Konecranes has introduced the E-VER electric empty container handler, showcasing their commitment to sustainable solutions. Capacity Trucks has launched the all-electric Excalibur E-Series terminal tractors, targeting the North American market. TICO Tractors continues to innovate with their Pro-Spotter models, introducing features like automated manual transmissions and advanced safety systems. Terberg Group BV has expanded its electric vehicle offerings with the YT202-EV terminal tractor. In terms of strategic developments, several companies have announced partnerships to enhance their technological capabilities. For instance, Hyster-Yale Materials Handling has partnered with nuTonomy to develop autonomous container handling trucks. These developments reflect the industry's focus on electrification, automation, and sustainability, as companies strive to meet evolving customer needs and regulatory requirements.