What is the Manufacturing Execution System (MES) Market Overview – Definition, scope, and significance?

The Manufacturing Execution System (MES) market comprises solutions that monitor, control, and synchronize production processes from raw material receipt to finished goods dispatch. MES bridges the gap between enterprise‑level planning systems (ERP) and shop‑floor operations, delivering real‑time visibility, traceability, and quality assurance. Its scope spans discrete, process, and hybrid manufacturing environments across industries such as automotive, aerospace, electronics, and pharmaceuticals. By enabling data‑driven decision making, MES drives operational efficiency, reduces waste, and enhances compliance, making it a cornerstone of Industry 4.0 transformation.

What are the key drivers, restraints, challenges, and opportunities influencing the MES market?

Key drivers include the accelerating adoption of smart factories, the need for real‑time production analytics, and regulatory pressures for traceability. Digital transformation initiatives and the shift to cloud‑based deployments further stimulate demand. Restraints stem from high initial implementation costs and integration complexities with legacy systems. Challenges involve cybersecurity concerns and a shortage of skilled MES professionals. Opportunities arise from expanding applications of AI/ML for predictive manufacturing, the growing SME segment seeking scalable cloud solutions, and emerging markets investing in advanced automation.

What are the current growth trends shaping the MES market?

Recent trends feature a rapid migration to cloud‑native MES platforms, offering subscription‑based pricing that lowers entry barriers. Edge computing is being leveraged for faster on‑premise data processing, while hybrid deployment models combine cloud scalability with on‑site control. The integration of Internet of Things (IoT) sensors enhances real‑time data capture, and manufacturers are increasingly embedding advanced analytics and machine learning to move from reactive to predictive execution.

How has COVID‑19 impacted the MES market and what is the recovery trajectory?

The pandemic disrupted supply chains and forced many manufacturers to adopt remote monitoring capabilities, accelerating MES adoption for resilience. While initial projects slowed due to capital constraints, the need for digital visibility sparked renewed investment. Recovery has been strong, with firms prioritizing cloud deployments to enable flexible, location‑independent operations, positioning the MES market for robust post‑pandemic growth.

Who are the major competitors in the MES market and how is consolidation evolving?

The competitive landscape includes global technology leaders and niche specialists. Prominent players such as Siemens AG, Rockwell Automation Inc, SAP SE, Oracle Corp, and Honeywell International Inc dominate with comprehensive suites. Emerging challengers like 42Q, EAZYWORKS INC., and PSI Software SE focus on agile, cloud‑first solutions. The market sees consolidation through strategic acquisitions and partnerships, enabling incumbents to broaden their IoT and AI capabilities while smaller firms gain scale and market reach.

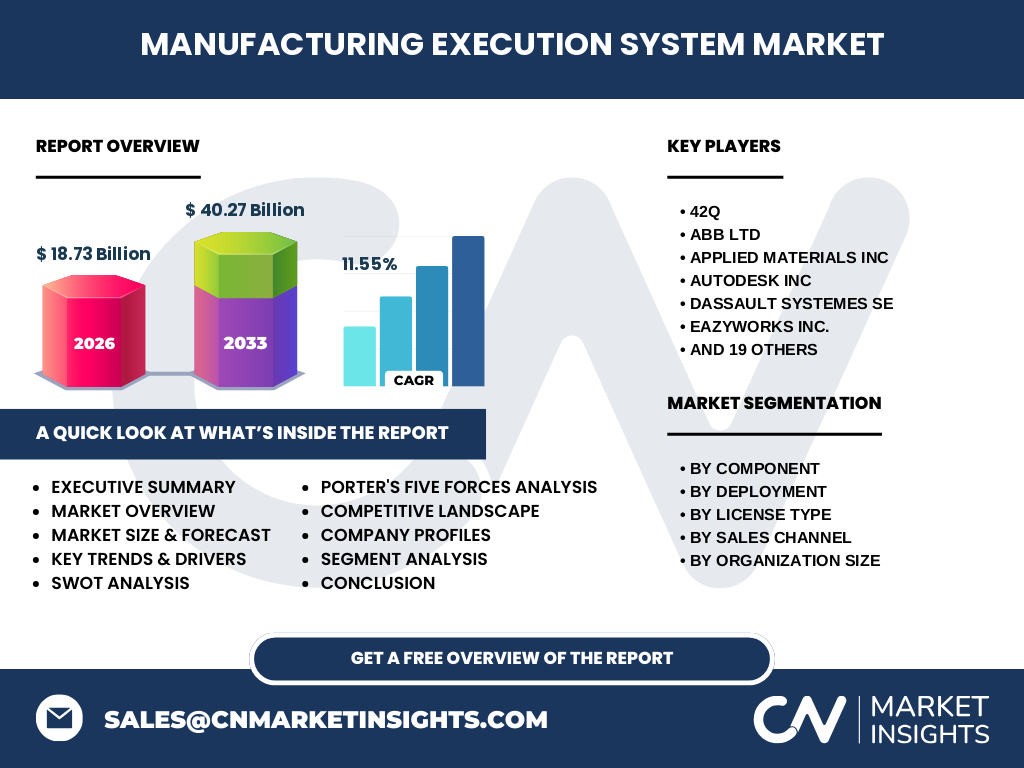

What are the high‑level findings and key takeaways from the MES market Executive Summary?

The MES market is projected to grow from a 2026 valuation of $18.73 billion to $40.27 billion by 2033, reflecting a CAGR of 11.55 % over the forecast horizon. Growth is propelled by digital‑factory initiatives, cloud adoption, and the need for real‑time operational intelligence. Cloud and subscription licensing are gaining traction, especially among SMEs, while large enterprises continue to invest in hybrid models. Competitive pressures are intensifying, with innovation focused on AI‑driven analytics and edge integration.

What are the forecasted market dynamics for 2025‑2032?

Based on the provided CAGR of 11.55 %, the MES market is expected to maintain double‑digit expansion through 2032. Drivers such as Industry 4.0 adoption, sustainability mandates, and the rollout of 5G networks will sustain demand. Cloud‑based solutions are forecasted to capture the largest share of new contracts, while on‑premise deployments will persist in highly regulated sectors. Subscription‑based licensing is projected to outpace traditional licensed models due to its flexibility and lower upfront cost.

How is the MES market sized and shared by component, deployment, license type, sales channel, and organization size?

Segmentation reveals two primary components: Software and Services, with software accounting for the majority of revenue. Deployment is split between Cloud and On‑Premise, with cloud gaining momentum. License types include Subscription‑Based and Licensed, where subscription models are expanding rapidly. Sales channels consist of Direct Sales and Channel Partners, the latter providing localized support and implementation expertise. Organization size segmentation distinguishes Large Enterprises, which favor integrated, hybrid solutions, and SMEs, which increasingly adopt cloud‑first, subscription‑based MES offerings.

What is the global MES market size and share by region?

The global market reached $18.73 billion in 2026 and is projected to exceed $40 billion by 2033. While specific regional dollar values are not disclosed, the market is globally distributed, with North America, Europe, and Asia‑Pacific leading adoption due to advanced manufacturing bases and strong Industry 4.0 initiatives. Emerging economies are expected to contribute a growing share as they modernize their production facilities.

What are the detailed regional performances in the MES market?

North America continues to lead in advanced MES implementations, driven by high automation levels and regulatory compliance requirements. Europe follows closely, emphasizing sustainability and smart‑factory standards. Asia‑Pacific shows the fastest growth rate, propelled by large‑scale manufacturing hubs in China, Japan, and South Korea investing heavily in digital transformation. Latin America and the Middle East & Africa exhibit modest but steady uptake as local manufacturers seek competitiveness.

Which companies are leading in the MES market and what are their strategic focuses?

Key players include Siemens AG, Rockwell Automation Inc, SAP SE, Oracle Corp, Honeywell International Inc, and Emerson Electric Co. Their strategies focus on expanding cloud portfolios, integrating AI/ML analytics, and forging ecosystem partnerships with IoT platform providers. New entrants such as 42Q and EAZYWORKS INC. concentrate on modular, subscription‑based solutions tailored for SMEs. Established firms are also pursuing acquisitions to enhance their service offerings and accelerate time‑to‑value.

How does Porter’s Five Forces assess the competitive environment of the MES market?

Threat of new entrants is moderate due to high development costs but lower for cloud‑native startups. Bargaining power of buyers is increasing as more vendors offer subscription models, giving customers pricing leverage. Supplier power is low because the core technology stack relies on widely available cloud infrastructure. Substitute threats are limited, with few alternatives providing comparable shop‑floor execution capabilities. Competitive rivalry is high, driven by rapid innovation and differentiation through AI, edge computing, and industry‑specific extensions.

What are the SWOT insights for the MES market?

Strengths: Strong demand for real‑time visibility, integration with ERP, and alignment with Industry 4.0.

Weaknesses: Complex integration with legacy equipment and high initial costs.

Opportunities: Cloud SaaS models, AI‑enabled predictive execution, and expansion into emerging economies.

Threats: Cybersecurity risks, talent shortages, and potential commoditization of basic MES functionalities.

What does the MES value chain look like?

The MES value chain starts with component suppliers (software developers, sensor manufacturers), followed by system integrators who tailor solutions to plant layouts. Cloud service providers host SaaS offerings, while consulting firms deliver implementation and training. Ongoing services include maintenance, upgrades, and analytics support. End‑users—manufacturers—close the loop by providing feedback that drives continuous product improvement.

What investment insights are critical for stakeholders in the MES market?

Investors should prioritize companies with strong cloud platforms and AI roadmaps, as subscription revenue offers recurring cash flow. Partnerships with IoT and edge providers enhance solution breadth. Targeting SMEs through scalable, low‑cost licensing models presents growth upside. Monitoring regulatory changes in pharma and aerospace can uncover niche opportunities where compliance‑driven MES adoption accelerates.

What are the concluding remarks and key takeaways for the MES market?

The MES market is on a decisive growth trajectory, propelled by digital transformation, cloud adoption, and the need for real‑time operational insights. The forecasted CAGR of 11.55 % underscores robust demand across all segments. Companies that innovate with AI, flexibly price subscription services, and forge strong ecosystem alliances will capture the majority of future market share.

How was the research methodology designed for this MES market study?

The study combined primary interviews with industry experts, technology vendors, and end‑user manufacturers, alongside secondary data from reputable industry reports, company filings, and market databases. Quantitative data were validated through triangulation, and qualitative insights were synthesized to produce a coherent market narrative. Forecasting employed a compound annual growth rate methodology anchored to the provided 2026 base and 2033 projection.

What is the scope of this MES market research?

The research covers global MES market dynamics, segmentation by component, deployment, license type, sales channel, and organization size, and regional analysis for major geographies. It includes competitive profiling of leading vendors, value‑chain mapping, and strategic frameworks such as Porter’s Five Forces and SWOT. Limitations pertain to the unavailability of granular regional revenue figures, which are presented in a qualitative context.

Which key companies and recent developments are shaping the MES market?

Leading firms such as Siemens AG, Rockwell Automation, SAP SE, and Oracle Corp have announced new cloud‑first MES platforms and AI‑enabled analytics modules. Honeywell International launched a subscription‑based MES suite targeting SMEs, while Emerson Electric introduced edge‑optimized execution controllers. Emerging players like 42Q and EAZYWORKS INC. secured strategic partnerships with IoT device manufacturers, expanding their ecosystem reach. Recent acquisitions by major vendors aim to strengthen service capabilities and accelerate time‑to‑market for advanced MES functionalities.