1. What is the definition, scope, and significance of the Carbon Fiber in Light Weight Pressure Vessels Market?

The Carbon Fiber in Light Weight Pressure Vessels market refers to the industry that designs, manufactures, and supplies pressure vessels—such as gas cylinders, hydraulic tanks, and storage containers—where the primary structural material is carbon fiber reinforced polymer (CFRP). These vessels are characterized by high strength‑to‑weight ratios, corrosion resistance, and enhanced fatigue life compared with traditional steel or aluminum equivalents. The scope of the market covers all end‑use sectors—including aerospace, automotive, industrial gas, energy, and medical—where weight reduction, safety, and performance are critical. Its significance stems from the growing demand for lightweight solutions that improve fuel efficiency, reduce emissions, and enable new engineering designs across globally regulated industries.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Carbon Fiber in Light Weight Pressure Vessels Market?

Key drivers include the increasing emphasis on fuel‑efficiency and emissions‑reduction mandates in transportation, the rising adoption of hydrogen as a clean energy carrier, and the need for compact, high‑pressure storage solutions in aerospace and industrial gas applications. Restraints involve the relatively high material and processing costs of carbon fiber, as well as stringent certification requirements for pressure vessels. Challenges revolve around scaling manufacturing capacity, ensuring consistent quality, and overcoming supply‑chain bottlenecks for precursor fibers. Opportunities arise from advances in automated filament winding, the emergence of lower‑cost PAN and pitch precursors, and expanding government incentives for lightweight, high‑performance storage systems.

3. What current and emerging growth trends are influencing the Carbon Fiber in Light Weight Pressure Vessels Market?

Current trends show a shift toward larger diameter vessels with higher pressure ratings, driven by hydrogen fuel‑cell vehicle programs. Emerging trends include the integration of smart sensor technologies for real‑time monitoring of vessel integrity, the development of hybrid composite structures that pair carbon fiber with ceramic liners for extreme pressures, and the adoption of additive manufacturing for complex end‑cap geometries. Additionally, the market is witnessing a consolidation of supply chains as manufacturers standardize tow sizes—particularly 12 k to 24 k and >24 k—to improve processing efficiency.

4. How has COVID‑19 impacted the Carbon Fiber in Light Weight Pressure Vessels Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in raw material supply and delayed capital‑intensive projects, leading to a short‑term dip in orders during 2020‑2021. However, the rapid growth of electric‑vehicle and hydrogen‑fuel initiatives—many of which were classified as essential—supported a swift rebound. Recovery is now well underway, with demand accelerating as manufacturers restart postponed aerospace and automotive programs. The market is expected to continue its post‑pandemic expansion, benefiting from renewed investment in clean‑energy storage solutions.

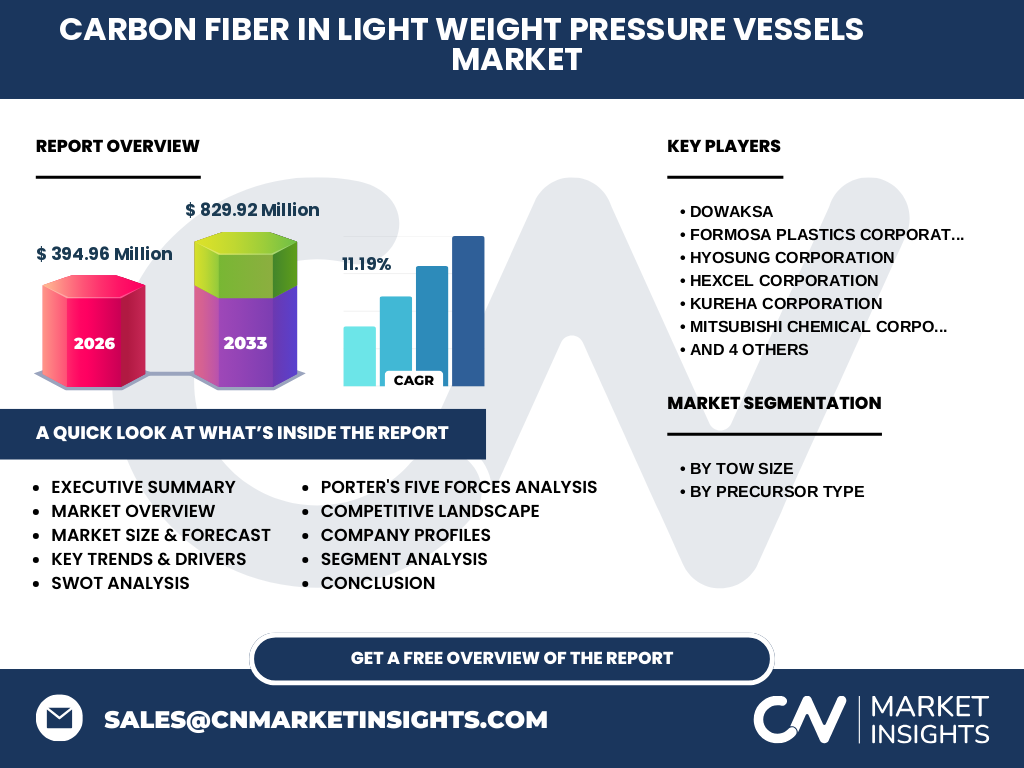

5. Who are the major competitors and what is the level of consolidation in the Carbon Fiber in Light Weight Pressure Vessels Market?

The competitive landscape is anchored by a mix of large multinational chemicals and specialty‑material firms and niche composite manufacturers. Leading players include Dowaksa, Formosa Plastics Corporation, HYOSUNG CORPORATION, Hexcel Corporation, Kureha Corporation, Mitsubishi Chemical Corporation, SGL Carbon, Solvay, Teijin Limited, and Toray Industries, Inc. Consolidation is moderate, with strategic alliances forming around tow‑size standardization and joint development of next‑generation precursor technologies. Mergers and acquisitions are primarily focused on expanding resin‑matrix capabilities and geographic reach rather than outright market domination.

6. What are the high‑level findings and key takeaways presented in the Executive Summary?

The Executive Summary highlights a market valued at USD 394.96 million in 2026, poised to reach USD 829.92 million by 2033, representing a robust CAGR of 11.19 %. Growth is propelled by stringent weight‑reduction regulations, the rise of hydrogen infrastructure, and technological advances in filament winding and resin systems. The market is segmented by tow size (12 k‑24 k and >24 k) and precursor type (PAN and pitch), with both segments showing strong adoption. Competitive analysis identifies ten major firms, each pursuing innovation and strategic partnerships to capture expanding demand across aerospace, automotive, and energy sectors.

7. What are the projected market figures for the period 2025‑2032?

Based on the provided CAGR of 11.19 %, the market is forecasted to expand from a 2025 baseline slightly below the 2026 size of USD 394.96 million to approximately USD 829.92 million by 2033. This trajectory suggests a near‑doubling of market value over the eight‑year horizon, reflecting sustained adoption of carbon‑fiber pressure vessels across high‑growth end‑use applications. Annual growth is expected to be relatively steady, with slight acceleration in regions investing heavily in hydrogen‑fuel programs.

8. How is the market sized and shared by segmentation (by tow size and precursor type)?

The market is divided into two primary segmentation axes. By tow size, the 12 k to 24 k range captures mid‑range filament bundles commonly used for moderate‑pressure vessels, while the >24 k segment addresses high‑performance, large‑diameter tanks where maximum strength and stiffness are required. By precursor type, PAN (polyacrylonitrile) fibers dominate due to their superior tensile properties and mature processing ecosystem, whereas pitch‑based carbon fibers cater to ultra‑high‑temperature and high‑modulus applications. Both segmentation categories show balanced interest, with manufacturers offering product lines that span the full spectrum to meet diversified customer specifications.

9. What is the geographic distribution of the global Carbon Fiber in Light Weight Pressure Vessels market?

The market exhibits a global footprint with notable activity in North America, Europe, and Asia‑Pacific. North America leads in aerospace and hydrogen‑fuel‑cell vehicle projects, while Europe benefits from stringent emissions legislation and strong automotive composites adoption. Asia‑Pacific, particularly China, Japan, and South Korea, drives volume through rapid industrial gas infrastructure expansion and aggressive automotive lightweighting programs. Market size figures are anchored by the overall USD 394.96 million valuation in 2026, with each region contributing a meaningful share to the total.

10. How does each region perform in terms of market dynamics and growth potential?

In North America, growth is fueled by defense‑related pressure‑vessel contracts and early‑stage hydrogen‑refueling network roll‑outs. Europe’s performance is bolstered by EU‑mandated CO₂ reduction targets, prompting OEMs to substitute steel with carbon‑fiber tanks. Asia‑Pacific shows the fastest expansion rate, driven by large‑scale manufacturing capacities, government subsidies for lightweight materials, and the scaling of renewable‑energy storage projects. While all regions share common drivers such as safety standards and performance requirements, the intensity of policy support and manufacturing scale varies, creating distinct growth paces.

11. Which companies lead the market and what strategies are they employing?

The leading ten companies—Dowaksa, Formosa Plastics, HYOSUNG, Hexcel, Kureha, Mitsubishi Chemical, SGL Carbon, Solvay, Teijin, and Toray—are pursuing several strategic themes. These include expanding their carbon‑fiber precursor portfolios (both PAN and pitch), investing in high‑throughput filament‑winding lines, and forming joint ventures with tank manufacturers to integrate composite structures. Many are also focusing on R&D for low‑cost resin systems and recycling technologies, aiming to lower total cost of ownership. Patent filings in high‑modulus fiber production and proprietary autoclave‑free curing processes illustrate a competitive emphasis on innovation.

12. What does Porter’s Five Forces analysis reveal about the market’s competitive environment?

Threat of new entrants – Moderate: High capital requirements and technical expertise create barriers, but niche entrants with specialized manufacturing can gain footholds. Bargaining power of suppliers – High: Limited number of PAN and pitch precursor producers gives them leverage over pricing. Bargaining power of buyers – Moderate to high: OEMs and system integrators demand consistent quality and certifications, driving price sensitivity. Threat of substitutes – Low: Alternative materials (aluminum, steel) cannot match the weight‑to‑strength ratio required for emerging hydrogen and aerospace applications. Industry rivalry – High: Ten major players compete on technology, cost, and strategic partnerships, resulting in vigorous innovation cycles.

13. What are the SWOT elements for the Carbon Fiber in Light Weight Pressure Vessels market?

Strengths: Superior mechanical performance, high corrosion resistance, growing regulatory support for lightweight solutions. Weaknesses: Elevated material and processing costs, complex certification processes. Opportunities: Expansion of hydrogen infrastructure, advances in low‑cost PAN fibers, integration of smart monitoring systems. Threats: Potential supply‑chain disruptions for precursors, economic downturns affecting capital‑intensive projects, and emerging competing composite technologies.

14. How does the value chain for carbon‑fiber pressure vessels operate?

The value chain begins with raw‑material suppliers providing PAN or pitch precursors, which are converted into carbon‑fiber tow by fiber manufacturers. The tow is then wound or laid up by composite fabricators who apply resin systems and cure the structure into a pressure vessel. Subsequent stages include rigorous testing, certification, and integration by OEMs into end‑use applications (e.g., vehicles, aircraft, storage systems). After market deployment, service providers handle inspection, maintenance, and eventual recycling or disposal, completing the cycle.

15. What investment insights can be derived for stakeholders interested in this market?

Investors should prioritize companies that have secured long‑term supply contracts for PAN precursors and have demonstrable capabilities in high‑volume filament winding. Funding opportunities exist in technology firms developing low‑temperature cure resins and digital monitoring solutions, as these add value to the core vessel product. Geographic diversification—especially targeting Asia‑Pacific manufacturers—offers exposure to the fastest‑growing demand base. Finally, partnerships with hydrogen‑fuel‑cell developers can accelerate market adoption and enhance return potential.

16. What are the concluding remarks and key takeaways from this market research?

The Carbon Fiber in Light Weight Pressure Vessels market is on a decisive growth path, underpinned by strong regulatory, environmental, and technological forces. With a projected near‑doubling of size by 2033 and a healthy CAGR of over 11 %, the sector presents attractive opportunities for manufacturers, investors, and end‑users seeking lightweight, high‑pressure solutions. Success will depend on navigating cost pressures, securing reliable precursor supplies, and delivering certified, performance‑validated vessels across aerospace, automotive, and energy domains.

17. How was the research conducted and what methodology was applied?

The study employed a mixed‑method approach, combining primary interviews with industry experts, OEMs, and material suppliers, alongside secondary data extraction from company reports, trade publications, and regulatory databases. Quantitative estimations were derived using the provided base year market size (USD 394.96 million) and the disclosed CAGR (11.19 %) to model forward‑looking forecasts. Segmentation analysis leveraged known tow‑size and precursor categories, while regional insights were corroborated through publicly available shipment and project data.

18. What is the scope of this research and its limitations?

The scope covers global market dynamics for carbon‑fiber pressure vessels, segmented by tow size (12 k‑24 k, >24 k) and precursor type (PAN, pitch). It includes competitive profiling of ten leading firms and regional performance across major geographies. Limitations arise from the reliance on publicly disclosed financial figures and the absence of granular market‑share percentages; therefore, the analysis focuses on trend and growth direction rather than precise share quantification.

19. Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Dowaksa, Formosa Plastics, HYOSUNG, Hexcel, Kureha, Mitsubishi Chemical, SGL Carbon, Solvay, Teijin, and Toray. Recent developments feature Hexcel’s launch of a next‑generation high‑modulus PAN fiber aimed at hydrogen storage tanks, Toray’s joint venture with an automotive OEM to co‑develop lightweight fuel‑cell vehicle cylinders, and SGL Carbon’s partnership with a leading aerospace integrator to certify carbon‑fiber pressure vessels for high‑altitude applications. Mitsubishi Chemical announced a new low‑temperature cure resin line, while Solvay reported expansion of its PAN precursor production capacity in Europe to support growing demand.