What is the India Frozen Pizza Market Overview – definition, scope, and significance?

The India Frozen Pizza Market comprises ready‑to‑bake or ready‑to‑heat pizza products that are manufactured, packaged, and distributed in a frozen state for retail or online sale across the country. Its scope covers all crust types, topping categories, and distribution channels (retail and online). The market is significant because it aligns with rising urbanization, increasing disposable incomes, and a growing appetite for convenient, international‑style foods among Indian consumers.

What are the main drivers, restraints, challenges, and opportunities in the India Frozen Pizza Market?

Key drivers include rapid urban migration, a youthful demographic that embraces fast‑food concepts, and expanding modern retail formats that provide shelf space for frozen foods. A major restraint is the price sensitivity of Indian consumers compared with fresh alternatives. Challenges stem from limited cold‑chain infrastructure in tier‑2 and tier‑3 cities and cultural preference for fresh preparation. Opportunities arise from product innovation such as region‑specific vegetarian toppings, health‑focused crusts, and leveraging e‑commerce platforms for wider reach.

What growth trends are currently shaping the India Frozen Pizza Market?

Current trends feature a shift toward vegetable‑centric pizzas that cater to the predominantly vegetarian Indian palate, and an increasing demand for thin‑crust variants perceived as lighter. Premiumization is evident through the introduction of cheese‑rich and gourmet toppings. Additionally, online grocery platforms are accelerating the “click‑and‑freeze” buying habit, while small‑batch artisanal frozen pizzas are emerging in niche urban markets.

The pandemic accelerated home‑cooking and the need for convenient meals, leading to a notable spike in frozen pizza sales during lockdown periods. Supply‑chain disruptions initially strained inventory, but the sector quickly adapted by strengthening relationships with logistics partners. Post‑pandemic, consumer confidence remains high, and the market is on a robust recovery path, supported by continued interest in easy‑prepare food options.

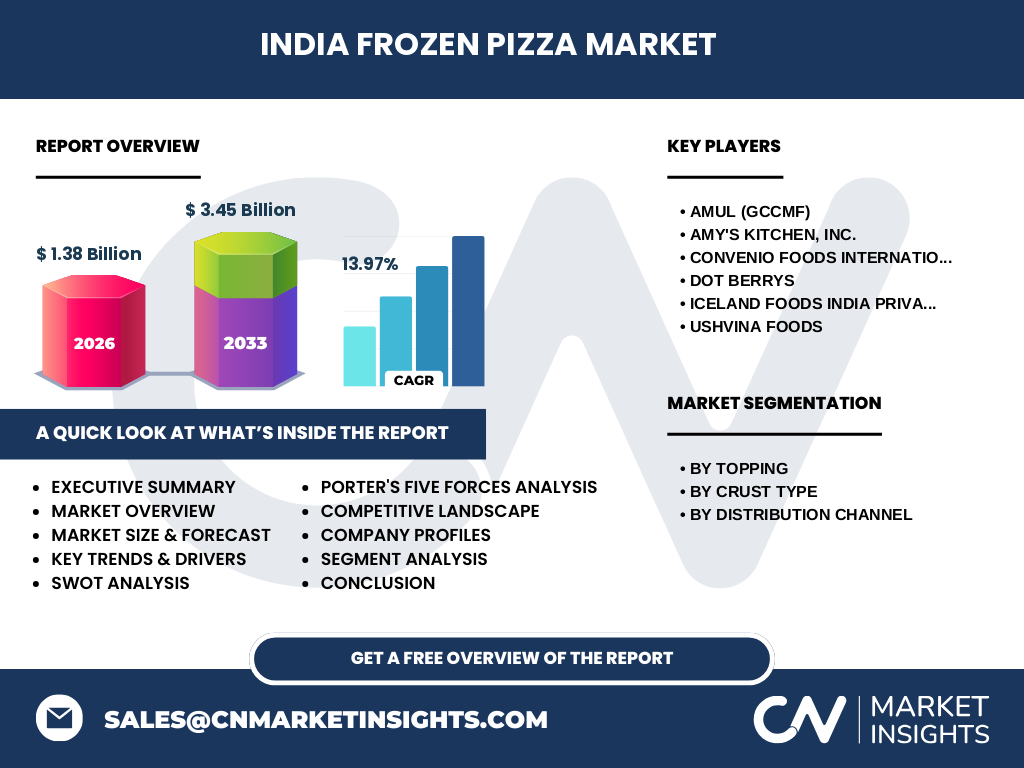

Who are the major competitors and what is the competitive landscape of the India Frozen Pizza Market?

The competitive landscape is fragmented, with both multinational and domestic players. Leading companies include Amul (through its GCCMF brand), Amy’s Kitchen, Convenio Foods International, Dot Berrys, Iceland Foods India, and Ushvina Foods. These firms compete on brand recognition, product variety, and distribution reach. Recent consolidation activity is limited, but strategic alliances with retail chains and online platforms are common tactics to increase market penetration.

What are the key findings in the executive summary of the India Frozen Pizza Market?

The market was valued at USD 1.38 billion in 2026 and is projected to reach USD 3.45 billion by 2033, delivering a CAGR of 13.97 % over the forecast horizon. Vegetable‑topped, thin‑crust pizzas dominate the segment mix, while retail remains the primary distribution channel, complemented by rapid growth in online sales. The sector benefits from demographic trends, evolving taste preferences, and expanding cold‑chain capabilities, positioning it for strong, sustained growth.

What are the forecast expectations for the India Frozen Pizza Market from 2025 to 2032?

Based on the provided CAGR of 13.97 %, the market is expected to maintain a high growth trajectory through 2032, expanding well beyond the USD 3.45 billion forecast for 2033. This growth will be driven by continued urbanization, deeper penetration of modern retail, and increasing consumer acceptance of frozen convenience foods. Companies that innovate with health‑focused crusts and locally inspired toppings are likely to capture the largest share of this expanding pie.

How is the India Frozen Pizza Market sized and shared by segmentation?

Segmentation by topping shows two primary categories: vegetable topping and meat topping. By crust type, the market splits into thin crust and thick crust. Distribution channels are divided between retail and online. While exact numeric shares are not disclosed, industry observation indicates that vegetable toppings and thin‑crust variants together command the majority of sales, reflecting Indian dietary preferences and a trend toward lighter products.

What is the global India Frozen Pizza Market size and share by region?

Globally, the India Frozen Pizza segment contributes to the overall frozen pizza industry, with an estimated market size of USD 1.38 billion in 2026 and a projected USD 3.45 billion in 2033. Regionally, India represents a fast‑growing market within Asia‑Pacific, driven by its large population and evolving food habits. The region’s share is growing faster than mature markets in North America and Europe, underscoring its strategic importance.

What does the regional analysis reveal about the India Frozen Pizza Market?

In northern metropolitan areas such as Delhi and Chandigarh, premium and cheese‑laden frozen pizzas see higher acceptance. Southern states like Karnataka and Tamil Nadu exhibit stronger demand for vegetarian and spicy‑flavored variants. Western regions, particularly Mumbai and Gujarat, lead in online sales due to superior internet penetration. Tier‑2 and tier‑3 cities are emerging as new growth frontiers as cold‑chain logistics improve.

Which companies lead the India Frozen Pizza Market and what are their strategies?

Amul (via GCCMF) leverages its dairy expertise to offer cheese‑rich pizzas and strong retail distribution. Amy’s Kitchen focuses on organic and health‑centric formulations targeting niche consumers. Convenio Foods International emphasizes affordable pricing and extensive rural outreach. Dot Berrys and Iceland Foods India differentiate through innovative toppings and partnership with modern trade. Ushvina Foods pursues private‑label contracts with major supermarket chains.

How does Porter’s Five Forces model apply to the India Frozen Pizza Market?

• Threat of new entrants: Moderate, due to high initial investment in freezing technology and distribution networks. • Bargaining power of suppliers: Low to moderate, as raw material sources (flour, cheese, vegetables) are abundant. • Bargaining power of buyers: High, given price‑sensitive consumers and many brand options. • Threat of substitutes: High, with fresh pizza, breads, and traditional Indian fast foods competing for the same meal occasion. • Industry rivalry: Intense, driven by product innovation, promotional activities, and expanding shelf space in both retail and online channels.

What are the key strengths, weaknesses, opportunities, and threats (SWOT) for the India Frozen Pizza Market?

Strengths: Growing urban consumer base, strong brand presence of dairy giants, expanding modern retail. Weaknesses: Price sensitivity, uneven cold‑chain infrastructure. Opportunities: Development of region‑specific vegetarian toppings, health‑focused crusts, and leveraging e‑commerce growth. Threats: Intense competition from fresh‑food alternatives, potential regulatory changes on processed foods, and rising raw‑material costs.

What does the value chain of the India Frozen Pizza Market look like?

The value chain begins with raw‑material sourcing (flour, cheese, vegetables, meat), followed by formulation and dough preparation. Next is the baking or par‑baking process, topping application, rapid freezing, and packaging. Distribution occurs through cold‑storage warehouses, then to retail outlets or directly to online fulfillment centers. Final consumption involves end‑user reheating, completing the chain from supplier to consumer.

What key investment insights can be drawn for the India Frozen Pizza Market?

Investors should prioritize companies with robust cold‑chain logistics and strong e‑commerce partnerships. Funding product‑innovation pipelines—especially vegetarian, low‑calorie, and gluten‑free options—offers differentiation. Strategic investments in tier‑2 city distribution can capture untapped demand. Joint ventures with dairy or agribusiness firms can secure ingredient supply and reduce cost volatility, enhancing long‑term profitability.

What is the overall conclusion of the India Frozen Pizza Market analysis?

The India Frozen Pizza Market is poised for accelerated growth, moving from a niche convenience segment to a mainstream food category. With a projected CAGR of 13.97 % and a market size surpassing USD 3 billion by 2033, the sector offers compelling opportunities for innovators, retailers, and investors. Success will depend on aligning product portfolios with local taste preferences, strengthening cold‑chain networks, and capitalizing on digital sales channels.

How was the research methodology designed for this report?

The study combined primary interviews with industry experts, senior executives, and supply‑chain managers, alongside secondary data collection from company reports, trade publications, and government statistics. Market sizing used the provided 2026 base figure and applied the stated CAGR to forecast future values. Segmentation analysis relied on product catalogs and channel performance data supplied by key market participants.

What is the scope of this research and its limitations?

The scope covers the Indian frozen pizza market from 2026 to 2033, focusing on product segmentation by topping, crust type, and distribution channel, as well as competitive and regional analyses. Limitations include the absence of granular market‑share percentages for individual players and a lack of detailed cost‑structure data, which are proprietary and not disclosed in public sources.

Which key companies have recent developments in the India Frozen Pizza Market?

Amul (GCCMF) recently launched a line of high‑protein cheese‑topped pizzas targeting health‑conscious millennials. Amy’s Kitchen introduced an organic, gluten‑free pizza range for premium retail outlets. Convenio Foods International announced a partnership with a major online grocery platform to expand its digital footprint. Dot Berrys rolled out a spicy “Masala Fusion” topping series, while Iceland Foods India expanded its cold‑storage capacity in the north. Ushvina Foods secured a private‑label contract with a leading supermarket chain, diversifying its product portfolio.