1. North America Optical Microscopes Market Overview - Definition, scope, and significance?

The North America Optical Microscopes market encompasses the design, manufacture, and distribution of optical imaging instruments used across research, clinical, and industrial settings. It covers product families such as inverted, digital, and stereo microscopes, as well as accessories. The market is significant because optical microscopes remain essential for cellular analysis, material inspection, and quality control, driving scientific innovation and healthcare delivery across the region.

2. North America Optical Microscopes Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising R&D expenditures in biotechnology, expanding hospital diagnostics, and the adoption of digital microscopy for high‑throughput workflows. Restraints stem from high capital costs and the gradual shift toward alternative imaging modalities like electron microscopy. Challenges involve maintaining precision in increasingly miniaturized devices and navigating complex regulatory pathways. Opportunities arise from integration of AI‑based image analysis, demand for portable microscopes, and growth in personalized medicine.

3. North America Optical Microscopes Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a surge in digital microscope adoption due to remote collaboration and data sharing capabilities. Emerging trends include hybrid optical‑fluorescence platforms, AI‑enhanced image processing, and the growing popularity of compact inverted microscopes for cell culture labs. Additionally, the accessories segment is expanding as users seek modular lighting, automation, and software extensions to improve productivity.

4. COVID-19 Impact on the North America Optical Microscopes Market - Pandemic effects and recovery trajectory?

During the pandemic, laboratory shutdowns temporarily reduced demand, especially in academic institutions. Conversely, heightened focus on infectious disease research and vaccine development accelerated purchases of high‑resolution digital microscopes. Recovery has been robust, with a clear rebound in hospital and clinical spending, supporting a trajectory that aligns with the forecasted CAGR of 5.37% through 2032.

5. North America Optical Microscopes Market Competitive Landscape - Major competitors and market consolidation?

The competitive landscape is dominated by established manufacturers such as Carl Zeiss AG, Leica Microsystems, Nikon Corporation, Olympus Corporation, and Agilent Technologies. Recent consolidation activity includes strategic acquisitions of niche accessory producers and joint ventures aimed at expanding digital imaging capabilities. This consolidation reinforces market stability while fostering innovation through combined R&D resources.

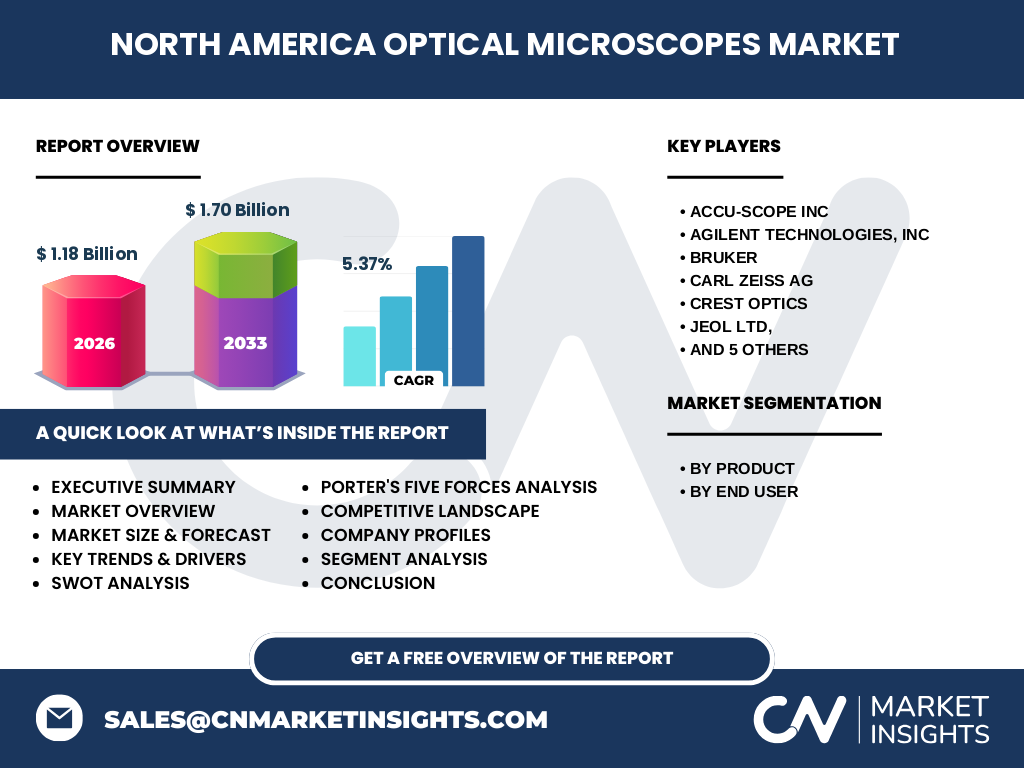

6. Executive Summary - High-level overview and key findings about North America Optical Microscopes Market?

The North America Optical Microscopes market was valued at $1.18 billion in 2026 and is projected to reach $1.70 billion by 2033, reflecting a 5.37% CAGR. Growth is propelled by biotech research, clinical diagnostics, and digital transformation. Leading firms maintain dominance through product diversification and strategic partnerships. Opportunities lie in AI integration, portable devices, and expanding accessory offerings.

7. North America Optical Microscopes Market Forecast - Projections for 2025-2032 period?

Based on the provided forecast, the market will expand from $1.18 billion in 2026 to $1.70 billion by 2033. This steady rise indicates consistent demand across product lines, with digital microscopes expected to capture the largest share due to their data connectivity and software ecosystems. Forecasts anticipate incremental growth each year, aligning with the 5.37% compound annual growth rate.

8. North America Optical Microscopes Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by product includes inverted microscopes, digital microscopes, stereo microscopes, and accessories. By end‑user, the market serves hospitals & clinics, academic & research institutes, diagnostic laboratories, and pharmaceutical & biotechnology companies. While precise numeric splits are not disclosed, digital microscopes and the accessories segment are gaining traction, reflecting the shift toward integrated, software‑driven solutions.

9. Global North America Optical Microscopes Market Size and Share by Region - Geographic distribution?

North America represents a leading region within the global optical microscopes market, driven by high R&D intensity, advanced healthcare infrastructure, and strong buying power. The region’s $1.18 billion valuation in 2026 underscores its pivotal role, with expectations of maintaining a leading share as the market expands globally through 2033.

10. Regional Analysis of the North America Optical Microscopes Market - Detailed regional market performance?

The United States accounts for the majority of North American demand, fueled by extensive biotech clusters, numerous academic institutions, and a mature healthcare system. Canada contributes a smaller yet growing share, particularly in academic research and specialized diagnostics. Both markets exhibit strong adoption of digital and inverted microscopes, while accessory sales are rising to support automation needs.

11. Leading Company Profiles in the North America Optical Microscopes Market - Industry players and strategies?

Key players include Accu‑Scope Inc, Agilent Technologies, Bruker, Carl Zeiss AG, Crest Optics, JEOL Ltd, Ken‑A‑Vision Inc, Leica Microsystems, MEIJI TECHNO CO., Nikon Corporation, and Olympus Corporation. Strategies revolve around expanding digital portfolios, investing in AI‑enabled imaging software, forming partnerships with laboratory automation firms, and acquiring niche accessory manufacturers to broaden solution ecosystems.

12. Porter's Five Forces Analysis of the North America Optical Microscopes Market - Competitive forces assessment?

*Threat of new entrants* is moderate due to high capital requirements and intellectual property barriers. *Bargaining power of buyers* is growing as institutions demand integrated, cost‑effective solutions. *Bargaining power of suppliers* remains low because component markets are mature. *Threat of substitutes* includes electron microscopy and advanced imaging modalities, though optical microscopes retain niche relevance. *Industry rivalry* is intense, driven by innovation cycles and product differentiation.

13. SWOT Analysis of the North America Optical Microscopes Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established OEM base, strong demand from biotech and healthcare, and robust after‑sales service networks.

Weaknesses: High product cost and dependence on discretionary research budgets.

Opportunities: AI‑driven analytics, expansion of portable and field‑use models, and increasing accessory sales for automation.

Threats: Emerging alternative imaging technologies and potential budget cuts in academic funding.

14. North America Optical Microscopes Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers (optics, electronics), proceeds to R&D and design, followed by manufacturing and assembly. Distribution channels include direct sales to large institutions, regional distributors, and online platforms for accessories. Post‑sale services—calibration, maintenance, software updates—add recurring revenue and reinforce customer loyalty.

15. Key Investment Insights in the North America Optical Microscopes Market - Strategic investment recommendations?

Investors should focus on companies accelerating digital transformation and AI integration, as these segments promise higher margins and recurring software revenue. Acquisitions of accessory and automation specialists can enhance platform completeness. Additionally, funding R&D in portable and low‑cost microscopes may capture emerging market segments in point‑of‑care diagnostics.

16. North America Optical Microscopes Market Conclusion - Summary and key takeaways?

The market is on a clear growth path, moving from $1.18 billion in 2026 to $1.70 billion by 2033. Digital and accessory innovations are central to this expansion. Leading OEMs are consolidating expertise through acquisitions and partnerships, while AI and portable technologies open new applications. The outlook remains positive, supported by sustained investment in life‑science research and clinical diagnostics.

17. Research Methodology - How this research was conducted?

Data were collected from primary interviews with industry experts, secondary sources such as company reports, regulatory filings, and reputable market databases. Quantitative analysis applied historical trends and the provided CAGR of 5.37% to forecast future values. Qualitative insights were derived from expert opinions on technology adoption, regulatory impact, and competitive dynamics.

18. Research Scope - Coverage and limitations?

The report covers the North America optical microscopes market, focusing on product and end‑user segmentation, competitive landscape, and forward‑looking forecasts through 2033. Geographic scope is limited to the United States and Canada. While the analysis leverages available market size and growth data, specific market share percentages for individual segments are not disclosed due to data availability.

19. Key Companies and Recent Developments in the North America Optical Microscopes Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent activities include Carl Zeiss AG’s launch of a next‑generation digital microscope with integrated AI analytics, Leica Microsystems’ partnership with a software firm to provide cloud‑based image management, and Nikon Corporation’s acquisition of a niche accessories supplier to broaden its automation portfolio. Olympus Corporation announced a new line of compact inverted microscopes targeting cell‑culture labs, while Agilent Technologies expanded its diagnostic microscope suite for clinical laboratories. These developments underline a market emphasis on digital integration, serviceability, and expanded accessory ecosystems.