What is the Europe Security Screening Market Overview – Definition, scope, and significance?

The Europe Security Screening Market comprises the manufacturing, distribution, and deployment of technologies used to detect prohibited items, threats, and illicit activities across a range of environments. Its scope includes hardware such as X‑ray scanners, biometric systems, explosive trace detectors, and electromagnetic metal detectors, as well as software integration and service support for applications at borders, airports, government facilities, and public places. The market is significant because it underpins the safety of millions of travelers, protects critical infrastructure, and supports regulatory compliance with stringent EU security directives.

What are the Europe Security Screening Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include heightened terrorist threats, stricter border‑control regulations, and increasing air passenger traffic. Technological advancement—particularly in AI‑enabled imaging and biometric verification—fuels demand. Restraints arise from high capital expenditure, lengthy procurement cycles, and privacy concerns surrounding biometric data. Challenges involve integration with legacy systems and the need for skilled operators. Opportunities lie in expanding screening solutions for mass‑gathering venues, adopting mobile screening units, and leveraging data analytics to improve threat detection efficiency.

What are the Europe Security Screening Market Growth Trends?

Current trends show a shift toward integrated, multi‑sensor platforms that combine X‑ray, metal detection, and biometrics into a single checkpoint solution. Adoption of cloud‑based analytics for real‑time threat assessment is emerging, as is the deployment of contactless biometric verification to meet hygiene expectations post‑COVID‑19. Additionally, there is growing interest in high‑throughput scanners capable of handling increasing passenger volumes without compromising detection accuracy.

How has COVID‑19 impacted the Europe Security Screening Market and what is the recovery trajectory?

The pandemic caused a temporary decline in passenger traffic, reducing short‑term demand for new screening equipment. However, it also accelerated the adoption of contactless technologies and heightened awareness of biosecurity, prompting operators to invest in touch‑free biometric systems. Recovery began in late 2021 as travel resumed, and the market has rebounded strongly, with a trajectory that aligns with the projected CAGR of 5.88% through 2032, indicating robust long‑term growth.

Who are the major competitors in the Europe Security Screening Market and what is the level of market consolidation?

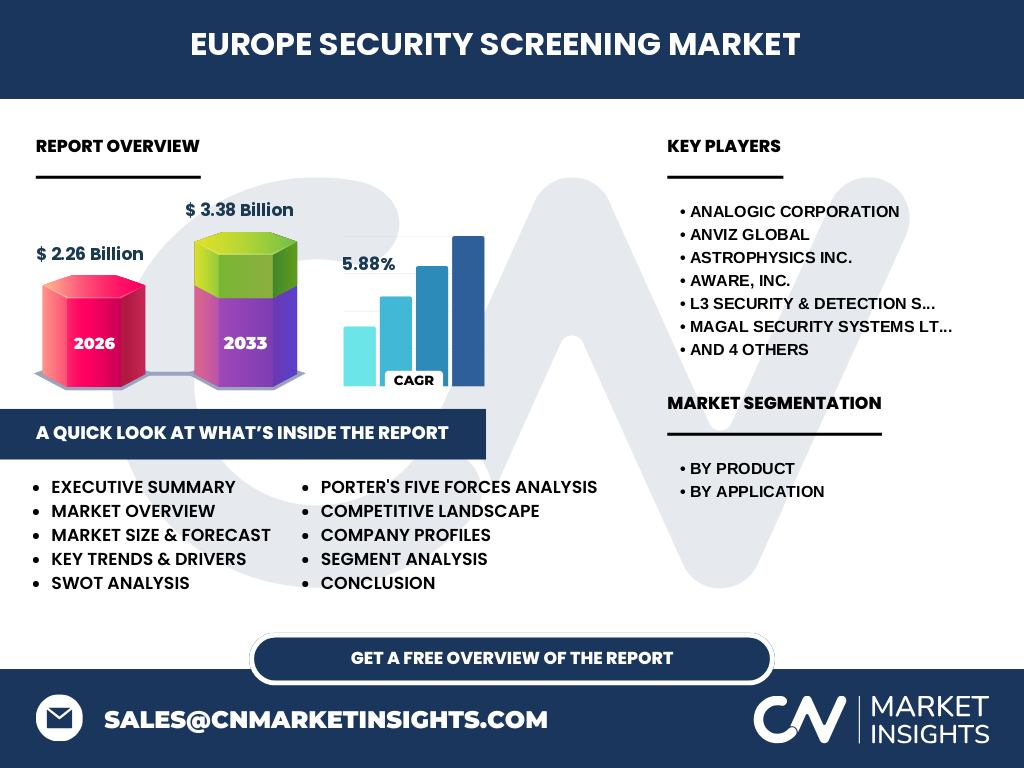

Leading players include Analogic Corporation, Anviz Global, Astrophysics Inc., Aware, Inc., L3 Security & Detection Systems, Magal Security Systems Ltd., Nuctech Company Limited, OSI Systems, Inc., Smiths Detection Inc., and Teledyne ICM. The market exhibits moderate consolidation, with a few large multinational firms holding significant design and IP advantages, while niche innovators focus on specialized biometric or detection technologies. Competitive dynamics are driven by product differentiation, service contracts, and strategic partnerships.

What does the Executive Summary reveal about the Europe Security Screening Market?

The Europe Security Screening Market was valued at €2.26 billion in 2026 and is projected to reach €3.38 billion by 2033, reflecting a CAGR of 5.88%. Growth is propelled by increasing security mandates across borders and transport hubs, rapid technology upgrades, and the post‑pandemic shift toward contactless screening. Key opportunities exist in expanding public‑place deployments and integrating AI‑driven analytics. Competitive pressure remains high, with incumbents leveraging scale and innovation to capture market share.

What are the forecast expectations for the Europe Security Screening Market for 2025‑2032?

Based on the provided CAGR of 5.88%, the market is expected to maintain steady expansion, moving from the 2026 base of €2.26 billion toward the 2033 estimate of €3.38 billion. This translates to incremental growth each year, supported by continued regulatory tightening, modernization of border checkpoints, and increasing investments by airport authorities to enhance passenger throughput while maintaining security standards.

How is the Europe Security Screening Market sized and shared by product and application segments?

By product, the market is divided among X‑ray scanners, biometric systems, explosive trace detectors, and electromagnetic metal detectors. By application, it serves border checkpoints, airports, government facilities, and public places. While exact monetary shares are not disclosed, each segment contributes to the overall market value, with X‑ray scanners and biometric systems typically commanding larger portions due to their critical role in high‑traffic environments such as airports and borders.

What is the geographic distribution of the Europe Security Screening Market?

The market encompasses the entire European region, with concentration in major aviation hubs (e.g., London, Frankfurt, Paris) and high‑traffic border zones (e.g., Schengen external borders). Although precise regional splits are not specified, the overall European market size of €2.26 billion in 2026 reflects the collective demand across Western, Central, and Eastern European nations.

What does the Regional Analysis of the Europe Security Screening Market reveal?

Western Europe leads in terms of technology adoption and investment, driven by mature airport infrastructures and stringent security regulations. Central and Eastern Europe are witnessing rapid upgrades to align with EU standards, creating growth opportunities for vendors. Nations with high passenger volumes and extensive land borders, such as Germany, France, and the United Kingdom, are primary contributors to market momentum.

Which companies lead the Europe Security Screening Market and what are their strategic approaches?

Key leaders include Analogic Corporation (advanced X‑ray solutions), Anviz Global (biometric identification), Nuctech Company Limited (large‑scale scanning systems), and Smiths Detection Inc. (explosive trace detection). Their strategies focus on R&D investment, expansion of service networks, partnership with airport operators, and acquisition of niche technology firms to broaden product portfolios and strengthen market positioning.

How does Porter’s Five Forces assess the Europe Security Screening Market?

• Threat of new entrants: Moderate – high capital and regulatory barriers limit newcomers. • Bargaining power of suppliers: Low to moderate – component suppliers are diversified. • Bargaining power of buyers: High – governments and large airport authorities negotiate extensive contracts. • Threat of substitutes: Low – few alternatives to reliable screening technologies. • Competitive rivalry: High – numerous established players compete on technology, price, and service.

What are the SWOT insights for the Europe Security Screening Market?

Strengths: Strong regulatory support and increasing security budgets. Weaknesses: High upfront costs and complex integration. Opportunities: Expansion into public venues and adoption of AI‑driven analytics. Threats: Data‑privacy concerns related to biometrics and potential supply‑chain disruptions for critical components.

What does the Europe Security Screening Market Value Chain look like?

The value chain begins with raw material procurement (electronics, imaging sensors), proceeds to R&D and product engineering, followed by manufacturing, system integration, and testing. Distribution is handled through direct sales, system integrators, and regional distributors. Post‑sale services—installation, maintenance, and software updates—complete the chain, creating recurring revenue streams for vendors.

What key investment insights are recommended for the Europe Security Screening Market?

Investors should focus on companies with robust AI and biometric capabilities, as these technologies drive next‑generation screening solutions. Funding firms that secure long‑term service contracts with major airports or border agencies can benefit from stable cash flows. Strategic M&A targeting niche sensor technologies can enhance product differentiation and market reach.

What are the main conclusions drawn from the Europe Security Screening Market analysis?

The market is on a clear growth path, supported by regulatory pressure, technological innovation, and post‑pandemic demand for contactless security. While capital intensity and privacy issues pose challenges, the projected CAGR of 5.88% indicates a healthy outlook. Companies that invest in integrated, AI‑enabled platforms and expand service networks are positioned to capture the expanding €3.38 billion market by 2033.

How was the research for this report conducted?

The study used a combination of primary interviews with industry experts, secondary data from company reports, government publications, and reputable market databases. Trend analysis, forecasting models, and competitive benchmarking were applied to derive the market size, growth rate, and segmentation insights.

What is the scope of this research and its limitations?

The scope covers the European region, focusing on security screening hardware and related services across four product categories and four application areas. Limitations include the reliance on publicly available financial data and the exclusion of confidential contract values, which may affect precise market‑share calculations.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Analogic Corporation (launch of a next‑generation dual‑energy X‑ray scanner), Anviz Global (new facial‑recognition biometric platform for airports), Nuctech Company Limited (strategic partnership with a leading European airport operator), and Smiths Detection Inc. (introduction of a portable explosive trace detector). Recent activities also feature OSI Systems, Inc. expanding its service footprint in Central Europe and Magal Security Systems Ltd. acquiring a small AI‑analytics startup to bolster its product suite.