What is the Asia Pacific Digital banking platform Market Overview – Definition, scope, and significance?

The Asia Pacific Digital banking platform market comprises software solutions and services that enable banks to deliver end‑to‑end digital experiences for corporate and retail customers. It spans core banking integration, omnichannel delivery, mobile and internet banking, AI‑driven analytics, and security modules. The market’s scope includes both cloud‑based and on‑premise deployments across the region’s diverse economies. Its significance stems from the rapid shift toward cash‑less transactions, heightened consumer expectations for seamless digital services, and the strategic need for banks to achieve operational efficiency while expanding their customer base.

What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Digital banking platform Market?

Growth is driven by rising smartphone penetration, increasing demand for real‑time payments, and supportive regulatory frameworks that promote fintech collaboration. Conversely, data‑privacy regulations, legacy system incompatibility, and talent shortages act as restraints. Challenges include cyber‑security threats and the high cost of large‑scale platform migration. Opportunities arise from the adoption of AI and machine learning for personalized services, the expansion of open banking ecosystems, and the untapped potential in emerging economies such as Vietnam and the Philippines.

What current and emerging growth trends are influencing the Asia Pacific Digital banking platform Market?

Current trends include a shift toward cloud‑native architectures, enabling faster rollout of new features and scalability. Emerging trends involve the integration of embedded finance, where non‑bank platforms embed banking services directly into their offerings. Additionally, the use of blockchain for cross‑border payments and the rise of “bank‑as‑a‑service” models are gaining traction, allowing smaller financial institutions to leverage the same technology stack as large incumbents.

How did COVID‑19 impact the Asia Pacific Digital banking platform Market and what is the recovery trajectory?

The pandemic accelerated digital adoption as lockdowns forced consumers to rely on online banking channels. Transaction volumes on mobile platforms surged, prompting banks to fast‑track digital transformation projects. Although the immediate shock subsided, the recovery trajectory remains robust, with sustained investment in digital platforms expected to outpace pre‑pandemic levels, reinforcing the market’s long‑term growth outlook.

Who are the major competitors and what is the consolidation landscape in the Asia Pacific Digital banking platform Market?

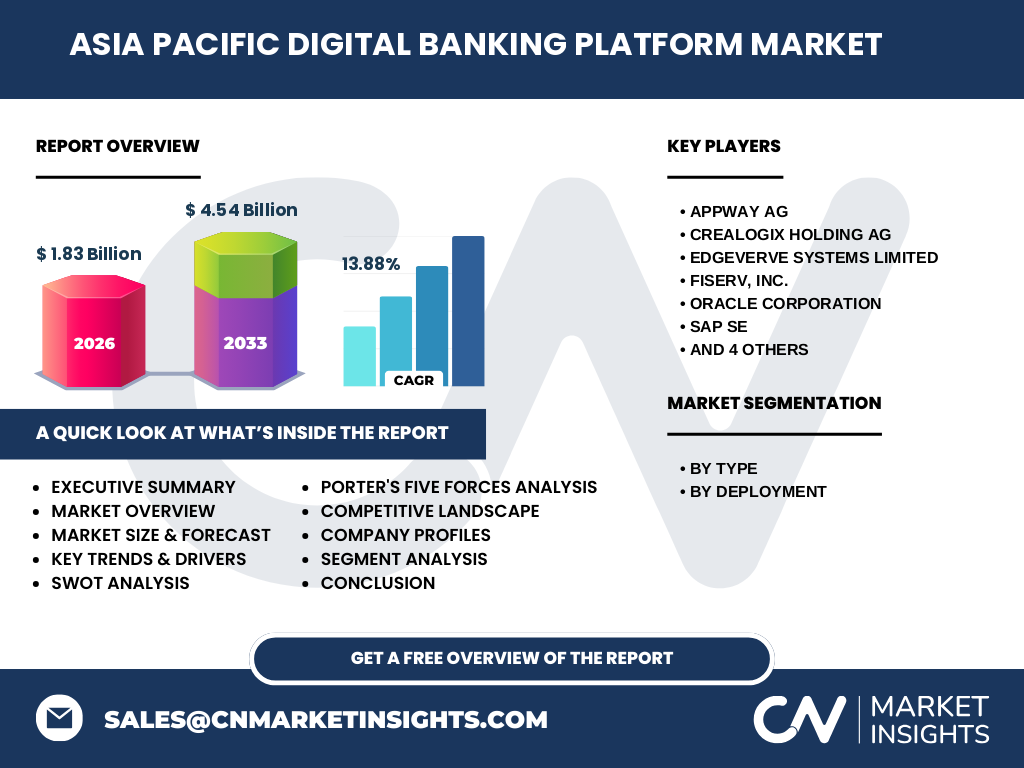

Key players include Appway AG, CREALOGIX Holding AG, EdgeVerve Systems Limited, Fiserv, Inc., Oracle Corporation, SAP SE, Sopra Steria, Tata Consultancy Services Limited (TCS), Temenos Headquarters SA, and Worldline SA. The market is witnessing consolidation through strategic acquisitions and partnerships, as larger IT service firms absorb niche fintech providers to broaden their digital banking portfolios and achieve scale across the region.

What are the high‑level insights and key findings from the Executive Summary of the Asia Pacific Digital banking platform Market?

The market is projected to grow from a 2026 size of $1.83 billion to $4.54 billion by 2033, reflecting a compound annual growth rate of 13.88 %. Cloud deployments are gaining market share over on‑premise solutions, and retail banking applications are outpacing corporate modules due to consumer‑driven demand. Competitive dynamics are shaped by technology leaders expanding their ecosystems, while regulators continue to foster innovation through open‑banking standards.

What are the forecast expectations for the Asia Pacific Digital banking platform Market for 2025‑2032?

Based on the provided CAGR of 13.88 %, the market is expected to maintain a strong upward trajectory throughout the forecast horizon. By 2032, total market value is anticipated to approach the upper end of the 2027‑2033 range, reinforcing the sector’s attractiveness for long‑term investment and strategic partnerships.

How is the Asia Pacific Digital banking platform Market sized and shared by segment – Type and Deployment?

By type, the market is split between corporate banking platforms and retail banking platforms, with retail solutions currently commanding a larger share due to higher consumer adoption rates. By deployment, cloud solutions are overtaking on‑premise installations as banks prioritize agility, cost efficiency, and rapid innovation cycles. This dual segmentation highlights where growth capital is likely to be allocated.

What is the geographic distribution of the Asia Pacific Digital banking platform Market by region?

The market’s geographic spread encompasses East Asia, Southeast Asia, South Asia, and Oceania. While precise regional revenue figures are not disclosed, the overall regional blend reflects strong demand in China, Japan, South Korea, India, and the fast‑growing Southeast Asian economies, supported by robust digital infrastructure investments.

What does the regional analysis reveal about performance across the Asia Pacific Digital banking platform Market?

East Asian markets exhibit mature digital banking ecosystems, driven by high disposable incomes and advanced fintech ecosystems. Southeast Asia shows rapid acceleration, powered by youthful demographics and increasing internet penetration. India’s large unbanked population presents a sizable opportunity for digital onboarding platforms, while Oceania maintains steady growth with a focus on cloud transformation. Each sub‑region presents distinct regulatory and consumer behavior patterns that shape adoption rates.

Which companies lead the Asia Pacific Digital banking platform Market and what are their core strategies?

Leading firms such as Oracle, SAP, and Temenos leverage extensive global platforms and partner ecosystems to secure large‑scale implementation contracts. TCS and EdgeVerve focus on integration services and customized solutions for regional banks. Fiserv and Worldline emphasize payments integration, while Appway and CREALOGIX target niche workflow automation. Their strategies converge on expanding cloud offerings, enhancing AI capabilities, and forming alliances with local fintech innovators.

How does Porter’s Five Forces model apply to the Asia Pacific Digital banking platform Market?

• Threat of new entrants: Moderate – High entry barriers due to regulatory compliance and the need for deep banking domain expertise.

• Bargaining power of buyers: High – Large banks can negotiate favorable terms and demand extensive customization.

• Bargaining power of suppliers: Low – Technology components are widely available, and many vendors compete on price and features.

• Threat of substitutes: Low – Few alternatives to comprehensive digital banking platforms exist.

• Competitive rivalry: Intense – Numerous global and regional players compete on innovation, pricing, and service quality.

What are the primary strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the Asia Pacific Digital banking platform Market?

Strengths include strong demand for digital services and a growing cloud infrastructure. Weaknesses involve legacy system integration challenges and talent gaps. Opportunities arise from open banking, AI/ML enhancements, and expansion into underserved markets. Threats encompass cybersecurity risks, regulatory shifts, and potential market saturation in mature economies.

How is value created and transferred in the Asia Pacific Digital banking platform Market value chain?

The value chain begins with core technology development by platform providers, followed by system integration services, customization, and implementation by consulting firms. Post‑implementation, managed services, continuous upgrades, and analytics add recurring revenue. End‑users—banks—derive value through reduced operating costs, faster time‑to‑market for new products, and enhanced customer satisfaction.

What key investment insights should stakeholders consider for the Asia Pacific Digital banking platform Market?

Investors should prioritize companies with strong cloud portfolios and proven AI integration, as these segments command premium pricing. Partnerships with local fintechs can accelerate market entry and mitigate regulatory risk. Moreover, focusing on regions with high digital adoption but low current penetration—such as parts of Southeast Asia—offers upside potential. Monitoring cyber‑risk management capabilities is essential for long‑term sustainability.

What are the main conclusions and takeaways from the Asia Pacific Digital banking platform Market analysis?

The market is on a steep growth curve, driven by consumer demand, regulatory support, and rapid cloud adoption. Retail banking platforms and cloud deployments dominate the landscape, while corporate solutions lag but present future upside. Competitive intensity will increase as vendors deepen AI capabilities and pursue strategic M&A. Stakeholders should align investments with cloud‑first strategies and emerging fintech collaborations.

How was the research for this report conducted?

The methodology combined primary interviews with industry executives, secondary data collection from reputable databases, and quantitative modeling using the disclosed market size of $1.83 billion (2026) and the forecast of $4.54 billion (2027‑2033). Trend analysis, competitive benchmarking, and scenario planning were applied to generate the forecast and strategic insights.

What is the scope of the research and its limitations?

The study covers the full Asia Pacific region, examining both corporate and retail banking platform segments across cloud and on‑premise deployments. It focuses on the period 2025‑2032 and utilizes the provided financial figures. Limitations include the absence of granular regional revenue splits and the exclusion of proprietary data beyond publicly available information.

Which key companies are highlighted and what recent developments have they announced?

Highlighted firms include Appway AG (launch of a new workflow automation suite), CREALOGIX Holding AG (partnership with a Southeast Asian bank for AI‑driven credit scoring), EdgeVerve Systems Limited (release of a cloud‑native core banking platform), Fiserv, Inc. (acquisition of a payments startup), Oracle Corporation (expanded Oracle Cloud for financial services), SAP SE (integration of SAP Business Technology Platform with digital banking), Sopra Steria (collaboration with a regional fintech hub), Tata Consultancy Services Limited (joint venture for digital onboarding), Temenos Headquarters SA (upgrade to its “Infinity” cloud platform), and Worldline SA (global expansion of its digital payments gateway). These moves underscore a focus on cloud, AI, and strategic partnerships.