1. North America Digital banking platform Market Overview - Definition, scope, and significance?

The North America Digital banking platform market comprises software solutions that enable banks and financial institutions to deliver end‑to‑end banking services through web and mobile channels. These platforms integrate core banking, payments, lending, compliance, analytics, and customer experience modules into a unified digital interface. The scope includes solutions for both corporate and retail banking customers, deployed either on cloud infrastructure or on‑premise data centers. Significance stems from the region’s high broadband penetration, mature fintech ecosystem, and strong consumer demand for seamless, real‑time financial services, which together drive rapid adoption and transformation of traditional banking models.

2. North America Digital banking platform Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include the accelerating shift toward omnichannel banking, regulatory encouragement of digital inclusion, and the need for cost‑efficient operations through automation. Cloud adoption further fuels scalability and speed‑to‑market. Restraints arise from legacy system integration complexities and heightened cybersecurity compliance costs. Challenges involve talent shortages in AI/ML development and the competitive pressure from agile fintech entrants. Opportunities lie in leveraging AI‑driven personalization, expanding open‑banking APIs, and targeting underserved Small‑Medium Enterprises (SMEs) with digital corporate banking solutions, all of which can unlock new revenue streams.

3. North America Digital banking platform Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a pronounced move to cloud‑native architectures, fostering flexible scaling and rapid feature rollout. Embedded finance is emerging, where non‑bank entities integrate banking services directly into their platforms. AI and machine‑learning models are increasingly embedded to enable predictive credit scoring, fraud detection, and hyper‑personalized offers. Additionally, the rise of “bank‑as‑a‑service” models allows third‑party developers to build niche solutions atop core platforms, accelerating innovation cycles across the ecosystem.

4. COVID-19 Impact on the North America Digital banking platform Market - Pandemic effects and recovery trajectory?

The pandemic acted as a catalyst, pushing customers to adopt digital channels at an unprecedented rate due to branch closures and social distancing measures. Banks accelerated their digital roadmap, leading to a surge in platform implementations and upgrades. Although the immediate shock subsided, the recovery trajectory remains positive, with sustained higher digital transaction volumes and a continued focus on resiliency, indicating lasting structural change rather than a temporary spike.

5. North America Digital banking platform Market Competitive Landscape - Major competitors and market consolidation?

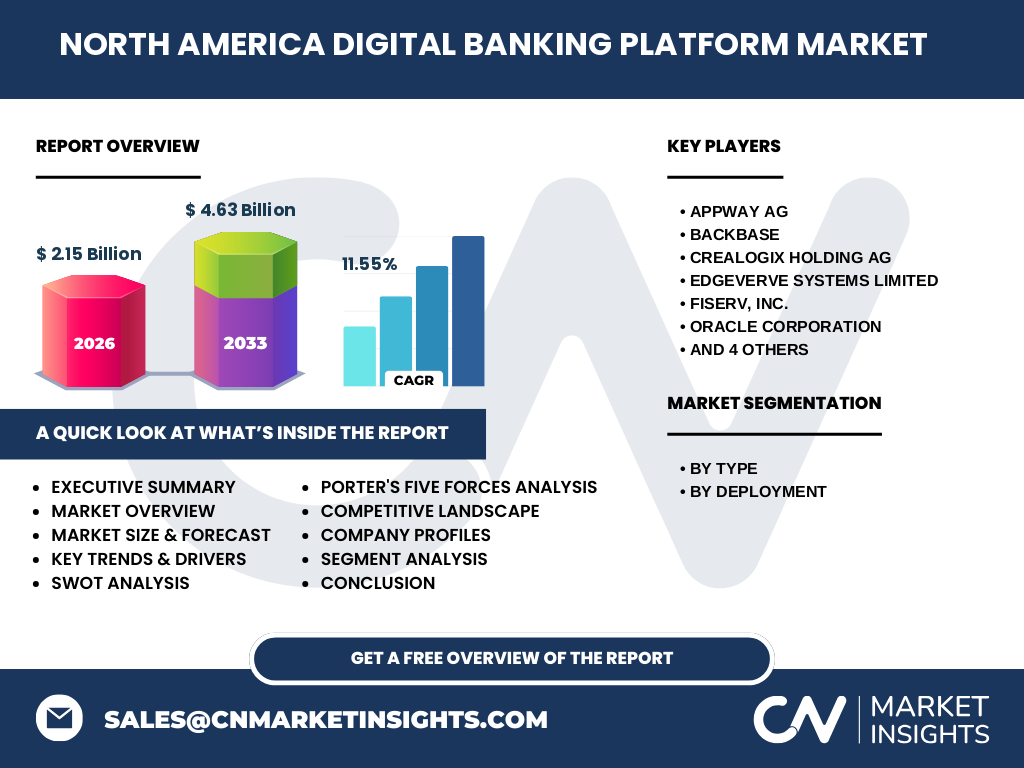

The competitive landscape is populated by global technology firms and specialized fintech vendors. Leading players include Appway AG, Backbase, CREALOGIX Holding AG, EdgeVerve Systems Limited, Fiserv, Inc., Oracle Corporation, SAP SE, Sopra Steria, Tata Consultancy Services Limited (TCS), and nCino, inc. These companies compete on breadth of functionality, integration depth, and cloud capabilities. Recent consolidation activity features strategic acquisitions aimed at enhancing AI and open‑banking capabilities, signaling a trend toward fewer, more comprehensive platform providers.

6. Executive Summary - High-level overview and key findings about North America Digital banking platform Market?

The North America Digital banking platform market is valued at $2.15 billion in 2026 and is projected to reach $4.63 billion by 2033, delivering a robust compound annual growth rate of 11.55%. Growth is propelled by cloud migration, AI‑enabled services, and escalating consumer expectations for digital experiences. While legacy integration and cybersecurity remain constraints, emerging opportunities in open banking and embedded finance provide clear pathways for further expansion. The market is dominated by a mix of established enterprise vendors and agile fintech specialists, with consolidation sharpening competitive dynamics.

7. North America Digital banking platform Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 11.55%, the market is expected to sustain a strong upward trajectory throughout the 2025‑2032 horizon. By 2028, the market size is anticipated to surpass the $3 billion threshold, and by the end of the forecast window (2032) it will approach the $4 billion mark, reflecting continued investment in digital transformation initiatives across both corporate and retail banking segments.

8. North America Digital banking platform Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type reveals two primary categories: corporate banking and retail banking platforms. Both segments are experiencing parallel growth, with corporate solutions gaining traction due to increasing demand for digitized treasury and cash‑management services. Deployment segmentation indicates cloud solutions are rapidly outpacing on‑premise installations, driven by the need for agility, lower total cost of ownership, and accelerated regulatory compliance. The market’s overall composition reflects a balanced mix, yet the momentum is distinctly tilted toward cloud‑based offerings.

9. Global North America Digital banking platform Market Size and Share by Region - Geographic distribution?

Within the global context, North America represents the largest regional share of the digital banking platform market, underpinned by the region’s mature financial infrastructure and early adoption of innovative technologies. The $2.15 billion valuation for 2026 underscores its leadership position, with the United States contributing the majority share, followed by Canada’s growing fintech sector.

10. Regional Analysis of the North America Digital banking platform Market - Detailed regional market performance?

The United States drives the core growth, propelled by extensive banking networks, high consumer digital spend, and significant cloud‑service provider presence. Canada exhibits a steady rise, boosted by progressive regulatory frameworks encouraging open banking and a vibrant startup ecosystem. Both countries show strong demand for AI‑enhanced retail platforms, while corporate banking platforms are gaining relevance in cross‑border trade financing and supply‑chain finance digitization.

11. Leading Company Profiles in the North America Digital banking platform Market - Industry players and strategies?

Appway AG focuses on low‑code workflow automation to accelerate onboarding. Backbase excels in customer experience design, offering modular front‑end layers. CREALOGIX delivers modular core banking suites with strong analytics. EdgeVerve (a Infosys unit) leverages its AI platform, Nia, for predictive banking services. Fiserv, Inc. integrates payment processing with digital banking. Oracle and SAP provide enterprise‑grade cloud platforms with deep data integration. Sopra Steria emphasizes consulting‑driven implementations, while TCS offers end‑to‑end digital transformation services. nCino, inc. specializes in cloud‑native loan origination for corporate customers.

12. Porter's Five Forces Analysis of the North America Digital banking platform Market - Competitive forces assessment?

*Threat of New Entrants*: Moderate – high capital and compliance barriers deter many, yet fintech startups with niche AI capabilities can enter through API ecosystems.

*Bargaining Power of Buyers*: Strong – large banks demand customized solutions and can negotiate pricing, pressing vendors to innovate.

*Bargaining Power of Suppliers*: Low – cloud infrastructure providers dominate, but multiple options (AWS, Azure, Google Cloud) reduce dependence.

*Threat of Substitutes*: Emerging – open‑source platforms and blockchain‑based banking services present alternative routes, though adoption remains nascent.

*Industry Rivalry*: Intense – multiple global vendors compete on functionality, integration speed, and cost, leading to frequent partnerships and acquisitions.

13. SWOT Analysis of the North America Digital banking platform Market - Strengths, weaknesses, opportunities, threats?

Strengths: High market capitalization, strong technology ecosystem, supportive regulatory environment.

Weaknesses: Legacy system integration challenges, cybersecurity cost pressures.

Opportunities: Expansion of open banking, AI‑driven personalization, embedded finance for non‑bank players.

Threats: Rapid fintech disruption, evolving cyber threats, potential regulatory tightening on data privacy.

14. North America Digital banking platform Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with core technology providers (cloud, AI, security) supplying infrastructure. Next, platform developers (vendors listed earlier) build modular banking suites. Integration services and system integrators add customization and migration expertise. Banks then deploy the solution, followed by end‑user interaction through mobile/web channels. Ongoing support, analytics, and continuous improvement loops close the chain, creating recurring revenue streams for vendors.

15. Key Investment Insights in the North America Digital banking platform Market - Strategic investment recommendations?

Investors should target companies with strong cloud‑native roadmaps and proven AI integration, as these capabilities align with the market’s growth trajectory. Partnerships with major cloud providers enhance scalability and lower entry barriers. Acquisitions of niche fintech firms that bring open‑banking APIs or specialized compliance tools can accelerate market share gains. Finally, focusing on firms with diversified client portfolios across corporate and retail segments mitigates concentration risk.

16. North America Digital banking platform Market Conclusion - Summary and key takeaways?

The market is on a clear expansion path, underpinned by a 11.55% CAGR and a projected near‑doubling of size by 2033. Cloud migration, AI integration, and regulatory support are the primary catalysts, while legacy integration and cybersecurity remain the chief hurdles. Competitive pressure is intensifying, driving consolidation and innovation. Stakeholders who invest in scalable, AI‑enabled, open‑banking capable platforms are positioned to capture the most value.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with senior banking IT executives, technology vendors, and industry analysts, alongside secondary research from reputable financial reports, regulatory filings, and market databases. Quantitative data were validated through triangulation across multiple sources, and qualitative insights were synthesized to produce the forward‑looking forecasts.

18. Research Scope - Coverage and limitations?

The scope covers North American digital banking platforms across corporate and retail segments, examining both cloud and on‑premise deployments. It includes market sizing, competitive analysis, and forecasts through 2033. Limitations stem from the rapidly evolving regulatory landscape, which may introduce new compliance requirements that could affect future adoption rates.

19. Key Companies and Recent Developments in the North America Digital banking platform Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Appway AG announced a low‑code onboarding suite targeting neo‑banks. Backbase launched a new AI‑driven journey orchestration engine. CREALOGIX introduced enhanced real‑time analytics dashboards. EdgeVerve integrated its Nia AI platform with banking workflow automation. Fiserv unveiled a unified payments‑plus‑digital banking solution. Oracle released a next‑gen cloud banking suite with embedded compliance controls. SAP expanded its banking portfolio with a digital ledger component. Sopra Steria secured a multi‑year contract with a major US bank for end‑to‑end platform migration. TCS announced a strategic partnership with a leading cloud provider to co‑develop industry‑specific services. nCino rolled out a cloud‑native loan origination module focusing on mid‑market corporates.