What is the Predictive Vehicle Technology Market overview, including its definition, scope, and significance?

The Predictive Vehicle Technology (PVT) market encompasses hardware and software solutions that enable vehicles to anticipate failures, optimize performance, and enhance safety through real‑time data analysis. Scope covers advanced driver‑assistance systems (ADAS), telematics, on‑board diagnostics (OBD), and applications such as proactive alerts, safety and security functions for both commercial vehicles and passenger cars. The significance lies in its ability to reduce downtime, lower maintenance costs, improve driver confidence, and support the broader shift toward connected and autonomous mobility.

What are the main drivers, restraints, challenges, and opportunities shaping the Predictive Vehicle Technology market?

Key drivers include rising vehicle connectivity, stringent safety regulations, and growing demand for cost‑effective fleet management. Restraints stem from high integration costs and data privacy concerns. Challenges involve interoperability among diverse hardware platforms and the need for robust cybersecurity. Opportunities arise from the expansion of data‑driven services, AI‑enhanced analytics, and emerging markets seeking modernized transport infrastructures, which can accelerate adoption of PVT solutions.

Which growth trends are currently influencing the Predictive Vehicle Technology market?

Current trends feature the convergence of ADAS and telematics into unified platforms, increased use of edge computing for instantaneous predictive analytics, and a shift toward subscription‑based service models. Emerging trends include the integration of 5G connectivity to improve data latency, and the adoption of machine‑learning algorithms that refine failure predictions over time, thereby enhancing system reliability and user experience.

How did COVID‑19 affect the Predictive Vehicle Technology market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains and slowed new vehicle production, temporarily reducing demand for PVT hardware. However, heightened awareness of health and safety accelerated interest in remote diagnostics and contactless maintenance. Post‑2020, the market rebounded strongly, supported by pent‑up demand and increased fleet digitization, setting a clear path toward sustained growth.

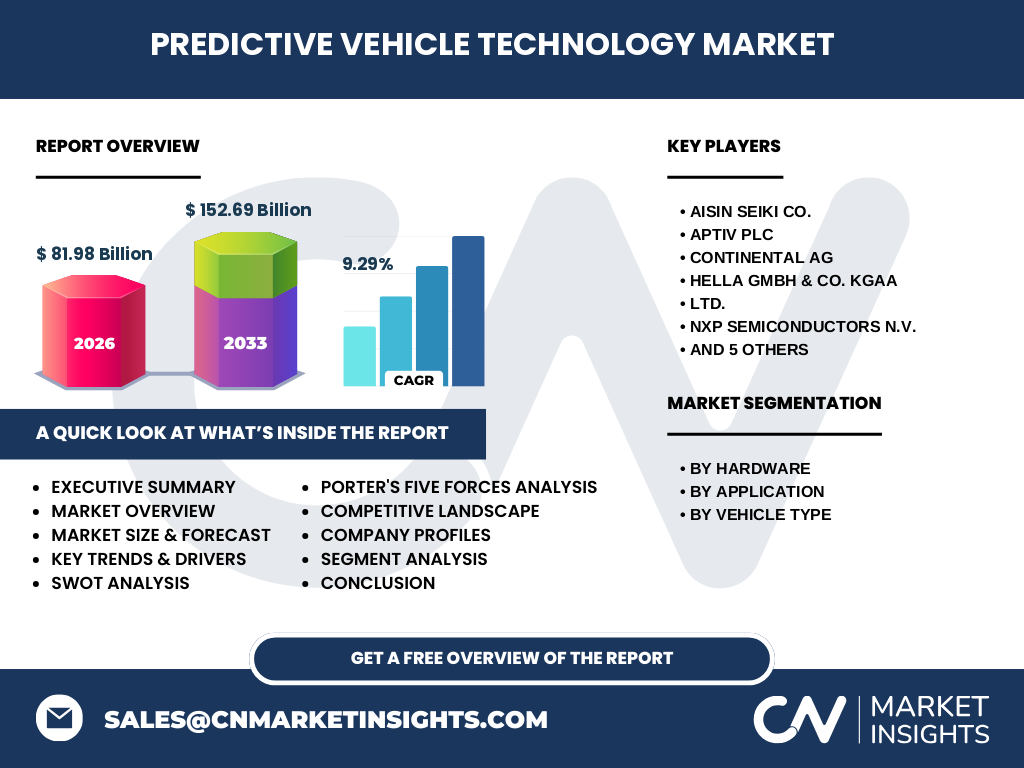

Who are the major competitors in the Predictive Vehicle Technology market, and what does the competitive landscape look like?

The market is populated by leading automotive suppliers and semiconductor firms such as AISIN SEIKI Co., Aptiv PLC, Continental AG, HELLA GmbH & Co. KGaA, NXP Semiconductors N.V., Robert Bosch GmbH, Traffilog LTD, Valeo, Visteon Corporation, and ZF Friedrichshafen AG. Competitive dynamics are characterized by strategic alliances, joint R&D initiatives, and occasional M&A activity aimed at expanding portfolio breadth and geographic reach.

What are the key findings presented in the executive summary of the Predictive Vehicle Technology market report?

The executive summary highlights a market size of $81.98 billion in 2026, with a forecast reaching $152.69 billion by 2033, representing a CAGR of 9.29 %. Growth is driven by expanding ADAS adoption, telematics proliferation, and increasing safety‑critical applications. Regional analysis shows strong momentum in North America and Europe, while emerging economies are emerging as new growth engines. The report underscores the strategic importance of data analytics and partnerships for sustained market leadership.

What are the forecast projections for the Predictive Vehicle Technology market from 2025 to 2032?

Based on a 9.29 % compound annual growth rate, the market is expected to expand from its 2026 baseline of $81.98 billion to approximately $152.69 billion by 2033. This trajectory indicates steady year‑over‑year growth, driven by continued investment in connected vehicle ecosystems and regulatory incentives for safety technologies across both commercial and passenger vehicle segments.

How is the Predictive Vehicle Technology market sized and shared across its primary segments?

Segmentation by hardware reveals three core categories: ADAS, telematics, and OBD. Application‑wise, the market splits between proactive alerts and safety & security functions. By vehicle type, commercial vehicles and passenger cars each command a distinct share, reflecting differing priorities—fleet efficiency for commercial fleets and advanced safety for passenger cars. While exact numeric shares are not disclosed, the structure indicates balanced opportunities across all segments.

What is the global geographic distribution of the Predictive Vehicle Technology market size and share?

The market exhibits a worldwide footprint, with major contributions from North America, Europe, and Asia‑Pacific. These regions host the majority of automotive OEMs and technology suppliers, driving demand for predictive systems. Emerging markets in Latin America and the Middle East are also participating, albeit at a smaller scale, indicating potential for future expansion as connectivity infrastructure improves.

What does the regional analysis reveal about performance of the Predictive Vehicle Technology market?

North America leads in early adoption of ADAS and telematics due to stringent safety regulations and robust funding for autonomous research. Europe follows closely, propelled by EU directives on vehicle emissions and safety standards. Asia‑Pacific shows rapid growth, fueled by large vehicle production volumes and government incentives for smart transportation. Each region demonstrates unique drivers, yet all share a common trend toward increased vehicle intelligence.

Which companies are leading in the Predictive Vehicle Technology market, and what strategies are they employing?

Industry leaders such as Continental AG and Robert Bosch GmbH focus on expanding their sensor portfolios and integrating AI capabilities. Valeo and ZF Friedrichshafen AG pursue strategic partnerships with telecom providers to enhance connectivity. NXP Semiconductors leverages its semiconductor expertise to embed predictive functions directly into vehicle ECUs. Companies are also investing in software platforms that enable over‑the‑air updates and subscription services.

How does Porter’s Five Forces analysis apply to the Predictive Vehicle Technology market?

Supplier power is moderate, given the specialized nature of sensors and semiconductors. Buyer power is rising as OEMs demand integrated solutions and cost efficiencies. Threat of new entrants is low due to high R&D barriers and regulatory compliance costs. Substitutes are limited, as alternative safety technologies lack the predictive capability. Competitive rivalry remains intense, driven by rapid innovation and the pursuit of ecosystem synergies.

What SWOT insights can be drawn for the Predictive Vehicle Technology market?

Strengths include strong technological differentiation and alignment with safety regulations. Weaknesses involve high implementation costs and data security concerns. Opportunities stem from expanding data‑as‑a‑service models and growing demand in emerging economies. Threats encompass cybersecurity risks, potential regulatory shifts, and market saturation in mature regions.

What does the value chain of the Predictive Vehicle Technology market look like?

The value chain starts with component suppliers (sensors, chips), moves through system integrators that assemble hardware and embed firmware, followed by software developers delivering analytics platforms. OEMs incorporate the assembled systems into vehicles, after which service providers manage data collection, cloud processing, and predictive insights delivered to fleet operators or end‑users. After‑sales support and OTA updates complete the loop.

What key investment insights are recommended for stakeholders in the Predictive Vehicle Technology market?

Investors should prioritize companies with strong AI and data‑analytics capabilities, as these are central to value creation. Funding ventures that enable secure over‑the‑air updates and modular hardware designs can capture growth. Strategic investments in partnerships that combine telecom bandwidth with vehicle data streams are also likely to yield high returns, especially in regions where connectivity is expanding.

What are the concluding remarks and takeaways from the Predictive Vehicle Technology market analysis?

The Predictive Vehicle Technology market is on a robust growth path, driven by safety imperatives, connectivity trends, and the economic benefits of proactive maintenance. With a projected 9.29 % CAGR through 2033, the sector offers substantial opportunities for technology leaders, OEMs, and investors willing to navigate data security challenges and invest in AI‑enabled platforms.

How was the research methodology designed for this Predictive Vehicle Technology market study?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from reputable automotive publications, and quantitative modeling to forecast market size. Trend analysis, competitive benchmarking, and scenario planning were applied to ensure accuracy and relevance of the projections.

What is the scope of this research, including coverage and limitations?

The scope covers global hardware segments (ADAS, telematics, OBD), applications (proactive alerts, safety & security), and vehicle types (commercial, passenger). Geographic coverage includes all major automotive regions. Limitations stem from the reliance on publicly available data and the exclusion of proprietary financial details beyond the provided market size and CAGR.

Which key companies and recent developments are highlighted in the Predictive Vehicle Technology market?

Notable players such as AISIN SEIKI Co., Aptiv PLC, Continental AG, HELLA GmbH & Co. KGaA, NXP Semiconductors, Robert Bosch GmbH, Traffilog LTD, Valeo, Visteon Corporation, and ZF Friedrichshafen AG have announced product launches that integrate AI‑driven diagnostics, forged partnerships with telecom operators for 5G‑enabled telematics, and secured strategic investments to expand their predictive analytics platforms. These activities underscore the market’s rapid evolution and collaborative nature.