Hereditary Cancer Testing Market Overview - Definition, scope, and significance?

The hereditary cancer testing market encompasses diagnostic solutions that identify germ‑line genetic mutations associated with increased cancer risk. It includes technologies such as sequencing, PCR, and microarray applied across hospitals, clinics, and diagnostic centers. By enabling early detection, personalized treatment planning, and family‑wide risk assessment, the market plays a critical role in preventive oncology, improves patient outcomes, and reduces long‑term healthcare costs.

Hereditary Cancer Testing Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising awareness of genetic risk, expanding insurance coverage, and advances in next‑generation sequencing that lower test costs. Restraints stem from high upfront equipment investment, complex regulatory pathways, and data privacy concerns. Challenges involve integrating genetic counseling services and addressing disparities in test access across regions. Opportunities arise from the adoption of liquid‑biopsy platforms, development of multi‑cancer panels, and partnerships between diagnostics firms and healthcare providers.

Hereditary Cancer Testing Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from single‑gene assays to comprehensive panel testing, driven by decreasing sequencing costs. Emerging trends include the incorporation of AI‑based variant interpretation, growth of direct‑to‑consumer genetic testing under medical supervision, and the use of cloud‑based data sharing to accelerate research. Tele‑genetics services are expanding access, particularly in underserved areas, while real‑world evidence studies are validating clinical utility.

COVID-19 Impact on the Hereditary Cancer Testing Market - Pandemic effects and recovery trajectory?

The pandemic initially disrupted sample collection and deferred elective screening, leading to a short‑term dip in test volumes. However, heightened telehealth adoption and increased focus on preventive health accelerated demand for remote genetic counseling and at‑home collection kits. Recovery has been robust, with test volumes rebounding faster than pre‑pandemic levels, positioning the market for a strong growth trajectory.

Hereditary Cancer Testing Market Competitive Landscape - Major competitors and market consolidation?

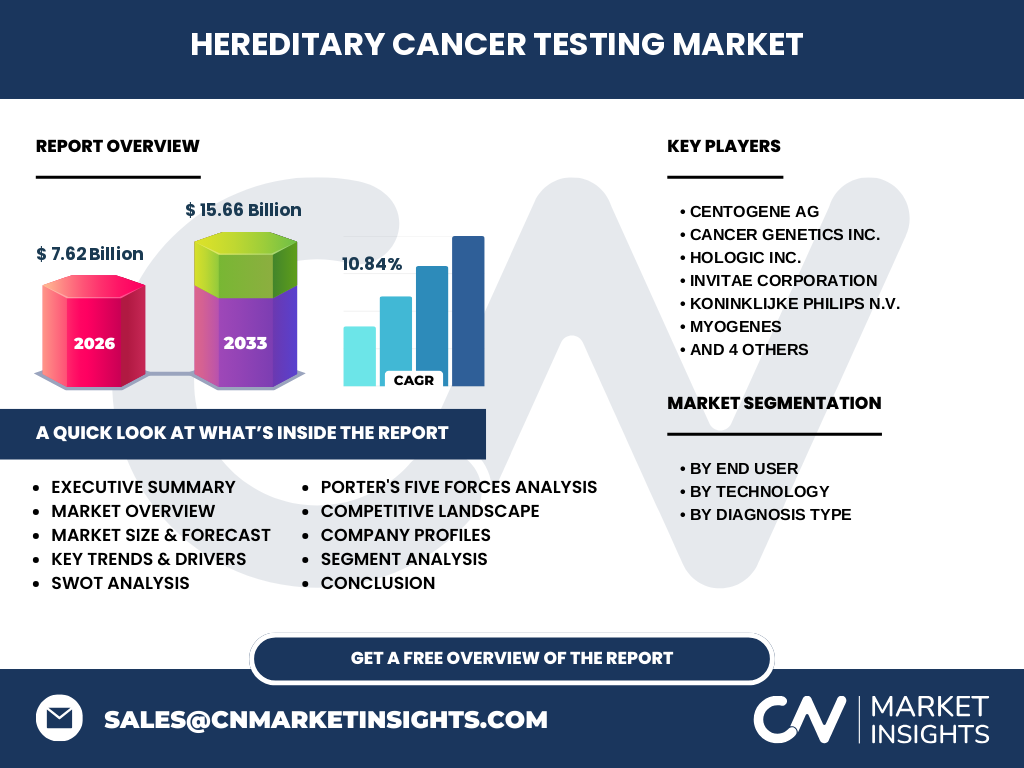

The competitive landscape features both established genetics specialists and diversified diagnostics firms. Major players include CENTOGENE AG, Cancer Genetics Inc., Hologic Inc., Invitae Corporation, Koninklijke Philips N.V., Myogenes, Myriad Genetics, Inc., Pathway Genomics Corporation, Quest Diagnostics Incorporated, and Strand Life Sciences Pvt. Ltd. Recent years have seen strategic mergers, joint ventures, and acquisitions to expand technology portfolios and geographic reach, intensifying competition.

Executive Summary - High-level overview and key findings about Hereditary Cancer Testing Market?

The hereditary cancer testing market is valued at USD 7.62 billion in 2026 and is projected to reach USD 15.66 billion by 2033, reflecting a robust CAGR of 10.84 %. Growth is propelled by expanding clinical adoption, technology innovation, and supportive reimbursement policies. The market is segmented by end user, technology, and diagnosis type, with sequencing leading the technology share. Regional expansion, especially in emerging economies, offers significant upside.

Hereditary Cancer Testing Market Forecast - Projections for 2025-2032 period?

Based on the provided CAGR of 10.84 %, the market is expected to sustain double‑digit expansion through 2032. This growth will be underpinned by increasing demand for multi‑gene panels, wider insurance reimbursement, and the rollout of cost‑effective sequencing platforms. While exact yearly figures are not disclosed, the forecast indicates a near‑doubling of market size by the early 2030s, presenting ample opportunity for entrants and incumbents alike.

Hereditary Cancer Testing Market Size and Share by Segmentation - Breakdown by segment?

Segmentation analysis reveals three primary dimensions. By end user, hospitals dominate due to integrated oncology services, followed by clinics and diagnostic centers. By technology, sequencing holds the largest share, benefitting from high throughput and decreasing costs, while PCR and microarray serve niche applications. By diagnosis type, biopsy‑based testing remains prevalent, with imaging used as a complementary tool for tumor localization and monitoring.

Global Hereditary Cancer Testing Market Size and Share by Region - Geographic distribution?

The market exhibits a broad geographic footprint, with North America leading due to advanced healthcare infrastructure and high reimbursement rates. Europe follows, driven by strong research institutions and regulatory support. Asia‑Pacific is emerging rapidly, fueled by rising cancer incidence, increasing awareness, and government initiatives supporting genetic testing. While exact regional revenue figures are not disclosed, the distribution aligns with healthcare spending patterns across these territories.

Regional Analysis of the Hereditary Cancer Testing Market - Detailed regional market performance?

In North America, the market benefits from early adoption of precision medicine and a dense network of specialized laboratories. Europe’s growth is supported by collaborative research programs and harmonized regulatory frameworks. Asia‑Pacific’s upside stems from large population bases, expanding private healthcare sectors, and governmental push for genomic initiatives. Latin America and the Middle East show modest but steady growth, primarily in urban tertiary care centers.

Leading Company Profiles in the Hereditary Cancer Testing Market - Industry players and strategies?

Key players such as Invitae Corporation focus on broad test menus and direct‑to‑physician distribution. Myriad Genetics leverages its heritage in BRCA testing while expanding into multi‑cancer panels. Hologic integrates hereditary testing into its broader diagnostic platform. CENTOGENE AG emphasizes rare disease expertise and partnerships with academic centers. Quest Diagnostics utilizes its extensive lab network to scale test volumes, while Philips combines imaging and genetic data for integrated diagnostics.

Porter's Five Forces Analysis of the Hereditary Cancer Testing Market - Competitive forces assessment?

• Threat of new entrants: Moderate – high capital requirements and regulatory barriers deter newcomers, yet innovative startups with novel sequencing methods pose a risk. • Bargaining power of suppliers: Low to moderate – reagents and instrument suppliers are numerous, but specialized consumables can command premium pricing. • Bargaining power of buyers: Growing – hospitals and insurers demand cost‑effective panels and outcome data. • Threat of substitutes: Low – alternative screening methods lack the genetic specificity of hereditary testing. • Industry rivalry: High – intense competition among established players drives continuous innovation and pricing pressure.

SWOT Analysis of the Hereditary Cancer Testing Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong clinical relevance, declining technology costs, and expanding reimbursement. Weaknesses: Complex test interpretation, need for genetic counseling, and high initial equipment outlay. Opportunities: Expansion into emerging markets, development of liquid‑biopsy‑compatible panels, and AI‑driven variant analysis. Threats: Data privacy regulations, potential reimbursement roll‑backs, and competitive pressure from broader genomic testing services.

Hereditary Cancer Testing Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with research institutions generating gene‑target insights, followed by reagent and instrument manufacturers supplying sequencing, PCR, and microarray kits. Laboratories (hospitals, clinics, diagnostic centers) perform sample processing and analysis. Results are interpreted by genetic counselors and reported to physicians. Post‑test, data is integrated into electronic health records and may be shared with research databases, completing the loop and creating feedback for next‑generation test development.

Key Investment Insights in the Hereditary Cancer Testing Market - Strategic investment recommendations?

Investors should target companies with diversified test portfolios and strong partnerships with healthcare systems. Funding in AI‑enabled interpretation platforms offers high upside due to scalability. Expansion into Asia‑Pacific through joint ventures can capture emerging demand. Acquisitions of niche PCR or microarray technology firms can broaden product offerings and create cross‑selling opportunities within existing customer bases.

Hereditary Cancer Testing Market Conclusion - Summary and key takeaways?

The hereditary cancer testing market is on a rapid growth path, projected to more than double its 2026 size by 2033. Sequencing dominates technology adoption, while hospitals remain the primary end users. Robust drivers such as preventive health focus, technology cost reductions, and supportive policies outweigh existing restraints, creating a compelling landscape for investors, clinicians, and technology innovators.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from reputable databases, and quantitative modeling to project market size. Trend analysis, competitive profiling, and scenario planning were applied to ensure accuracy and relevance of the forecast.

Research Scope - Coverage and limitations?

The scope covers global hereditary cancer testing across all major regions, segmented by end user, technology, and diagnosis type. While the analysis leverages the most recent available data, proprietary financial details of individual companies are not disclosed, and short‑term market fluctuations beyond the forecast horizon are not captured.

Key Companies and Recent Developments in the Hereditary Cancer Testing Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Invitae’s launch of an expanded multi‑cancer panel, Myriad Genetics’ acquisition of a bioinformatics start‑up to enhance variant interpretation, and Hologic’s partnership with leading hospitals to integrate hereditary testing into oncology pathways. CENTOGENE AG announced a collaboration with European research networks to standardize rare‑cancer genetic testing, while Quest Diagnostics rolled out a nationwide at‑home sample collection service, broadening access to hereditary testing.