What is the North America RTD Alcoholic Beverages Market Overview – Definition, scope, and significance?

The North America Ready‑to‑Drink (RTD) alcoholic beverages market comprises pre‑mixed cocktails, malt‑based coolers, hard seltzers, and flavored spirits that are sold in a finished, portable format. The scope covers all beverage categories that are blended, carbonated, or infused with alcohol and packaged for immediate consumption, including whiskey, rum, vodka, and gin variants. This segment is significant because it meets the growing consumer demand for convenient, low‑effort drinking experiences, appeals to younger demographics seeking novelty, and contributes a multi‑billion‑dollar revenue stream to the region’s overall alcoholic drinks industry.

What are the North America RTD Alcoholic Beverages Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising urbanisation, a shift toward on‑the‑go lifestyles, and the popularity of low‑calorie, flavored alcoholic options such as hard seltzers. Premiumisation and brand extensions from established spirits houses also stimulate growth. Restraints stem from stringent alcohol regulations, higher tax rates on ready‑made drinks, and growing health‑conscious sentiment that can limit consumption. Challenges involve intense competition for shelf space and the need to constantly innovate flavour profiles. Opportunities arise from expanding distribution through e‑commerce, targeting “no‑alcohol‑required” social occasions, and leveraging sustainable packaging to attract environmentally aware consumers.

What are the North America RTD Alcoholic Beverages Market Growth Trends?

Current trends feature the rapid rise of hard seltzer categories, driven by younger adults seeking lighter alcohol alternatives. Flavor experimentation—tropical, botanical, and exotic fruit blends—continues to differentiate products. Brands are increasingly launching limited‑edition seasonal flavours to create urgency and social media buzz. Additionally, there is a noticeable shift toward premium RTD cocktails that use high‑quality base spirits, aligning with the broader premiumisation movement in alcohol.

How has COVID‑19 impacted the North America RTD Alcoholic Beverages Market?

The pandemic initially disrupted on‑premise sales, accelerating a migration to off‑premise channels such as supermarkets, hypermarkets, and specialty stores. Home consumption of RTD drinks surged, reinforcing the segment’s convenience advantage. As restrictions eased, the market experienced a swift rebound, with the growth trajectory remaining robust. Recovery is supported by lingering consumer habits formed during lockdown, especially the preference for ready‑made, single‑serve alcoholic beverages.

What does the North America RTD Alcoholic Beverages Market Competitive Landscape look like?

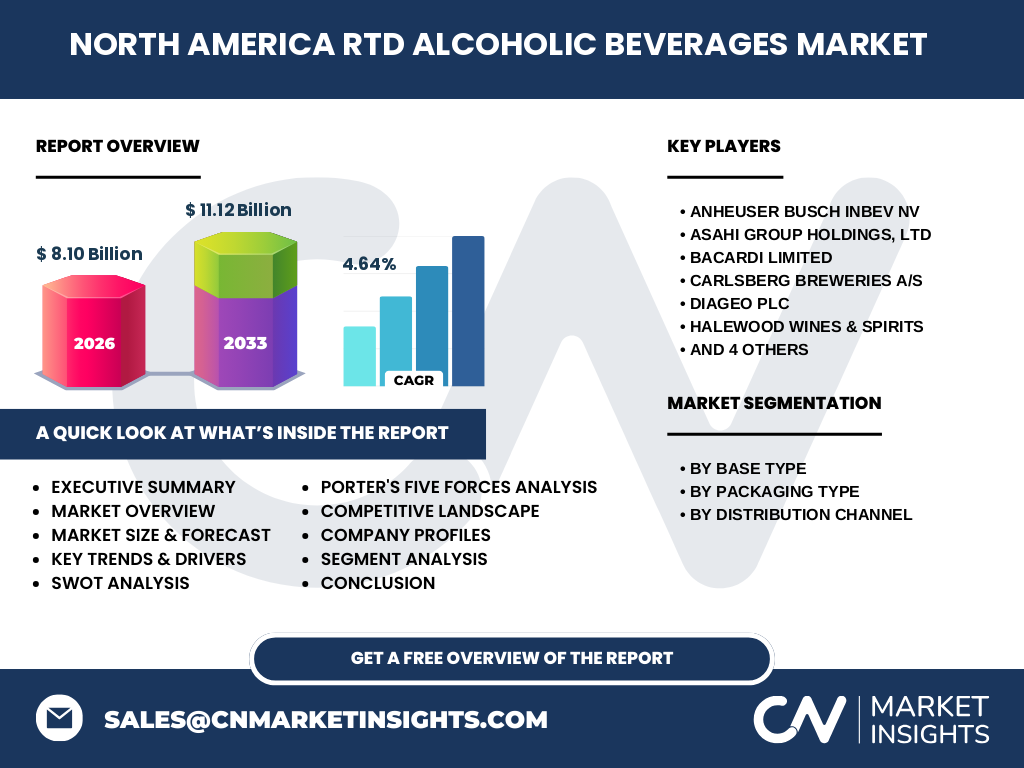

The market is characterised by a mix of global spirits giants and specialised RTD producers. Major competitors include Anheuser‑Busch InBev, Asahi Group Holdings, Bacardi Limited, Carlsberg Breweries, Diageo plc, Halewood Wines & Spirits, Heineken N.V., Mike’s Hard Lemonade Co., Pernod Ricard, and The Boston Beer Company. Consolidation trends are evident through strategic acquisitions of niche RTD brands and joint ventures aimed at expanding product portfolios and distribution reach.

What are the key findings in the Executive Summary?

The North America RTD alcoholic beverages market is valued at $8.10 billion in 2026 and is projected to reach $11.12 billion by 2033, representing a 4.64 % CAGR. Growth is underpinned by convenience‑driven consumption, flavour innovation, and the premium RTD cocktail wave. While regulatory pressures act as a restraint, opportunities in sustainable packaging and digital sales channels provide pathways for further expansion. Competitive dynamics are shaped by both legacy spirits houses and agile RTD specialists.

What is the forecast for the North America RTD Alcoholic Beverages Market for 2025‑2032?

Building on the current CAGR of 4.64 %, the market is expected to maintain steady growth through 2032. By 2032, the market size is anticipated to exceed $11 billion, reflecting continued consumer preference for ready‑to‑drink formats and the successful rollout of new product innovations across the whiskey, rum, vodka, and gin base categories.

How is the North America RTD Alcoholic Beverages Market sized and shared by segmentation?

Segmentation by base type shows whiskey, rum, vodka, and gin as the core spirit foundations for RTD products. Packaging segmentation splits the market between bottles and cans, with cans gaining traction due to portability and recyclability. Distribution channels are divided among supermarkets and hypermarkets, which dominate shelf presence, and specialty stores that cater to niche, premium, or craft‑focused RTD offerings.

What is the global North America RTD Alcoholic Beverages Market size and share by region?

Within the global RTD alcoholic beverages landscape, the North American region accounts for a substantial share, anchored by a $8.10 billion market size in 2026. This positions the region as a leading contributor to worldwide RTD sales, reflecting strong consumer demand for convenient alcoholic options.

What does the Regional Analysis of the North America RTD Alcoholic Beverages Market reveal?

Regional performance varies across the United States and Canada. The United States drives the majority of volume, supported by extensive distribution networks and a large on‑premise-to‑off‑premise shift. Canada shows solid growth, particularly in premium RTD cocktail segments, and benefits from a regulatory environment that encourages innovation in low‑alcohol, flavored drinks.

Which companies lead the North America RTD Alcoholic Beverages Market and what are their strategies?

Top players such as Anheuser‑Busch InBev, Diageo plc, and The Boston Beer Company leverage their extensive brand portfolios to launch RTD extensions of flagship spirits. Bacardi and Pernod Ricard focus on flavour diversification and limited‑edition releases. Heineken and Carlsberg pursue strategic acquisitions of craft RTD brands, while Mike’s Hard Lemonade Co. emphasises value‑priced, high‑volume products. Sustainability, digital marketing, and partnership with retailers are common strategic themes.

How does Porter’s Five Forces analysis apply to the North America RTD Alcoholic Beverages Market?

• Threat of new entrants: Moderate, due to high brand‑building costs but relatively low manufacturing barriers for small‑scale RTD launches. • Bargaining power of suppliers: Low to moderate, as base spirits are sourced from established distilleries with competitive pricing. • Bargaining power of buyers: High, driven by retailer shelf‑space constraints and consumer price sensitivity. • Threat of substitutes: Moderate, with traditional cocktails, beer, and emerging low‑ alcohol options offering alternatives. • Competitive rivalry: Intense, with numerous global and niche players vying for market share through innovation and promotional activity.

What are the SWOT highlights for the North America RTD Alcoholic Beverages Market?

Strengths: Strong demand for convenience, growing premium RTD segment, and robust distribution networks.

Weaknesses: Exposure to regulatory changes and tax structures.

Opportunities: Expansion into e‑commerce, sustainable packaging, and flavour‑forward product lines.

Threats: Health‑focused consumer shifts and aggressive competition for limited retail shelf space.

What does the value chain of the North America RTD Alcoholic Beverages Market look like?

The value chain begins with sourcing base spirits (whiskey, rum, vodka, gin) from distilleries, followed by formulation and blending, carbonation or infusion, packaging (bottles or cans), and distribution through wholesale channels to supermarkets, hypermarkets, and specialty stores. Marketing and brand‑building activities overlay the entire chain, while end‑consumer purchase completes the flow.

What key investment insights can be drawn for the North America RTD Alcoholic Beverages Market?

Investors should target companies that demonstrate strong innovation pipelines, especially those expanding premium RTD cocktail lines. Brands that secure shelf‑space in dominant retail channels and adopt recyclable packaging are positioned for long‑term growth. Strategic M&A activity aimed at acquiring niche, high‑growth RTD labels offers a clear pathway to market acceleration.

What conclusions can be drawn about the North America RTD Alcoholic Beverages Market?

The market remains on an upward trajectory, driven by consumer cravings for ready‑made, flavourful alcoholic drinks. Despite regulatory and health‑related headwinds, the sector’s adaptability—through packaging, flavour, and distribution innovations—supports sustained growth through 2032. Companies that combine premiumisation with sustainability and digital engagement are likely to capture the most value.

How was the research methodology designed for this report?

The study employed a mixed‑method approach, integrating primary interviews with industry executives, secondary data from company reports, trade publications, and government statistics. Market sizing used a top‑down model based on total alcoholic beverage sales, adjusted for RTD share, while forecasting applied historic growth rates, CAGR calculations, and scenario analysis to project 2027‑2033 figures.

What is the scope of this research and its limitations?

The scope covers the North America RTD alcoholic beverages market, segmented by base spirit type, packaging, and distribution channel, with a focus on the 2026 baseline and forecasts to 2033. Limitations include the exclusion of informal or unrecorded sales channels and the reliance on publicly available financial data, which may not capture proprietary brand‑specific performance.

Which key companies have recent developments in the North America RTD Alcoholic Beverages Market?

Recent developments include Anheuser‑Busch InBev’s launch of a new hard seltzer line, Diageo’s partnership with an e‑commerce platform to expand online sales, and The Boston Beer Company’s acquisition of a boutique RTD cocktail brand. Bacardi introduced a limited‑edition rum‑based RTD for summer, while Heineken unveiled a recyclable aluminum can range targeting sustainability‑focused consumers.