1. What is the Asia Pacific PACS and RIS Market Overview – definition, scope, and significance?

The Asia Pacific PACS (Picture Archiving and Communication System) and RIS (Radiology Information System) market encompasses technologies that capture, store, manage, and transmit medical imaging data, as well as systems that schedule, track, and report radiology workflow. The scope includes hardware, software, and services deployed in hospitals, diagnostic centers, research and academic institutes, and other health‑care facilities across the region. This market is significant because it enables faster diagnosis, reduces paperwork, improves data accessibility, and supports tele‑radiology initiatives that are critical for the geographically dispersed populations of Asia Pacific.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Asia Pacific PACS and RIS Market?

Key drivers include rising healthcare expenditures, increasing prevalence of chronic diseases, and government initiatives promoting digital health. The shift toward cloud‑based and web‑based solutions accelerates adoption. Restraints arise from high upfront capital costs, especially for on‑premise hardware, and limited interoperability standards in some countries. Challenges involve data privacy regulations and the need for skilled IT staff. Opportunities are found in AI‑enhanced imaging analytics, expanding tele‑radiology services in remote areas, and partnerships with cloud providers to lower entry barriers.

3. Which growth trends are currently influencing the Asia Pacific PACS and RIS Market?

Current trends include a rapid migration to cloud‑based deployment models, integration of AI for image interpretation and workflow optimization, and the emergence of hybrid solutions that combine on‑premise reliability with cloud scalability. Vendors are increasingly offering subscription‑based pricing, and there is a growing emphasis on mobile access for clinicians. Additionally, regional collaborations for standardizing DICOM and HL7 protocols are enhancing cross‑institutional data sharing.

4. How has COVID‑19 impacted the Asia Pacific PACS and RIS Market and what is the recovery trajectory?

The pandemic accelerated digital transformation as hospitals needed remote image review and reporting capabilities. Demand for web‑based and cloud solutions surged, while elective imaging volumes temporarily dropped, offset by increased tele‑radiology usage. Post‑COVID, the market has maintained momentum, with institutions retaining remote workflows and investing in resilient IT infrastructures, indicating a strong recovery and continued growth.

5. What does the competitive landscape look like for the Asia Pacific PACS and RIS Market?

The market is fragmented with several global and regional players competing on technology, service quality, and pricing. Major competitors such as Agfa‑Gevaert, Fujifilm, Philips, Siemens, IBM, Cerner, INFINITT, General Electric, McKesson, and Novarad dominate through extensive product portfolios and strategic partnerships. Recent consolidation includes joint ventures and acquisitions aimed at expanding AI capabilities and cloud service offerings.

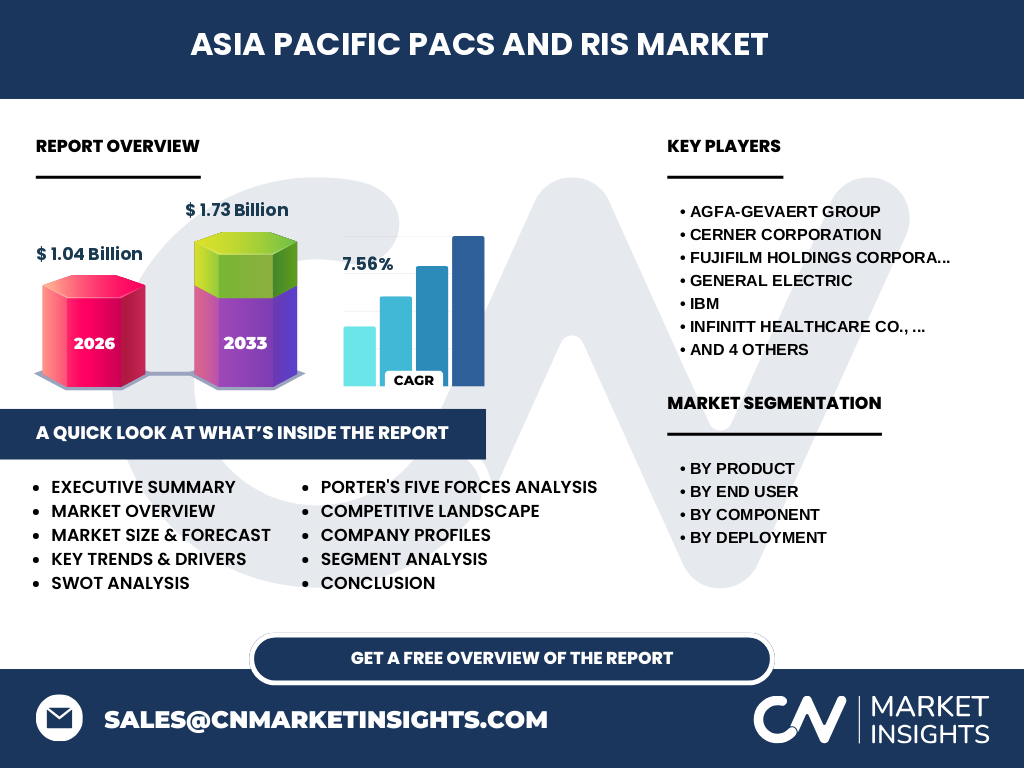

6. Can you provide an executive summary of the key findings for the Asia Pacific PACS and RIS Market?

The Asia Pacific PACS and RIS market is valued at US 1.04 billion in 2026 and is projected to reach US 1.73 billion by 2033, delivering a CAGR of 7.56 % over the forecast period. Growth is driven by digital health policies, rising imaging volumes, and cloud adoption. The market exhibits strong competition among ten leading vendors, with emerging opportunities in AI‑driven analytics and tele‑radiology. COVID‑19 catalyzed remote solution uptake, reinforcing long‑term demand.

7. What are the forecast expectations for the Asia Pacific PACS and RIS Market from 2025 to 2032?

Based on the provided CAGR of 7.56 %, the market is expected to expand steadily, moving from the 2026 baseline of US 1.04 billion to approximately US 1.73 billion by 2033. This trajectory suggests consistent year‑over‑year growth, driven by increasing hardware refresh cycles, software upgrades, and service contracts, as well as expanding adoption in emerging economies within the region.

8. How is the Asia Pacific PACS and RIS Market sized and shared across its primary segments?

The market is segmented by product (PACS and RIS), by end user (hospitals, diagnostic centers, research & academic institutes, other end users), by component (hardware, software, services), and by deployment (web‑based, on‑premise and cloud‑based). While exact monetary shares are not disclosed, hospitals remain the largest end‑user segment, followed by diagnostic centers. Software and services together capture a significant portion of spend, reflecting the shift toward subscription and cloud models, whereas hardware retains importance for on‑premise installations.

9. What is the geographic distribution of the Asia Pacific PACS and RIS Market?

The market covers the entire Asia Pacific region, with notable activity in China, Japan, India, South Korea, Australia, and Southeast Asian nations. Mature markets such as Japan and Australia lead in early cloud adoption, while high‑growth markets like India and Vietnam are expanding their imaging infrastructure, contributing to the overall regional expansion.

10. How does regional performance vary within the Asia Pacific PACS and RIS Market?

East Asia (Japan, South Korea, China) shows the highest penetration due to advanced healthcare systems and strong regulatory support for digital imaging. South‑East Asia displays rapid growth fueled by new hospital projects and government digital health agendas. South Asia, led by India, is characterized by a large population base and increasing private‑sector investment, driving demand for cost‑effective, cloud‑centric solutions. Australasia presents steady growth with a focus on interoperability and AI integration.

11. Which leading companies operate in the Asia Pacific PACS and RIS Market and what are their strategies?

Key players include Agfa‑Gevaert, Cerner, Fujifilm, General Electric, IBM, INFINITT Healthcare, Philips, McKesson, Novarad, and Siemens. Strategies revolve around expanding cloud portfolios, bundling AI analytics with existing PACS/RIS suites, forming partnerships with local distributors, and investing in regional R&D centers. Several firms are pursuing subscription‑based models to lower entry costs and increase recurring revenue.

12. What does Porter’s Five Forces analysis reveal about the Asia Pacific PACS and RIS Market?

• Threat of new entrants – Moderate; high capital requirements and regulatory hurdles limit newcomers, but cloud platforms lower barriers. • Bargaining power of buyers – High; large hospital groups can negotiate pricing and demand integrated solutions. • Bargaining power of suppliers – Low to moderate; component suppliers are numerous, though specialized AI algorithms add leverage. • Threat of substitutes – Low; alternative imaging workflows are limited. • Industry rivalry – Intense; ten major vendors compete on technology, service levels, and pricing.

13. What are the main SWOT considerations for the Asia Pacific PACS and RIS Market?

Strengths: Robust demand for digital imaging, strong vendor expertise, and increasing cloud adoption. Weaknesses: Capital‑intensive hardware, fragmented standards, and skill shortages. Opportunities: AI‑enhanced diagnostics, expansion into underserved rural markets, and subscription‑based pricing models. Threats: Data privacy regulations, cyber‑security risks, and economic fluctuations affecting health‑care budgets.

14. How is value created and transferred in the Asia Pacific PACS and RIS Market value chain?

The value chain begins with component manufacturers (servers, storage, networking), followed by software developers delivering PACS/RIS platforms. System integrators assemble hardware and software, adding customization and implementation services. Cloud providers supply hosting and scalability, while after‑sales support, training, and maintenance generate recurring revenue. End users (hospitals, diagnostic centers) extract value through faster diagnosis, reduced operational costs, and improved patient outcomes.

15. What key investment insights should stakeholders consider for the Asia Pacific PACS and RIS Market?

Investors should focus on vendors with strong cloud and AI roadmaps, as these capabilities are driving next‑generation growth. Partnerships with local health ministries can unlock public‑sector contracts. Companies offering flexible subscription models are likely to capture price‑sensitive buyers. Monitoring regulatory developments around data protection will be essential to mitigate risk.

16. What conclusions can be drawn about the future of the Asia Pacific PACS and RIS Market?

The market is on a clear upward trajectory, supported by a 7.56 % CAGR and a projected rise to US 1.73 billion by 2033. Digital transformation, AI integration, and cloud deployment are the pillars of future growth. While challenges such as cost and data security persist, the overall outlook remains positive, with ample room for innovation and market entry.

17. Which research methodology was employed to compile this market report?

The study combined primary interviews with industry experts, vendor executives, and health‑care providers, together with secondary data from company filings, press releases, and reputable databases. Trend analysis, CAGR calculations, and Porter’s Five Forces modeling were applied to synthesize insights and validate market size estimates.

18. What is the scope of this research and its limitations?

The scope covers the Asia Pacific region, focusing on PACS and RIS products, end‑users, components, and deployment models. It includes market sizing for 2026 and forecasts to 2033. Limitations stem from the reliance on publicly available financial figures and the absence of granular country‑level revenue breakdowns, which are beyond the provided dataset.

19. Which key companies have made recent developments in the Asia Pacific PACS and RIS Market?

Recent activity includes Agfa‑Gevaert launching a cloud‑native PACS platform, Fujifilm expanding its AI imaging suite across Japan, Philips introducing a hybrid on‑premise/cloud RIS solution in Australia, Siemens unveiling a subscription‑based imaging workflow service, and IBM partnering with regional hospitals to integrate Watson AI for radiology reporting. These moves illustrate an industrywide shift toward cloud, AI, and service‑oriented offerings.