North America Mobile Cardiac Telemetry Systems Market Overview - Definition, scope, and significance?

North America Mobile Cardiac Telemetry (MCT) Systems refer to portable, wireless solutions that continuously monitor a patient’s cardiac rhythm in real‑time and transmit data to healthcare providers for immediate analysis. The market encompasses hardware (lead‑based and patch‑based devices), software platforms, data‑communication services, and related support services delivered to hospitals, ambulatory surgical centres, and cardiac centres across the United States and Canada. Its significance lies in enabling early detection of arrhythmias, reducing hospital stays, improving patient outcomes, and supporting value‑based care models that prioritize preventive monitoring over episodic treatment.

North America Mobile Cardiac Telemetry Systems Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising prevalence of cardiovascular disease, increasing demand for remote patient monitoring, reimbursement reforms that favour tele‑health, and rapid adoption of wearable sensor technologies. Restraints stem from high upfront equipment costs, stringent regulatory pathways, and interoperability concerns with legacy hospital IT systems. Challenges involve maintaining data security, ensuring patient compliance with device usage, and managing the learning curve for clinicians. Opportunities arise from advancements in AI‑based arrhythmia detection, integration with electronic health records, and expansion of service models into post‑acute care and home‑based cardiac rehabilitation.

North America Mobile Cardiac Telemetry Systems Market Growth Trends - Current and emerging trends shaping the market?

Current trends show a shift from traditional lead‑based monitors toward adhesive patch‑based solutions that improve patient comfort and enable longer monitoring periods. Emerging trends include the incorporation of cloud‑based analytics, real‑time alerts powered by machine learning, and hybrid models that combine telemetry with smartphone applications for patient‑reported outcomes. Partnerships between device manufacturers and digital health platforms are accelerating, while payers increasingly adopt bundled payment structures that reward remote monitoring effectiveness.

COVID-19 Impact on the North America Mobile Cardiac Telemetry Systems Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated adoption of MCT systems as hospitals sought to minimize inpatient exposure and discharge patients earlier. Telemetry services proved critical for monitoring cardiac complications in COVID‑19 patients, leading to a surge in short‑term contracts and rapid scaling of data‑communication infrastructure. Post‑pandemic, the market retained momentum, with healthcare providers integrating telemetry into broader virtual care pathways. Recovery is characterized by steady investment in remote monitoring, reinforced by patient preference for at‑home care.

North America Mobile Cardiac Telemetry Systems Market Competitive Landscape - Major competitors and market consolidation?

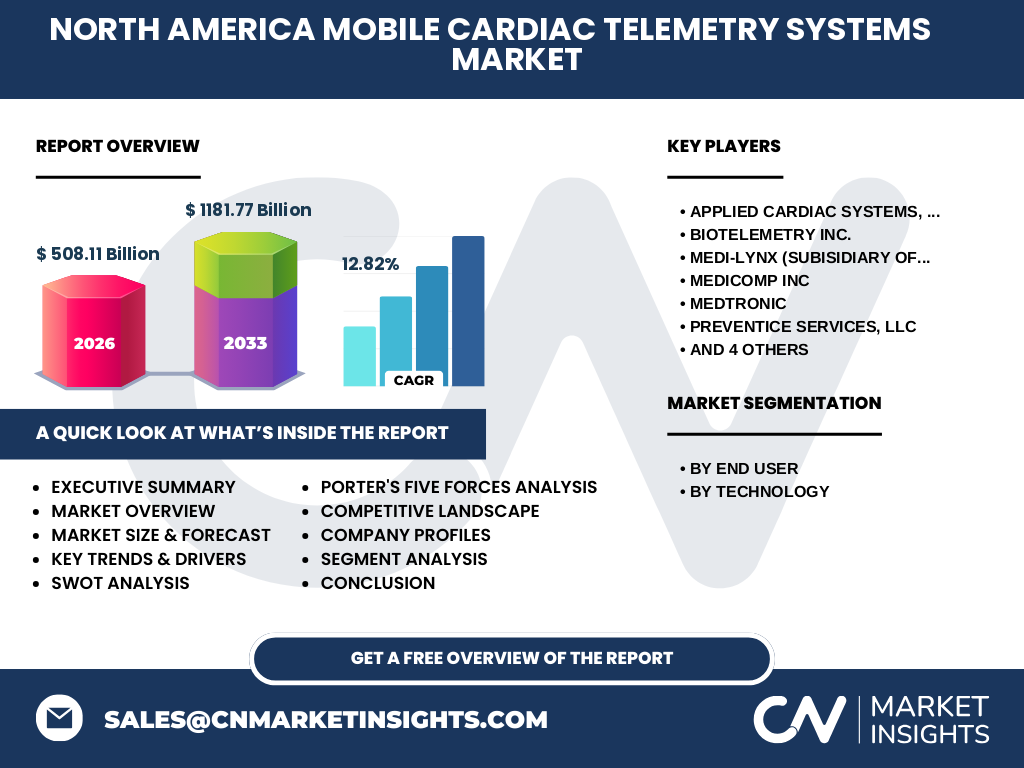

The competitive arena is populated by established cardiac diagnostics firms and emerging digital health players. Notable companies include Applied Cardiac Systems, Inc., BioTelemetry Inc., Medi‑Lynx (a subsidiary of Medicalgorithmics, S.A.), Medicomp Inc., Medtronic, Preventice Services, LLC, Telerhythmics, LLC, The Scottcare Corporation, Welch Allyn, and Zoll Medical Corporation. Recent activity shows strategic mergers, acquisition of niche software vendors, and joint ventures aimed at expanding service networks and enhancing data‑analytics capabilities, indicating moderate consolidation focused on end‑to‑end solutions.

Executive Summary - High-level overview and key findings about North America Mobile Cardiac Telemetry Systems Market?

The North America MCT market is expanding rapidly, driven by a strong prevalence of cardiovascular conditions and a healthcare ecosystem that rewards remote monitoring. With a 2026 market size of $508.11 billion and a projected valuation of $1,181.77 billion by 2033, the market is expected to grow at a compound annual growth rate of 12.82 %. Growth is supported by technology shifts toward patch‑based devices, AI‑enabled analytics, and supportive reimbursement policies. Competitive dynamics are characterized by a blend of legacy manufacturers and agile digital entrants, while regional demand is strongest in hospital settings, followed by ambulatory surgical centres and specialized cardiac centres.

North America Mobile Cardiac Telemetry Systems Market Forecast - Projections for 2025-2032 period?

Based on current trajectories, the market will continue its robust expansion through 2032, maintaining a CAGR close to the historical 12.82 % range. The forecast reflects sustained investment in wearable telemetry, increased integration with tele‑health platforms, and expanding payer coverage. Growth will be most pronounced in the United States, where regulatory support and large healthcare networks drive adoption, while Canada will experience moderate but steady uptake driven by national health system initiatives.

North America Mobile Cardiac Telemetry Systems Market Size and Share by Segmentation - Breakdown by End User and Technology?

Segmentation by end user reveals hospitals as the largest consumer, leveraging telemetry for acute cardiac monitoring and post‑procedural surveillance. Ambulatory surgical centres represent a growing niche as same‑day procedures increase, while dedicated cardiac centres adopt telemetry for specialized arrhythmia clinics. Technology segmentation shows a clear transition: lead‑based systems still hold a legacy share but are being overtaken by patch‑based devices, which command higher growth due to better patient compliance and reduced skin irritation.

Global North America Mobile Cardiac Telemetry Systems Market Size and Share by Region - Geographic distribution?

Within the global context, North America accounts for the dominant share of the Mobile Cardiac Telemetry market, reflecting its advanced healthcare infrastructure, high per‑capita spending on cardiac care, and early adoption of remote monitoring technologies. The United States contributes the bulk of the regional volume, while Canada adds a smaller but strategically important portion, especially in provinces that prioritize digital health transformation.

Regional Analysis of the North America Mobile Cardiac Telemetry Systems Market - Detailed regional market performance?

The United States exhibits the highest growth velocity, driven by large integrated health systems, strong venture capital activity, and progressive Medicare policies that reimburse remote cardiac monitoring. Key states such as California, Texas, and New York lead in device deployment. In Canada, provinces like Ontario and British Columbia are early adopters, supported by provincial tele‑health frameworks and public‑sector procurement contracts. Both regions show parallel trends toward patch‑based technology and AI‑enabled data interpretation.

Leading Company Profiles in the North America Mobile Cardiac Telemetry Systems Market - Industry players and strategies?

Applied Cardiac Systems, Inc. focuses on integrated telemetry platforms with a strong service network. BioTelemetry Inc. leverages its extensive patient monitoring database to offer predictive analytics. Medi‑Lynx (Medicalgorithmics) brings European‑grade algorithmic expertise to the North American market. Medicomp Inc. specializes in customizable software solutions for cardiac data visualization. Medtronic incorporates telemetry into its broader cardiac rhythm management portfolio, while Preventice Services, LLC emphasizes subscription‑based monitoring services. Telerhythmics, LLC and The Scottcare Corporation target niche ambulatory markets, and Welch Allyn and Zoll Medical Corporation expand their diagnostic device portfolios to include mobile telemetry capabilities.

Porter's Five Forces Analysis of the North America Mobile Cardiac Telemetry Systems Market - Competitive forces assessment?

Threat of new entrants is moderate; high capital requirements and regulatory hurdles limit easy entry, yet digital startups with AI expertise can disrupt. Bargaining power of suppliers is low to moderate, as component manufacturers are numerous, though specialized sensor technology can command premium pricing. Bargaining power of buyers is rising, with large hospital systems negotiating volume discounts and demanding integrated data solutions. Threat of substitutes remains limited, as alternative monitoring (e.g., implantable loop recorders) serves different clinical scenarios. Industry rivalry is intense, driven by product innovation, service differentiation, and strategic alliances.

SWOT Analysis of the North America Mobile Cardiac Telemetry Systems Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven clinical utility, strong payer support, and a growing ecosystem of interoperable devices. Weaknesses: Cost of deployment, data‑security concerns, and fragmented standards across vendors. Opportunities: Expansion into home‑based cardiac rehabilitation, AI‑driven predictive algorithms, and bundled reimbursement models. Threats: Regulatory changes, potential cyber‑security breaches, and competition from invasive monitoring technologies.

North America Mobile Cardiac Telemetry Systems Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with component suppliers (sensors, batteries, communications modules), proceeds to device manufacturers (lead‑based and patch‑based systems), followed by software developers that create data‑analytics platforms. Next, service providers deliver installation, patient onboarding, and data interpretation. Finally, payers and healthcare providers close the loop by reimbursing services and integrating insights into clinical decision‑making. Collaboration across each stage—especially between device makers and analytics firms—adds the most incremental value.

Key Investment Insights in the North America Mobile Cardiac Telemetry Systems Market - Strategic investment recommendations?

Investors should prioritize companies that combine hardware with robust, subscription‑based analytics services, as recurring revenue streams enhance valuation stability. Targets with strong FDA clearances, established hospital contracts, and AI‑enabled detection algorithms present attractive growth prospects. Additionally, strategic investments in cloud‑infrastructure partners and cybersecurity firms can provide ancillary upside as data integrity becomes a critical differentiator.

North America Mobile Cardiac Telemetry Systems Market Conclusion - Summary and key takeaways?

The North America MCT market is on a decisive upward trajectory, underpinned by escalating cardiovascular disease burden, payer incentives for remote monitoring, and rapid technological evolution from lead‑based to patch‑based devices. With a 2026 market size of $508.11 billion and a forecasted $1,181.77 billion by 2033, the sector offers compelling opportunities for innovators, service providers, and investors alike. Success will hinge on delivering seamless, secure, and AI‑enhanced telemetry solutions that integrate fully with existing care pathways.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with key industry executives, surveys of hospital procurement leaders, and secondary data from regulatory filings, payer policy documents, and reputable market databases. Trend extrapolation used historical CAGR data and scenario analysis to project the 2025‑2032 outlook. Competitive profiling combined financial statements, product roadmaps, and partnership announcements to assess market positioning.

Research Scope - Coverage and limitations?

The research covers the North American Mobile Cardiac Telemetry Systems market, focusing on product categories (lead‑based and patch‑based), end‑user segments (hospitals, ambulatory surgical centres, cardiac centres), and major geographic territories (United States and Canada). It excludes detailed pricing breakdowns and proprietary clinical trial results, and it relies on publicly available data and voluntarily disclosed information from participating firms.

Key Companies and Recent Developments in the North America Mobile Cardiac Telemetry Systems Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Applied Cardiac Systems, Inc. announced a cloud‑based analytics upgrade that reduces data latency by 30 %. BioTelemetry Inc. launched a next‑generation patch device with integrated Bluetooth Low Energy for direct smartphone pairing. Medi‑Lynx expanded its North American footprint through a distribution agreement with a major U.S. health system. Medicomp Inc. introduced an open‑API platform to enable seamless EHR integration. Medtronic incorporated telemetry into its cardiac resynchronization therapy portfolio, emphasizing hybrid monitoring. Preventice Services, LLC rolled out a subscription model that bundles device, data analytics, and clinical support. Telerhythmics, LLC partnered with a tele‑health insurer to pilot remote arrhythmia detection in post‑discharge patients. The Scottcare Corporation released a lightweight, disposable patch aimed at pediatric cardiology. Welch Allyn unveiled a modular telemetry unit compatible with its existing bedside monitors. Zoll Medical Corporation announced a strategic investment in AI‑driven arrhythmia classification software, positioning its telemetry line for future data‑centric care models.