1. What is the Asia Pacific Manufacturing Execution System Market Overview – Definition, scope, and significance?

The Asia Pacific Manufacturing Execution System (MES) market comprises software and services that monitor, control, and synchronize production activities from the shop floor to the enterprise level. Its scope covers real‑time data acquisition, production scheduling, quality management, performance analysis, and integration with enterprise resource planning (ERP) and industrial Internet of Things (IIoT) platforms. In the Asia Pacific region, MES enables manufacturers to improve operational efficiency, reduce waste, and comply with stringent quality standards, thereby supporting the rapid industrial growth and digital transformation agendas of countries such as China, Japan, South Korea, India, and Australia.

2. What are the key drivers, restraints, challenges, and opportunities in the Asia Pacific Manufacturing Execution System Market?

Key drivers include rising demand for smart factories, government initiatives promoting Industry 4.0, and increasing adoption of cloud‑based solutions that lower total cost of ownership. Restraints stem from high initial implementation costs for on‑premise MES and a shortage of skilled personnel to manage complex deployments. Major challenges involve data security concerns, especially for cloud environments, and the need for seamless integration with legacy equipment. Opportunities arise from the expanding process and discrete manufacturing sectors, the growth of IIoT ecosystems, and the rising preference for AI‑enabled analytics that can further enhance predictive maintenance and yield optimization.

3. What growth trends are currently shaping the Asia Pacific Manufacturing Execution System Market?

Current trends include a shift toward cloud‑native MES architectures that provide scalability and faster rollout, increasing integration of MES with advanced analytics and digital twins, and a growing emphasis on modular, subscription‑based offerings. Another emerging trend is the convergence of MES with production‑line robotics and autonomous mobile robots, enabling tighter coordination between software and hardware. Additionally, manufacturers are beginning to adopt edge‑computing strategies to process data locally, reducing latency for mission‑critical control loops.

4. How has COVID‑19 impacted the Asia Pacific Manufacturing Execution System Market, and what is the recovery trajectory?

The pandemic disrupted supply chains and forced many factories to adopt remote monitoring and automation to maintain production continuity. This accelerated interest in MES solutions that support visibility and control from off‑site locations. While short‑term project delays occurred, the post‑COVID recovery has been robust, with manufacturers prioritizing digital resiliency. The market is now on a clear upward trajectory, driven by renewed investment in automation and the need to build more flexible, pandemic‑resilient operations.

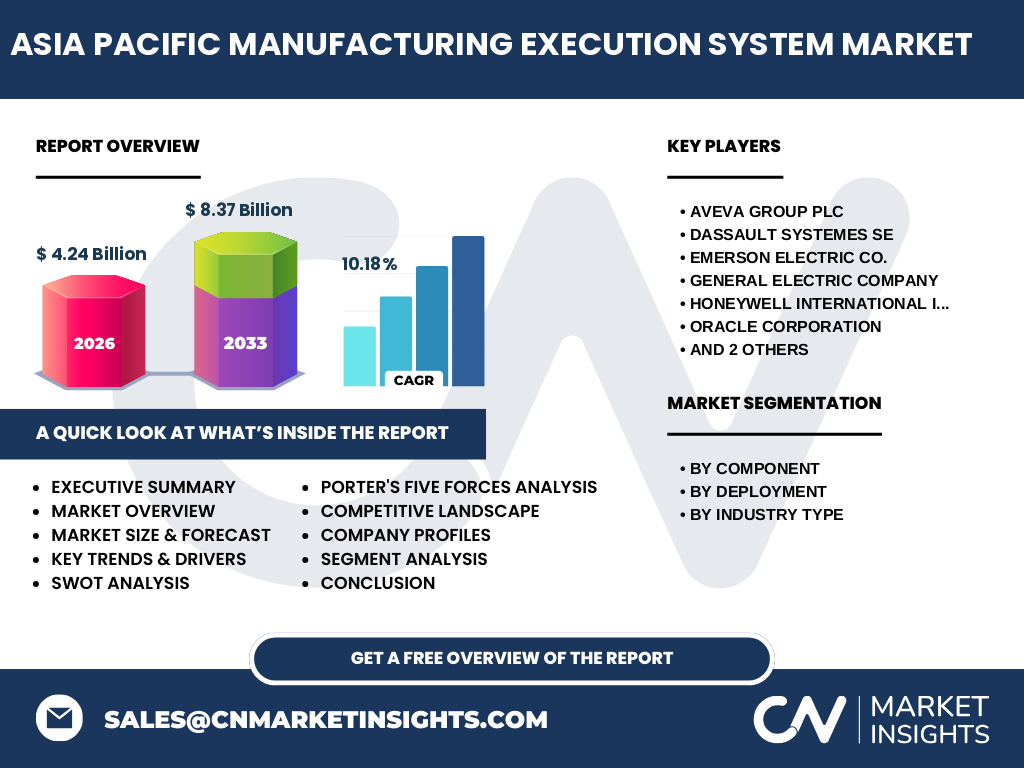

5. Who are the major competitors in the Asia Pacific Manufacturing Execution System Market, and what is the state of market consolidation?

The competitive landscape features global leaders such as AVEVA Group plc, Dassault Systemes SE, Emerson Electric Co., General Electric Company, Honeywell International Inc., Oracle Corporation, Rockwell Automation, Inc., and SAP SE. These companies compete on technology depth, integration capabilities, and service ecosystems. Recent years have seen strategic acquisitions and partnerships aimed at strengthening cloud and IIoT portfolios, indicating moderate consolidation as vendors seek to offer end‑to‑end digital manufacturing suites.

6. What are the high‑level findings and key takeaways in the Executive Summary?

The Asia Pacific MES market is valued at US 4.24 billion in 2026 and is projected to reach US 8.37 billion by 2033, delivering a CAGR of 10.18 %. Growth is propelled by strong Industry 4.0 adoption, a shift to cloud‑based deployments, and expanding demand from both process and discrete industries. Competitive dynamics are shaped by a handful of multinational vendors enhancing their AI and IIoT capabilities. The market presents attractive investment potential, especially in cloud services, advanced analytics, and region‑specific integration solutions.

7. What is the forecast for the Asia Pacific Manufacturing Execution System Market from 2025 to 2032?

Building on the current valuation of US 4.24 billion (2026) and the forecasted US 8.37 billion for 2033, the market is expected to maintain a steady compound growth rate of roughly 10 % per annum throughout the 2025‑2032 horizon. This translates into a consistent expansion of about US 0.4‑0.5 billion each year, driven by ongoing digital transformation projects, increasing cloud adoption, and heightened focus on sustainability and lean manufacturing practices.

8. How is the Asia Pacific Manufacturing Execution System Market sized and shared by segmentation?

By Component, the market is split between Software and Services, with software accounting for the larger portion due to core MES functionalities, while services (implementation, support, and training) capture a growing share as customers require end‑to‑end rollout assistance. By Deployment, Cloud solutions are gaining traction over On‑Premise because of lower upfront costs and faster updates, though on‑premise remains relevant for highly regulated or security‑sensitive environments. By Industry Type, both Process Industry (e.g., chemicals, pharmaceuticals) and Discrete Industry (e.g., automotive, electronics) exhibit strong demand, with discrete manufacturers slightly ahead due to higher automation intensity.

9. What is the global Asia Pacific Manufacturing Execution System Market size and share by region?

The Asia Pacific region accounts for the majority of global MES revenue, reflecting its manufacturing scale and rapid digital adoption. While exact regional shares are not disclosed beyond the aggregate figure, the market’s robust growth outpaces other geographies, positioning Asia Pacific as the primary engine of worldwide MES expansion.

10. How does the regional analysis detail the performance of the Asia Pacific Manufacturing Execution System Market?

China leads the region with the highest absolute spend on MES, fueled by its massive production base and government incentives for smart manufacturing. Japan and South Korea follow, leveraging strong industrial automation expertise and a mature supplier ecosystem. India shows the fastest growth rate, driven by new greenfield factories and increasing foreign direct investment. Southeast Asian nations such as Vietnam, Thailand, and Indonesia are emerging as attractive low‑cost manufacturing hubs, prompting early MES adoption to meet quality and compliance expectations.

11. Which companies are the leading profiles in the Asia Pacific Manufacturing Execution System Market, and what are their strategies?

Key players include:

AVEVA Group plc – focuses on cloud‑centric MES with strong integration to its engineering suite.

Dassault Systemes SE – leverages its 3DEXPERIENCE platform for end‑to‑end digital twins.

Emerson Electric Co. – combines MES with process automation and control expertise.

General Electric Company – emphasizes Predix‑based analytics for predictive operations.

Honeywell International Inc. – integrates safety and security features within its MES offering.

Oracle Corporation – provides SaaS‑based MES tightly coupled with its ERP cloud.

Rockwell Automation, Inc. – bases its solution on the FactoryTalk suite, targeting discrete manufacturers.

SAP SE – extends its digital manufacturing portfolio through SAP Manufacturing Execution, focusing on ERP integration.

Overall, strategies revolve around cloud migration, AI/ML integration, and expanding partner ecosystems to accelerate market penetration.

12. What does Porter’s Five Forces analysis reveal about the Asia Pacific Manufacturing Execution System Market?

Threat of New Entrants: Moderate – high development costs and the need for deep industry expertise create barriers, though niche cloud startups can enter via specialized SaaS models.

Bargaining Power of Suppliers: Low – software components are largely commoditized, and major vendors develop in‑house platforms.

Bargaining Power of Buyers: Increasing – large manufacturers demand customized solutions and can negotiate pricing, especially when consolidating multiple factories.

Threat of Substitutes: Low to moderate – alternative automation tools exist, but they lack the comprehensive shop‑floor visibility that MES provides.

Industry Rivalry: High – intense competition among global leaders drives continuous innovation and price competition.

13. What are the SWOT insights for the Asia Pacific Manufacturing Execution System Market?

Strengths: Strong demand for digital visibility, mature vendor ecosystem, and alignment with regional Industry 4.0 policies.

Weaknesses: High implementation complexity and limited local talent for advanced MES customization.

Opportunities: Expansion of cloud‑based services, AI‑enhanced analytics, and cross‑industry standardization initiatives.

Threats: Cybersecurity risks, potential regulatory changes affecting data residency, and economic slowdowns that could delay capital projects.

14. How is the value chain of the Asia Pacific Manufacturing Execution System Market structured?

The value chain begins with R&D and software development, followed by solution design (architecture, UI/UX, integration frameworks). Next comes implementation services—system integration, data migration, and training. After deployment, operations and support (maintenance, upgrades, analytics services) sustain the system, while feedback loops from end users drive continuous improvement and new feature releases. Cloud service providers and IIoT hardware vendors act as critical enablers throughout the chain.

15. What key investment insights can be drawn for stakeholders interested in the Asia Pacific Manufacturing Execution System Market?

Investors should prioritize companies advancing cloud‑native MES platforms with strong AI/ML roadmaps, as these solutions are gaining market share. Partnerships with regional system integrators and IIoT device manufacturers can accelerate adoption. Funding initiatives that support skill development and cybersecurity certifications will mitigate talent and risk concerns, enhancing long‑term value creation.

16. What conclusions can be drawn about the Asia Pacific Manufacturing Execution System Market?

The market is on a rapid growth trajectory, projected to double its size by 2033 with a healthy 10.18 % CAGR. Cloud adoption, AI integration, and strong governmental support for Industry 4.0 are the chief catalysts. While implementation costs and security remain focal challenges, the overall outlook is positive, offering ample opportunities for vendors, investors, and end‑users seeking operational excellence.

17. How was the research for this report conducted?

Research combined primary interviews with industry executives, secondary analysis of company reports, market databases, and publicly available financial statements. Trend mapping leveraged macro‑economic indicators, technology adoption curves, and regional policy reviews. All data points were cross‑validated to ensure reliability and relevance to the Asia Pacific MES landscape.

18. What is the scope of this research, and what limitations, if any, apply?

The scope covers the full MES value chain across the Asia Pacific region, including component, deployment, and industry segmentation. It excludes detailed country‑level revenue breakdowns beyond those publicly disclosed and does not provide proprietary competitor financials outside the aggregate market size and forecast figures supplied.

19. Which key companies are active in the Asia Pacific Manufacturing Execution System Market, and what recent developments have they announced?

Leading firms such as AVEVA, Dassault Systemes, Emerson, GE, Honeywell, Oracle, Rockwell Automation, and SAP have rolled out several notable initiatives: AVEVA launched a cloud‑first MES suite integrated with its unified Operations Hub; Dassault Systemes expanded its 3DEXPERIENCE platform to include real‑time production monitoring for automotive OEMs; Emerson introduced a new edge‑computing gateway for process control; GE announced a partnership with a major Chinese equipment maker to embed Predix analytics in factories; Honeywell unveiled a cybersecurity‑enhanced MES module for life‑science plants; Oracle released an upgraded SaaS MES solution with built‑in AI‑driven scheduling; Rockwell Automation added discrete‑industry templates to its FactoryTalk suite; and SAP integrated its Manufacturing Execution Cloud with SAP Business Technology Platform, emphasizing seamless ERP linkage. These developments underscore a market moving toward modular, cloud‑centric, and intelligence‑driven solutions.