1. Europe Manufacturing Execution System Market Overview - Definition, scope, and significance?

The Europe Manufacturing Execution System (MES) market comprises software and services that monitor, control, and synchronize production activities on the factory floor. MES bridges the gap between enterprise‑level planning (ERP) and the actual manufacturing processes, delivering real‑time visibility, traceability, and performance analytics. Its scope covers core functions such as production scheduling, resource allocation, quality management, compliance reporting, and data collection across both process‑heavy (e.g., chemicals, pharmaceuticals) and discrete (e.g., automotive, electronics) industries. In Europe, MES is a strategic enabler for Industry 4.0 initiatives, helping manufacturers improve operational efficiency, reduce waste, and meet stringent regulatory standards, thereby safeguarding competitiveness in a highly regulated and innovation‑driven market.

2. Europe Manufacturing Execution System Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Drivers: accelerating digital transformation, stringent EU environmental and quality regulations, and the need for greater supply‑chain resilience are propelling MES adoption. The shift toward smart factories and the integration of IoT, AI, and advanced analytics further stimulate demand.

Restraints: high implementation costs, legacy system incompatibility, and a shortage of skilled personnel can delay projects.

Challenges: data security concerns and the complexity of scaling MES across multi‑site operations are notable hurdles.

Opportunities: emerging cloud‑based MES models, modular service offerings, and the expansion of MES into SMEs and emerging European manufacturing hubs present significant growth avenues.

3. Europe Manufacturing Execution System Market Growth Trends - Current and emerging trends shaping the market?

Key trends include a rapid migration from on‑premise to cloud‑hosted MES solutions, delivering lower upfront investment and easier scalability. Manufacturers are increasingly adopting hybrid deployments that combine cloud flexibility with on‑premise data sovereignty for critical processes. Integration of advanced analytics and AI is enabling predictive maintenance and real‑time quality optimization. Additionally, the convergence of MES with Manufacturing Operations Management (MOM) platforms creates unified control layers that support end‑to‑end digital twins, further enhancing decision‑making speed.

4. COVID-19 Impact on the Europe Manufacturing Execution System Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains and forced many European factories into temporary shutdowns, highlighting the need for greater operational agility. MES vendors experienced a surge in demand for remote monitoring and visibility tools, accelerating cloud adoption. Post‑pandemic, the market entered a robust recovery phase, with manufacturers investing in MES to improve resilience, enable flexible production lines, and meet fluctuating demand patterns. This recovery is reflected in the strong projected CAGR of 11.79% for the period 2027‑2033.

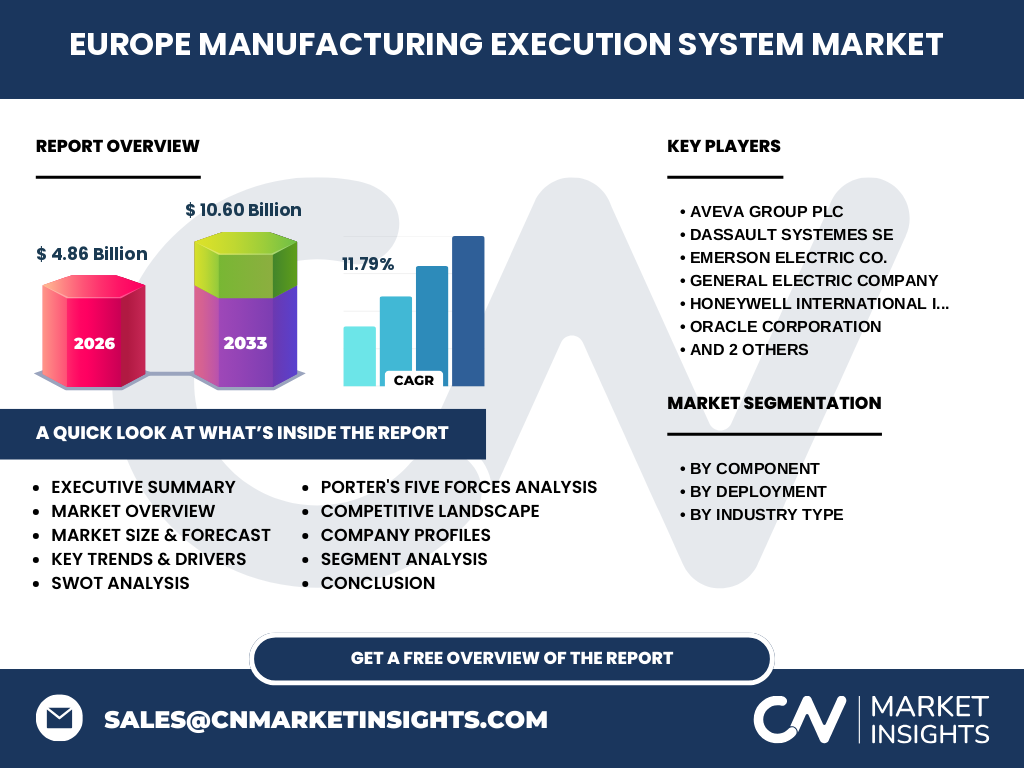

5. Europe Manufacturing Execution System Market Competitive Landscape - Major competitors and market consolidation?

The European MES arena is dominated by a mix of global technology providers and niche specialists. Leading firms such as AVEVA Group plc, Dassault Systèmes SE, Emerson Electric Co., General Electric Company, Honeywell International Inc., Oracle Corporation, Rockwell Automation, Inc., and SAP SE command the primary share through comprehensive portfolios and strong channel networks. Recent years have seen strategic acquisitions—particularly in the cloud‑MES space—to bolster capabilities and expand customer bases, indicating a moderate level of consolidation aimed at delivering end‑to‑end digital manufacturing solutions.

6. Executive Summary - High-level overview and key findings about Europe Manufacturing Execution System Market?

The Europe MES market, valued at €4.86 billion in 2026, is projected to reach €10.60 billion by 2033, representing a compound annual growth rate of 11.79%. Growth is driven by digital‑transformation imperatives, regulatory pressure, and a swift shift toward cloud and AI‑enabled solutions. While cost and skill gaps pose challenges, opportunities abound in modular, cloud‑first offerings and expanding into SMEs. The competitive landscape is led by eight major technology firms, with ongoing consolidation enhancing solution breadth. Overall, the market presents a compelling growth narrative for investors and manufacturers seeking to future‑proof European production.

7. Europe Manufacturing Execution System Market Forecast - Projections for 2025-2032 period?

Building on the 2026 baseline of €4.86 billion, the market is expected to accelerate to €10.60 billion by the end of 2033, translating to an 11.79% CAGR. By 2028, the market is anticipated to surpass the €7 billion mark, driven by heightened cloud adoption and AI integration. The growth trajectory remains robust through 2032, underpinned by continued EU initiatives supporting Industry 4.0, and increasing demand for real‑time production optimization across both process and discrete sectors.

8. Europe Manufacturing Execution System Market Size and Share by Segmentation - Breakdown by component, deployment, and industry type?

Segmentation reveals three primary dimensions:

Component: Software dominates the market, complemented by services that include implementation, integration, and ongoing support.

Deployment: Cloud solutions are gaining market share rapidly, while on‑premise remains significant for manufacturers with strict data‑sovereignty requirements.

Industry Type: Discrete manufacturing (automotive, aerospace, electronics) accounts for a substantial portion of MES spend, yet the process industry (pharma, chemicals, food & beverage) shows higher growth rates due to extensive compliance and traceability needs.

9. Global Europe Manufacturing Execution System Market Size and Share by Region - Geographic distribution?

Europe represents a leading regional hub for MES adoption, contributing a sizeable share of the global market due to dense manufacturing clusters in Germany, France, Italy, and the United Kingdom. While precise global percentages are not disclosed, Europe’s strategic focus on sustainability, smart‑factory standards, and strong regulatory frameworks positions it ahead of many other regions in MES penetration.

10. Regional Analysis of the Europe Manufacturing Execution System Market - Detailed regional market performance?

Western Europe, led by Germany and the United Kingdom, exhibits the highest MES penetration, driven by advanced automotive and aerospace sectors. Northern Europe (Scandinavia) shows strong cloud‑MES uptake, reflecting its early cloud adoption culture. Southern Europe (Italy, Spain) is expanding MES use in the process industry, especially food and beverage. Eastern European economies are emerging adopters, attracted by cost‑effective cloud solutions and EU funding for digitalization projects.

11. Leading Company Profiles in the Europe Manufacturing Execution System Market - Industry players and strategies?

AVEVA Group plc: Leverages its engineering heritage to deliver integrated MES‑MOM platforms with strong process‑industry focus.

Dassault Systèmes SE: Emphasizes 3DEXPERIENCE‑driven MES that aligns design and production data.

Emerson Electric Co.: Offers robust process‑MES solutions tied to automation hardware.

General Electric Company: Provides Predix‑based MES for high‑value, asset‑intensive plants.

Honeywell International Inc.: Focuses on safety‑critical MES for chemicals and aerospace.

Oracle Corporation: Delivers cloud‑native MES through its ERP ecosystem.

Rockwell Automation, Inc.: Combines PLC expertise with MES for discrete manufacturers.

SAP SE: Integrates MES tightly with SAP ERP, targeting large, multinational plants.

12. Porter's Five Forces Analysis of the Europe Manufacturing Execution System Market - Competitive forces assessment?

Threat of New Entrants: Moderate; high development costs and strong incumbent IP create barriers, yet cloud platforms lower entry thresholds.

Bargaining Power of Buyers: Increasing, as manufacturers demand modular, scalable solutions and can switch between vendors more easily in a cloud‑first environment.

Bargaining Power of Suppliers: Low to moderate; key technology components (cloud infrastructure, AI algorithms) are sourced from few large providers, but MES vendors can negotiate favorable terms.

Threat of Substitutes: Limited; while ERP extensions and niche shop‑floor data capture tools exist, they lack full MES functionality.

Industry Rivalry: High; eight major players compete on integration breadth, cloud capabilities, and industry‑specific modules, driving continuous innovation.

13. SWOT Analysis of the Europe Manufacturing Execution System Market - Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory push, high demand for real‑time visibility, and mature technology base.

Weaknesses: Complex implementation, high upfront costs, and talent shortages.

Opportunities: Cloud‑first MES models, AI‑driven predictive analytics, expansion into SMEs, and cross‑border EU digital‑funding programs.

Threats: Cybersecurity risks, potential economic slowdown affecting capital spending, and rapid technology shifts that may outpace legacy system upgrades.

14. Europe Manufacturing Execution System Market Value Chain Analysis - Industry structure and value flow?

The MES value chain begins with core software development (vendor R&D), followed by system integration services, cloud infrastructure provision, and end‑user implementation. Post‑implementation, ongoing support, data analytics, and continuous improvement services add recurring revenue. Partnerships with ERP, IoT device manufacturers, and AI platform providers create synergistic value, while regulatory compliance consulting sits at the downstream end, ensuring that MES outputs meet EU standards.

15. Key Investment Insights in the Europe Manufacturing Execution System Market - Strategic investment recommendations?

Investors should prioritize companies with proven cloud‑MES capabilities and strong AI integration roadmaps, as these segments exhibit the fastest growth. Partnerships with ERP giants or IoT ecosystems enhance market reach and reduce customer acquisition costs. Acquisitions of niche process‑industry specialists can provide immediate access to regulated sectors. Finally, allocating capital to service‑oriented models (implementation, training, managed services) can generate stable, recurring cash flows amid the transition to subscription‑based licensing.

16. Europe Manufacturing Execution System Market Conclusion - Summary and key takeaways?

The European MES market is on a decisive growth path, expanding from €4.86 billion in 2026 to €10.60 billion by 2033 with an 11.79% CAGR. Digital transformation, regulatory compliance, and the shift to cloud and AI are the primary catalysts. While cost and skill gaps persist, the market offers substantial upside for providers that can deliver scalable, secure, and industry‑tailored solutions. The competitive arena is concentrated among eight leading firms, each pursuing consolidation and innovation to capture the expanding demand across process and discrete sectors.

17. Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, integrating primary interviews with industry executives, technology partners, and end‑user manufacturers, alongside secondary data from company reports, regulatory filings, and reputable market databases. Quantitative data were validated through triangulation, and forecast modeling used historical growth patterns adjusted for identified macro‑economic and technology drivers. Scenario analysis examined the impact of cloud adoption rates and regulatory changes on the projected CAGR.

18. Research Scope - Coverage and limitations?

The scope encompasses the European MES market across component, deployment, and industry‑type segments, covering the period 2025‑2032. It includes major manufacturers, technology providers, and service integrators operating within the EU and EFTA regions. The analysis does not extend to non‑European markets, nor does it quantify market share beyond the aggregate figures provided. All financial values strictly adhere to the supplied data points.

19. Key Companies and Recent Developments in the Europe Manufacturing Execution System Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent highlights include AVEVA’s launch of a cloud‑native MES platform that integrates with its engineering suite, Dassault Systèmes’ partnership with leading automotive OEMs to embed MES data into its 3DEXPERIENCE environment, Emerson’s acquisition of a process‑analytics start‑up to enhance real‑time quality monitoring, and GE’s rollout of Predix‑based MES for renewable‑energy facilities. Honeywell announced a joint venture with a European cybersecurity firm to fortify MES data protection. Oracle expanded its cloud MES offering with AI‑driven scheduling. Rockwell Automation introduced a modular MES add‑on for small‑batch discrete manufacturers, while SAP released an integrated MES‑ERP module optimized for the EU’s sustainability reporting requirements.