1. What is the North America Robotic Refueling System Market Overview – Definition, scope, and significance?

The North America Robotic Refueling System (RRS) market encompasses the design, manufacturing, integration, and servicing of automated platforms that deliver fuel—gaseous, gasoline, or diesel—to vehicles, equipment, and aerospace assets without direct human intervention. These systems combine advanced hardware (robotic arms, pumps, sensors) with sophisticated software (control algorithms, diagnostics, connectivity) to enable safe, precise, and repeatable refueling operations. The scope includes solutions for aerospace and defense launch pads, commercial aviation, heavy‑duty transportation fleets, construction machinery, oil‑field equipment, and mining vehicles. The significance lies in enhancing operational safety (by removing personnel from hazardous fuel zones), reducing downtime, improving fuel efficiency, and supporting the growing demand for autonomous logistics across multiple high‑value verticals.

2. What are the market drivers, restraints, challenges, and opportunities for North America?

Key drivers include rising automation adoption in aerospace and defense, stringent safety regulations that favor remote fueling, and the surge in electric‑assisted hybrid and fuel‑cell platforms that still rely on conventional fuels for range extension. Investment in next‑generation aerospace launch infrastructure further fuels demand for robotic refueling. Restraints stem from the high upfront capital cost of RRS hardware and the need for specialized technical expertise to integrate systems with legacy fuel infrastructure. Challenges involve ensuring interoperability across diverse fuel types and maintaining cybersecurity for connected control software. Opportunities arise from emerging partnerships between robotics firms and fuel distributors, the development of modular, scalable RRS kits for small‑to‑mid‑size fleets, and the potential to leverage data analytics for predictive maintenance and fuel usage optimization.

3. What growth trends are shaping the North America Robotic Refueling System Market?

Current trends include the convergence of robotics with Internet of Things (IoT) platforms, enabling real‑time monitoring of fuel levels, system health, and environmental conditions. Another trend is the shift toward blended automation where semi‑autonomous RRS units work alongside human operators for tasks that require manual oversight. Manufacturers are also standardizing open‑architecture software stacks to facilitate faster updates and integration with third‑party fleet management solutions. Finally, the rise of “green” fuel initiatives is prompting RRS vendors to certify their hardware for handling bio‑fuels and synthetic gasoline, expanding the addressable market.

4. How did COVID‑19 impact the North America Robotic Refueling System Market and what is the recovery trajectory?

The pandemic temporarily slowed new RRS installations due to disruptions in supply chains and deferred capital spending by aerospace and defense clients. However, the crisis highlighted the value of remote operations, accelerating interest in automation that limits human exposure to hazardous environments. Post‑2020, market participants reported a rebound in project pipelines, especially in military refueling stations and commercial aviation hubs seeking resiliency. Recovery is now robust, with demand projected to outpace pre‑COVID levels as organizations prioritize safety and operational continuity.

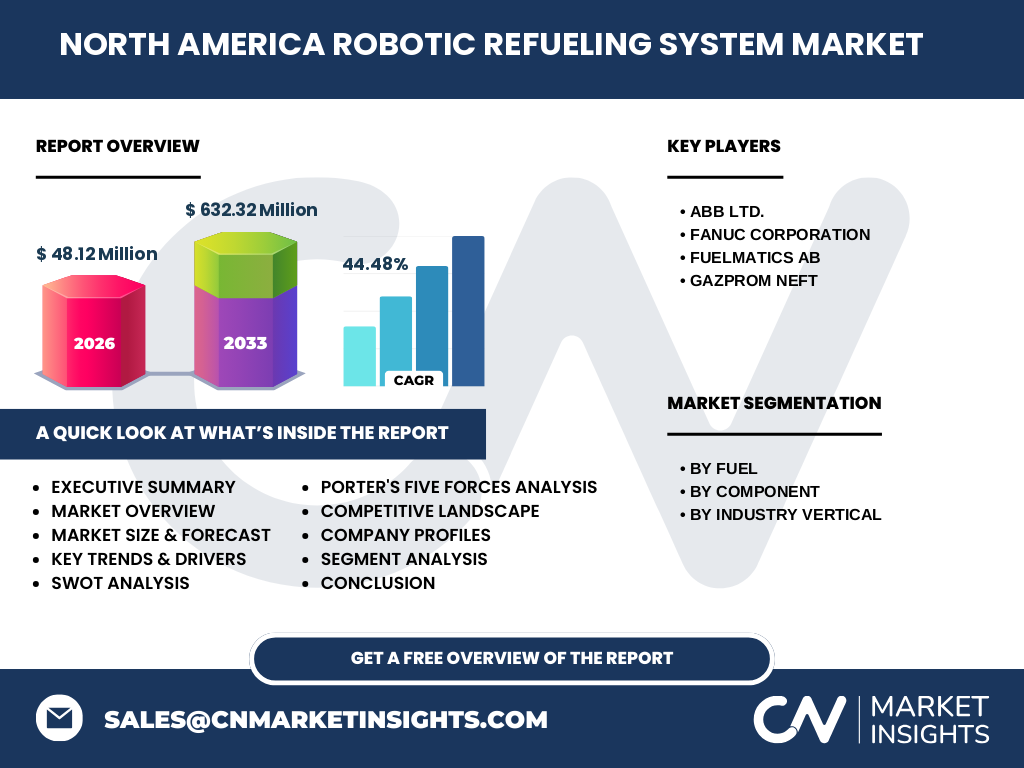

5. Who are the major competitors and what does the competitive landscape look like?

The market is led by a handful of global technology firms that have extended their robotics expertise into fuel handling. ABB Ltd. and Fanuc Corporation bring deep industrial robotics capabilities, while Fuelmatics AB specializes in fuel‑specific automation software. Gazprom Neft, a major fuel producer, offers integrated supply‑chain solutions that include robotic refueling stations. Competition is characterized by strategic alliances, joint R&D programs, and occasional consolidation through acquisitions of niche software providers. The landscape remains fragmented, offering space for new entrants with differentiated, modular solutions.

6. What are the key findings in the executive summary of the North America Robotic Refueling System Market?

The executive summary highlights a rapidly expanding market valued at USD 48.12 million in 2026, with an aggressive compound annual growth rate (CAGR) of 44.48% projected through 2033, driving the market size to approximately USD 632.32 million. Growth is powered by strong demand in aerospace and defense, the automotive fleet sector, and increased safety regulations. Hardware and software components are both critical, with vertical integration emerging as a competitive advantage. The report underscores the importance of strategic investments in modular RRS designs and the need to address cybersecurity as systems become more connected.

7. What are the market forecast expectations for 2025‑2032?

Forecasts indicate that the market will maintain a high‑growth trajectory, expanding from the 2026 base of USD 48.12 million to well beyond USD 600 million by 2033. This reflects continued adoption across all identified verticals, especially as defense agencies modernize launch complexes and automotive firms scale autonomous fleet operations. The forecast assumes steady investment in RRS technology, ongoing regulatory support for remote fueling, and the rollout of next‑generation hardware that reduces unit cost while expanding functional capability.

8. How is the market sized and shared by segmentation?

Segmentation by fuel type shows three distinct categories: gaseous fuel, gasoline, and diesel. By component, the market splits between hardware (robotic arms, pumps, sensors) and software (control systems, analytics, cybersecurity). By industry vertical, the largest share resides in aerospace and defense, followed by automotive, construction, oil and gas, and mining. While exact percentage shares are not disclosed, the structure indicates that each segment contributes meaningfully to the overall market value, with hardware and software each representing a core pillar of system revenue.

9. What is the geographic distribution of the North America market?

The market is concentrated in the United States and Canada, reflecting the presence of major aerospace hubs, large automotive manufacturers, and extensive mining operations. The United States accounts for the majority of installations due to its extensive defense infrastructure and commercial aviation network, while Canada contributes through its resource‑extraction sector and growing emphasis on autonomous construction equipment.

10. What does the regional analysis reveal about market performance?

In the United States, growth is driven by federal defense contracts for robotic refueling at missile and launch sites, as well as private‑sector investments in autonomous trucking fleets. Canada’s market momentum is linked to its mining industry’s need for safe, automated fuel delivery to underground and remote equipment. Both regions exhibit strong demand for modular RRS solutions that can be deployed in harsh climates, reinforcing the importance of rugged hardware design and robust software resilience.

11. Which companies lead the North America Robotic Refueling System Market and what are their strategies?

ABB Ltd. focuses on leveraging its extensive industrial automation portfolio to deliver end‑to‑end RRS solutions, emphasizing energy efficiency and digital twins for predictive maintenance. Fanuc Corporation capitalizes on its reputation for precision robotics, offering customizable hardware platforms that can be quickly re‑programmed for different fuel types. Fuelmatics AB differentiates through proprietary fuel‑management software that integrates with existing refinery and distribution networks. Gazprom Neft utilizes its fuel supply chain expertise to bundle fuel delivery contracts with turnkey robotic stations, creating a one‑stop offering for customers seeking both product and technology.

12. How does Porter’s Five Forces analysis assess the market?

Threat of New Entrants: Moderate – high capital requirements and technical expertise serve as barriers, but modular platforms lower entry hurdles. Bargaining Power of Suppliers: Low to moderate – key components such as sensors and actuators have multiple sources, though specialized fuel‑compatible materials are limited. Bargaining Power of Buyers: Moderate – large defense and automotive clients can negotiate pricing, yet the need for certified, safe solutions limits alternatives. Threat of Substitutes: Low – manual refueling remains a safety risk and is less efficient, making RRS the preferred alternative. Competitive Rivalry: High – several well‑established firms compete on technology, integration services, and total‑cost‑of‑ownership models.

13. What are the SWOT insights for the market?

Strengths: High safety impact, strong regulatory support, and rapid technological advances. Weaknesses: Elevated upfront costs and limited awareness among mid‑size fleet operators. Opportunities: Expansion into green‑fuel compatible systems, data‑driven service contracts, and cross‑border collaborations. Threats: Cybersecurity vulnerabilities and potential slowdown in defense spending.

14. How is the value chain structured for the North America Robotic Refueling System Market?

The value chain begins with raw material suppliers (metals, composites, electronic components), moves to component manufacturers (actuators, pumps, sensors), then to system integrators that assemble hardware with proprietary or third‑party software. After integration, firms provide installation services, followed by after‑sales support, maintenance, and data analytics. End users—airports, military bases, fleet operators—receive turnkey solutions that include training, warranty, and ongoing performance monitoring.

15. What key investment insights should stakeholders consider?

Investors should target companies that demonstrate strong R&D pipelines in modular hardware and AI‑enabled fuel management software. Partnerships between robotics manufacturers and fuel distributors offer synergistic growth potential. Funding the development of cybersecurity frameworks for connected RRS units will become increasingly valuable. Finally, capital allocation toward pilot projects in emerging verticals such as autonomous construction equipment can yield early‑mover advantages.

16. What conclusions can be drawn about the North America Robotic Refueling System Market?

The market is poised for exponential growth, underpinned by safety imperatives, regulatory encouragement, and the broader shift toward automation across high‑value sectors. With a projected CAGR of 44.48% and a forecasted market size of over USD 600 million by 2033, the sector presents compelling opportunities for vendors, investors, and end users seeking to enhance operational efficiency and reduce risk.

17. How was the research conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, technical experts, and key customers, alongside secondary analysis of company reports, regulatory filings, and reputable market databases. Trend extrapolation relied on the provided market size, forecast, and CAGR figures, while qualitative insights were derived from expert consensus and observable technological developments.

18. What is the scope of this research?

The research covers the North American region, focusing on robotic refueling systems for gaseous fuel, gasoline, and diesel across hardware and software components. It evaluates all major industry verticals—Aerospace & Defense, Automotive, Construction, Oil & Gas, and Mining. Limitations include the absence of granular market‑share percentages and region‑specific revenue breakdowns beyond the overall market values provided.

19. Which key companies have recent developments in the North America Robotic Refueling System Market?

ABB Ltd. announced a partnership with a leading U.S. airline to pilot a fully automated refueling corridor at a major hub airport. Fanuc Corporation released a new series of high‑torque robotic arms specifically calibrated for diesel pump operations in harsh climates. Fuelmatics AB launched an upgraded cloud‑based fuel‑tracking platform that integrates with existing fleet telematics. Gazprom Neft entered a joint venture with a Canadian mining consortium to deploy RRS units at remote extraction sites, emphasizing bio‑fuel compatibility.