What is the Choline Chloride Market Overview – definition, scope, and significance?

Choline chloride is a quaternary ammonium compound used primarily as a nutritional supplement, feed additive, and industrial chemical. The market encompasses the production, distribution, and application of choline chloride across three main end‑use industries: the feed industry, human nutrition, and the oil & gas sector. Its significance stems from its role in improving animal growth performance, supporting liver function in humans, and acting as a corrosion inhibitor and surfactant in drilling fluids. Growing awareness of animal welfare, rising demand for functional foods, and the need for environmentally friendly drilling additives drive its relevance worldwide.

What are the key drivers, restraints, challenges, and opportunities in the Choline Chloride Market?

Major drivers include expanding livestock populations, increasing consumption of protein‑rich diets, and heightened regulatory support for feed additives that enhance animal health. Opportunities arise from the development of certified organic and non‑GMO choline chloride variants, and from its application in biodegradable oil‑field chemicals. Restraints involve price volatility of raw materials such as ethylene oxide and regulatory hurdles in certain regions. Challenges include the need for stringent purity standards and competition from alternative nutrients like betaine and phosphatidylcholine.

What are the current growth trends shaping the Choline Chloride Market?

Current trends feature a shift toward high‑concentration liquid formulations that improve handling efficiency in feed mills. There is also a rising preference for sustainable production processes, including bio‑based synthesis routes. In the human nutrition segment, fortified beverages and functional foods incorporating choline chloride are gaining market traction. Moreover, the oil & gas industry is adopting greener drilling fluids, creating a niche for choline‑based additives.

How did COVID‑19 impact the Choline Chloride Market and what is the recovery trajectory?

The pandemic caused temporary disruptions in supply chains and reduced feed‑lot operations during lockdowns, leading to a short‑term dip in demand. However, rapid recovery followed as livestock production rebounded and consumer demand for protein‑rich foods intensified. Post‑COVID, the market has experienced accelerated adoption of digital procurement platforms, enhancing resilience and supporting a steady upward trajectory toward the forecast period.

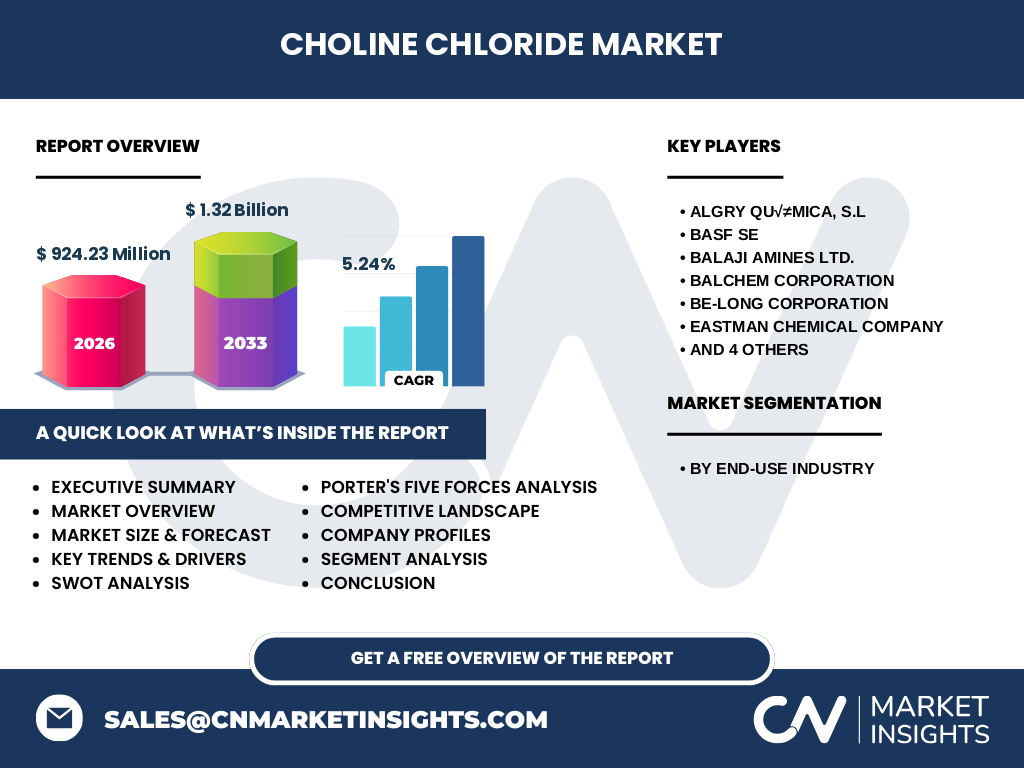

Who are the major competitors and what is the competitive landscape in the Choline Chloride Market?

The market is moderately consolidated with several global and regional players. Key competitors include Algry Química, S.L., BASF SE, Balaji Amines Ltd., Balchem Corporation, Be‑Long Corporation, Eastman Chemical Company, GHW Eurochemicals S.R.O., Jubilant Life Sciences Limited, NB Group Co., Ltd, and Pestell Minerals & Ingredients Inc. Companies compete on product purity, price, and value‑added services such as custom blending and technical support. Recent consolidation activity has focused on strategic acquisitions to expand geographic reach and broaden product portfolios.

What are the high‑level findings in the Executive Summary?

The Choline Chloride Market is valued at USD 924.23 million in 2026 and is projected to reach USD 1.32 billion by 2033, reflecting a CAGR of 5.24 % over the forecast horizon. Growth is propelled by robust demand in the feed industry, expanding applications in human nutrition, and emerging opportunities in oil & gas drilling fluids. Competitive dynamics are characterized by a mix of large multinational chemical firms and specialized niche producers. Sustainability and product innovation are the primary levers for future market expansion.

What are the market forecast expectations for 2025‑2032?

Based on the indicated CAGR of 5.24 %, the market is expected to maintain steady growth throughout the 2025‑2032 period, surpassing the USD 1 billion threshold by the early 2020s and approaching the USD 1.32 billion forecast for 2033. The feed segment will continue to dominate, while the human nutrition and oil & gas segments are anticipated to record higher growth rates due to functional‑food trends and greener drilling additive requirements.

How is the Choline Chloride Market sized and shared by end‑use segmentation?

The market is segmented into three primary end‑use categories. The feed industry commands the largest share, driven by its extensive use as a growth‑promoting additive in poultry, swine, and ruminant feeds. The human nutrition segment, encompassing dietary supplements and fortified foods, holds a smaller yet rapidly growing portion of the market. The oil & gas sector, while currently the smallest segment, is expected to expand as environmental regulations push for biodegradable drilling fluid components.

What is the geographic distribution of the Global Choline Chloride Market?

Geographically, the market is spread across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. North America and Europe lead in terms of demand from the feed and human nutrition sectors, whereas Asia‑Pacific demonstrates the fastest growth due to expanding livestock farms and rising disposable incomes. Emerging markets in Latin America and the Middle East are beginning to invest in modern feed formulations, adding to regional diversification.

Can you provide a detailed regional analysis of the Choline Chloride Market?

In North America, stringent feed‑regulation frameworks and a mature livestock industry underpin stable demand. Europe benefits from advanced animal health standards and increasing consumer focus on functional foods. Asia‑Pacific shows the strongest growth momentum, driven by China, India, and Southeast Asian nations expanding their animal‑protein production capacity. Latin America’s growth is linked to large cattle operations and a growing poultry sector. The Middle East & Africa present niche opportunities, particularly in countries investing in modern agricultural practices and offshore drilling projects.

What are the profiles and strategies of leading companies in the Choline Chloride Market?

Leading firms such as BASF SE and Eastman Chemical Company leverage extensive R&D capabilities to develop high‑purity grades and specialty blends. Balchem Corporation focuses on integrated supply‑chain solutions for the feed sector. Algry Química, S.L. emphasizes cost‑competitive production in the Iberian market. Jubilant Life Sciences and Balaji Amines pursue geographic expansion through joint ventures and acquisitions. Overall, strategies revolve around product differentiation, strategic partnerships, and capacity expansion to meet rising demand.

How does Porter’s Five Forces framework assess the Choline Chloride Market?

Threat of new entrants is moderate; high capital investment and regulatory compliance create barriers. Bargaining power of suppliers is moderate, as raw‑material availability (e.g., ethylene oxide) can affect pricing. Bargaining power of buyers is relatively high in the feed segment due to large, consolidated feed‑mill operators seeking price competitiveness. Threat of substitutes is low to moderate, with alternatives like betaine gaining niche traction but not overtaking choline chloride. Industry rivalry is high, driven by a handful of well‑established players competing on price, purity, and service.

What are the SWOT insights for the Choline Chloride Market?

Strengths: Proven efficacy in animal growth, essential nutrient status for humans, and versatile industrial applications. Weaknesses: Dependence on petrochemical feedstocks and sensitivity to raw‑material cost fluctuations. Opportunities: Development of bio‑based production routes, expansion into organic feed markets, and increased use in eco‑friendly drilling fluids. Threats: Regulatory changes limiting certain additives, potential supply disruptions, and competition from emerging nutrient alternatives.

How is the Choline Chloride value chain structured?

The value chain begins with raw‑material procurement (ethylene oxide, trimethylamine), followed by synthesis, purification, and formulation into liquid or solid products. Distribution channels include direct sales to large feed manufacturers, distributors serving the food‑ingredient sector, and specialized suppliers for oil‑field chemicals. End‑users—livestock producers, food manufacturers, and drilling contractors—receive the product for incorporation into feeds, supplements, or drilling fluids. Supporting services such as technical assistance, regulatory compliance support, and logistics play a critical role in value creation.

What key investment insights can be drawn for the Choline Chloride Market?

Investors should focus on companies that are expanding production capacity in regions with strong feed‑industry growth, especially Asia‑Pacific. Firms investing in sustainable synthesis technologies are likely to gain competitive advantage as environmental standards tighten. Partnerships with agricultural cooperatives or oil‑field service providers can unlock new revenue streams. Monitoring regulatory trends will be essential to mitigate risks associated with additive approvals.

What are the main conclusions of the Choline Chloride Market report?

The market is on a solid growth trajectory, underpinned by consistent demand from the feed sector and emerging applications in human nutrition and oil & gas. With a projected CAGR of 5.24 % and a market size surpassing the USD 1 billion mark by the early 2030s, opportunities abound for innovators and investors. Success will depend on delivering high‑purity products, embracing sustainable production, and navigating regional regulatory landscapes.

What research methodology was employed in this study?

The analysis combined primary interviews with industry experts, secondary data extraction from company reports, trade publications, and governmental statistics. Market sizing used a bottom‑up approach, aggregating production volumes and pricing information from key players. Forecasting employed compound annual growth rate calculations based on historical trends and forward‑looking drivers identified during the research.

What is the scope of the research and its limitations?

The study covers global choline chloride production, end‑use segmentation, and regional performance up to 2033. While it incorporates the most recent publicly available data, the analysis does not account for confidential pricing agreements or undisclosed R&D pipelines. Geographic granularity is limited to major regions, and sub‑regional nuances are not exhaustively detailed.

Who are the key companies and what recent developments have they announced?

Key players include Algry Química, S.L., BASF SE, Balaji Amines Ltd., Balchem Corporation, Be‑Long Corporation, Eastman Chemical Company, GHW Eurochemicals S.R.O., Jubilant Life Sciences Limited, NB Group Co., Ltd, and Pestell Minerals & Ingredients Inc. Recent developments feature BASF’s launch of a high‑purity liquid choline chloride for dairy feed, Eastman’s partnership with an Asian nutraceutical firm to create fortified beverages, and Balchem’s expansion of its production facility in the United States to meet rising demand. Several companies have also announced sustainability initiatives aimed at reducing the carbon footprint of their manufacturing processes.