1. What is the North America Hereditary Cancer Testing Market Overview – Definition, scope, and significance?

The North America Hereditary Cancer Testing Market encompasses all diagnostic services and technologies used to identify genetic mutations that predispose individuals to cancer. The scope includes testing performed in hospitals, clinics, and diagnostic centers using sequencing, PCR, and microarray platforms for both biopsy and imaging‑based diagnosis. Its significance lies in enabling personalized preventive care, guiding targeted therapies, and reducing long‑term treatment costs by detecting high‑risk patients early.

2. What are the market drivers, restraints, challenges, and opportunities?

Key drivers include rising awareness of genetic risk, expanding insurance coverage, and advances in next‑generation sequencing that lower costs. Restraints stem from high upfront equipment investment and regulatory complexities. Challenges involve data privacy concerns and limited reimbursement for some test types. Opportunities arise from emerging multi‑gene panels, integration of AI for result interpretation, and growing demand for companion diagnostics linked to targeted oncology drugs.

3. What are the current growth trends shaping the market?

Current trends feature a shift toward comprehensive panel testing over single‑gene assays, increased adoption of liquid biopsy techniques, and partnerships between diagnostic firms and pharmaceutical companies for trial enrollment. Additionally, there is a notable rise in direct‑to‑consumer genetic testing, driving broader market awareness and prompting clinical laboratories to expand service portfolios.

4. How has COVID‑19 impacted the market and what is the recovery trajectory?

The pandemic caused a temporary dip in elective testing volumes, but accelerated telehealth adoption and remote sample collection services. Post‑2022, demand rebounded strongly as healthcare systems prioritized preventive screening. The recovery trajectory is upward, supported by pent‑up demand and renewed focus on early detection, positioning the market for sustained growth.

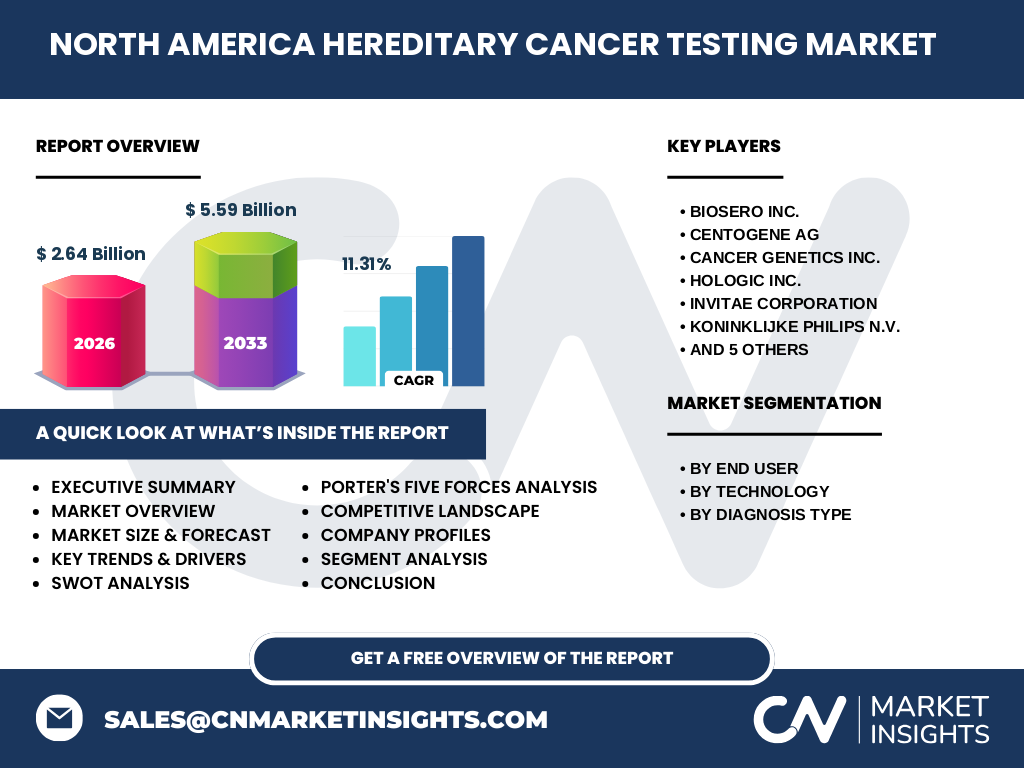

5. Who are the major competitors and what is the state of market consolidation?

Leading players include Biosero Inc., CENTOGENE AG, Cancer Genetics Inc., Hologic Inc., Invitae Corporation, Koninklijke Philips N.V., Myogenes, Myriad Genetics, Inc., Pathway Genomics Corporation, Quest Diagnostics Incorporated, and Strand Life Sciences Pvt. Ltd. The competitive landscape is characterized by strategic alliances, technology licensing, and selective acquisitions, leading to moderate consolidation focused on expanding test menus and geographic reach.

6. What are the high‑level findings in the executive summary?

The market is valued at US$2.64 billion in 2026 and is projected to reach US$5.59 billion by 2033, reflecting an 11.31 % CAGR. Growth is driven by expanding genetic testing awareness, technological innovation, and supportive reimbursement policies. Hospital and diagnostic‑center segments dominate usage, while sequencing holds the largest technology share. The market remains attractive for investors seeking exposure to precision oncology.

7. What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 11.31 %, the market is expected to maintain robust double‑digit expansion through 2032. This continued growth will be fueled by broader adoption of multi‑gene panels, integration of testing into routine oncology pathways, and increased utilization of AI‑driven analytics for result interpretation.

8. How is the market sized and shared by segmentation?

By end user, hospitals lead the market, followed by clinics and diagnostic centers. In technology terms, sequencing commands the largest share, with PCR and microarray serving niche applications. Regarding diagnosis type, biopsy‑based testing remains predominant, while imaging‑linked genetic analysis is an emerging complementary segment.

9. What is the geographic distribution of the market within North America?

The market is concentrated in the United States, which accounts for the majority of revenue due to its extensive healthcare infrastructure and favorable reimbursement environment. Canada contributes a smaller yet growing share, driven by provincial health programs that increasingly cover hereditary cancer tests.

10. What are the regional performance insights?

In the United States, adoption is accelerated by large integrated health systems and robust research networks. The western region shows higher uptake of advanced sequencing platforms, while the eastern corridor leads in clinical trial enrollment that relies on genetic testing. Canada’s market growth is propelled by provincial initiatives to integrate hereditary testing into standard cancer screening protocols.

11. Which companies are leading and what are their key strategies?

Invitae Corporation expands its portfolio through acquisitions of niche panel developers. Myriad Genetics focuses on proprietary biomarkers and companion‑diagnostic collaborations. Quest Diagnostics leverages its nationwide laboratory network to increase test accessibility. Hologic invests in automated PCR solutions, while Philips emphasizes integrated imaging‑genomics platforms. These strategies underline a mix of organic innovation and strategic partnerships.

12. What does Porter’s Five Forces reveal about the market?

• Bargaining power of buyers: Moderate, as large health systems negotiate volume discounts. • Bargaining power of suppliers: Low to moderate, given multiple reagent and instrument providers. • Threat of new entrants: Moderate, due to high capital and regulatory barriers. • Threat of substitutes: Low, because genetic testing is uniquely positioned for hereditary risk assessment. • Competitive rivalry: High, driven by rapid innovation and portfolio diversification.

13. What are the SWOT highlights?

Strengths: Strong clinical demand and clear evidence of cost‑effectiveness. Weaknesses: High upfront technology costs. Opportunities: Expansion into multi‑ethnic panels and digital health integrations. Threats: Potential regulatory tightening and data‑privacy legislations that could slow adoption.

14. How does the value chain of the market operate?

The value chain begins with research‑grade sample collection, followed by DNA extraction, assay preparation (sequencing, PCR, or microarray), data generation, bioinformatics analysis, clinical interpretation, and finally reporting to physicians. Supporting services include logistics, quality assurance, and reimbursement processing, each adding incremental value and cost.

15. What are the key investment insights?

Investors should target companies with scalable sequencing platforms, robust reimbursement pipelines, and strategic partnerships with pharma. Firms expanding into AI‑driven analytics or offering bundled testing services across hospitals and diagnostic centers present attractive upside. Monitoring regulatory developments and reimbursement policy changes will be critical for risk mitigation.

16. What is the overall conclusion of the market analysis?

The North America Hereditary Cancer Testing Market is on a strong growth trajectory, underpinned by technological advances and escalating demand for personalized cancer care. With a projected market size of US$5.59 billion by 2033, the sector offers substantial opportunities for players that can innovate, scale, and navigate the evolving regulatory landscape.

17. How was the research methodology designed?

The study combined secondary data from industry reports, company filings, and peer‑reviewed literature with primary interviews of key opinion leaders in oncology and diagnostics. Market sizing employed a top‑down approach anchored on known 2026 revenue, while forecasting applied the stated 11.31 % CAGR. Validation involved cross‑checking with multiple independent sources.

18. What is the scope of the research?

The research covers all hereditary cancer diagnostic services offered in North America, segmented by end user, technology, and diagnosis type. It excludes non‑hereditary oncology testing, therapeutic drug development, and markets outside of North America. The analysis focuses on the period 2025‑2032, using the provided financial figures as the baseline.

19. Which key companies have recent developments and what are they?

Invitae announced the launch of a 30‑gene hereditary cancer panel and a partnership with a major insurer for coverage expansion. Myriad Genetics introduced an AI‑enhanced report workflow that shortens turnaround time. Quest Diagnostics reported the acquisition of a boutique microarray firm to broaden its test menu. Hologic unveiled a fully automated PCR system aimed at point‑of‑care settings, while Philips integrated its imaging suite with genomic analytics for seamless radiogenomic reporting.