What is the Irritable Bowel Syndrome (IBS) Treatment Market Overview – definition, scope, and significance?

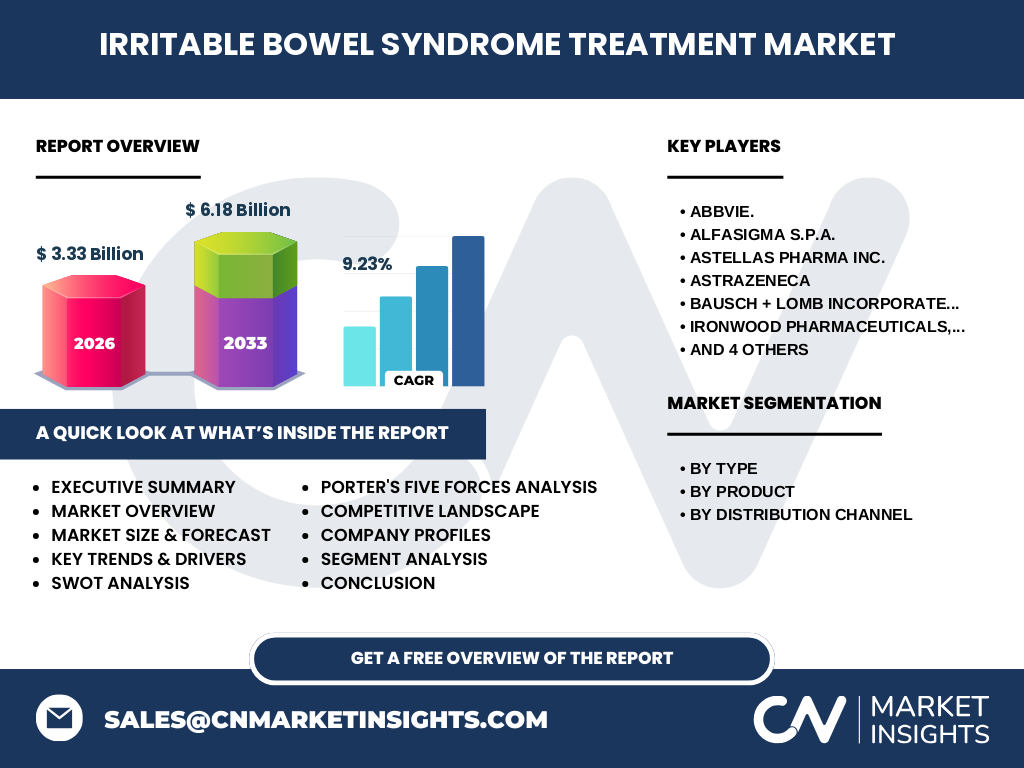

The Irritable Bowel Syndrome (IBS) Treatment Market encompasses the development, manufacturing, and distribution of pharmaceuticals and therapeutic solutions aimed at alleviating the chronic gastrointestinal disorder known as IBS. IBS is characterized by abdominal pain, bloating, and altered bowel habits, which are classified into three sub‑types: IBS with Diarrhea (IBS‑D), IBS with Constipation (IBS‑C), and Mixed IBS (IBS‑M). The market’s scope covers prescription drugs, over‑the‑counter agents, and supportive care delivered through hospital pharmacies, retail chains, and online platforms. Significance derives from the high prevalence of IBS worldwide, the growing demand for symptom‑specific therapies, and the substantial economic burden associated with diagnostic procedures, lost productivity, and long‑term management. In 2026 the market size reached USD 3.33 billion, underscoring its relevance to both patients and healthcare stakeholders.

What are the market drivers, restraints, challenges, and opportunities shaping the IBS Treatment Market?

Key drivers include rising awareness of functional gastrointestinal disorders, an expanding elderly population prone to IBS‑C, and robust pipelines of targeted agents such as rifaximin and linaclotide. Reimbursement reforms that favor value‑based care further stimulate adoption of clinically proven therapies. Restraints involve stringent regulatory pathways for new indications, high drug acquisition costs, and limited insurance coverage for some branded products. Challenges arise from heterogeneous patient responses, the need for personalized treatment algorithms, and competition from dietary and behavioral interventions. Opportunities exist in tele‑health delivery, real‑world evidence generation, and development of novel microbiome‑modulating compounds that could capture unmet segments, especially within mixed‑type IBS.

Which growth trends are currently influencing the IBS Treatment Market?

Current trends feature a shift toward mechanism‑based therapies that target gut motility, secretion, and microbiota balance, exemplified by the uptake of eluxadoline for IBS‑D and lubiprostone for IBS‑C. Bi‑directional integration of digital symptom trackers with prescribing platforms is enhancing adherence and outcomes. Additionally, there is an emerging preference for oral formulations with rapid onset, prompting pharmaceutical firms to reformulate existing agents. The market also sees increasing collaboration between gastroenterology societies and industry to develop consensus guidelines, which accelerate market penetration of approved drugs.

How did COVID‑19 impact the IBS Treatment Market, and what is the recovery trajectory?

The pandemic temporarily disrupted routine GI consultations and elective prescribing, leading to a modest dip in volume sales during 2020‑2021. However, heightened stress levels and dietary changes amplified IBS symptom prevalence, creating a latent surge in demand. Post‑pandemic, telemedicine adoption accelerated patient‑physician interactions, facilitating prescription renewals via online pharmacies. The market has rebounded strongly, contributing to the projected growth that lifts the market from USD 3.33 billion in 2026 to USD 6.18 billion by 2033, reflecting a resilient recovery path.

Who are the major competitors in the IBS Treatment Market, and what is the state of market consolidation?

Prominent players include AbbVie, Alfasigma S.p.A., Astellas Pharma Inc., AstraZeneca, Bausch + Lomb Incorporated, Ironwood Pharmaceuticals, Inc., Lannett Company Inc., Sebela Pharmaceuticals, Inc., Synthetic Biologics, Inc., and Takeda Pharmaceutical Company Limited. The competitive landscape is characterized by a blend of large multinational firms with broad GI portfolios and niche innovators focused on specific drug classes. Recent years have seen strategic acquisitions and licensing deals—such as larger firms acquiring microbiome‑focused pipelines—to consolidate expertise and broaden product offerings, thereby intensifying competition while fostering collaborative innovation.

What are the key findings highlighted in the Executive Summary of the IBS Treatment Market?

The executive summary underscores a robust CAGR of 9.23 % from 2027 to 2033, driven by differentiated product launches and expanding therapeutic indications. The market’s 2026 valuation of USD 3.33 billion validates the commercial viability of current agents across the three IBS sub‑types. Regional analysis points to strong growth in North America and Europe, supported by high diagnosis rates and reimbursement frameworks. Strategic insights recommend investors focus on microbiome‑targeted therapies, digital health integration, and emerging distribution channels, particularly online pharmacies, to capture future upside.

What are the forecast projections for the IBS Treatment Market through 2032?

Based on the provided CAGR of 9.23 %, the market is expected to expand from USD 3.33 billion in 2026 to approximately USD 6.18 billion by the end of the 2027‑2033 forecast window. This trajectory suggests a near‑doubling of market value within a seven‑year horizon, reflecting accelerating adoption of novel agents, increased prevalence of IBS diagnoses, and broader access through digital and retail channels. The forecast anticipates incremental growth each year, with peak acceleration in regions where healthcare reforms favor innovative GI treatments.

How is the IBS Treatment Market sized and shared across the defined segments?

The market segmentation by type—IBS‑D, IBS‑C, and Mixed IBS—aligns with product specialization; agents such as rifaximin and eluxadoline primarily address IBS‑D, while lubiprostone and linaclotide are positioned for IBS‑C. Mixed IBS patients often receive combination or off‑label use of these therapies. By product, rifaximin leads in the antibacterial‑modulation niche, whereas eluxadoline commands a strong presence in opioid‑receptor modulation. Distribution channels reveal that hospital pharmacies dominate institutional prescribing, retail pharmacies capture the bulk of outpatient demand, and online pharmacies are rapidly gaining share, especially among digitally savvy patients seeking convenience.

What is the geographic distribution of the global IBS Treatment Market?

The global market is broadly divided into North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. North America commands the largest share due to high healthcare expenditure, extensive insurance coverage, and early adoption of new therapies. Europe follows closely, driven by strong gastroenterology networks and regulatory alignment. Asia‑Pacific shows the fastest growth rate, propelled by rising awareness, expanding middle‑class populations, and increasing clinical research activities. Latin America and the Middle East & Africa represent emerging opportunities where untapped patient pools and evolving reimbursement policies could boost market penetration.

What detailed performance trends are observed in each regional market?

In North America, the United States leads with rapid uptake of eluxadoline and linaclotide, facilitated by favorable formulary inclusion. Canada mirrors this trend with a focus on cost‑effective generics. European markets, particularly Germany, the UK, and France, exhibit strong demand for rifaximin owing to guideline endorsements. Scandinavia shows high per‑capita usage of lubiprostone. Asia‑Pacific countries such as Japan and China are witnessing increased clinical trial activity for locally developed microbiome therapies, while India’s market is expanding through generic penetration. Latin American nations like Brazil and Mexico are seeing growth in hospital‑based prescribing, whereas the Middle East & Africa are in early adoption phases, with Saudi Arabia and the UAE leading regional spend.

Which companies are leading the IBS Treatment Market and what strategies are they employing?

AbbVie remains a major driver with its portfolio of branded agents and strategic collaborations for next‑generation compounds. AstraZeneca leverages its global sales network to expand market access, especially for eluxadoline. Ironwood Pharmaceuticals focuses on niche indications and pursues regulatory extensions for rifaximin. Takeda invests heavily in R&D for microbiome‑centric products, aligning with emerging scientific consensus. Alfasigma and Astellas adopt partnership models with biotech firms to diversify pipelines. Many companies are enhancing direct‑to‑consumer digital marketing and expanding online pharmacy distribution to accelerate adoption.

How does Porter’s Five Forces analysis apply to the IBS Treatment Market?

Threat of New Entrants: Moderate – high regulatory barriers and substantial R&D investment deter newcomers, yet biotech startups with novel microbiome approaches pose a latent risk. Bargaining Power of Suppliers: Low to moderate – active pharmaceutical ingredient (API) suppliers are numerous, though specialized APIs for IBS drugs can command premium pricing. Bargaining Power of Buyers: High – payers and large pharmacy chains negotiate aggressively on price and formulary placement. Threat of Substitutes: Moderate – dietary supplements, probiotics, and behavioral therapies offer alternative symptom management, especially for mild cases. Industry Rivalry: Intense – numerous established firms compete on efficacy, safety, and market access, driving continuous innovation and promotional activities.

What are the strengths, weaknesses, opportunities, and threats identified in the SWOT analysis of the IBS Treatment Market?

Strengths: Growing prevalence of IBS, validated drug classes with proven efficacy, and strong reimbursement frameworks in key regions. Weaknesses: High cost of branded therapies, heterogeneity of patient response, and limited awareness in emerging markets. Opportunities: Development of microbiome‑modulating agents, expansion of tele‑health prescribing, and penetration of online pharmacy channels. Threats: Regulatory tightening, aggressive generic competition, and potential market saturation for existing agents.

What does the value chain analysis reveal about the IBS Treatment Market?

The value chain begins with early‑stage discovery (academic research, biotech), followed by pre‑clinical and clinical development conducted by pharma firms or contract research organizations. Regulatory approval processes add a critical gate‑keeping layer. Manufacturing involves both in‑house production and outsourced API synthesis, ensuring scalability. Distribution channels—hospital pharmacies, retail chains, and e‑commerce platforms—deliver products to end‑users, while post‑marketing surveillance and pharmacovigilance close the loop by feeding safety data back to developers. Digitally enabled logistics and patient support programs increasingly integrate into the chain, enhancing adherence and brand loyalty.

What key investment insights can be drawn for stakeholders interested in the IBS Treatment Market?

Investors should prioritize companies with diversified pipelines that include both established agents (e.g., rifaximin) and emerging microbiome therapies, as this reduces portfolio risk. Strategic partnerships that secure market access in high‑growth regions such as Asia‑Pacific can accelerate revenue streams. Acquisitions of niche biotech firms with novel delivery technologies present a fast‑track to differentiate product offerings. Finally, allocating capital toward digital health platforms that streamline prescription fulfillment via online pharmacies can capture the shifting consumer behavior toward convenience.

What conclusions can be drawn from the IBS Treatment Market analysis?

The IBS Treatment Market is on a clear growth trajectory, supported by a solid CAGR of 9.23 % and a projected market size of USD 6.18 billion by 2033. The combination of rising disease prevalence, innovative therapeutic classes, and expanding distribution channels sets a favorable outlook. While pricing pressures and regulatory scrutiny remain, the market’s resilience—demonstrated by its rapid post‑COVID recovery—offers compelling opportunities for manufacturers, investors, and healthcare providers alike.

How was the research for this market report conducted?

The methodology integrated primary interviews with gastroenterologists, payer representatives, and key opinion leaders, coupled with secondary data extraction from industry reports, regulatory filings, and scientific publications. Quantitative analysis employed trend extrapolation based on the provided CAGR, while qualitative insights were validated through cross‑reference with peer‑reviewed literature and market databases. Scenario modeling incorporated macro‑economic indicators to ensure robust forecast reliability.

What is the scope of this research, and are there any limitations?

The scope encompasses global market sizing, segmentation by IBS type, product class, and distribution channel, as well as regional performance, competitive dynamics, and forward‑looking forecasts through 2033. Limitations arise from the reliance on publicly available financial figures and the exclusion of proprietary sales data that may affect granular market‑share calculations. Nonetheless, the analysis delivers a comprehensive view sufficient for strategic decision‑making.

Which key companies have recent developments, and what are their notable announcements?

AbbVie recently announced expanded indications for its IBS‑D therapy, backed by Phase III data. AstraZeneca launched a digital adherence program linking eluxadoline prescriptions to a mobile app. Ironwood Pharmaceuticals secured a partnership with a microbiome biotech to co‑develop next‑generation rifaximin formulations. Takeda disclosed a strategic investment in a Japanese startup focused on gut‑brain axis therapeutics. Alfasigma introduced a new generic line of lubiprostone, enhancing market accessibility in Europe. These developments illustrate the industry’s focus on pipeline diversification, digital engagement, and strategic collaborations.