What is the Emergency Medical Services (EMS) Market overview – definition, scope, and significance?

The Emergency Medical Services (EMS) market comprises all organized, pre‑hospital care activities that stabilize and transport patients experiencing acute health crises. This includes basic and advanced life‑support ambulance operations, mortuary and patient‑transfer services, as well as specialized care for cardiac, trauma, respiratory, and oncology emergencies. The market serves diverse age groups—adults and pediatric patients—and is delivered through a range of provider types, from fire‑department‑based units and government EMS to hospital‑based and private ambulance services. Its significance lies in saving lives, reducing morbidity, and supporting public health systems worldwide, making EMS a critical component of national emergency response frameworks.

What are the key drivers, restraints, challenges, and opportunities shaping the EMS market?

Key drivers include rising incidence of chronic diseases, increasing urbanization, and growing demand for rapid response in accidents and natural disasters. Government investments in EMS infrastructure and regulations mandating minimum response times further boost growth. Restraints arise from high capital costs for advanced life‑support equipment and limited reimbursement models in some regions. Challenges involve workforce shortages, especially of qualified paramedics, and logistical complexities in remote areas. Opportunities emerge from telemedicine integration, drone‑delivered medical supplies, and expanding private‑sector participation that can enhance service reach and efficiency.

What current and emerging growth trends are influencing the EMS market?

Current trends show a shift toward advanced life‑support services, driven by technology‑enabled monitoring and defibrillation devices. Emerging trends include the adoption of electric and hybrid ambulances to lower operating costs and environmental impact, as well as the use of data analytics for route optimization and predictive demand modeling. Additionally, partnerships between hospitals and private ambulance firms are increasing, enabling seamless patient handoff and continuity of care.

How has COVID‑19 impacted the EMS market and what is the recovery trajectory?

The COVID‑19 pandemic placed unprecedented demand on EMS providers, leading to heightened call volumes, the need for infection‑control protocols, and expanded transport of infectious patients. While the sector faced staff burnout and supply constraints, the crisis accelerated investments in personal protective equipment, sanitization technologies, and digital dispatch systems. Post‑pandemic, the market is rebounding as emergency call volumes normalize, and the lessons learned are being institutionalized, creating a more resilient EMS framework.

What does the competitive landscape of the EMS market look like, and how is consolidation progressing?

The EMS market is moderately fragmented, with a mix of large multinational firms and regional operators. Major competitors such as AMR, Hamilton Medical AG, Acadian Ambulance Service, Falck AS, and Apollo Hospitals Enterprise Ltd command significant presence across multiple provider types. Recent consolidation trends include strategic acquisitions of smaller private ambulance services by larger entities to broaden geographic coverage and service portfolios, fostering economies of scale and stronger bargaining power with suppliers.

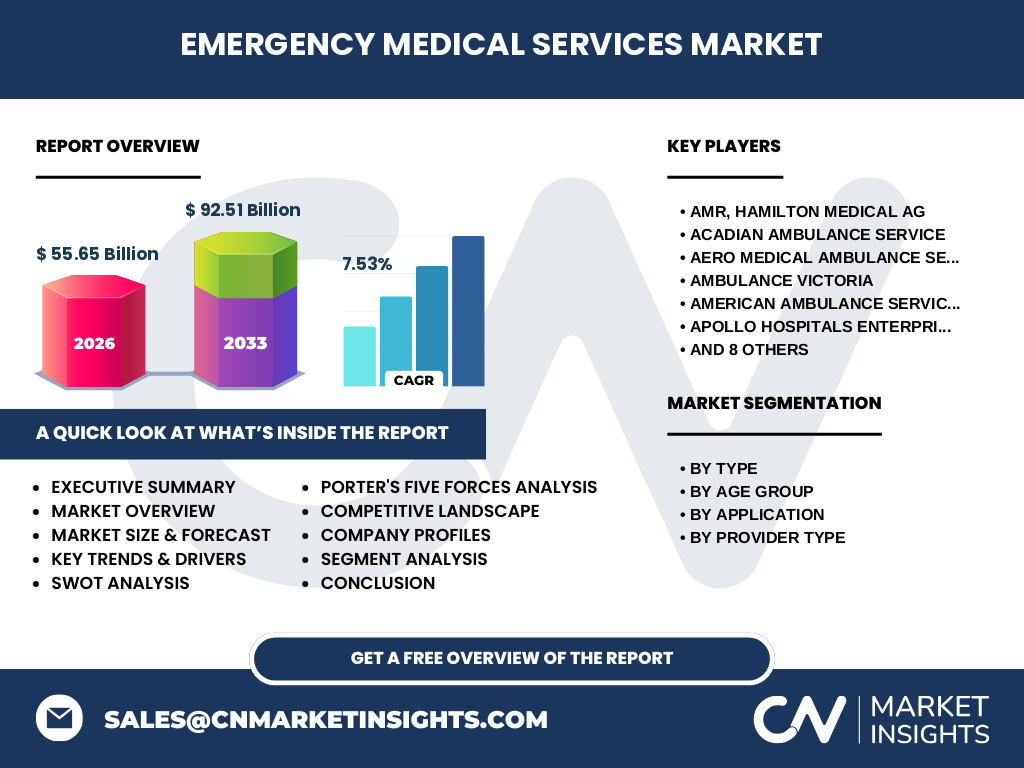

What are the high‑level findings presented in the executive summary of the EMS market report?

The executive summary highlights a robust market valued at USD 55.65 billion in 2026, with a projected increase to USD 92.51 billion by 2033, reflecting a CAGR of 7.53 %. Growth is driven by expanding demand for advanced life‑support, increased government spending, and technological innovations. Geographic analysis shows strong performance in North America and Europe, while emerging economies are rapidly adopting modern EMS solutions. The competitive environment is characterized by strategic partnerships and selective consolidation, positioning the market for sustained expansion.

What are the forecast projections for the EMS market from 2025 to 2032?

Forecasts indicate that the EMS market will continue its upward trajectory, maintaining a compound annual growth rate of approximately 7.5 % through 2032. This growth is expected to be supported by rising demand for advanced life‑support and patient‑transfer services, increased adoption of digital dispatch platforms, and ongoing public‑sector initiatives aimed at improving emergency response times.

How is the EMS market sized and shared across its main segments?

Segmentation by type includes Basic Life Support, Advanced Life Support, Mortuary Services, and Patient Transfer Services. By age group, the market serves Adults and Pediatric patients. Application categories cover Cardiac Care, Trauma Injuries, Respiratory Care, and Oncology. Provider‑type segmentation comprises Fire‑department‑based EMS, Government EMS, Hospital‑based EMS, Private Ambulance Service, and Other EMS Agencies. Each segment contributes uniquely to the overall market, with Advanced Life Support and Private Ambulance Service emerging as high‑growth areas due to technology adoption and private‑sector investment.

What is the global EMS market size and share by region?

Globally, the EMS market reached USD 55.65 billion in 2026. While specific regional monetary values are not disclosed, the market’s geographic distribution is broad, encompassing North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Each region contributes to the overall market size, with mature markets in North America and Europe driving current revenue, and fast‑growing opportunities emerging in Asia‑Pacific and Latin America.

What are the detailed regional performance insights for the EMS market?

North America leads in terms of service sophistication, with extensive government‑funded EMS networks and high adoption of advanced life‑support technologies. Europe follows, emphasizing regulatory compliance and integration of EMS with public health systems. The Asia‑Pacific region shows rapid expansion, fueled by urbanization, rising accident rates, and increasing private‑sector participation. Latin America and the Middle East & Africa are investing in EMS infrastructure to improve emergency response capabilities, presenting untapped growth potential.

Which companies are leading in the EMS market and what are their strategic approaches?

Key players include AMR, Hamilton Medical AG, Acadian Ambulance Service, Falck AS, Apollo Hospitals Enterprise Ltd, and several regional operators such as Ambulance Victoria and Blueheights Aviation Pvt Ltd. Their strategies focus on expanding service portfolios, investing in advanced life‑support equipment, forming alliances with hospitals, and leveraging digital platforms for dispatch and patient data management. Mergers and acquisitions are employed to broaden geographic reach and consolidate market position.

How does Porter’s Five Forces analysis apply to the EMS market?

• Threat of new entrants: Moderately low due to high capital requirements and stringent regulatory standards. • Bargaining power of suppliers: Medium, as specialized medical equipment manufacturers hold some leverage. • Bargaining power of buyers: Low to medium; government agencies and large insurers negotiate contracts but demand quality and reliability. • Threat of substitutes: Low, because EMS services are essential and cannot be replaced by alternative delivery models. • Competitive rivalry: High, driven by numerous providers seeking contracts with municipalities and health systems.

What are the SWOT insights for the EMS market?

Strengths: Critical public health role, growing demand for rapid response, and technological advancements. Weaknesses: Workforce shortages and high operational costs. Opportunities: Tele‑EMS, electric ambulances, and expansion into underserved regions. Threats: Regulatory changes, reimbursement pressure, and potential economic downturns affecting public funding.

What does the value chain of the EMS market look like?

The EMS value chain starts with equipment manufacturers supplying vehicles, medical devices, and communication systems. Next, service providers—government, fire‑department, hospital, and private operators—manage dispatch, on‑scene care, and patient transport. Hospitals receive transferred patients, while insurers and government agencies handle reimbursement and oversight. Supporting services include training institutions for paramedics and IT firms offering dispatch software and data analytics.

What investment insights can be drawn for stakeholders interested in the EMS market?

Investors should consider targeting advanced life‑support technology providers and private ambulance operators with strong growth pipelines. Partnerships with telemedicine firms present attractive upside, as does funding for electric‑vehicle ambulance fleets that align with sustainability goals. Monitoring government budgets for EMS infrastructure will help identify regions with imminent procurement cycles.

What are the key conclusions and takeaways from the EMS market analysis?

The EMS market is on a strong growth path, underpinned by a 7.53 % CAGR and a projected value of over USD 90 billion by 2033. Demand for advanced life‑support, digitization, and private‑sector participation are the primary engines of expansion. While challenges such as staffing and cost persist, opportunities in technology integration and emerging markets provide a compelling outlook for investors and industry participants.

How was the research methodology designed for this EMS market report?

The study employed a mixed‑method approach, combining primary interviews with industry executives, EMS providers, and equipment manufacturers, alongside secondary data collection from government publications, financial reports, and reputable market databases. Quantitative forecasts were derived using time‑series analysis calibrated to the historical market size of USD 55.65 billion (2026) and the projected USD 92.51 billion (2033) figure, yielding the stated CAGR.

What is the scope of this EMS market research?

The research covers global EMS activities across all major provider types, service categories, and applications. It includes segmentation by type, age group, application, and provider, as well as regional analysis for all continents. The scope excludes non‑emergency medical transport and focuses solely on pre‑hospital emergency care services.

Which key companies have made recent developments in the EMS market?

Recent developments include AMR’s rollout of a next‑generation tele‑EMS platform, Hamilton Medical AG’s launch of compact advanced life‑support devices, and Falck AS’s acquisition of several regional private ambulance firms to strengthen its European footprint. Apollo Hospitals Enterprise Ltd expanded its hospital‑based EMS division, while Blueheights Aviation Pvt Ltd introduced air‑ambulance services equipped with advanced neonatal care units. These activities illustrate the market’s dynamic nature and the emphasis on technology and consolidation.