1. North America RTLS for Healthcare Market Overview - Definition, scope, and significance?

Real‑time location systems (RTLS) for healthcare in North America refer to technologies that enable the instantaneous tracking and monitoring of assets, patients, staff, and environmental conditions within medical facilities. The scope covers hardware (tags, sensors, readers), software platforms, integration services, and related consulting. Significance lies in improving operational efficiency, enhancing patient safety, reducing equipment loss, and supporting regulatory compliance, thereby driving cost savings and higher quality of care across hospitals, senior‑living communities and other health settings.

2. North America RTLS for Healthcare Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising demand for asset visibility, pressure to lower healthcare expenditures, increasing patient throughput, and regulatory mandates for infection control. Opportunities arise from the adoption of advanced technologies such as Ultra‑Wideband (UWB) and Bluetooth Low Energy, integration with IoT platforms, and expansion into senior‑living facilities. Primary restraints are high upfront capital costs and concerns about data security. Challenges involve complex integration with legacy hospital information systems and the need for staff training to maximize ROI.

3. North America RTLS for Healthcare Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift from solely RFID‑based solutions toward hybrid architectures that combine Wi‑Fi, Bluetooth, and UWB for greater accuracy and interoperability. Cloud‑based analytics dashboards are gaining traction, enabling real‑time decision making. Emerging trends include AI‑driven predictive maintenance for equipment, integration with electronic health records (EHR) for patient flow optimization, and the use of RTLS data to support telehealth workflows and contact‑less monitoring post‑COVID‑19.

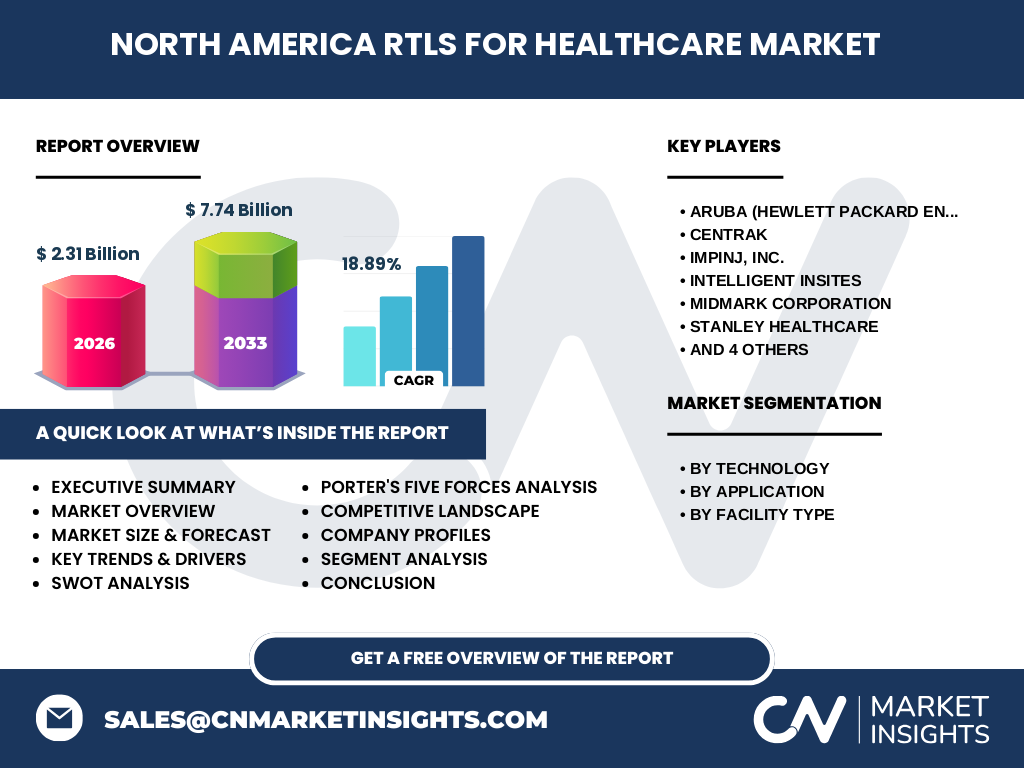

4. COVID-19 Impact on the North America RTLS for Healthcare Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic accelerated adoption as hospitals required precise staff and patient tracking to enforce social distancing and infection control protocols. Demand for environment monitoring (temperature, humidity) and access control surged. Although initial procurement slowed during the early lockdowns, the market rebounded quickly, with many institutions accelerating projects to improve resilience. The recovery trajectory remains strong, feeding into the forecasted CAGR of 18.89% through 2032.

5. North America RTLS for Healthcare Market Competitive Landscape - Major competitors and market consolidation?

Leading competitors include Aruba (Hewlett Packard Enterprise Development LP), CenTrak, Impinj, Inc., Intelligent InSites, Midmark Corporation, STANLEY Healthcare, Sanitag, Sonitor Technologies, Teletracking Technologies, Inc., and Zebra Technologies Corp. The market exhibits moderate consolidation, with larger players acquiring niche specialists to broaden technology portfolios—particularly in UWB and AI analytics—while smaller innovators focus on vertical solutions for senior‑living and specialty clinics.

6. Executive Summary - High-level overview and key findings about North America RTLS for Healthcare Market?

The North America RTLS for Healthcare market was valued at $2.31 billion in 2026 and is projected to reach $7.74 billion by 2033, reflecting an 18.89% CAGR. Growth is propelled by cost‑containment pressures, regulatory demands, and technology convergence. RFID remains the dominant technology, yet Wi‑Fi, Bluetooth, GPS, and UWB are expanding rapidly. Applications span inventory tracking, patient and staff monitoring, access control, environment monitoring, and supply‑chain automation, with hospitals leading adoption and senior‑living facilities emerging as a fast‑growing segment.

7. North America RTLS for Healthcare Market Forecast - Projections for 2025-2032 period?

Based on a robust CAGR of 18.89%, the market is expected to more than triple its 2026 size by the end of the forecast horizon. Continued investment in hybrid technology stacks and cloud analytics will sustain momentum. By 2032, RTLS solutions are anticipated to become standard infrastructure in virtually all acute‑care and senior‑living facilities, supporting integrated patient safety programs and automated supply‑chain operations.

8. North America RTLS for Healthcare Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by technology includes RFID, Wi‑Fi, Bluetooth, GPS, and UWB, with RFID holding the largest share due to its mature ecosystem, while UWB is the fastest‑growing segment because of its superior accuracy. Application‑wise, inventory and asset tracking leads adoption, followed closely by patient and staff tracking. Facility‑type segmentation shows hospitals and healthcare facilities as the primary buyers, with senior‑living communities gaining traction as they seek operational efficiency and resident safety.

9. Global North America RTLS for Healthcare Market Size and Share by Region - Geographic distribution?

North America dominates the global RTLS for Healthcare landscape, accounting for the majority of the $2.31 billion 2026 market size. The United States drives most of the revenue, supported by large hospital networks and advanced technology adoption, while Canada contributes a smaller yet growing share as government‑backed health initiatives encourage digital transformation.

10. Regional Analysis of the North America RTLS for Healthcare Market - Detailed regional market performance?

In the United States, strong capital spending, a high concentration of academic medical centers, and early adoption of IoT standards boost RTLS deployment. Canada’s market is characterized by publicly funded health systems that prioritize cost‑effective asset management, leading to steady growth. Both regions benefit from robust supply chains and a skilled workforce, fostering rapid implementation of next‑generation RTLS solutions.

11. Leading Company Profiles in the North America RTLS for Healthcare Market - Industry players and strategies?

Aruba (HPE) focuses on integrated Wi‑Fi and Bluetooth solutions with strong enterprise security. CenTrak emphasizes infection‑control features and compliance reporting. Impinj supplies high‑performance RFID chips and platforms. Intelligent InSites offers cloud‑native analytics. Midmark provides turnkey RTLS for asset management. STANLEY Healthcare delivers comprehensive patient‑tracking suites. Zebra Technologies leverages its barcode legacy to expand into BLE and UWB tagging. Each company pursues strategic partnerships, acquisitions, and R&D to broaden portfolio breadth.

12. Porter's Five Forces Analysis of the North America RTLS for Healthcare Market - Competitive forces assessment?

• Threat of new entrants: Moderate; high technology expertise and capital requirements create barriers, yet niche startups can enter via software‑only models. • Bargaining power of suppliers: Low to moderate, as many component vendors (chipsets, tags) are commoditized. • Bargaining power of buyers: High; hospitals negotiate large contracts and demand customization. • Threat of substitutes: Low; alternative manual tracking methods are inefficient. • Rivalry among existing firms: Intense, driven by innovation cycles, price competition, and service differentiation.

13. SWOT Analysis of the North America RTLS for Healthcare Market - Strengths, weaknesses, opportunities, threats?

Strengths: Proven technology, clear ROI, regulatory alignment. Weaknesses: High upfront costs, integration complexity. Opportunities: Expansion into senior‑living, AI‑driven analytics, hybrid sensor networks. Threats: Data privacy concerns, potential market saturation, rapid technology shifts that could render legacy systems obsolete.

14. North America RTLS for Healthcare Market Value Chain Analysis - Industry structure and value flow?

The value chain starts with component manufacturers (semiconductor tags, antennas), moves to system integrators who design hardware‑software platforms, followed by solution providers that customize deployments for healthcare clients. Services such as installation, training, and ongoing analytics add value, while end‑users—hospitals and senior‑living operators— generate demand and feedback that shape future product development.

15. Key Investment Insights in the North America RTLS for Healthcare Market - Strategic investment recommendations?

Investors should target companies with strong hybrid technology portfolios, cloud analytics capabilities, and established relationships with major health systems. Mergers that combine sensor expertise with data‑science platforms are likely to create differentiated offerings. Funding for AI‑enabled predictive maintenance and compliance reporting tools presents a high‑growth niche, especially in the senior‑living segment.

16. North America RTLS for Healthcare Market Conclusion - Summary and key takeaways?

The market is on a rapid expansion path, underpinned by a $2.31 billion base in 2026 and an expected $7.74 billion valuation by 2033. High CAGR, technology convergence, and expanding applications across asset, patient, and environmental monitoring position RTLS as a strategic enabler of modern healthcare operations. Stakeholders that invest in interoperable, data‑rich solutions will capture the greatest share of future growth.

17. Research Methodology - How this research was conducted?

Primary data were gathered through interviews with senior executives from leading RTLS vendors, hospital procurement officers, and industry analysts. Secondary sources included company annual reports, regulatory filings, market databases, and reputable industry publications. Quantitative analysis applied trend extrapolation based on the 2026 market size and the projected 18.89% CAGR, while qualitative insights derived from expert opinion shaped the strategic sections.

18. Research Scope - Coverage and limitations?

The study covers North America, focusing on technology, application, and facility‑type segments. It excludes detailed country‑by‑country breakdowns beyond the United States and Canada and does not provide granular market share percentages beyond the aggregate figures supplied. Financial forecasts are limited to the 2025‑2032 horizon using the provided base and forecast values.

19. Key Companies and Recent Developments in the North America RTLS for Healthcare Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Aruba (HPE) launched an integrated Wi‑Fi 6E and BLE 5.2 chipset for ultra‑low‑latency tracking. CenTrak introduced a pandemic‑response module that automates isolation‑room monitoring. Impinj announced a next‑generation RFID chip with extended read range for large‑scale asset pools. Intelligent InSites partnered with a major EHR vendor to embed location data into patient records. STANLEY Healthcare released a UWB‑based patient‑tracking platform with sub‑meter accuracy. Zebra Technologies expanded its BLE beacon portfolio for senior‑living resident safety. These initiatives illustrate a market moving toward tighter integration, higher accuracy, and broader functional coverage.