1. What is the Edge Computing Market Overview – definition, scope, and significance?

Edge computing refers to the processing, storage, and analytics of data at or near the source of generation rather than relying solely on centralized cloud datacenters. The market encompasses hardware devices, software platforms, and services that enable latency‑critical applications across industries such as manufacturing, healthcare, and smart cities. Its significance lies in reducing latency, conserving bandwidth, enhancing privacy, and supporting real‑time decision‑making, which are essential for emerging digital transformation initiatives.

2. What are the Edge Computing Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include exponential data growth from IoT devices, the need for low‑latency processing in autonomous systems, and rising adoption of AI at the edge. Restraints stem from high initial capital expenditure and fragmented standards. Challenges involve security concerns, talent shortages, and integration complexity with legacy IT. Opportunities arise from 5G rollout, industry‑specific edge solutions, and the expanding ecosystem of edge‑as‑a‑service models that lower entry barriers.

3. What are the current Edge Computing Market Growth Trends?

Trend highlights include convergence of edge with 5G, which unlocks ultra‑reliable low‑latency communications; increasing deployment of micro‑data centers in remote locations; growing preference for containerized workloads and serverless edge platforms; and rising investments in edge AI accelerators. Additionally, sector‑specific pilots—such as predictive maintenance in manufacturing and remote patient monitoring in healthcare—are accelerating commercial adoption.

4. How has COVID‑19 impacted the Edge Computing Market and what is the recovery trajectory?

The pandemic accelerated remote work, digital learning, and tele‑health, all of which heightened demand for localized processing to ensure quality of experience. Supply‑chain disruptions temporarily slowed hardware deployments, but the overall market showed resilience, with a swift rebound as enterprises prioritized edge solutions to support distributed operations. Recovery is now on a strong upward path, reinforcing the market’s long‑term growth momentum.

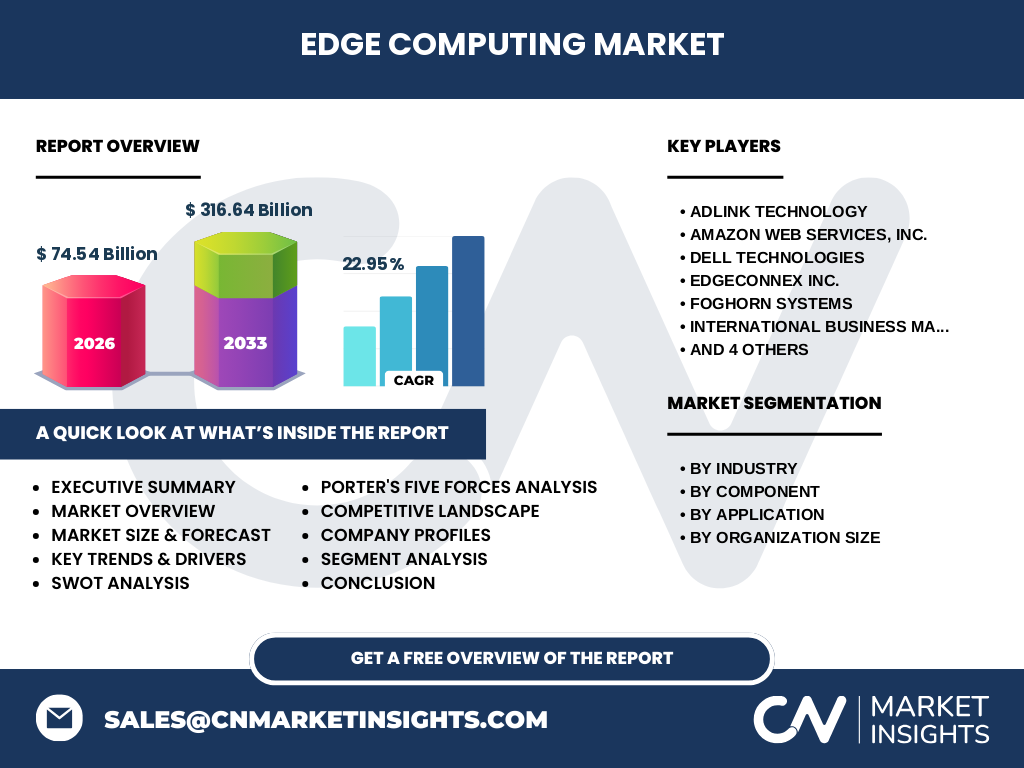

5. Who are the major competitors in the Edge Computing Market and what is the state of market consolidation?

Leading players include ADLINK Technology, Amazon Web Services, Dell Technologies, EdgeConnex, FogHorn Systems, IBM, Litmus Corporation, Microsoft, Hewlett Packard Enterprise, and Vapor IO. Competition is intense across hardware, software, and services, leading to strategic partnerships and selective acquisitions. While consolidation remains moderate, major cloud providers are expanding edge footprints, prompting smaller niche firms to collaborate or merge to enhance go‑to‑market reach.

6. What are the key findings in the Executive Summary of the Edge Computing Market?

The market is projected to reach $316.64 billion by 2033, growing from $74.54 billion in 2026 at a CAGR of 22.95%. Growth is driven by 5G adoption, AI‑enabled edge analytics, and sector‑specific use cases. North America and Asia‑Pacific lead adoption, while Europe shows robust regulatory‑driven deployments. Competitive dynamics favor vendors that provide integrated hardware‑software‑service bundles, and investment interest is high across venture and corporate capital.

7. What is the Edge Computing Market Forecast for the 2025‑2032 period?

Based on the provided CAGR of 22.95%, the market is expected to expand rapidly, surpassing $300 billion by the early 2030s. The forecast anticipates increasing share of services relative to hardware as managed edge platforms gain traction. Emerging applications such as AR/VR, autonomous vehicles, and real‑time industrial IoT will contribute substantially to revenue growth throughout the forecast horizon.

8. How is the Edge Computing Market sized and shared by segmentation?

By industry, manufacturing and IT/telecom dominate due to high data velocity needs, followed by energy & utility, healthcare, retail, and government. Component‑wise, hardware accounts for the largest portion, with software and services gaining proportionate growth as deployment models mature. Application segmentation shows smart cities, Industrial IoT, and content delivery as primary drivers, while AR/VR is emerging rapidly. Organization size analysis indicates large enterprises lead adoption, but SMEs are increasingly leveraging edge‑as‑a‑service.

9. What is the global Edge Computing Market size and share by region?

Geographically, North America holds the largest market share, propelled by early cloud adoption and heavyweight technology vendors. Asia‑Pacific follows closely, spurred by rapid 5G rollouts, manufacturing clusters, and smart‑city initiatives. Europe maintains a solid position, driven by regulatory frameworks and industrial automation projects. While specific monetary shares are not disclosed, the regional hierarchy reflects the concentration of technology ecosystems and infrastructure investments.

10. What does the Regional Analysis of the Edge Computing Market reveal?

North America’s growth is anchored by large enterprise deployments and strong R&D activity among leading vendors. Asia‑Pacific benefits from government‑led smart‑city programs, a surge in IoT device penetration, and aggressive 5G expansion, especially in China, Japan, and South Korea. Europe’s market is shaped by stringent data‑privacy regulations that favor localized processing. Emerging markets in Latin America and the Middle East show nascent yet promising adoption, primarily in telecom and energy sectors.

11. Which leading companies are profiled in the Edge Computing Market and what are their strategies?

Key profiles include ADLINK Technology’s focus on rugged edge hardware, AWS’s extensive edge services (e.g., AWS Outposts), Dell’s integrated edge‑to‑cloud solutions, EdgeConnex’s micro‑data center network, FogHorn’s real‑time analytics platform, IBM’s hybrid cloud‑edge approach, Litmus’s edge security suite, Microsoft’s Azure Edge, HPE’s EdgeLine appliances, and Vapor IO’s decentralized edge infrastructure. Strategies revolve around ecosystem partnerships, AI integration, and expanding managed services to capture recurring revenue.

12. How does Porter’s Five Forces analysis apply to the Edge Computing Market?

Threat of new entrants is moderate due to high capital requirements but mitigated by open‑source edge platforms. Supplier power is moderate; component suppliers (semiconductors) have some leverage, yet volume manufacturing reduces risk. Buyer power is increasing as enterprises demand flexible, pay‑as‑you‑go edge services. Substitutes are limited, as traditional cloud cannot meet latency‑critical needs. Competitive rivalry is intense, driven by innovation cycles and ecosystem alliances.

13. What are the SWOT analysis highlights for the Edge Computing Market?

Strengths: rapid latency reduction, bandwidth savings, and alignment with 5G. Weaknesses: fragmented standards and high upfront costs. Opportunities: AI at the edge, vertical‑specific solutions, and edge‑as‑a‑service monetization. Threats: cybersecurity vulnerabilities, regulatory compliance complexities, and potential slowdown in hardware supply chains.

14. How is the Edge Computing Market value chain structured?

The value chain begins with component manufacturers (chips, sensors), proceeds to hardware integrators building edge gateways and micro‑datacenters, followed by software developers delivering platforms and analytics. Service providers layer managed operations, deployment, and support. End‑users—enterprises and public sector entities—consume the integrated solution. Ancillary players such as system integrators and network operators facilitate connectivity and localization.

15. What key investment insights can be drawn from the Edge Computing Market?

Investors should target companies that combine hardware durability with software agility, especially those offering subscription‑based edge services. Partnerships with telecom operators for 5G‑enabled edge nodes present high‑growth opportunities. Funding rounds focusing on AI accelerators and security solutions are likely to yield strong returns. Diversifying across hardware, software, and services reduces exposure to any single segment’s volatility.

16. What is the concluding summary of the Edge Computing Market?

The edge computing market is on a steep growth trajectory, underpinned by a 22.95% CAGR and a projected valuation of $316.64 billion by 2033. Core drivers include 5G, AI, and industry‑specific latency needs, while challenges such as security and standards persist. Regional dynamics favor North America and Asia‑Pacific, and the competitive landscape is marked by both large cloud providers and specialized edge innovators. Strategic investments in integrated solutions are recommended.

17. Which research methodology was employed for this market study?

The study combined primary interviews with industry executives, technology vendors, and end‑user decision makers, alongside secondary research from reputable databases, vendor whitepapers, and regulatory filings. Quantitative data were validated through triangulation, and forecasts were derived using compound annual growth rate (CAGR) modeling anchored to the provided market size figures.

18. What is the scope of this research and its limitations?

The scope covers global edge computing across hardware, software, and services, segmented by industry, application, component, and organization size. It includes regional analysis for major markets and profiles of leading vendors. Limitations are confined to publicly available information; proprietary financial details beyond the provided figures were not included, and forecasts assume continued macro‑economic stability.

19. Which key companies have recent developments in the Edge Computing Market?

Recent highlights include Amazon Web Services launching new AWS Snowball Edge instances, Microsoft expanding Azure Edge Zones, Dell unveiling ruggedized edge servers, ADLINK introducing AI‑optimized edge gateways, FogHorn releasing updated real‑time analytics SDK, IBM rolling out hybrid cloud‑edge orchestration tools, HPE announcing EdgeLine Flex, Vapor IO deploying decentralized edge nodes across major metros, EdgeConnex scaling its micro‑data centre network, and Litmus unveiling an edge‑focused cybersecurity platform. These moves reflect intensified innovation and partnership activity.