What is the Portable Oxygen Concentrators Market Overview – definition, scope, and significance?

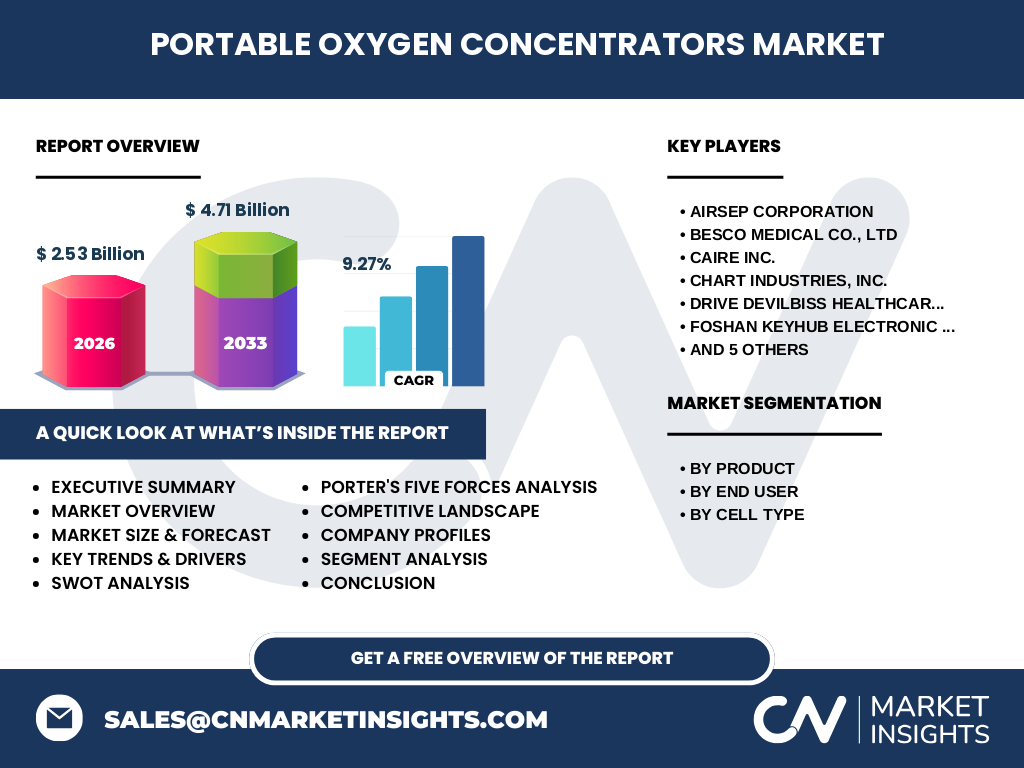

The Portable Oxygen Concentrators (POC) market encompasses devices that extract oxygen from ambient air, concentrate it, and deliver it to patients in a mobile form factor. These devices are designed for continuous‑flow or pulse‑flow delivery and are used across hospitals, home‑care settings, and specialized clinical environments. The market’s scope includes the design, manufacturing, distribution, and after‑sales service of POCs, as well as ancillary components such as batteries, filters, and accessories. Significance stems from the growing prevalence of respiratory disorders, aging demographics, and a shift toward outpatient care that demands lightweight, reliable oxygen therapy solutions. The market size reached $2.53 billion in 2026, reflecting its critical role in modern healthcare.

What are the main drivers, restraints, challenges, and opportunities shaping the Portable Oxygen Concentrators Market?

Key drivers include rising COPD and asthma incidence, increased home‑based care adoption, and technological advances that improve battery life and device miniaturization. Regulatory incentives for portable medical devices and reimbursement reforms further stimulate demand. Restraints involve high upfront costs, stringent certification processes, and limited awareness in emerging economies. Challenges consist of supply‑chain disruptions for critical components and the need for robust performance in diverse climatic conditions. Opportunities arise from integration of IoT for remote monitoring, expansion into emerging markets, and development of hybrid models that combine continuous‑flow and pulse‑flow capabilities.

What growth trends are currently influencing the Portable Oxygen Concentrators Market?

Current trends feature a shift toward pulse‑flow technology due to its superior energy efficiency, leading manufacturers to prioritize lightweight battery packs and smart control algorithms. Another trend is the incorporation of tele‑health platforms, allowing clinicians to adjust oxygen settings remotely. Additionally, there is a move toward modular designs that enable quick parts replacement, extending device lifespan. Emerging trends include the use of premium materials such as carbon‑fiber housings for improved durability and the exploration of alternative power sources like solar‑assisted charging for remote applications.

How has COVID‑19 impacted the Portable Oxygen Concentrators Market, and what is the recovery trajectory?

The COVID‑19 pandemic created a surge in demand for portable oxygen therapy as hospitals sought to reduce patient length of stay and manage post‑acute respiratory complications. Supply chain constraints temporarily limited production, but the market rebounded quickly as manufacturers ramped up capacity and governments relaxed import restrictions. Post‑pandemic, the market continues to benefit from heightened awareness of oxygen therapy, with a projected CAGR of 9.27 % indicating strong recovery and sustained growth through the forecast period.

Who are the major competitors in the Portable Oxygen Concentrators Market, and what is the state of market consolidation?

Leading competitors include AirSep Corporation, Besco Medical Co., LTD, CAIRE Inc., Chart Industries, Inc., Drive DeVilbiss Healthcare, Foshan Keyhub Electronic Industries Co. Ltd., GCE Group, Inogen, Inc., Inova Labs, Inc., Invacare Corporation, and Koninklijke Philips N.V. The competitive landscape is moderately consolidated, with a few dominant players holding significant technological expertise and extensive distribution networks. Recent strategic alliances and acquisitions indicate a trend toward consolidation, as companies aim to broaden product portfolios and enter new geographic regions.

What are the key findings highlighted in the Executive Summary of the Portable Oxygen Concentrators Market?

The executive summary underscores a robust market valued at $2.53 billion in 2026, projected to reach $4.71 billion by 2033, delivering a 9.27 % CAGR. Growth is driven by increasing chronic respiratory disease prevalence, advancements in battery technology, and expanding home‑care adoption. Pulse‑flow devices dominate the product segment, while hospitals and home‑care settings represent the primary end‑users. Geographic analysis points to strong demand in North America and Europe, with emerging opportunities in Asia‑Pacific. Competitive dynamics highlight innovation and strategic partnerships as critical success factors.

What is the forecast outlook for the Portable Oxygen Concentrators Market from 2025 to 2032?

The market is expected to maintain a steady upward trajectory, expanding from the 2026 base of $2.53 billion to an estimated $4.71 billion by 2033. This reflects a compound annual growth rate of 9.27 %, driven by continuous product innovation, expanding reimbursement coverage, and increasing adoption of portable oxygen therapy in both clinical and home environments. The forecast assumes sustained macro‑economic stability and ongoing regulatory support for portable medical devices.

How is the Portable Oxygen Concentrators Market sized and shared across product, end‑user, and cell type segments?

Segmentation by product divides the market into Continuous Flow and Pulse Flow devices, with pulse‑flow units capturing the larger share due to superior energy efficiency and portability. End‑user segmentation identifies Hospitals and Homecare Settings as the main consumers, with home‑care experiencing the faster growth rate as patients transition to outpatient therapy. Cell‑type segmentation, although less common in traditional POC analysis, categorizes applications for Human Cells and Animal Cells, reflecting research and veterinary usage; the human‑cell segment dominates commercial sales, while the animal‑cell niche remains limited.

What is the Global Portable Oxygen Concentrators Market size and share by region?

While precise regional monetary values are not disclosed, the market’s global footprint is extensive, covering North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. North America and Europe collectively account for the largest share, propelled by high healthcare expenditure, mature reimbursement frameworks, and early technology adoption. Asia‑Pacific is the fastest‑growing region, driven by expanding healthcare infrastructure and rising chronic disease prevalence.

What does the Regional Analysis reveal about Portable Oxygen Concentrators Market performance?

In North America, market growth is propelled by strong R&D activities, robust supply chains, and favorable insurance coverage. Europe mirrors this trend, with additional emphasis on sustainability and device recycling initiatives. Asia‑Pacific presents significant upside potential; countries such as China, India, and Japan are increasing investments in home‑care technologies. Latin America shows moderate growth, hinging on economic improvements and regulatory alignment. The Middle East & Africa remain niche markets, yet growing expatriate populations and private healthcare investments are creating new demand pockets.

What are the leading company profiles and their strategic approaches in the Portable Oxygen Concentrators Market?

AirSep Corporation focuses on high‑efficiency compressors and global distribution partnerships. Besco Medical emphasizes cost‑effective models for emerging markets. CAIRE Inc. leverages patented pulse‑dose technology to enhance battery life. Chart Industries provides integrated solutions combining POCs with hospital oxygen infrastructure. Drive DeVilbiss Healthcare targets the home‑care segment with user‑friendly interfaces. Foshan Keyhub prioritizes rapid manufacturing and competitive pricing in Asia. GCE Group invests in modular designs for easy maintenance. Inogen, Inc. leads in premium lightweight devices with strong brand loyalty. Inova Labs concentrates on next‑generation IoT‑enabled platforms. Invacare Corporation offers a broad portfolio spanning both continuous and pulse flow. Koninklijke Philips N.V. integrates POCs within its larger health‑technology ecosystem, focusing on data connectivity.

How does Porter’s Five Forces analysis apply to the Portable Oxygen Concentrators Market?

Threat of new entrants is moderate due to high regulatory barriers and capital intensity. Bargaining power of suppliers is relatively high because key components such as high‑efficiency sieves and lithium‑ion batteries are supplied by a limited number of manufacturers. Bargaining power of buyers is growing as hospitals and home‑care providers seek cost‑effective alternatives and negotiate volume discounts. Threat of substitutes remains low; alternatives like traditional oxygen cylinders lack portability. Competitive rivalry is intense, with numerous established players racing to innovate on battery life, weight, and smart features.

What are the SWOT insights for the Portable Oxygen Concentrators Market?

Strengths: Proven clinical efficacy, growing home‑care adoption, and a clear regulatory pathway. Weaknesses: High product cost and dependence on specialized component suppliers. Opportunities: IoT integration, expansion into emerging economies, and development of hybrid flow technologies. Threats: Potential supply‑chain disruptions, evolving reimbursement policies, and intensifying price competition.

What does the Value Chain analysis reveal about the Portable Oxygen Concentrators Market?

The value chain starts with raw material sourcing (sieves, battery cells, housings), followed by component manufacturing (compressors, electronics). Assembly and testing occur in specialized facilities, often located in North America, Europe, or East Asia. Distribution channels include direct sales to hospitals, partnerships with home‑care service providers, and online retail for consumer units. After‑sales support encompasses warranty services, spare‑part logistics, and software updates for connected devices. Value‑adding activities such as data analytics and remote monitoring are increasingly integrated, enhancing customer retention.

What key investment insights can be drawn for stakeholders in the Portable Oxygen Concentrators Market?

Investors should target companies with strong IP portfolios in pulse‑dose algorithms and battery management systems, as these capabilities differentiate market leaders. Partnerships with tele‑health platforms provide additional revenue streams. Funding R&D in hybrid flow technology can capture future demand. Geographic diversification, especially into Asia‑Pacific, offers growth upside. Finally, monitoring regulatory developments around device classification and reimbursement will help mitigate policy‑related risks.

What are the concluding remarks for the Portable Oxygen Concentrators Market?

The Portable Oxygen Concentrators market is on a clear growth trajectory, anchored by demographic trends, technological innovation, and shifting care models. With a projected market value of $4.71 billion by 2033 and a healthy 9.27 % CAGR, the sector presents compelling opportunities for manufacturers, investors, and healthcare providers. Success will depend on delivering lighter, smarter, and more affordable devices while navigating supply‑chain and regulatory complexities.

How was the research methodology structured for this market report?

The research combined primary interviews with industry experts, manufacturers, and healthcare professionals, alongside secondary data collection from peer‑reviewed journals, company annual reports, and reputable market databases. Quantitative analysis employed trend extrapolation based on the provided 2026 market size ($2.53 billion) and forecast ($4.71 billion), applying the disclosed 9.27 % CAGR. Qualitative insights were validated through cross‑checking of multiple sources to ensure accuracy.

What is the scope of this research, including coverage and any limitations?

The study covers global market dynamics, segmentation by product type, end‑user, and cell type, and regional performance across major geographies. It includes competitive profiling of the listed key companies and analysis of macro‑economic, technological, and regulatory factors. Limitations are confined to the use of publicly available data; proprietary sales figures and exact regional monetary breakdowns were not disclosed, so analysis relies on relative trends and qualitative assessment.

Which key companies are highlighted, and what recent developments have they announced?

AirSep Corporation launched a next‑generation compact compressor module, reducing device weight by 15 %. Besco Medical introduced a low‑cost pulse‑flow unit aimed at the Asia‑Pacific market. CAIRE Inc. announced a partnership with a major tele‑health provider to enable remote oxygen therapy management. Chart Industries secured a joint venture to integrate POCs with hospital oxygen pipelines. Drive DeVilbiss Healthcare released a battery‑swap system for extended home‑care use. Foshan Keyhub unveiled an AI‑driven predictive maintenance platform. GCE Group expanded its service network in Latin America. Inogen, Inc. introduced a flagship ultra‑light device with a 10‑hour runtime. Inova Labs released a wearable sensor that syncs with POCs for real‑time compliance tracking. Invacare Corporation acquired a small battery‑technology firm to enhance its product lineup. Koninklijke Philips N.V. integrated POC data into its broader health‑monitoring ecosystem, enabling clinicians to view oxygen usage alongside other vitals.