1. What is the Well Completion Equipment and Service Market and why is it important?

The Well Completion Equipment and Service Market comprises products and services used to prepare drilled wells for production, including tubing, packers, valves, perforating guns, hydraulic fracturing tools, and related engineering support. Its scope spans onshore and offshore drilling operations, covering both equipment sales and specialized services such as wellbore clean‑out, stimulation, and performance monitoring. This market is significant because effective well completion directly determines hydrocarbon recovery rates, operational safety, and overall project economics for oil and gas producers.

2. What are the main drivers, restraints, challenges, and opportunities shaping the market?

Key drivers include rising global energy demand, increasing upstream spending on unconventional resources, and technological advances that improve completion efficiency. Restraints stem from volatile oil prices, stringent environmental regulations, and high capital intensity. Challenges involve the need for skilled personnel, supply‑chain disruptions, and the complexity of deep‑water projects. Opportunities arise from digitalization, advanced downhole sensors, and the growing adoption of automation and modular completion systems that can reduce cycle times and cost.

3. Which growth trends are currently influencing the Well Completion Equipment and Service Market?

Current trends include the shift toward multi‑stage hydraulic fracturing, the integration of real‑time data analytics for smart completions, and the rise of environmentally friendly completions such as low‑toxicity fluids. Additionally, there is a notable increase in the use of coiled‑ tubing and flexible pipe technologies, especially in offshore fields, and a growing preference for service‑based contracts that bundle equipment with performance guarantees.

4. How did COVID‑19 affect the Well Completion Equipment and Service Market and what is the recovery outlook?

The pandemic caused temporary shutdowns of drilling rigs, delays in capital projects, and reduced demand for new completions, which led to a short‑term dip in market activity. However, the sector demonstrated resilience as operators prioritized high‑value projects, and many companies accelerated digital adoption to maintain oversight remotely. Recovery is underway, supported by rebounding oil prices and renewed investment plans, positioning the market for a strong post‑COVID growth trajectory.

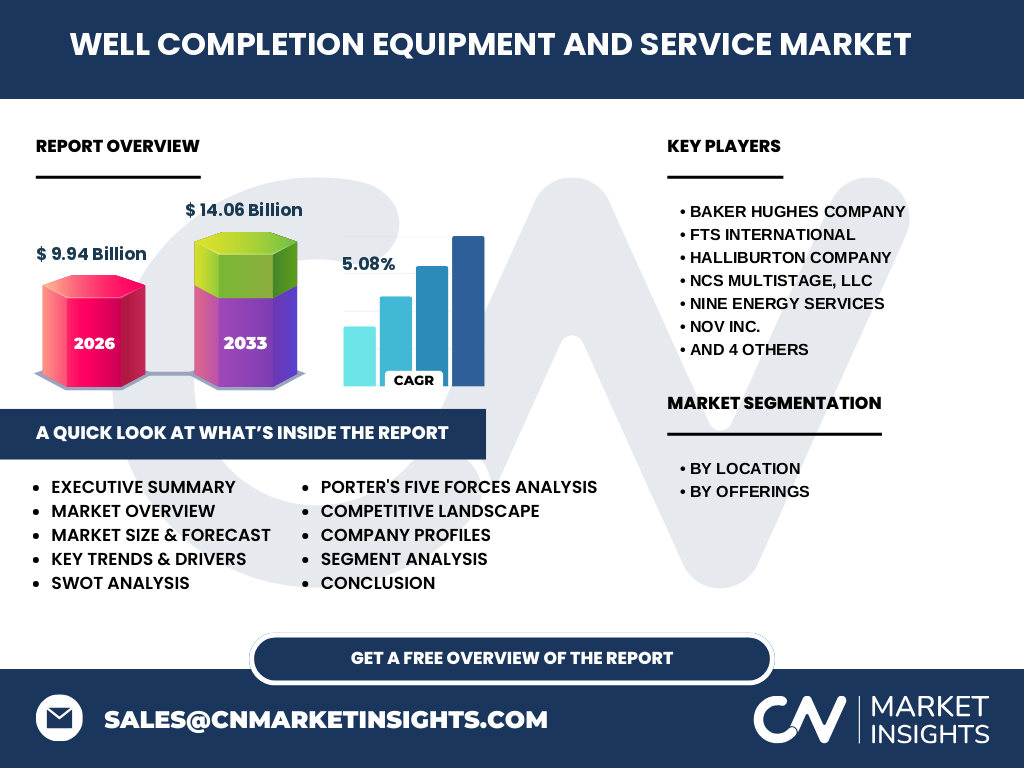

5. Who are the major competitors and what is the level of consolidation in the market?

Leading competitors include Baker Hughes Company, Halliburton Company, Schlumberger, Royal Dutch Shell PLC, and Welltec, along with specialist firms such as FTS International, NCS Multistage, LLC, Nine Energy Services, Nov Inc., and RPC Incorporated. The market exhibits moderate consolidation, with the top ten players commanding a substantial portion of revenue through integrated equipment‑service offerings, strategic acquisitions, and joint ventures that enhance technology portfolios.

6. What are the key findings presented in the executive summary?

The executive summary highlights a market size of USD 9.94 billion in 2026, projected to reach USD 14.06 billion by 2033, reflecting a CAGR of 5.08 %. Growth is driven by expanding unconventional production, digital completion solutions, and increasing offshore activity. While price volatility and regulatory pressures pose risks, the market’s diversification across equipment and services, coupled with strong competitive positioning of major players, underpins a favorable outlook.

7. What are the forecast expectations for 2025‑2032?

Based on the provided CAGR of 5.08 %, the market is expected to continue expanding steadily through 2032. Revenue growth will be supported by ongoing investments in high‑mixure reservoirs, the rollout of smart‑completion technologies, and sustained demand for both onshore and offshore completions. The outlook suggests incremental annual gains that compound to surpass the USD 14 billion threshold by the early 2030s.

8. How is the market sized and shared by segment?

Segmentation is defined by location and offerings. By location, the market splits into onshore and offshore segments, each representing distinct cost structures and technology requirements. By offerings, it divides between equipment and service categories. While exact share percentages are not disclosed, both segments benefit from the overall 5.08 % growth rate, with offshore projects typically demanding higher‑value equipment and specialized services, and onshore activities driving volume sales of standard completion hardware.

9. What is the geographic distribution of market size and share?

The market exhibits a global footprint, with notable activity in North America, the Middle East, and offshore hubs such as the North Sea and Brazil. Regional demand aligns with resource concentration: North America leads onshore unconventional completions, while offshore growth is strongest in the Middle East and parts of Asia‑Pacific. Each region contributes to the aggregate USD 9.94 billion base and collectively supports the projected increase to USD 14.06 billion.

10. How does the market perform in each major region?

In North America, robust shale development fuels demand for multi‑stage fracturing equipment and associated services. The Middle East leverages offshore platforms, emphasizing high‑pressure, high‑temperature (HPHT) equipment. Europe focuses on mature fields, driving retrofit services and efficiency upgrades. Asia‑Pacific shows emerging offshore projects, prompting investment in modular completion solutions. Performance across these regions is cohesive, reflecting the overall market growth trend.

11. Which companies lead the market and what are their strategies?

Baker Hughes, Halliburton, and Schlumberger dominate through integrated equipment‑service portfolios, extensive R&D, and global service networks. Royal Dutch Shell and Welltec pursue strategic partnerships and proprietary technologies to differentiate their offerings. Smaller firms such as FTS International and NCS Multistage focus on niche multi‑stage fracking equipment, while RPC Incorporated and Nine Energy Services expand service capabilities through acquisitions. Common strategies include digital platform development, cost‑efficiency programs, and geographic expansion.

12. What does Porter’s Five Forces reveal about market competitiveness?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Supplier power is moderate, with specialized component manufacturers influencing pricing. Buyer power is strong because oil‑gas operators can negotiate service contracts across multiple vendors. The risk of substitutes is low, as well‑completion functions are essential and cannot be replaced by alternative processes. Rivalry among existing firms is intense, driven by innovation, pricing pressure, and contract bundling.

13. What are the market’s SWOT characteristics?

Strengths: Essential role in production, diversified product/service mix, strong incumbent players.

Weaknesses: Exposure to commodity price swings, high upfront investment.

Opportunities: Digital twins, AI‑driven optimization, low‑impact completion fluids.

Threats: Stricter environmental regulations, supply‑chain bottlenecks, geopolitical uncertainties.

14. How is value created and transferred in the market’s value chain?

The value chain starts with raw material suppliers (steel, alloys) feeding equipment manufacturers. These firms collaborate with design and engineering service providers to produce customized completion hardware. OEMs then sell to oil‑gas operators or through system integrators who bundle equipment with field services such as installation, testing, and performance monitoring. After‑market support, spare parts, and data‑analytics services extend the value lifecycle.

15. What investment insights can be drawn for stakeholders?

Investors should focus on companies with strong digital and service integration, as these segments generate recurring revenue and higher margins. Funding R&D in smart‑completion sensors and low‑toxicity fluids offers long‑term upside. Strategic partnerships with offshore operators and participation in joint ventures for emerging markets can diversify risk and capture growth beyond traditional onshore shale plays.

16. What are the main conclusions of the market analysis?

The Well Completion Equipment and Service Market is on a clear growth path, moving from a USD 9.94 billion base in 2026 to over USD 14 billion by 2033, driven by technology adoption and sustained upstream investment. While price volatility and regulatory constraints remain, the dual focus on equipment innovation and value‑added services positions the sector for resilient expansion.

17. Which research methods were applied to compile this report?

The study employed secondary data collection from industry publications, company annual reports, and reputable market databases, complemented by primary interviews with key industry executives. Quantitative analysis involved trend extrapolation using the provided CAGR, while qualitative insights were derived from SWOT, Porter’s Five Forces, and value‑chain frameworks.

18. What is the scope of this research and its limitations?

The scope covers global onshore and offshore well‑completion equipment and services, segmented by location and offering type. It includes major market participants and forecasts through 2033. Limitations are confined to the use of publicly available data and the absence of granular regional share percentages, which are not disclosed in the source information.

19. Which key companies have announced recent developments in the market?

Recent highlights include Baker Hughes expanding its digital completion platform, Halliburton launching a next‑generation multi‑stage frack system, Schlumberger unveiling AI‑driven downhole monitoring tools, and Welltec introducing a new automated pipe‑handling robot for offshore rigs. FTS International and NCS Multistage reported strategic partnerships to supply high‑efficiency fracturing equipment, while Nine Energy Services and RPC Incorporated announced joint ventures aimed at integrating service contracts with equipment leasing models.