1. What is the Disposable Incontinence Products Market and why is it significant?

The Disposable Incontinence Products Market comprises consumable, single‑use solutions designed to manage urinary and fecal leakage in adults. Products include disposable adult diapers, under pads, leg urine bags, indwelling catheters, and intermittent catheters. The market spans a broad user base—men, women, and unisex consumers—and is distributed through supermarkets, specialty stores, and online platforms. Its significance stems from a rapidly aging global population, increasing prevalence of chronic conditions such as diabetes and prostate disorders, and a growing preference for hygienic, convenient solutions that enable greater mobility and dignity for users.

2. What are the main drivers, restraints, challenges, and opportunities in the Disposable Incontinence Products Market?

Key drivers include demographic aging, rising awareness of incontinence management, and expanding e‑commerce channels that improve product accessibility. Restraints involve price sensitivity in emerging economies and stringent regulatory requirements for medical‑grade catheters. Challenges arise from supply‑chain disruptions, especially for raw materials like super‑absorbent polymers, and from the stigma that can limit market penetration. Opportunities are found in product innovation—such as breathable fabrics and integrated odor‑control technologies—and in geographic expansion into under‑served markets where aging demographics are accelerating.

3. What current and emerging trends are shaping the Disposable Incontinence Products Market?

Trend analysis shows a shift toward “smart” disposable products equipped with moisture sensors that alert caregivers via mobile apps. Eco‑friendly formulations, using biodegradable backings, are gaining traction as sustainability concerns grow. Additionally, customization—offering varied absorbency levels and fit options for different body types—is becoming a differentiator. Online sales are accelerating, driven by subscription models that guarantee discreet, regular deliveries, reducing stock‑out risk for end‑users.

4. How did COVID‑19 affect the Disposable Incontinence Products Market and what is the recovery trajectory?

The pandemic initially disrupted manufacturing and logistics, causing short‑term inventory gaps. However, heightened health‑care awareness and increased home‑care needs boosted demand, especially for online channels. Post‑2020, the market rebounded quickly, with a clear recovery path supported by rising tele‑health services that recommend disposable solutions for remote patients. The overall trajectory remains upward, reinforcing the market’s resilience.

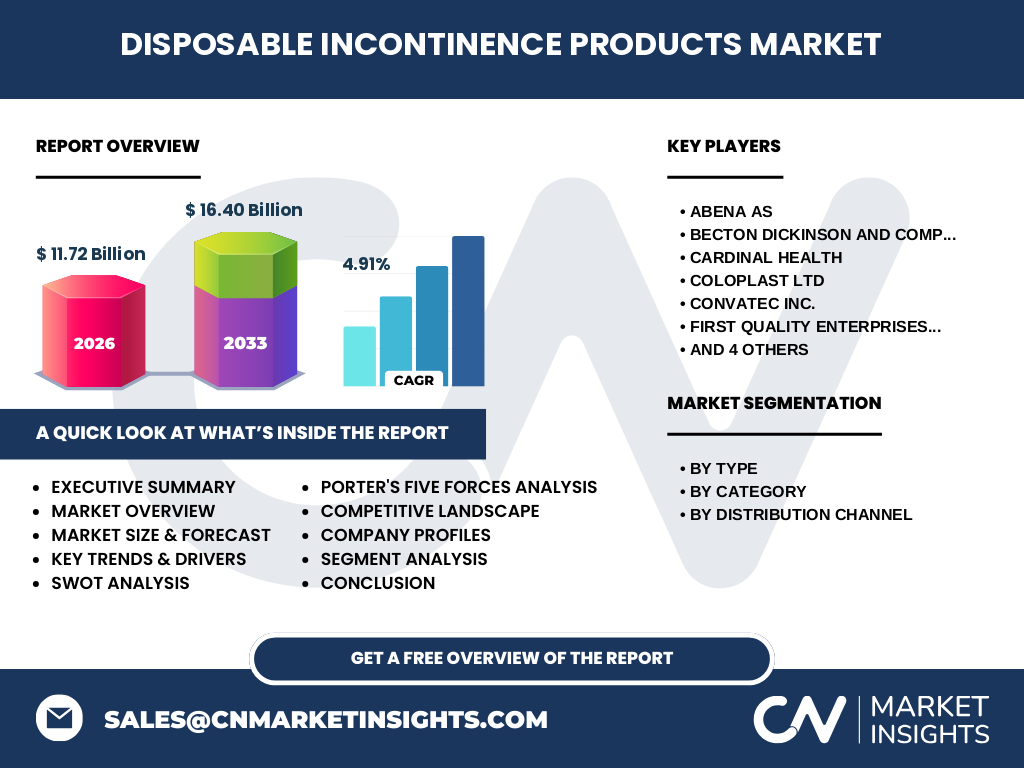

5. Who are the major competitors and how consolidated is the Disposable Incontinence Products Market?

The market is moderately consolidated, featuring a mix of large multinational manufacturers and specialized niche players. Prominent competitors include Abena AS, Becton Dickinson (C R Bard Inc.), Cardinal Health, Coloplast Ltd, ConvaTec Inc., First Quality Enterprises Inc., HARTMANN USA Inc., Hollister Incorporated, Kimberly Clark, and Medline Industries Inc. These firms compete on product breadth, technological innovation, and channel reach, with occasional strategic alliances and acquisitions that further consolidate market share.

6. What are the high‑level findings of the Disposable Incontinence Products Market?

The market is valued at $11.72 billion in 2026 and is projected to reach $16.40 billion by 2033, reflecting a CAGR of 4.91 %. Growth is propelled by aging demographics, increasing chronic disease prevalence, and digital sales acceleration. Product innovation and sustainability are emerging as critical success factors. Competitive dynamics are characterized by a handful of global leaders expanding through product diversification and strategic distribution enhancements.

7. What are the forecasted market prospects for 2025‑2032?

Based on the provided CAGR, the market is expected to maintain steady expansion through 2032, approaching the $16.40 billion forecast for 2033. The forecast underscores continued demand across all product types, with particular growth anticipated in disposable adult diapers and catheter segments due to demographic trends. Online platforms are projected to capture a larger share of distribution, driven by convenience and subscription‑based purchasing models.

8. How is the market sized and shared across the identified segments?

Segmentation is defined by product type, user category, and distribution channel. By type, disposable adult diapers dominate due to universal applicability, followed by under pads, leg urine bags, indwelling catheters, and intermittent catheters. User categories are split among men, women, and unisex offerings, with unisex products gaining momentum for broader market appeal. Distribution analysis shows supermarkets and hypermarkets hold the largest traditional share, while specialty stores cater to clinical and high‑margin buyers, and online platforms exhibit the fastest growth rate.

9. What is the geographic distribution of the Disposable Incontinence Products Market?

The market spans North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. While specific monetary shares are not disclosed, regions with mature health‑care infrastructure—such as North America and Europe—currently command the highest sales volumes. Rapidly aging populations in Asia‑Pacific and emerging economies in Latin America present sizable upside potential, especially as distribution channels evolve.

10. How does each region perform within the Disposable Incontinence Products Market?

North America leads in adoption of premium disposable solutions, supported by strong reimbursement frameworks and extensive e‑commerce penetration. Europe follows closely, emphasizing regulatory compliance and eco‑friendly product innovations. Asia‑Pacific shows the steepest growth trajectory, driven by large population bases and increasing health‑care spending. Latin America and the Middle East & Africa are in earlier adoption stages but are expected to accelerate as awareness and distribution networks improve.

11. Which companies are leading the market and what strategies are they employing?

Key players such as Kimberly Clark and HARTMANN USA focus on brand diversification and expanding premium lines. Coloplast and ConvaTec leverage clinical partnerships to promote catheter solutions. Becton Dickinson (C R Bard) emphasizes R&D for advanced materials that improve comfort and safety. Abena and First Quality pursue cost‑leadership while expanding online sales. Across the board, firms are investing in digital marketing, subscription services, and sustainability initiatives to capture evolving consumer preferences.

12. What does Porter’s Five Forces reveal about market competitiveness?

• Threat of new entrants: Moderate, due to high regulatory barriers and capital‑intensive manufacturing. • Bargaining power of suppliers: Moderate; raw material scarcity can elevate costs, but large manufacturers negotiate favorable terms. • Bargaining power of buyers: High for institutional buyers (hospitals, long‑term care) who demand volume discounts; individual consumers have limited power but influence product features. • Threat of substitutes: Low to moderate; reusable cloth products exist but face hygiene concerns. • Rivalry among existing firms: Intense, driven by product innovation, channel expansion, and price competition.

13. What are the SWOT highlights for the Disposable Incontinence Products Market?

Strengths: Growing demand, strong brand loyalty, and proven technology. Weaknesses: Sensitivity to raw‑material price swings and stigma affecting consumer outreach. Opportunities: Sustainable product lines, smart‑sensor integration, and untapped emerging markets. Threats: Regulatory changes, potential supply‑chain disruptions, and competitive pressure from reusable alternatives.

14. How is value created and transferred across the Disposable Incontinence Products value chain?

The value chain begins with raw‑material suppliers (super‑absorbent polymers, non‑woven fabrics), proceeds to R&D and formulation, followed by manufacturing and quality assurance. Distribution channels—wholesale, retail, and e‑commerce—deliver finished goods to end users. Post‑sale services include customer support, product education, and waste‑management guidance. Digital platforms increasingly integrate logistics with data analytics, enhancing inventory efficiency and consumer insights.

15. What investment insights can be drawn from the Disposable Incontinence Products Market?

Investors should prioritize companies with diversified product portfolios and strong online capabilities, as digital sales are outpacing traditional retail. Firms advancing sustainability—through biodegradable components or reduced carbon footprints—are likely to capture premium pricing. Strategic M&A targeting niche catheter innovators or specialty distribution networks can accelerate market penetration in high‑growth regions such as Asia‑Pacific.

16. What are the key takeaways from the Disposable Incontinence Products Market analysis?

The market is on a robust growth path, underpinned by demographic trends and evolving consumer expectations. Innovation, especially around comfort, smart features, and eco‑friendliness, will differentiate winners. While supply‑chain resilience and regulatory compliance remain critical, the shift to online channels offers scalable revenue streams. Overall, the market presents a compelling blend of stability and upside for stakeholders.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining secondary data extraction from industry reports, company filings, and reputable market databases with primary insights gathered through expert interviews across manufacturing, distribution, and clinical domains. Quantitative modeling applied the provided market size, forecast, and CAGR to project future values, while qualitative analysis interpreted trends, competitive dynamics, and strategic implications.

18. What is the scope and any limitations of this market research?

The scope covers global disposable incontinence products segmented by type, user category, and distribution channel, focusing on the period 2025‑2032. Geographic coverage includes all major regions, with emphasis on market size, growth drivers, and competitive landscape. Limitations stem from the reliance on publicly available data and the absence of granular regional revenue figures, which constrains precise market‑share calculations.

19. Which companies have made notable recent developments in the Disposable Incontinence Products Market?

Recent activities include Kimberly Clark’s launch of a new breathable adult diaper line featuring odor‑control technology; Becton Dickinson’s acquisition of a catheter‑design start‑up to enhance its smart‑catheter portfolio; ConvaTec’s partnership with a major e‑commerce platform to expand direct‑to‑consumer sales; and Abena’s introduction of a biodegradable under‑pad series targeting environmentally conscious consumers. These developments illustrate the industry’s focus on innovation, channel diversification, and sustainability.