What is the Calcium Carbonate Market Overview – definition, scope, and significance?

Calcium carbonate is a versatile inorganic compound used as a filler, pigment, and functional additive across multiple industries. The market encompasses the production, processing, and distribution of both ground calcium carbonate (GCC) and precipitated calcium carbonate (PCC). Its scope stretches from traditional applications such as paper and paints to high‑performance sectors like plastics, adhesives, sealants, and building‑construction materials. The significance of the market lies in its role as a cost‑effective, environmentally benign material that enhances product durability, brightness, and mechanical properties while supporting sustainability targets worldwide.

What are the Calcium Carbonate Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising demand for lightweight composites in automotive and construction, increasing paper consumption in emerging economies, and growth of the plastics sector seeking cost‑effective fillers. Environmental regulations favor calcium carbonate because it reduces reliance on petro‑based fillers, creating an opportunity for green product lines. Restraints involve price volatility of raw limestone and transportation costs due to the bulk nature of the product. Challenges stem from competition with alternative minerals such as talc and silica, and the need for consistent particle‑size control in high‑spec applications. Opportunities arise from the development of nano‑calcium carbonate for advanced coatings and the expansion of PCC in high‑purity pharmaceutical and food packaging markets.

What are the Calcium Carbonate Market Growth Trends – current and emerging trends shaping the market?

Current trends show a shift toward PCC for applications requiring superior brightness and dispersibility, especially in premium paper and high‑performance plastics. Emerging trends include the integration of calcium carbonate in 3D‑printed polymers to improve printability and reduce material costs. The construction sector is adopting calcium carbonate‑based additives to improve the fire‑resistance and acoustic performance of cementitious products. Additionally, manufacturers are investing in greener production processes, such as CO₂‑capture technologies that turn waste gases into useful calcium carbonate, aligning with circular‑economy principles.

How has COVID‑19 impacted the Calcium Carbonate Market – pandemic effects and recovery trajectory?

The COVID‑19 pandemic caused a temporary slowdown in demand for paper, packaging, and construction as lockdowns reduced industrial activity. Supply chain disruptions led to short‑term logistics bottlenecks, especially for bulk shipments. However, the rapid growth of e‑commerce and the rebound in packaging demand accelerated recovery in the latter half of 2020. By 2022, the market regained momentum, with a pronounced shift toward medical‑grade and food‑contact calcium carbonate, supporting a resilient post‑pandemic trajectory.

What does the Calcium Carbonate Market Competitive Landscape look like – major competitors and market consolidation?

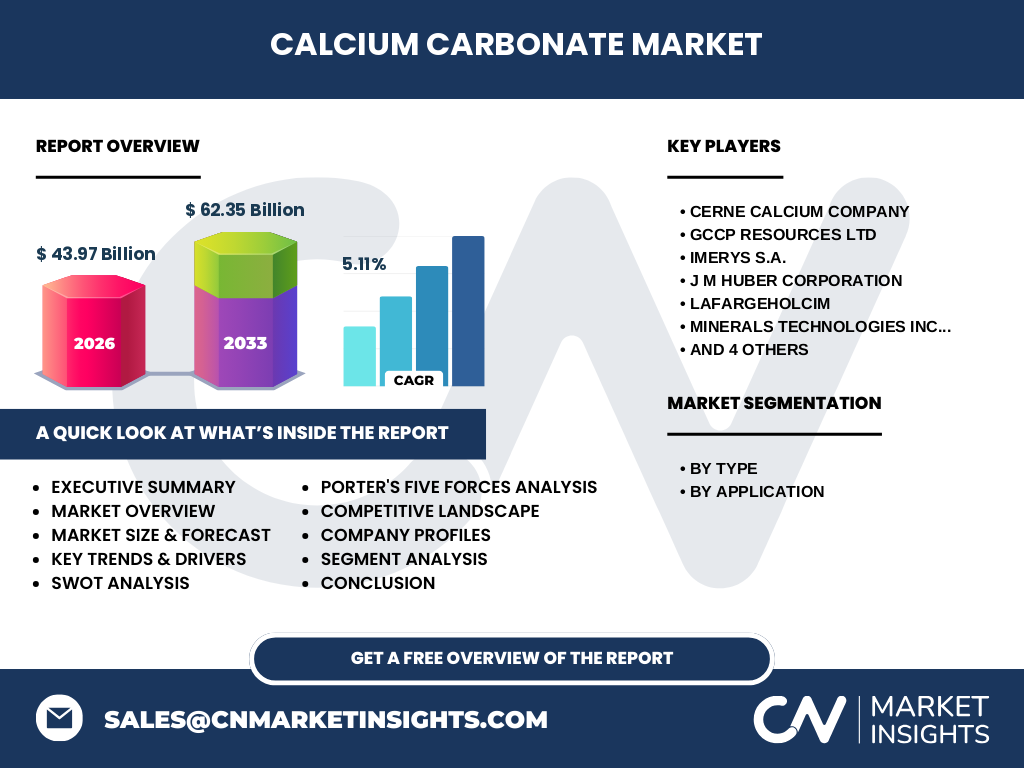

The competitive landscape is fragmented, comprising a mix of multinational conglomerates and regional specialists. Leading players such as Imerys S.A., Omya AG, and Lafargeholcim dominate the global supply chain through extensive limestone reserves and integrated processing facilities. Companies like Cerne Calcium Company, GCCP Resources Ltd., and Mississippi Lime Company focus on niche segments, offering tailored GCC or PCC grades. Recent consolidation activities include strategic joint ventures to expand geographic reach and technology sharing agreements aimed at enhancing product purity and reducing production footprints.

What are the key points in the Executive Summary – high‑level overview and key findings about the Calcium Carbonate Market?

The calcium carbonate market is valued at $43.97 billion in 2026 and is projected to reach $62.35 billion by 2033, reflecting a compound annual growth rate (CAGR) of 5.11 %. Growth is driven by expanding applications in paper, plastics, paints, adhesives, and construction. PCC is gaining market share due to its superior performance attributes, while GCC remains essential for bulk, cost‑sensitive uses. Regional demand is strongest in Asia‑Pacific, driven by urbanization and infrastructure investment, whereas Europe focuses on high‑purity applications. Competitive dynamics are marked by both large multinationals and agile regional firms, fostering innovation and strategic collaborations.

What is the Calcium Carbonate Market Forecast – projections for the 2025‑2032 period?

Based on the provided CAGR of 5.11 %, the market is expected to sustain steady expansion through 2032. The forecast indicates continued diversification of end‑use applications, with plastics and construction materials contributing the largest incremental volumes. PCC growth is anticipated to outpace GCC due to rising demand for high‑performance fillers in automotive lightweighting and specialty coatings. Investment in advanced manufacturing and sustainability initiatives will further bolster market resilience, supporting a trajectory that keeps the market above $60 billion by the early 2030s.

What is the Calcium Carbonate Market Size and Share by Segmentation – breakdown by type and application?

By type, the market is divided into Ground Calcium Carbonate (GCC) and Precipitated Calcium Carbonate (PCC). GCC accounts for the larger volume share owing to its lower cost and suitability for bulk applications such as building materials and standard paints. PCC, while representing a smaller volume, commands a higher value share because of its premium characteristics required in paper, high‑clarity plastics, and specialty coatings. By application, paper remains a core segment, followed by plastic, paints and coatings, adhesives and sealants, and building & construction, each contributing to the overall market mix.

What is the Global Calcium Carbonate Market Size and Share by Region – geographic distribution?

The global market is geographically dispersed, with Asia‑Pacific holding the dominant share due to rapid industrialization, large‑scale construction projects, and expanding packaging demand. North America follows, supported by a mature plastics industry and stringent environmental standards that favor calcium carbonate as a sustainable filler. Europe maintains a strong presence in high‑purity PCC applications for paper and specialty coatings. Emerging markets in Latin America and the Middle East show incremental growth as infrastructure development accelerates.

What does the Regional Analysis of the Calcium Carbonate Market reveal – detailed regional market performance?

In Asia‑Pacific, China and India drive growth through massive paper production, plastic extrusion, and construction activities. Southeast Asian nations contribute via rising paint and coating consumption. North America’s market is characterized by innovation in nanocalcium carbonate for advanced coatings and a push toward greener manufacturing processes. Europe’s performance is anchored by demand for high‑brightness PCC in premium paper and eco‑friendly building materials. Latin America experiences modest gains linked to expanding petrochemical complexes, while the Middle East benefits from abundant limestone resources and strategic export hubs.

Who are the Leading Company Profiles in the Calcium Carbonate Market – industry players and strategies?

Imerys S.A. leverages a vertically integrated model, controlling limestone mines and advanced processing plants to offer a broad grade spectrum. Omya AG focuses on specialty PCC solutions, investing in research to develop nano‑scale products for high‑performance coatings. Lafargeholcim utilizes its construction‑materials portfolio to embed calcium carbonate into cement and aggregates. J M Huber Corporation emphasizes sustainable sourcing and circular‑economy initiatives, converting industrial CO₂ into usable calcium carbonate. Smaller firms like Cerne Calcium Company and Mississippi Lime Company differentiate through customized GCC blends for regional markets.

What does Porter’s Five Forces Analysis of the Calcium Carbonate Market indicate – competitive forces assessment?

Threat of New Entrants: Moderate; high capital requirements for limestone extraction and processing create barriers, but niche players can enter with specialized PCC technologies. Bargaining Power of Suppliers: Low to moderate; limestone is abundant, but logistics and transportation costs can influence pricing. Bargaining Power of Buyers: Moderate; large manufacturers in paper and plastics can negotiate volume discounts, yet product quality requirements limit switching. Threat of Substitutes: Moderate; alternatives like talc, silica, and bio‑based fillers compete, especially where performance specifications differ. Industry Rivalry: High; numerous global and regional firms compete on price, product purity, and sustainability credentials, driving continuous innovation.

What are the SWOT Analysis findings for the Calcium Carbonate Market – strengths, weaknesses, opportunities, threats?

Strengths: Low raw‑material cost, broad applicability, and recognized environmental benefits. Weaknesses: Bulk transportation challenges and dependence on limestone quality. Opportunities: Development of nano‑calcium carbonate, expansion into high‑purity pharmaceutical and food‑grade markets, and adoption of carbon‑capture production methods. Threats: Volatile fuel and logistics costs, potential regulatory changes on mining activities, and competitive pressure from emerging bio‑based fillers.

How is the Calcium Carbonate Market Value Chain structured – industry structure and value flow?

The value chain begins with limestone mining, followed by crushing, grinding (for GCC) or precipitation (for PCC). Subsequent steps include classification, surface treatment, and packaging. Distribution channels consist of bulk shipments to large manufacturers and specialized packaging for premium PCC customers. End‑users—paper mills, plastic converters, paint manufacturers, and construction material producers—integrate calcium carbonate into their formulations, completing the chain. Value‑added services such as technical support, custom grading, and sustainability consulting enhance customer relationships and capture additional margin.

What are the Key Investment Insights in the Calcium Carbonate Market – strategic investment recommendations?

Investors should prioritize companies with integrated mining‑to‑product capabilities that can mitigate logistical costs and ensure consistent product quality. Targets with strong R&D pipelines in PCC and nano‑calcium carbonate offer higher margin potential. Partnerships that enable access to emerging markets in Asia‑Pacific provide growth leverage. Sustainable production initiatives—particularly those converting industrial CO₂ into calcium carbonate—are likely to attract ESG‑focused capital and differentiate market participants.

What is the Calcium Carbonate Market Conclusion – summary and key takeaways?

The calcium carbonate market is on a robust growth path, supported by a 5.11 % CAGR and a projected valuation of $62.35 billion by 2033. Its versatility across paper, plastics, paints, adhesives, and construction underpins stable demand. While logistical and competitive pressures persist, opportunities in high‑purity PCC, nano‑scale products, and sustainable manufacturing present compelling avenues for differentiation. Companies that invest in technology, regional expansion, and ESG practices are best positioned to capture future market share.

What Research Methodology was used – how this research was conducted?

The study combines primary interviews with industry experts, surveys of key end‑users, and secondary data collection from company reports, trade publications, and government statistics. Market sizing employs a top‑down approach using known revenue figures and growth rates, while segmentation analysis applies bottom‑up validation through volume‑to‑value conversions. Forecasting utilizes a compound annual growth rate (CAGR) model calibrated to historical trends and macro‑economic indicators.

What is the Research Scope – coverage and limitations?

The scope covers global calcium carbonate production, processing, and end‑use applications across the defined type and application segments. Geographic coverage includes all major regions, with emphasis on markets where detailed data are available. Limitations stem from the reliance on publicly disclosed financials and the exclusion of confidential proprietary information, which may affect granularity of regional market share estimates.

Who are the Key Companies and Recent Developments in the Calcium Carbonate Market – top companies and their recent announcements?

Key companies include Cerne Calcium Company, GCCP Resources Ltd., Imerys S.A., J M Huber Corporation, Lafargeholcim, Minerals Technologies Inc., Mississippi Lime Company, Okutama Kogyo Co., Ltd., Omya AG, and SCHAEFER KALK GmbH & Co. KG. Recent developments feature Imerys’s launch of a new high‑purity PCC line for specialty paper, Omya’s partnership with a leading automotive supplier to develop lightweight plastic composites, and Lafargeholcim’s investment in a carbon‑capture plant that converts captured CO₂ into market‑grade calcium carbonate, reinforcing its sustainability agenda.