What is the Feminine Hygiene Products Market Overview – Definition, scope, and significance?

The Feminine Hygiene Products Market encompasses all consumable and reusable items designed for women’s personal care, including menstrual care products, cleaning and deodorizing solutions, and specialized underwear. The scope covers manufacturing, distribution, and retail across both traditional brick‑and‑mortar and online channels. Its significance is driven by growing awareness of women's health, rising disposable incomes, and cultural shifts toward hygiene and comfort, making it a vital segment of the broader consumer goods industry.

What are the main drivers, restraints, challenges, and opportunities shaping the Feminine Hygiene Products Market?

Key drivers include increasing female workforce participation, heightened health consciousness, and demand for eco‑friendly alternatives such as reusable underwear and menstrual cups. Restraints stem from price sensitivity in emerging economies and regulatory scrutiny over product safety. Challenges involve supply‑chain disruptions and cultural taboos that limit market penetration in certain regions. Opportunities arise from technological innovation, custom‑fit solutions, and expanding e‑commerce platforms that reduce distribution barriers.

What growth trends are currently influencing the Feminine Hygiene Products Market?

Current trends feature a shift toward sustainable products, with consumers preferring biodegradable pads and reusable menstrual cups. Personalization is emerging through product lines tailored to different flow levels and skin sensitivities. Digital engagement, including subscription services and influencer‑driven marketing, is reshaping purchasing behavior. Additionally, health‑focused formulations—such as pH‑balanced cleansers—are gaining traction among health‑aware consumers.

How has COVID‑19 impacted the Feminine Hygiene Products Market, and what is the recovery trajectory?

The pandemic caused short‑term supply constraints and spikes in demand for essential hygiene items, leading to temporary stockouts. Lockdown measures accelerated online sales, prompting many brands to strengthen digital channels. As economies reopen, the market is recovering steadily, with a return to pre‑pandemic growth rates and continued emphasis on health and safety that sustains higher consumer vigilance.

Who are the major competitors in the Feminine Hygiene Products Market, and what is the state of market consolidation?

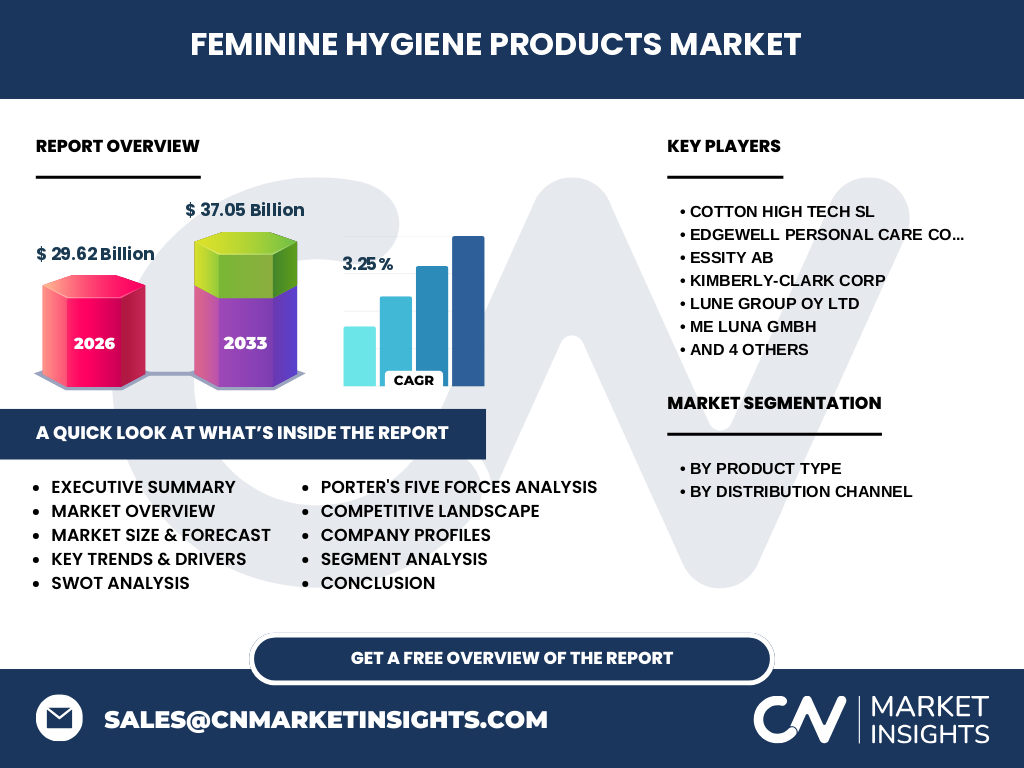

Leading players include Cotton High Tech SL, Edgewell Personal Care Co., Essity AB, Kimberly‑Clark Corp, Lune Group Oy Ltd, Me Luna GmbH, Mooncup Ltd, Ontex BV, The Procter & Gamble Co, and Wuka Ltd. The market exhibits moderate consolidation, with large multinationals leveraging extensive distribution networks while niche innovators focus on sustainability and specialty products. Strategic partnerships and acquisitions are common as firms aim to broaden product portfolios and geographic reach.

What are the key findings highlighted in the Executive Summary of the Feminine Hygiene Products Market?

The market is valued at $29.62 billion in 2026 and is projected to reach $37.05 billion by 2033, reflecting a CAGR of 3.25 %. Growth is propelled by rising health awareness, sustainability trends, and expanding online retail. Competitive dynamics show both global giants and agile startups competing on quality, innovation, and price. Regional demand varies, with mature markets emphasizing premium segments while emerging regions focus on affordability.

What is the forecast for the Feminine Hygiene Products Market for the 2025‑2032 period?

Based on the provided CAGR of 3.25 %, the market is expected to maintain steady expansion, moving from a 2026 base of $29.62 billion to approximately $37.05 billion by 2033. This trajectory suggests consistent year‑over‑year growth, driven by product innovation, broader distribution channels, and increasing consumer willingness to invest in health‑focused personal care solutions.

How is the Feminine Hygiene Products Market sized and shared by product type and distribution channel?

By product type, the market is divided into Menstrual Care Products, Cleaning and Deodorizing Products, and Feminine Hygiene Products Underwear. By distribution channel, sales occur through Supermarkets and Hypermarkets, Drug Stores and Pharmacies, Health and Beauty Stores, and Online Retail. While exact numerical shares are not disclosed, each segment contributes to the overall market value, with online retail showing rapid growth due to shifting consumer purchase habits.

What is the global geographic distribution of the Feminine Hygiene Products Market?

The market spans multiple regions, including North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa. Each region demonstrates unique demand drivers—such as high disposable income in North America and Europe, and expanding middle‑class populations in Asia‑Pacific. The global footprint ensures diversified revenue streams and opportunities for localized product adaptations.

What are the detailed regional performance insights for the Feminine Hygiene Products Market?

In North America, premium and organic product lines dominate, supported by strong retail infrastructure. Europe emphasizes sustainability, with a growing preference for reusable options. Asia‑Pacific registers the fastest volume growth, propelled by population size and increasing urbanization. Latin America and the Middle East & Africa show moderate growth, where price‑sensitive segments and expanding retail networks shape market dynamics.

Which companies lead the Feminine Hygiene Products Market, and what strategies do they employ?

Key leaders—such as Procter & Gamble, Kimberly‑Clark, and Essity—focus on extensive R&D, brand diversification, and strategic acquisitions to broaden their portfolios. Niche firms like Mooncup Ltd and Me Luna GmbH prioritize sustainability and targeted marketing to capture eco‑conscious consumers. Across the board, firms are investing in digital commerce, private‑label partnerships, and product differentiation to sustain competitive advantage.

How does Porter’s Five Forces analysis apply to the Feminine Hygiene Products Market?

Threat of new entrants is moderate due to high brand loyalty and regulatory barriers. Bargaining power of suppliers is relatively low, as raw material markets are competitive. Bargaining power of buyers is high, driven by abundant product choices and price sensitivity. Threat of substitutes is moderate, with reusable products offering alternatives to disposables. Industry rivalry is intense, with numerous global and regional players competing on innovation, pricing, and distribution.

What are the SWOT highlights for the Feminine Hygiene Products Market?

Strengths: Strong demand fundamentals, established distribution networks, and continuous product innovation. Weaknesses: Sensitivity to raw‑material cost fluctuations and dependence on retail shelf space. Opportunities: Expansion of sustainable product lines, penetration of emerging markets, and growth of direct‑to‑consumer channels. Threats: Regulatory changes, cultural barriers in certain regions, and aggressive price competition.

How is the value chain structured in the Feminine Hygiene Products Market?

The value chain begins with raw‑material sourcing (cotton, polymers, absorbent gels), followed by formulation, manufacturing, and packaging. Distribution proceeds through wholesale aggregators to retailers—both offline (supermarkets, pharmacies) and online platforms. End‑users purchase through various channels, while after‑sales services include consumer education, subscription management, and waste‑recycling initiatives for reusable products.

What key investment insights can be drawn for the Feminine Hygiene Products Market?

Investors should target companies with robust sustainable portfolios and strong e‑commerce capabilities. Growth potential lies in emerging markets where hygiene awareness is rising, as well as in premium segments that command higher margins. Strategic acquisitions of innovative startups can accelerate entry into niche categories such as menstrual cups and biodegradable pads, offering differentiation in a crowded marketplace.

What conclusions can be drawn about the Feminine Hygiene Products Market?

The market is on a steady growth path, backed by health awareness, sustainability trends, and expanding digital sales channels. While competitive pressure remains high, firms that combine product innovation with flexible distribution strategies are best positioned to capture value. The projected increase to $37.05 billion by 2033 underscores the sector’s resilience and long‑term attractiveness.

What research methodology underpins this market analysis?

The study employs a mixed‑method approach, integrating primary interviews with industry experts, secondary data from company reports, trade publications, and reputable market databases. Quantitative analysis includes trend extrapolation using the disclosed CAGR of 3.25 %. Qualitative insights are derived from SWOT, Porter’s Five Forces, and value‑chain assessments to ensure a comprehensive view.

What is the scope of this research, and what limitations should be considered?

The scope covers global market size, segment breakdown by product type and distribution channel, regional performance, and competitive profiling of leading firms. Limitations include reliance on publicly available financial figures and the exclusion of proprietary market share percentages. Therefore, estimates are presented within the constraints of the disclosed data.

Which key companies have made recent developments in the Feminine Hygiene Products Market?

Recent activities include Procter & Gamble expanding its organic menstrual line, Kimberly‑Clark launching a new biodegradable pad series, and Essity investing in reusable underwear technology. Mooncup Ltd announced a partnership with online retailers to boost subscription sales, while Edgewell Personal Care introduced a premium deodorizing wash. These developments reflect a focus on sustainability, innovation, and digital distribution.