What is the Broaching Machines Market Overview – definition, scope, and significance?

The Broaching Machines Market comprises manufacturers and suppliers of specialized cutting tools designed to remove material with a single-pass motion. Broaching machines include horizontal, vertical, and surface types, serving end‑users such as automotive, metal fabrication, aerospace & defense, and oil & gas. The market’s significance lies in its ability to deliver high‑precision, repeatable components with superior surface finish, reducing machining time and waste, which is critical for sectors that demand tight tolerances and high productivity.

What are the main drivers, restraints, challenges, and opportunities in the Broaching Machines Market?

Key drivers include rising demand for lightweight, high‑strength components in automotive and aerospace, and the need for efficient mass‑production of complex parts. Restraints stem from high initial capital costs and the niche expertise required to operate advanced broaching equipment. Challenges involve limited awareness of broaching benefits among smaller manufacturers and competition from alternative machining technologies. Opportunities arise from automation integration, development of hybrid broaching– CNC systems, and expanding applications in renewable energy and oil‑gas infrastructure.

What growth trends are currently shaping the Broaching Machines Market?

Current trends feature a shift toward CNC‑controlled broaching machines that enhance precision and reduce operator dependence. Manufacturers are also embedding IoT sensors for predictive maintenance, extending machine uptime. Another emerging trend is the adoption of modular broaching heads, allowing quick change‑over for different profiles, which improves flexibility for low‑batch production. Sustainability concerns are encouraging the use of high‑efficiency motors and recyclable cutting tools.

How did COVID‑19 impact the Broaching Machines Market and what is the recovery trajectory?

The pandemic caused temporary shutdowns of automotive and aerospace plants, leading to reduced orders for new broaching equipment in 2020‑21. However, the market demonstrated resilience as existing machines supported re‑tooling for pandemic‑related products, such as medical device components. Post‑2021, demand rebounded strongly, driven by pent‑up orders and a resurgence in vehicle production, setting the market on a clear recovery path that aligns with the projected CAGR of 4.85%.

Who are the major competitors and what is the consolidation landscape in the Broaching Machines Market?

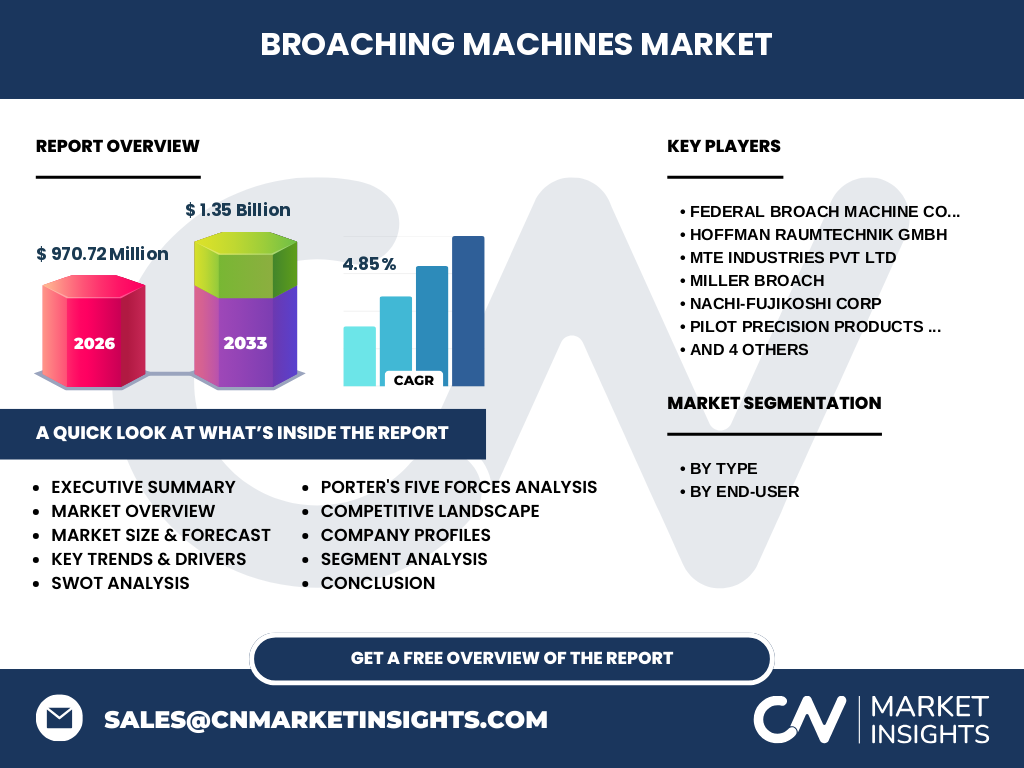

Key players include Federal Broach Machine Company, Hoffman Raumtechnik GmbH, MTE Industries Pvt Ltd, Miller Broach, Nachi‑Fujikoshi Corp, Pilot Precision Products (DuPont), Stenhoj Hydraulik, Suntech Landriani Machine Tools Pvt Ltd., The Ohio Broach & Machine Co., and Yeoshe Hydraulics Technology Co., Ltd. Consolidation is modest, with strategic alliances and joint ventures focused on technology sharing rather than large‑scale mergers, reflecting a market that values specialized expertise.

What are the high‑level findings in the Executive Summary of the Broaching Machines Market?

The market is valued at USD 970.72 million in 2026 and is forecast to reach USD 1.35 billion by 2033, growing at a 4.85% CAGR. Horizontal and vertical broaching machines dominate the type segment, while automotive and metal fabrication are the largest end‑users. Technological advancements, such as CNC integration and IoT‑enabled monitoring, are primary growth catalysts. Competitive dynamics are characterized by a mix of established OEMs and emerging regional manufacturers.

What are the market forecasts for 2025‑2032?

Based on the provided CAGR of 4.85%, the market is expected to expand steadily from the 2026 base of USD 970.72 million to surpass USD 1.35 billion by 2033. This trajectory signals consistent demand across core end‑user sectors, with incremental growth each year driven by automation and the rollout of next‑generation broaching solutions.

How is the market sized and shared by segmentation?

By type, the market is divided into Horizontal Broaching Machine, Vertical Broaching Machine, and Surface Broaching Machine, each serving distinct production needs. By end‑user, the segmentation comprises Automotive, Metal Fabrication, Aerospace & Defense, and Oil & Gas. While exact share percentages are not disclosed, these categories collectively represent the full market landscape, guiding manufacturers to target specific applications and customer segments.

What is the geographic distribution of the Global Broaching Machines Market?

The market exhibits a worldwide presence, with key activities in North America, Europe, Asia‑Pacific, and the Middle East & Africa. Regional demand aligns with the concentration of automotive assembly plants, aerospace hubs, and oil‑gas infrastructure projects, ensuring a balanced global footprint for broaching machine suppliers.

What are the detailed regional market performances?

North America continues to lead in technology adoption, especially in aerospace and defense applications. Europe shows strong growth in automotive component manufacturing, supported by stringent emission standards. Asia‑Pacific is the fastest‑growing region, driven by expanding automotive production and rising metal‑fabrication capacity in China and India. The Middle East & Africa contribute niche demand, primarily from oil‑gas sector expansions.

Which companies lead the Broaching Machines Market and what are their strategies?

Leading firms such as Federal Broach Machine Company and Nachi‑Fujikoshi Corp focus on expanding product portfolios with CNC‑enabled and hybrid models. Hoffman Raumtechnik GmbH emphasizes precision engineering for aerospace, while MTE Industries Pvt Ltd targets cost‑effective solutions for emerging markets. Recent strategic moves include partnerships for digital monitoring, acquisitions of specialized tooling firms, and investments in R&D for high‑speed broaching heads.

How does Porter’s Five Forces shape the Broaching Machines Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of buyers is elevated as large OEMs can negotiate pricing and demand customization. Bargaining power of suppliers is limited because key components such as high‑grade steel are widely sourced. Threat of substitutes remains low; alternative processes cannot match the speed and finish of broaching for many applications. Industry rivalry is intense among specialized manufacturers seeking differentiation through technology and service support.

What are the SWOT highlights for the Broaching Machines Market?

Strengths: High precision, single‑pass efficiency, and strong demand in high‑value sectors. Weaknesses: High upfront cost and limited awareness among small firms. Opportunities: Automation, IoT integration, and expansion into renewable energy components. Threats: Economic downturns affecting capital spending and rapid advances in alternative additive manufacturing technologies.

How is the value chain structured in the Broaching Machines Market?

The value chain begins with raw‑material suppliers (steel, alloys), followed by component manufacturers (gearboxes, hydraulic systems). These feed into machine assemblers who integrate CNC controls and safety systems. Distributors and system integrators then deliver finished broaching machines to end‑users, who may also engage aftermarket services such as maintenance, tool replacement, and software upgrades.

What investment insights are critical for stakeholders in the Broaching Machines Market?

Investors should focus on companies with strong R&D pipelines for CNC and IoT capabilities, as these technologies drive future demand. Geographic diversification into Asia‑Pacific offers growth potential, while partnerships with automotive OEMs can secure long‑term contracts. Monitoring regulatory trends in emission standards and defense spending can also uncover niche investment opportunities.

What conclusions can be drawn about the Broaching Machines Market?

The market is on a steady growth path, underpinned by technological upgrades and expanding applications across automotive, aerospace, and oil‑gas sectors. Despite cost barriers, the shift toward automation and digitalization is likely to boost adoption rates. Competitive dynamics favor firms that combine precision engineering with smart‑machine services.

How was the research conducted for this report?

The study employed a combination of primary interviews with industry experts, secondary data extraction from company reports, trade publications, and reputable market databases. Quantitative analysis used the known market size (USD 970.72 million in 2026) and projected growth (USD 1.35 billion by 2033) to calculate the 4.85% CAGR, which underpins the forecasting model.

What is the scope of this research?

The research covers global broaching machine manufacturers, product types, end‑user applications, and regional market dynamics. It excludes detailed financial statements of individual companies and does not provide granular market share percentages beyond the overall market size and forecast figures supplied.

Which key companies have recent developments in the Broaching Machines Market?

Federal Broach Machine Company announced a new line of IoT‑enabled horizontal broachers. Nachi‑Fujikoshi Corp launched a high‑speed vertical broach with advanced cooling. Miller Broach entered a joint venture with an Asian distributor to expand its surface broaching portfolio. Stenhoj Hydraulik introduced a modular hydraulic system that reduces change‑over time by 30%.