What is the Cartesian Robot Market Overview – definition, scope, and significance?

The Cartesian robot market comprises manufacturers and suppliers of linear robotic systems that move along orthogonal X, Y, and Z axes. These robots, also known as gantry or linear robots, are characterized by their high positional accuracy, repeatability, and simple control architecture. The market’s scope includes a broad range of applications—from precise pick‑and‑place operations in electronics assembly to heavy‑load material handling in automotive factories. Their significance lies in enabling automation of repetitive tasks, reducing labor costs, improving product quality, and supporting the Industry 4.0 transition through easy integration with vision systems and IoT platforms.

What are the primary drivers, restraints, challenges, and opportunities shaping the Cartesian Robot Market?

Key drivers include rising demand for automation in manufacturing, the need for high‑precision positioning in electronics and medical device assembly, and cost‑effective alternatives to multi‑axis articulated robots. Restraints stem from the relatively limited flexibility of Cartesian designs compared with articulated solutions, which can constrain adoption in complex three‑dimensional tasks. Challenges involve integrating these robots with advanced AI‑based vision and safety systems, as well as addressing skill gaps in programming. Opportunities arise from the growing trend toward modular, plug‑and‑play robot kits, the expansion of e‑commerce warehousing that requires fast, accurate palletizing, and the emergence of collaborative Cartesian robots that can safely work alongside human operators.

What growth trends are currently influencing the Cartesian Robot Market?

Current trends feature a shift toward higher payload capacities and longer travel ranges to serve large‑scale assembly lines. Manufacturers are embedding edge‑computing capabilities for real‑time diagnostics and predictive maintenance. There is also a noticeable move toward open‑source control software, which reduces integration costs and accelerates customization. Emerging trends include the development of hybrid systems that combine Cartesian axes with rotary joints, delivering greater flexibility while retaining the precision advantages of linear motion.

How has COVID‑19 impacted the Cartesian Robot Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains for key components such as linear guides and motor drives, causing short‑term order delays. However, the crisis accelerated automation adoption as manufacturers sought to maintain production with reduced on‑site labor. Post‑2020, demand rebounded strongly, with firms reallocating capital expenditures toward robotic cells to improve resilience. The recovery trajectory is positive, driven by continued emphasis on workforce safety and the need to meet surging consumer demand in sectors like food‑and‑beverage and electronics.

Who are the major competitors in the Cartesian Robot Market and what is the level of market consolidation?

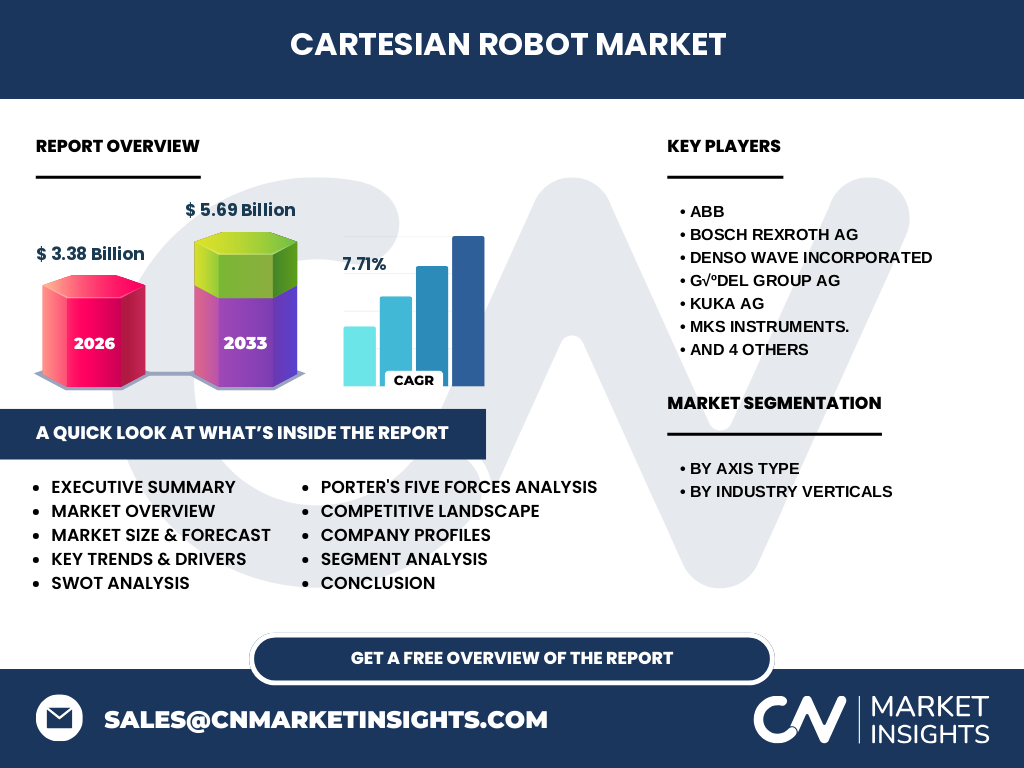

The market features a mix of global industrial giants and specialized niche players. Prominent competitors include ABB, Bosch Rexroth AG, DENSO WAVE INCORPORATED, G√ºdel Group AG, KUKA AG, MKS Instruments, Midea Group, Seiko Epson Corporation, Shibaura Machine CO., LTD, and Yamaha Motor Co., Ltd. Consolidation has remained moderate; while large firms continue to acquire complementary technology startups, many specialized firms retain independent operations to focus on vertical‑specific solutions, maintaining a competitive but fragmented landscape.

What are the key findings highlighted in the Executive Summary of the Cartesian Robot Market?

The market is projected to expand from a 2026 base of $3.38 billion to $5.69 billion by 2033, reflecting a robust CAGR of 7.71 %. Growth is powered by increasing automation in manufacturing and automotive sectors, coupled with the emergence of collaborative and hybrid Cartesian systems. Regional demand is strongest in Asia‑Pacific, driven by large‑scale production facilities and government incentives for smart manufacturing. Competitive dynamics emphasize innovation in payload capacity, software openness, and safety features, positioning the market for sustained expansion.

What are the forecasted market dynamics for the Cartesian Robot Market from 2025 to 2032?

Forecasts indicate a steady upward trajectory, with the market expected to reach approximately $5.69 billion by 2033. Annual growth will be driven by continued investment in Industry 4.0 initiatives, especially in high‑mix, low‑volume production environments that benefit from the adaptability of Cartesian robots. Anticipated product launches focusing on integrated vision and AI will further stimulate demand, while cost reductions in sensor and motor technology will broaden adoption across small and medium‑sized enterprises.

How is the Cartesian Robot Market sized and shared across key segments?

Segmentation by axis type includes 1‑Axis, 2‑Axis, 3‑Axis, and 4‑Axis configurations, each targeting distinct application needs. Simpler 1‑Axis models dominate low‑cost pick‑and‑place tasks, while 4‑Axis systems are favored for complex assembly and machining processes. By industry vertical, manufacturing holds the largest share, reflecting its broad use in material handling and assembly. Automotive and electrical & electronics follow closely, leveraging high precision for component placement. Food & beverages and chemicals & petrochemicals represent niche but growing segments, driven by hygienic design requirements and hazardous environment handling.

What is the global geographic distribution of the Cartesian Robot Market?

The market exhibits strong presence in North America, Europe, and Asia‑Pacific. Asia‑Pacific leads in absolute volume due to extensive manufacturing bases in China, Japan, and South Korea, supported by government automation incentives. Europe maintains a solid share, especially in automotive and high‑precision electronics manufacturing. North America shows steady growth, propelled by advanced robotics adoption in semiconductor and aerospace sectors.

What does a detailed regional analysis reveal about the Cartesian Robot Market’s performance?

In Asia‑Pacific, rapid industrialization and large‑scale factories drive high demand for 3‑Axis and 4‑Axis systems, with China accounting for a sizable portion of new installations. Europe’s market is characterized by a focus on safety standards and integration with collaborative robot frameworks, leading to higher adoption of hybrid Cartesian‑articulated solutions. North America emphasizes smart factory initiatives and retrofitting legacy lines, resulting in a preference for modular Cartesian kits that can be quickly deployed.

Which companies lead the Cartesian Robot Market and what are their strategic approaches?

ABB leverages its broad automation portfolio to offer integrated Cartesian solutions with advanced motion control. Bosch Rexroth focuses on modular designs and strong after‑sales service. KUKA emphasizes high payload capacities and seamless integration with its software ecosystem. Seiko Epson promotes compact, high‑speed models for electronics assembly. Yamaha Motor highlights energy‑efficient drives and customizable control interfaces. These leaders pursue strategies such as strategic partnerships, acquisition of AI vision firms, and expansion of regional service networks.

How does Porter’s Five Forces analysis apply to the Cartesian Robot Market?

• Threat of new entrants – Moderate; high capital requirements and technical expertise create barriers, yet the rise of open‑source platforms lowers entry hurdles. • Bargaining power of suppliers – Moderate; component suppliers for linear guides and precision motors are concentrated, but long‑term contracts mitigate risk. • Bargaining power of buyers – High; OEMs and system integrators can negotiate price and demand customization, driving suppliers to innovate. • Threat of substitutes – Low to moderate; while articulated robots can perform many similar tasks, they often lack the precision and simplicity that Cartesian systems provide for linear motions. • Industry rivalry – High; intense competition among established manufacturers leads to continuous product improvement and price competition.

What are the major strengths, weaknesses, opportunities, and threats identified in the SWOT analysis?

Strengths: High positional accuracy, simple control architecture, and scalability for various payloads.

Weaknesses: Limited flexibility for complex three‑dimensional paths and larger footprint compared with compact articulated robots.

Opportunities: Integration with AI‑driven vision, development of collaborative Cartesian robots, and expansion into emerging markets with government automation incentives.

Threats: Rapid advances in multi‑axis robots that could erode niche advantages, supply chain disruptions for precision components, and increasing price sensitivity among small manufacturers.

How is the Cartesian Robot Market value chain structured?

The value chain begins with raw material suppliers (steel, aluminum, precision bearings), proceeds to component manufacturers (motors, drives, sensors), followed by system integrators that assemble axes and control units. Next are software developers providing motion control, safety, and AI vision packages. Distributors and system integrators then deliver turnkey solutions to end‑users across various industries. After‑sales services, including maintenance, upgrades, and training, complete the chain, creating recurring revenue streams for manufacturers.

What key investment insights should stakeholders consider when entering the Cartesian Robot Market?

Investors should prioritize companies with strong R&D pipelines in AI integration and collaborative safety features, as these capabilities differentiate market leaders. Emphasis on modular, upgradeable designs can capture both new installations and retrofitting projects. Geographic diversification, particularly targeting Asia‑Pacific growth hubs, offers robust return potential. Partnerships with software firms that specialize in machine‑learning analytics can unlock higher‑margin service contracts, enhancing long‑term profitability.

What conclusions can be drawn about the future of the Cartesian Robot Market?

The Cartesian robot market is poised for solid, double‑digit growth driven by automation imperatives across multiple verticals. Its combination of precision, reliability, and evolving intelligence positions it as a cornerstone of modern manufacturing. While competition and technological shifts pose challenges, the sector’s adaptability and ongoing innovation forecast a resilient and expanding market through 2033 and beyond.

What research methodology was employed to compile this market report?

The study utilized a mixed‑method approach, combining primary interviews with industry experts, surveys of end‑users, and secondary data analysis from company filings, trade publications, and market databases. Quantitative data were validated through cross‑referencing multiple sources, while qualitative insights were derived from expert opinion and case studies. Forecast modeling applied a compound annual growth rate (CAGR) of 7.71 % based on historical trends and projected industry drivers.

What is the scope of this research and its coverage limitations?

The research covers global Cartesian robot market dynamics, focusing on axis‑type and industry‑vertical segmentation, and includes geographic analysis for major regions. It does not delve into detailed pricing structures or proprietary technology patents, and regional data is presented at a macro level without city‑specific breakdowns. The forecast horizon extends to 2033, reflecting available trend data.

Which key companies are highlighted and what recent developments have they announced?

ABB announced a new high‑speed Cartesian line featuring integrated cloud‑based analytics for predictive maintenance. Bosch Rexroth launched a modular 4‑Axis system with plug‑and‑play safety sensors aimed at the automotive sector. KUKA introduced a collaborative Cartesian robot that can operate within a 1.5‑meter safety radius of human workers. Seiko Epson released a compact 3‑Axis model optimized for PCB assembly, emphasizing reduced cycle times. Yamaha Motor unveiled energy‑efficient drives that lower operational electricity consumption by up to 15 %.