1. What is the Contract Management Software Market Overview – definition, scope, and significance?

The Contract Management Software (CMS) market encompasses solutions that automate the entire contract lifecycle—from draft creation, negotiation, approval, execution, to post‑signing compliance and renewal. These platforms centralize contract repositories, embed workflow automation, and provide analytics that help organizations enforce obligations, mitigate risk, and accelerate revenue cycles. The scope includes software products (stand‑alone or integrated suites) and associated services such as implementation, training, and support. Significance lies in the growing volume and complexity of contracts across industries, the need for regulatory compliance, and the strategic role that timely contract execution plays in cost control and business agility.

2. What are the Contract Management Software Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include digital transformation initiatives, heightened regulatory scrutiny (e.g., GDPR, HIPAA), and the demand for faster sales and procurement cycles. The shift toward cloud‑based delivery accelerates adoption due to lower upfront costs and scalability. Restraints stem from legacy system inertia, data security concerns, and the perceived complexity of migrating existing contracts. Challenges involve integrating CMS with ERP, CRM, and procurement platforms, and ensuring user adoption across legal, sales, and procurement teams. Opportunities arise from AI‑enabled contract analytics, contract‑as‑a‑service models, and expanding use cases in emerging verticals such as telehealth and autonomous logistics.

3. What are the current Contract Management Software Market Growth Trends?

Trend analysis shows a rapid move from on‑premise to cloud‑based solutions, driven by subscription models that align costs with usage. AI and machine learning are being embedded to automate clause extraction, risk scoring, and renewal alerts. Low‑code/no‑code configuration tools are democratizing CMS use beyond legal departments, enabling sales and procurement users to create templates quickly. Additionally, integration ecosystems are maturing, with APIs linking CMS to ERP, CRM, and e‑signature providers, creating end‑to‑end digital contract pipelines.

4. How has COVID‑19 impacted the Contract Management Software Market and what is the recovery trajectory?

The pandemic accelerated remote work and highlighted the limitations of paper‑based or locally stored contracts. Organizations rushed to adopt cloud‑based CMS to maintain business continuity, resulting in a noticeable uptick in deployments throughout 2020‑2021. Post‑pandemic, the market retains its momentum as firms recognize the long‑term efficiency gains of digital contracts, positioning the sector on a sustained growth path aligned with overall digital transformation budgets.

5. Who are the major competitors in the Contract Management Software Market and what is the level of market consolidation?

The competitive landscape is characterized by a mix of legacy enterprise software giants and specialized vendors. Prominent players include Agiloft Inc, Apttus Corporation, CobbleStone Software, ContractsWise, IBM Corporation, Icertis, JAGGAER, SAP SE, Wolters Kluwer, and Zycus Inc. While the market remains fragmented, recent years have seen strategic acquisitions—such as larger ERP providers buying niche CMS firms—to broaden end‑to‑end contract capabilities, indicating a moderate level of consolidation.

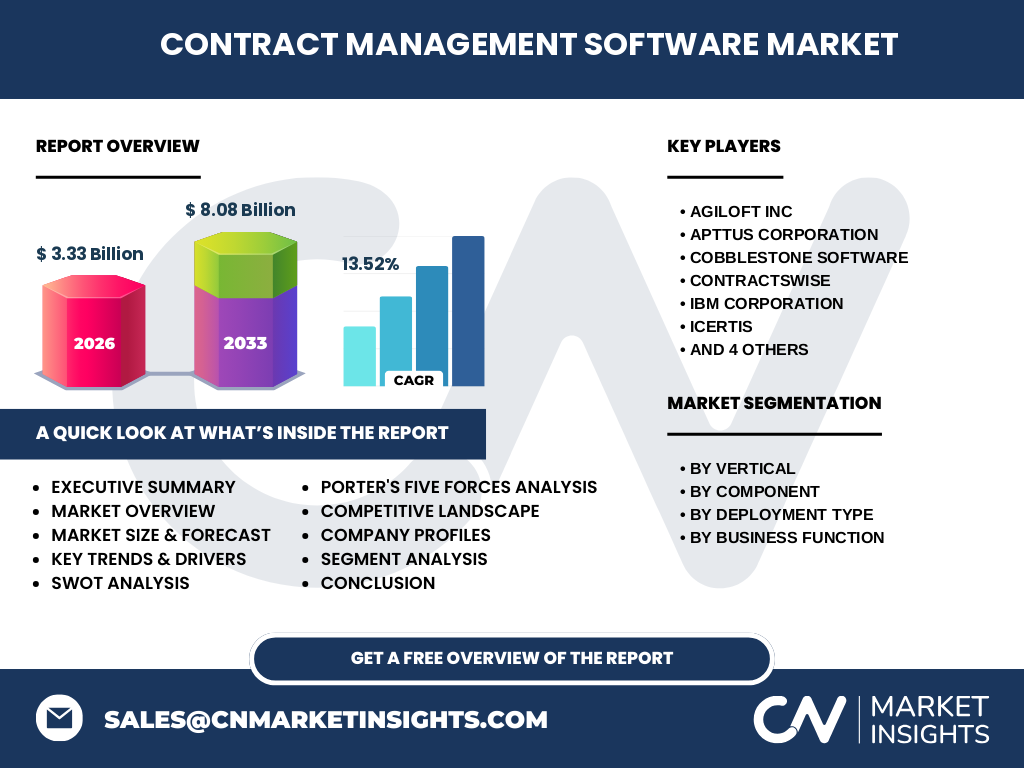

6. What are the key findings in the Executive Summary of the Contract Management Software Market?

The market is projected to expand from a 2026 valuation of US$3.33 billion to US$8.08 billion by 2033, reflecting a robust CAGR of 13.52 percent. Growth is fueled by cloud adoption, AI‑driven analytics, and cross‑functional demand from legal, sales, and procurement. Horizontal segments such as healthcare, BFSI, and manufacturing are leading adopters, while verticals like telecom and logistics are emerging fast. Competitive pressure is intensifying, prompting vendors to bundle services, enhance AI capabilities, and pursue strategic partnerships.

7. What is the Contract Management Software Market Forecast for 2025‑2032?

Based on the provided CAGR of 13.52 %, the market will continue an upward trajectory, reaching approximately US$8.08 billion by the end of 2033. The forecast period (2025‑2032) anticipates annual growth rates closely tracking the historical CAGR, with the bulk of expansion driven by cloud‑based deployments and AI‑enhanced modules. Mid‑term estimates suggest the market will surpass the US$5 billion mark by 2029, underscoring strong investor confidence.

8. How is the Contract Management Software Market sized and shared by segment?

Segmentation is defined across four dimensions. By vertical, the market serves Healthcare, Life Sciences, Transportation, Logistics, Government, Manufacturing, Telecom, IT, and BFSI, each leveraging CMS for regulatory compliance and operational efficiency. By component, Software accounts for the majority of spend, while Services (implementation, consulting, support) represent a growing ancillary revenue stream. Deployment type is split between Cloud‑Based—now the dominant model—and On‑Premise, which retains niche appeal for highly regulated environments. Business function segmentation shows Legal as the traditional user, with Sales and Procurement rapidly expanding their share as organizations seek to shorten quote‑to‑cash and source‑to‑pay cycles.

9. What is the global Contract Management Software Market size and share by region?

While precise regional dollar values are not disclosed, the market is globally distributed, with North America and Europe leading in early adoption due to mature regulatory frameworks and high enterprise software spend. APAC is emerging quickly, propelled by rapid digitalization in manufacturing, logistics, and telecom sectors. The Americas collectively hold the largest share, followed by Europe, with APAC displaying the highest growth rate.

10. What does the regional analysis of the Contract Management Software Market reveal?

North America benefits from a dense concentration of enterprise headquarters and a strong legal‑tech ecosystem, driving both cloud and on‑premise deployments. Europe’s GDPR environment fuels demand for compliance‑centric CMS features. In APAC, especially China, India, and Southeast Asia, the surge in e‑commerce, telecommunication, and smart logistics creates a fertile market for cloud‑native, AI‑enabled contract platforms. The Middle East and Africa are in early adoption stages, indicating future upside as multinational corporations expand operations there.

11. Which companies lead the Contract Management Software Market and what are their strategies?

Leading vendors such as Icertis and SAP SE focus on end‑to‑end digital transformation, integrating CMS with broader ERP and supply‑chain suites. IBM leverages its AI Watson capabilities to enhance contract analytics. Agiloft emphasizes low‑code customization, targeting businesses that need rapid adaptation. Apttus (now part of Conga) combines CPQ with CMS to serve sales‑centric workflows. Zycus and JAGGAER expand through procurement‑focused suites, while CobbleStone and ContractsWise cater to mid‑market legal departments. Partnerships with e‑signature providers and cloud platforms are common strategic moves.

12. How does Porter’s Five Forces analysis apply to the Contract Management Software Market?

Threat of New Entrants: Moderate – entry barriers exist due to required AI expertise and integration capabilities, yet SaaS models lower upfront investment. Bargaining Power of Buyers: High – enterprises can choose from many vendors and demand extensive customization. Bargaining Power of Suppliers: Low – core technology components (cloud infrastructure, AI libraries) are commoditized. Threat of Substitutes: Low to moderate – manual processes remain a fallback but are increasingly untenable. Industry Rivalry: Intense – numerous players compete on features, pricing, and ecosystem integration, driving rapid innovation.

13. What are the SWOT insights for the Contract Management Software Market?

Strengths: Proven cost‑savings, risk mitigation, and acceleration of revenue cycles; strong AI and automation roadmaps. Weaknesses: Integration complexity and lingering legacy system inertia. Opportunities: AI‑driven analytics, contract‑as‑a‑service, expansion into high‑growth verticals like telehealth and autonomous logistics. Threats: Data security concerns, regulatory changes that may require rapid re‑engineering, and price pressure from emerging low‑cost SaaS entrants.

14. How is the Contract Management Software value chain structured?

The value chain begins with research & development, focusing on AI, workflow automation, and API frameworks. Next, productization creates modular SaaS or on‑premise packages. Sales & marketing drive acquisition through direct enterprise sales, channel partners, and marketplace listings. Implementation services—configuration, data migration, and training—add value, followed by ongoing support, maintenance, and continuous innovation (e.g., new analytics modules). Feedback loops from customers fuel R&D, completing the cycle.

15. What key investment insights can be drawn for the Contract Management Software Market?

Investors should target vendors with strong AI capabilities and proven integration ecosystems, as these are differentiators that command premium pricing. Companies expanding into under‑penetrated verticals (e.g., Government, Telecom) and regions (APAC) present upside potential. Acquisitions of niche service providers can accelerate go‑to‑market speed and broaden service‑based revenue. Monitoring partnership announcements with cloud giants (AWS, Azure, Google Cloud) can signal future scaling opportunities.

16. What is the overall conclusion of the Contract Management Software Market analysis?

The Contract Management Software market is on a decisive growth path, driven by digital transformation, regulatory pressure, and the quest for operational efficiency. With a projected valuation of US$8.08 billion by 2033 and a healthy CAGR of 13.52 %, the sector offers compelling opportunities for vendors, investors, and enterprise buyers alike. Success will hinge on AI integration, seamless ecosystem connectivity, and the ability to serve diverse verticals and functional users.

17. How was the research for this report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data review from reputable market databases, and financial modeling based on disclosed market size (US$3.33 billion in 2026) and forecast (US$8.08 billion in 2033). Trend analysis leveraged technology adoption curves, while competitive assessment used publicly available information on product portfolios, mergers, and partnership announcements.

18. What is the scope of the research and its limitations?

The scope covers global Contract Management Software offerings, segmented by vertical, component, deployment type, and business function, and evaluates regional dynamics across major geographies. Limitations include reliance on publicly disclosed financials and the absence of granular market‑share percentages for individual vendors, which are proprietary.

19. Which key companies are leading the Contract Management Software Market and what recent developments have they announced?

Leading firms include Agiloft Inc, Apttus Corporation, CobbleStone Software, ContractsWise, IBM Corporation, Icertis, JAGGAER, SAP SE, Wolters Kluwer, and Zycus Inc. Recent developments feature Icertis’s launch of an AI‑driven risk analytics engine, SAP’s integration of CMS with its Business Network, IBM’s partnership with a leading e‑signature provider to embed secure signing, and Zycus’s expansion of its procurement‑focused contract suite into APAC. Agiloft announced a low‑code configuration update that reduces deployment time by 40 %, while Apttus introduced a bundled CPQ‑CMS solution aimed at accelerating the quote‑to‑cash cycle for enterprise sales teams.