1. North America Meat Snacks Market Overview - Definition, scope, and significance?

The North America meat snacks market comprises ready‑to‑eat protein‑rich products derived primarily from beef, turkey, pork or game meats. It spans a broad product portfolio—including jerky, sticks, strips, bites, bars and sausages—distributed through both direct (company‑owned stores, e‑commerce) and indirect channels (retail, foodservice). The market’s significance stems from rising consumer demand for convenient, high‑protein snack options that align with on‑the‑go lifestyles and evolving dietary preferences across the United States and Canada.

2. North America Meat Snacks Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include increasing health consciousness, the popularity of high‑protein diets, and the expansion of e‑commerce which enhances product accessibility. Restraints involve stringent labeling regulations and rising raw material costs, while challenges are presented by intense competition from plant‑based alternatives and fluctuating consumer taste trends. Opportunities arise from product innovation (e.g., organic, low‑sodium, exotic flavours) and geographic expansion into underserved retail formats such as convenience‑store chains and subscription services.

3. North America Meat Snacks Market Growth Trends - Current and emerging trends shaping the market?

Current trends highlight a shift toward cleaner‑label offerings, with organic meat snacks gaining traction among health‑focused shoppers. Flavor experimentation—such as spicy red pepper and pepperoni—continues to drive repeat purchases. Emerging trends include the integration of functional ingredients (e.g., collagen, probiotics) and the use of sustainable packaging to appeal to environmentally conscious consumers. Additionally, limited‑edition collaborations with culinary brands are creating buzz and expanding the consumer base.

4. COVID-19 Impact on the North America Meat Snacks Market - Pandemic effects and recovery trajectory?

The pandemic accelerated demand for shelf‑stable, single‑serve protein snacks as consumers stocked up for home consumption and remote‑work snacking. While initial supply‑chain disruptions led to temporary inventory gaps, the market rebounded quickly, supported by strong e‑commerce growth. Post‑COVID, the momentum has sustained, with consumers maintaining higher snack‑frequency habits and prioritizing convenient, nutritious options, positioning the market for continued expansion.

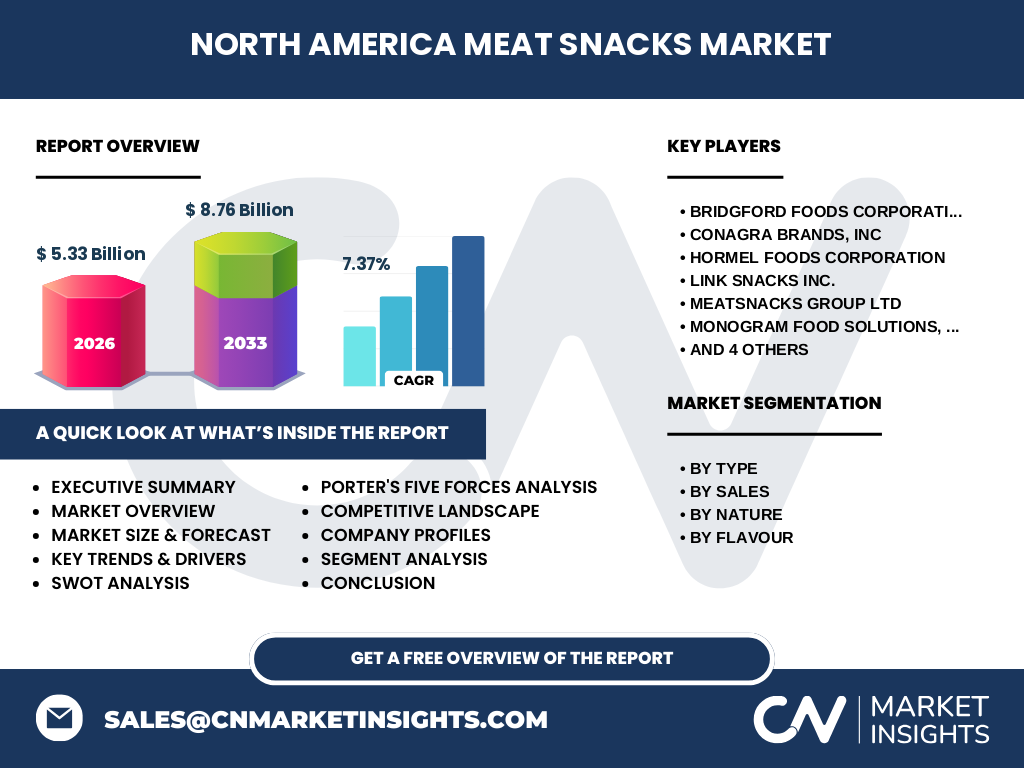

5. North America Meat Snacks Market Competitive Landscape - Major competitors and market consolidation?

The market is characterized by a mix of legacy food manufacturers and emerging specialty brands. Major players such as Bridgford Foods Corporation, Conagra Brands, Inc., Hormel Foods Corporation, and Tyson Food Inc. dominate the scale segment, while niche innovators like Link Snacks Inc. and Meatsnacks Group Ltd. focus on premium or organic offerings. Recent consolidation activity includes strategic acquisitions to broaden product portfolios and enhance distribution reach, reinforcing a competitive but increasingly integrated landscape.

6. Executive Summary - High-level overview and key findings about North America Meat Snacks Market?

In 2026 the North America meat snacks market reached a valuation of $5.33 billion and is projected to grow to $8.76 billion by 2033, reflecting a robust CAGR of 7.37 %. Growth is fueled by health‑driven snacking, flavor diversity, and expanding direct‑to‑consumer channels. Key opportunities lie in organic product lines, functional enhancements, and sustainable packaging, while regulatory compliance and raw‑material volatility remain principal concerns.

7. North America Meat Snacks Market Forecast - Projections for 2025-2032 period?

Based on the stated CAGR of 7.37 %, the market is expected to maintain steady upward momentum through 2032. By 2027 the market size will surpass $5.9 billion, advancing to $7.5 billion by 2030 and reaching the forecasted $8.76 billion by 2033. This trajectory underscores the durability of consumer demand for protein‑rich, convenient snack formats across both traditional retail and digital sales avenues.

8. North America Meat Snacks Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type shows jerky as the largest category, supported by its long‑standing popularity, while sticks and bars are experiencing rapid growth due to portable formats. Sales‑channel segmentation reveals direct channels (company websites, subscription boxes) capturing an expanding share, especially among younger demographics. In terms of nature, organic products are gaining market share despite higher price points, and flavor segmentation highlights Original as the baseline, with Pepperoni and Spicy Red Pepper driving incremental sales through flavor‑focused promotions.

9. Global North America Meat Snacks Market Size and Share by Region - Geographic distribution?

Within the global context, North America remains the dominant region for meat snacks, accounting for the majority of worldwide sales due to high disposable income and established snack culture. The United States leads the domestic market, followed by Canada, which contributes a measurable yet smaller portion. This concentration provides a solid foundation for manufacturers to leverage economies of scale while exploring cross‑border expansion opportunities.

10. Regional Analysis of the North America Meat Snacks Market - Detailed regional market performance?

The United States exhibits the strongest growth, driven by urban‑centered demand, a wide retail network, and strong brand loyalty. The West Coast shows heightened interest in organic and exotic flavors, whereas the Midwest favors traditional jerky and sausage formats. Canada’s market is modest but growing, with consumer preferences leaning toward convenient snack packs and a rising acceptance of premium‑priced organic options, indicating untapped potential for expansion.

11. Leading Company Profiles in the North America Meat Snacks Market - Industry players and strategies?

Bridgford Foods Corporation focuses on value‑added jerky and sausage products, leveraging extensive distribution partnerships. Conagra Brands, Inc. utilizes its broad snack portfolio to cross‑sell meat snacks through supermarket chains. Hormel Foods Corporation emphasizes brand diversification, merging legacy brands with innovative flavor lines. Tyson Food Inc. capitalizes on its supply‑chain scale to offer competitive pricing. Smaller innovators like Link Snacks Inc. prioritize organic certifications and niche flavors to capture premium segments.

12. Porter's Five Forces Analysis of the North America Meat Snacks Market - Competitive forces assessment?

Threat of new entrants is moderate; low barriers to product development are offset by the need for meat sourcing and compliance. Bargaining power of suppliers is high due to limited premium meat supplies and price volatility. Bargaining power of buyers is strong, as retailers demand promotional allowances and consumers compare numerous brands. Threat of substitutes is growing, especially from plant‑based snacks. Industry rivalry is intense, driven by brand differentiation, flavor innovation, and aggressive marketing.

13. SWOT Analysis of the North America Meat Snacks Market - Strengths, weaknesses, opportunities, threats?

Strengths: Established consumer base, high protein appeal, diverse product formats. Weaknesses: Dependence on raw meat price stability, regulatory complexity for labeling. Opportunities: Expansion of organic and functional lines, entry into health‑focused retail channels, adoption of sustainable packaging. Threats: Rising competition from plant‑based alternatives, potential supply‑chain disruptions, and shifting consumer preferences toward lower‑fat snack options.

14. North America Meat Snacks Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with livestock farming and meat processing, followed by seasoning and drying operations that create the final snack product. Packaging firms add convenience and branding elements before distribution through wholesale distributors to retail outlets or directly to consumers via e‑commerce platforms. End‑users purchase through supermarkets, convenience stores, online marketplaces, and specialty health‑food retailers, completing the cycle and providing feedback for product iteration.

15. Key Investment Insights in the North America Meat Snacks Market - Strategic investment recommendations?

Investors should target companies with scalable production capabilities and diversified flavor portfolios, as these are positioned to capture both mass‑market and premium segments. Funding innovation in organic and functional meat snacks can yield high‑margin growth. Strategic acquisitions of niche brands can accelerate entry into emerging sub‑categories, while partnerships with e‑commerce platforms enhance direct‑to‑consumer reach and data‑driven marketing.

16. North America Meat Snacks Market Conclusion - Summary and key takeaways?

The North America meat snacks market is on a clear growth trajectory, moving from $5.33 billion in 2026 to $8.76 billion by 2033. Core drivers include health‑centric snacking, flavor innovation, and expanding digital channels. Companies that invest in organic, functional, and sustainable solutions while maintaining efficient supply‑chains are likely to outperform. The market’s resilience post‑COVID and steady CAGR underscore its attractiveness for both strategic and financial stakeholders.

17. Research Methodology - How this research was conducted?

The study combined primary interviews with industry executives, retail buyers and supply‑chain experts, alongside secondary data extraction from company filings, trade publications and market databases. Quantitative analysis applied time‑series forecasting to the known market size (2026) and CAGR (7.37 %). Qualitative insights were validated through triangulation of multiple sources to ensure accuracy and reliability of the findings.

18. Research Scope - Coverage and limitations?

The scope encompasses the North America meat snacks market, covering product types, sales channels, nature (organic vs. conventional) and flavor categories. Geographic focus is limited to the United States and Canada. While the analysis leverages the latest available data, it does not include granular market‑share percentages beyond the provided figures, nor does it project macro‑economic variables that could affect future demand.

19. Key Companies and Recent Developments in the North America Meat Snacks Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Recent developments include Bridgford Foods launching a line of grass‑fed jerky with sustainable packaging, Conagra Brands expanding its meat snack portfolio through a partnership with a leading spice manufacturer, Hormel introducing a low‑sodium organic strip range, and Tyson Food Inc. acquiring a boutique snack brand to strengthen its premium offering. The Hershey Company entered the market via a joint venture focusing on sweet‑savory meat bar concepts, while Meatsnacks Group Ltd. announced a new plant in the Midwest to boost production capacity.