1. What is the Male Infertility Market and why is it significant?

The Male Infertility Market encompasses all products, services, and technologies used to diagnose, treat, and manage male reproductive disorders that affect the ability to conceive. It includes diagnostic tests such as DNA fragmentation analysis and computer‑assisted semen analysis, treatment options ranging from assisted reproductive technologies (ART) to varicocele surgery, and distribution channels that supply hospitals, clinics, fertility centers and research institutes. The market’s significance stems from the rising prevalence of infertility worldwide, increasing awareness of male reproductive health, and the growing demand for advanced, non‑invasive diagnostic tools that enable personalized treatment plans. With a 2026 market size of US$4.18 billion, the sector represents a critical component of the broader reproductive health industry.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Male Infertility Market?

Key drivers include heightened awareness of male factor infertility, rising incidences of lifestyle‑related conditions (obesity, smoking, environmental toxins) that impair sperm quality, and expanding insurance coverage for fertility services. Technological advancements in molecular diagnostics, such as oxidative stress analysis, also fuel growth. Restraints involve high costs of sophisticated testing, limited reimbursement in several regions, and cultural stigma that may delay seeking care. Challenges consist of a fragmented regulatory environment and the need for standardization across diagnostic protocols. Opportunities arise from tele‑medicine platforms, online pharmacy distribution, and emerging biomarkers that can improve early detection and treatment efficacy.

3. Which growth trends are currently influencing the Male Infertility Market?

Current trends include a shift toward precision‑medicine diagnostics, where tests like DNA fragmentation and oxidative stress analysis provide deeper insights into sperm health. Integration of artificial intelligence in computer‑assisted semen analysis is improving accuracy and reducing operator bias. Moreover, the market is seeing a rise in combined therapy approaches that blend ART with pharmacological interventions, and an expanding role for fertility centers that offer comprehensive, one‑stop services. Digital health solutions, such as remote sperm analysis kits, are also emerging, catering to privacy‑concerned patients.

4. How did COVID‑19 affect the Male Infertility Market and what is the recovery outlook?

The pandemic caused a temporary slowdown in elective fertility procedures and clinic visits due to lockdowns and resource reallocation. However, demand for at‑home testing kits and tele‑consultations surged, accelerating digital adoption. Post‑pandemic, the market has rebounded strongly, with a renewed focus on health monitoring and a backlog of postponed treatments. The recovery trajectory is positive, supported by continued investment in remote diagnostics and an increasing number of patients seeking care once restrictions eased.

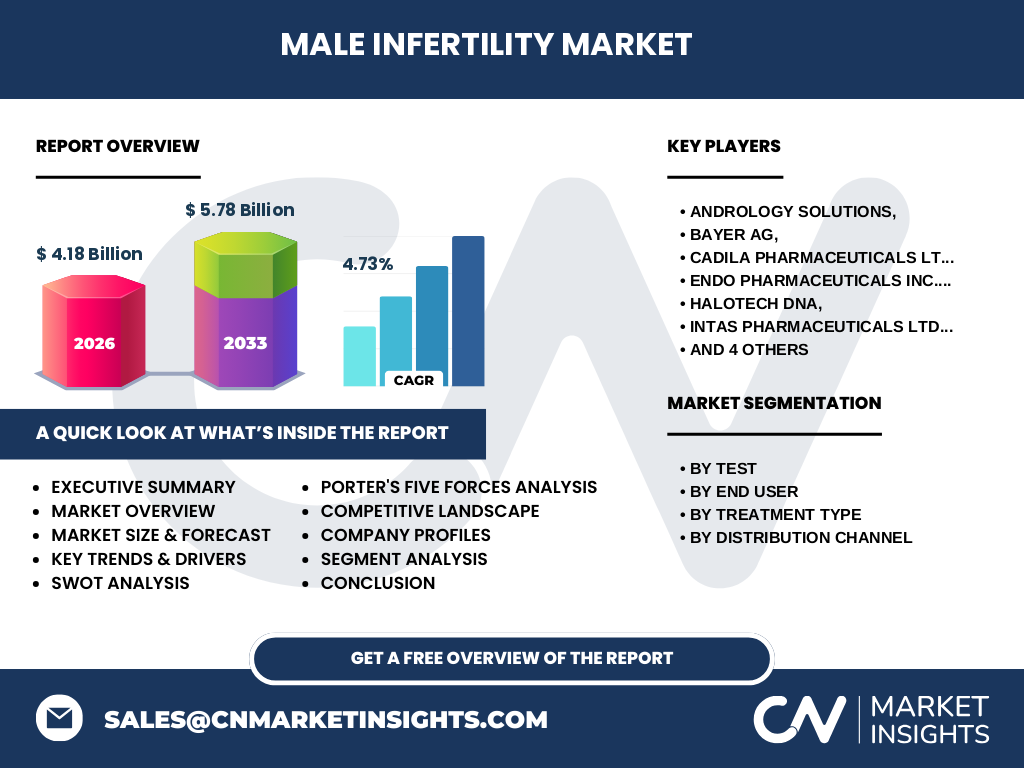

5. Who are the major competitors and what is the level of consolidation in the Male Infertility Market?

Key competitors include Andrology Solutions, Bayer AG, Cadila Pharmaceuticals Ltd., Endo Pharmaceuticals Inc., Halotech DNA, INTAS PHARMACEUTICALS LTD., MERCK KGaA, SCSA Diagnostics, Inc., Sanofi, and Vitrolife. The market exhibits moderate consolidation, with large pharmaceutical firms leveraging extensive R&D pipelines while specialized firms focus on niche diagnostic technologies. Recent strategic alliances and acquisitions have intensified competition, resulting in a dynamic landscape where innovation and portfolio diversification are critical success factors.

6. What are the high‑level findings presented in the Executive Summary?

The Executive Summary highlights a robust market valued at US$4.18 billion in 2026, projected to reach US$5.78 billion by 2033, reflecting a CAGR of 4.73%. Growth is driven by increasing infertility prevalence, advanced diagnostic modalities, and expanding ART adoption. Digital channels and online pharmacies are emerging distribution routes. Regional analyses indicate strong demand in North America and Europe, while Asia‑Pacific growth is propelled by rising awareness and expanding fertility clinics. Competitive dynamics show both multinational pharmaceutical giants and niche diagnostics firms actively shaping the market.

7. What is the forecast for the Male Infertility Market from 2025 to 2032?

Based on the provided CAGR of 4.73%, the market is expected to maintain steady expansion through 2032. By 2027, the market will surpass US$4.5 billion, advancing to US$5.78 billion by 2033. This trajectory underscores ongoing investment in diagnostic innovation and an increasing share of ART procedures, reinforcing the market’s long‑term growth potential.

8. How is the Male Infertility Market sized and shared across its primary segments?

Segmentation is organized by test type, end user, treatment type, and distribution channel. Diagnostic test segments—DNA fragmentation technique, oxidative stress analysis, microscopic examination, sperm agglutination, computer‑assisted semen analysis, and sperm penetration assay—collectively dominate the market, reflecting a strong focus on accurate sperm quality assessment. End users are split among hospitals and clinics, fertility centers, research institutes, and other users, with fertility centers commanding the largest share due to their specialized services. Treatment segmentation includes ART and varicocele surgery versus medication, with ART representing the higher‑value segment. Distribution channels are divided into hospital pharmacies, retail pharmacies/drug stores, and online pharmacies, the latter gaining traction as patients seek discreet, convenient access.

9. What is the geographic distribution of the Global Male Infertility Market?

The market is globally dispersed, with notable concentration in North America and Europe where fertility services are well‑established and reimbursement frameworks are supportive. Emerging economies in the Asia‑Pacific region are experiencing rapid uptake due to increasing disposable incomes, growing fertility clinic networks, and heightened public awareness. While specific regional market shares are not disclosed, the overall trend points to a balanced global footprint with growth hotspots in developed and high‑growth emerging markets.

10. Can you provide a detailed regional analysis of the Male Infertility Market?

In North America, strong insurance coverage, a high density of specialized fertility centers, and leading research institutions drive market leadership. Europe mirrors this pattern, with regulatory support for advanced reproductive technologies and a mature healthcare infrastructure. The Asia‑Pacific region, particularly China, India, and Japan, is witnessing accelerated adoption of ART and diagnostic tests, propelled by expanding middle‑class populations and government initiatives to address declining birth rates. Latin America and the Middle East show moderate growth, limited primarily by variable reimbursement policies but bolstered by increasing awareness campaigns.

11. What are the profiles and strategies of leading companies in the Male Infertility Market?

Andrology Solutions focuses on cutting‑edge diagnostic kits, emphasizing rapid turnaround and portability. Bayer AG leverages its extensive pharmaceutical portfolio to integrate medication‑based treatments with diagnostic offerings. Cadila Pharmaceuticals Ltd. and Endo Pharmaceuticals Inc. concentrate on generics and novel therapeutic agents for male reproductive health. Halotech DNA and SCSA Diagnostics, Inc. specialize in DNA‑based sperm quality assessments, positioning themselves as leaders in precision diagnostics. MERCK KGaA and Sanofi maintain broad reproductive health pipelines, while Vitrolife supplies ART media and culture systems, reinforcing its role in assisted reproduction. Across the board, companies pursue strategic alliances, R&D investments, and geographic expansion to capture market share.

12. How does Porter's Five Forces model apply to the Male Infertility Market?

Bargaining Power of Buyers: Moderate to high, as clinics and hospitals demand accurate, cost‑effective diagnostics and can switch suppliers. Bargaining Power of Suppliers: Relatively low, given multiple sources for reagents and equipment. Threat of New Entrants: Moderate, due to high regulatory barriers but attractive market CAGR. Threat of Substitutes: Low, because specialized sperm analysis tests have limited alternatives. Industry Rivalry: Intense, with both large pharma and niche diagnostics firms competing on innovation, price, and service quality.

13. What are the SWOT findings for the Male Infertility Market?

Strengths: Growing prevalence of male factor infertility, strong technological innovation, and robust pipeline of ART solutions. Weaknesses: High cost of advanced diagnostics, fragmented reimbursement, and cultural barriers in certain regions. Opportunities: Expansion of tele‑medicine, online pharmacy channels, and discovery of novel biomarkers. Threats: Regulatory uncertainties, potential economic downturns affecting elective procedures, and competitive pressure from emerging biotech entrants.

14. How is value created and transferred across the Male Infertility Market value chain?

The value chain starts with research institutions developing diagnostic biomarkers and therapeutic agents. These innovations are then transferred to manufacturers who produce test kits, pharmaceuticals, and ART consumables. Distribution channels—hospital pharmacies, retail drug stores, and online pharmacies— deliver products to end users. Hospitals, clinics, and fertility centers provide the clinical interface, performing diagnostics and delivering treatments. Post‑treatment follow‑up and data analytics feed back into R&D, closing the loop for continuous improvement.

15. What investment insights are most relevant for stakeholders in the Male Infertility Market?

Investors should prioritize companies with diversified portfolios that combine diagnostics and therapeutics, as this integration reduces dependency on a single revenue stream. Firms that have secured partnerships with leading fertility centers or have strong presence in online pharmacy distribution are positioned for accelerated growth. Funding R&D in AI‑enhanced semen analysis and non‑invasive biomarkers offers high upside, while monitoring regulatory landscapes will mitigate risk.

16. What are the key takeaways from the Male Infertility Market analysis?

The market is on a steady growth trajectory, reaching US$5.78 billion by 2033 with a 4.73% CAGR. Diagnostic innovation, particularly in DNA fragmentation and oxidative stress analysis, is a primary growth engine. ART and medication treatments complement the diagnostic side, while online pharmacies are reshaping distribution. Regional demand is strongest in North America and Europe, with rapid expansion in Asia‑Pacific. Competitive dynamics are driven by both large pharma and specialized diagnostics firms, creating opportunities for strategic alliances and investment in precision technologies.

17. How was the research for this report conducted?

The research employed a mixed‑method approach, combining primary interviews with key opinion leaders in andrology, secondary data extraction from industry publications, regulatory filings, and company financial reports. Market sizing relied on the provided 2026 baseline of US$4.18 billion and applied a 4.73% CAGR to generate forward projections. Segmentation analysis used the defined test, end‑user, treatment, and distribution categories to structure the market landscape.

18. What is the scope of this research and its limitations?

The scope covers global market size, segmentation by test type, end user, treatment modality, and distribution channel, as well as regional performance, competitive landscape, and strategic insights up to 2033. Limitations include reliance on publicly available data and the absence of proprietary sales figures for individual companies, which may affect granularity of market‑share estimates.

19. Which key companies have recently announced developments in the Male Infertility Market?

Recent developments include Andrology Solutions launching a portable DNA fragmentation kit, Bayer AG expanding its male infertility medication portfolio with a new hormonal therapy, and Vitrolife introducing an advanced culture medium for IVF that improves embryo viability. MERCK KGaA announced a partnership with a leading fertility center network to co‑develop AI‑driven semen analysis software. Sanofi reported a collaboration with an online pharmacy platform to increase accessibility of male infertility medications. These announcements underscore the market’s focus on innovation, collaboration, and expanding patient access.