What is the Industrial Filters Market Overview – definition, scope, and significance?

The Industrial Filters Market encompasses products and services that remove contaminants from air, liquids, and gases across a wide range of manufacturing and processing sectors. It includes filters by type (air, liquid), media (fiberglass, metal, non‑woven fabrics, activated carbon, others), product forms (bag, drum, cartridge, HEPA, gravity filtration, electrostatic precipitator, others) and end‑use industries such as food & beverages, power generation, semiconductors, chemicals, healthcare, metals, mining, paper & paints, among others. The market is significant because clean processes drive product quality, regulatory compliance, equipment longevity, and energy efficiency in industrial operations worldwide.

What are the key drivers, restraints, challenges, and opportunities shaping the Industrial Filters Market?

Growth is driven by rising environmental regulations, increasing demand for high‑purity processes in semiconductor and pharmaceutical production, and expanding industrial output in emerging economies. Restraints include high upfront capital costs for advanced filtration systems and the cyclic nature of heavy‑industry investment. Challenges involve technical complexity of handling aggressive chemicals and maintaining filter performance under extreme temperatures. Opportunities arise from the adoption of smart, IoT‑enabled monitoring, development of reusable and high‑efficiency media, and growing retro‑fit projects aimed at improving energy consumption in legacy plants.

What current and emerging growth trends are influencing the Industrial Filters Market?

Current trends feature a shift toward modular filter designs that allow quick replacement and minimal downtime, as well as increased use of HEPA and ULPA filters in clean‑room environments. Emerging trends include integration of nanofiber media for superior capture efficiency, adoption of AI‑based predictive maintenance, and the rise of circular‑economy models where filter components are reclaimed and regenerated. Additionally, the push for low‑emission processes is spurring demand for high‑performance electrostatic precipitators and activated‑carbon filters.

How has COVID‑19 impacted the Industrial Filters Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and delayed capital‑expenditure projects, causing a short‑term dip in orders for large‑scale filtration equipment. However, heightened awareness of airborne contaminants accelerated demand for air filtration solutions in manufacturing and healthcare facilities. Recovery accelerated in 2022 as industries resumed expansion, and the market has since entered a robust growth phase, supported by renewed investment in plant upgrades and stricter health‑safety standards.

Who are the major competitors and what is the state of market consolidation in the Industrial Filters Market?

Key players include Alfa Laval AB, Daikin Industries Ltd., Donaldson, Eaton Corp Plc, Filtcare Technology Pvt. Ltd., HYDAC International GmbH, Hollingsworth & Vose, Honeywell International Inc., MANN+HUMMEL International GmbH & Co. KG, and Parker Hannifin Corp. The competitive landscape is characterized by strategic alliances, technology licensing, and selective M&A activity focused on adding advanced media capabilities and expanding geographic reach. Consolidation is moderate, with incumbents leveraging scale to offer integrated filtration solutions.

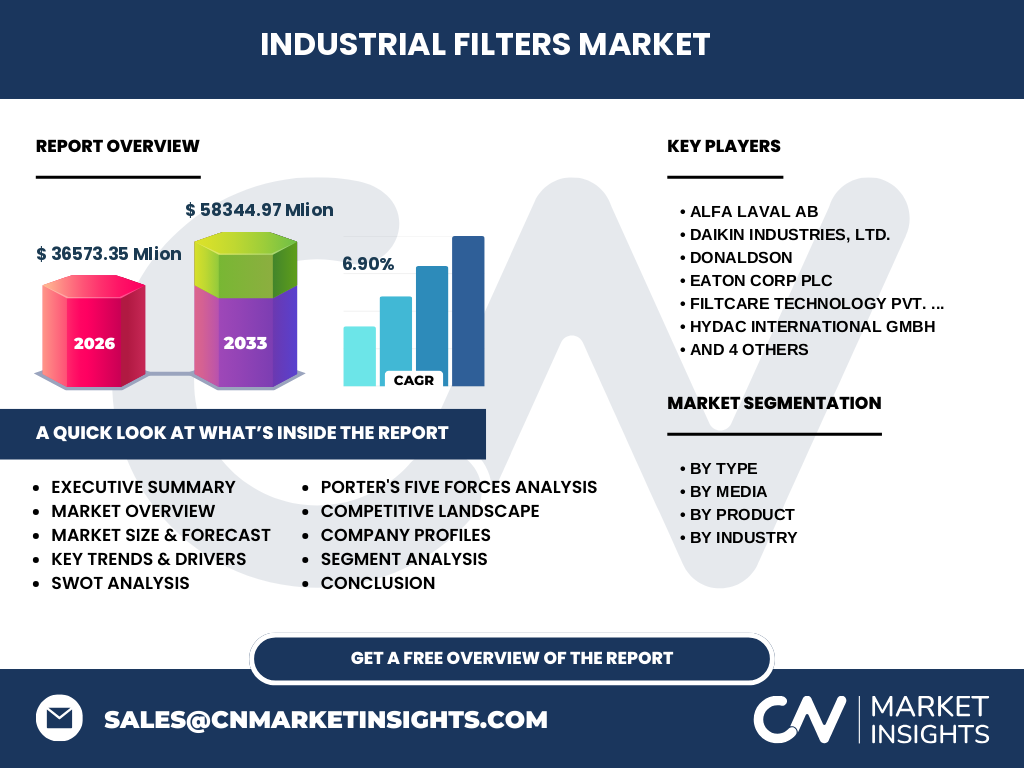

What are the high‑level findings presented in the Executive Summary of the Industrial Filters Market report?

The Executive Summary highlights a market size of USD 36,573.35 million in 2026, projected to reach USD 58,344.97 million by 2033, reflecting a compound annual growth rate (CAGR) of 6.90 %. Growth is underpinned by regulatory pressure, industrial expansion, and technological innovation. Air and liquid filters command the largest demand, while media such as fiberglass and activated carbon dominate current supply. North America and Asia‑Pacific emerge as the strongest regions, with Asia‑Pacific showing the fastest growth due to expanding manufacturing bases.

What are the forecast expectations for the Industrial Filters Market for 2025‑2032?

Based on the provided CAGR of 6.90 %, the market is expected to maintain steady expansion through 2032. The forecast anticipates continued adoption of high‑efficiency air filters in power generation and semiconductor facilities, alongside increasing demand for liquid filtration in chemicals, petrochemicals, and food processing. The upward trajectory will be reinforced by ongoing regulatory tightening and the rollout of smart‑filtering technologies that improve operational uptime and reduce total cost of ownership.

How is the Industrial Filters Market sized and shared across the defined segmentation?

Segmentation by type splits the market into air and liquid filters, each representing a substantial share of the total USD 36,573.35 million base year. By media, fiberglass, metal, non‑woven fabrics, activated carbon, and others constitute the supply mix, with fiberglass and activated carbon being the most prevalent due to cost‑effectiveness and high adsorption capacity. Product‑level segmentation includes bag, drum, cartridge, HEPA, gravity filtration, electrostatic precipitator, and others, where bag and cartridge filters dominate the volume share. Industry‑wise, food & beverages, power generation, semiconductors & electronics, chemicals & petrochemicals, healthcare, metals & mining, and paper & paints collectively drive demand, with the semiconductor and power sectors showing the highest per‑unit value.

What is the global geographic distribution of the Industrial Filters Market size and share?

The market is globally distributed, with North America and Europe holding mature shares due to stringent environmental standards, while Asia‑Pacific leads in growth volume, fueled by rapid industrialization and expanding manufacturing capacities. The Middle East & Africa and Latin America present emerging opportunities, with incremental investments in power generation and mining projects that require robust filtration solutions.

What detailed regional performance trends are observed in the Industrial Filters Market?

In North America, demand is driven by upgrades to legacy plants and strong adoption of smart filtration in the automotive and aerospace sectors. Europe’s growth is anchored in renewable‑energy projects and rigorous workplace air‑quality regulations. Asia‑Pacific shows the highest compounded growth, bolstered by China’s and India’s large‑scale industrial expansions, increasing food‑processing output, and aggressive clean‑room construction for semiconductor fabs. The Middle East & Africa benefit from rising petrochemical complexes, while Latin America’s growth hinges on mining and agro‑industrial developments.

Which leading companies dominate the Industrial Filters Market and what strategies are they employing?

Alfa Laval focuses on energy‑efficient heat‑exchange‑integrated filters, while Daikin leverages its HVAC expertise to cross‑sell air‑filtration modules. Donaldson invests heavily in R&D for nanofiber media and digital monitoring. Eaton expands its portfolio through acquisitions of specialty filter manufacturers. HYDAC emphasizes customized solutions for heavy‑industry applications. Honeywell pursues IoT‑enabled filter management platforms. MANN+HUMMEL pursues global expansion via joint ventures, and Parker Hannifin broadens its reach in fluid‑control filtration systems.

How does Porter’s Five Forces analysis characterize the Industrial Filters Market?

• Threat of new entrants: Moderate – high capital requirements and the need for technical expertise limit newcomers. • Bargaining power of suppliers: Low to moderate – multiple raw‑material sources for media reduce supplier leverage. • Bargaining power of buyers: Moderate – large industrial customers negotiate volume discounts and demand performance guarantees. • Threat of substitutes: Low – limited alternatives to high‑efficiency filtration for critical processes. • Competitive rivalry: High – numerous established players vie for market share through innovation, service contracts, and geographic expansion.

What are the SWOT highlights for the Industrial Filters Market?

Strengths: Essential role in compliance and process reliability; diversified applications across many industries.

Weaknesses: High upfront costs; dependence on cyclical capital‑expenditure patterns.

Opportunities: Smart‑filtering, reusable media, expansion in emerging economies, and stricter global emission standards.

Threats: Economic downturns affecting industrial spending, rapid technology shifts that could render legacy products obsolete, and supply‑chain disruptions for specialty media.

What does the value chain of the Industrial Filters Market look like?

The value chain begins with raw‑material suppliers (fiberglass, metal, activated carbon), followed by filter media manufacturers, component fabricators, and system integrators who assemble bag, cartridge, or drum filters. Next are distributors and system integrators who install and commission the filters at end‑user sites. After installation, service providers deliver routine maintenance, monitoring, and filter replacement, creating a recurring revenue stream. End‑users (manufacturers, power plants, healthcare facilities) complete the chain by consuming the filtration solutions to achieve operational goals.

What key investment insights can be drawn for stakeholders interested in the Industrial Filters Market?

Investors should focus on companies that combine proven filtration expertise with digital service platforms, as recurring service contracts improve cash flow stability. Target firms with strong presence in high‑growth regions such as Asia‑Pacific and those offering reusable or regenerative media, which align with sustainability trends. M&A activity remains a viable path to acquire niche technologies or geographic footholds. Monitoring regulatory developments will help anticipate demand spikes in specific sectors like semiconductor manufacturing.

What are the concluding observations and takeaways from the Industrial Filters Market analysis?

The market is on a clear growth trajectory, supported by a 6.90 % CAGR and a projected increase from USD 36.5 billion in 2026 to USD 58.3 billion by 2033. Demand is broadly diversified across air and liquid filtration, with advanced media and smart technologies driving higher margins. Regional dynamics favor Asia‑Pacific as the primary growth engine, while North America and Europe maintain stable, mature demand. Companies that innovate in media efficiency and digital service models are best positioned to capture value.

What research methodology was employed to produce this Industrial Filters Market report?

The study combined primary interviews with industry experts, senior engineers, and key buyers, along with secondary data collection from company annual reports, trade publications, and regulatory filings. Market sizing used a bottom‑up approach, aggregating revenues from major product categories and regional sales figures. Forecasting applied a compound annual growth rate (CAGR) of 6.90 % derived from historical trends and forward‑looking indicators such as capital‑expenditure pipelines and regulatory timelines.

What is the scope of this research and any limitations?

The research covers global industrial filtration across air and liquid applications, encompassing all major media types, product forms, and end‑use industries listed. It excludes residential and automotive‑only filters that are not classified as industrial. Data is limited to publicly available information and proprietary estimates; therefore, exact market shares for individual companies or regions are not disclosed beyond the aggregate figures provided.

Which key companies are highlighted and what recent developments have they announced?

Alfa Laval announced a new energy‑efficient heat‑exchange filter line for power plants. Daikin launched a compact air‑purification module targeting semiconductor fabs. Donaldson introduced a nanofiber cartridge with integrated sensor telemetry. Eaton completed the acquisition of a niche liquid‑filter specialist to broaden its petrochemical portfolio. HYDAC unveiled a customized metal‑mesh filter for high‑temperature metal‑working processes. Honeywell rolled out an AI‑driven filter‑health monitoring platform. MANN+HUMMEL entered a joint venture in Southeast Asia to produce activated‑carbon media locally. Parker Hannifin reported a strategic partnership with a leading OEM to supply drum filters for large‑scale chemical reactors.