What is the Robot End-Effector Market Overview – definition, scope, and significance?

The Robot End‑Effector market comprises devices such as welding guns, clamps, grippers, suction cups, tool changers and other specialized attachments that enable industrial robots to interact with products and work‑pieces. These components form the functional “hand” of a robot, extending its capabilities across handling, assembly, welding, processing and dispensing operations. The market is pivotal to the automation ecosystem because end‑effectors directly influence productivity, product quality, flexibility and overall return on automation investments across diverse manufacturing sectors.

What are the key drivers, restraints, challenges, and opportunities shaping the Robot End-Effector Market?

Primary drivers include increasing adoption of collaborative robots, rising demand for high‑speed, precision manufacturing, and the push for Industry 4.0 integration. Restraints stem from high upfront costs of advanced end‑effectors and the need for skilled integration engineers. Challenges involve rapid technology obsolescence and stringent safety standards that can slow deployment. Opportunities arise from growth in the automotive and electronics industries, the emergence of soft‑gripping technologies for delicate goods, and service‑oriented business models such as leasing and aftermarket support.

Which growth trends are currently influencing the Robot End-Effector Market?

Current trends feature a shift toward modular, plug‑and‑play end‑effectors that reduce change‑over time, the incorporation of AI‑driven force feedback for adaptive grasping, and the expansion of hybrid tools that combine welding and handling functions. Additionally, lightweight composite materials are being used to improve payload efficiency, while cloud‑based monitoring platforms enable predictive maintenance of end‑effector assemblies, extending service life and uptime.

How did COVID‑19 affect the Robot End‑Effector Market, and what is the recovery trajectory?

The pandemic initially disrupted supply chains for precision components and delayed capital projects, causing a short‑term dip in orders. However, heightened concerns about labor shortages and the need for resilient, contact‑less production accelerated longer‑term demand. Post‑2020, the market rebounded strongly, with manufacturers accelerating automation roadmaps to mitigate future disruptions, setting the stage for sustained growth.

What does the competitive landscape look like for the Robot End‑Effector Market?

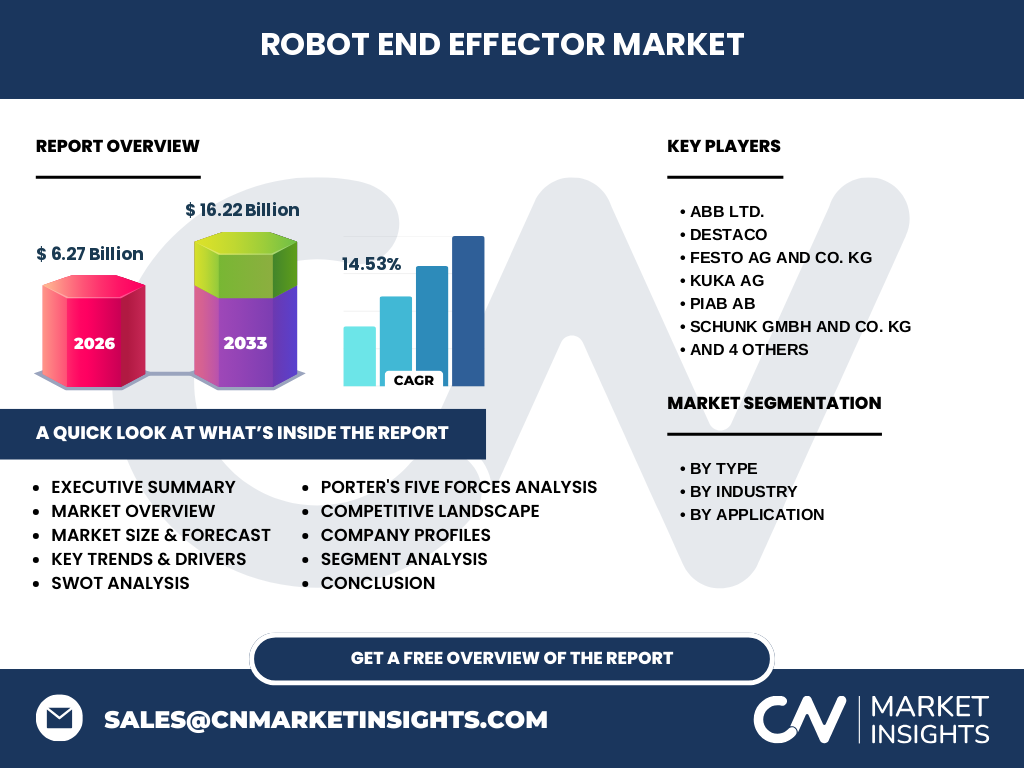

The market is moderately consolidated, led by established manufacturers such as ABB Ltd., DESTACO, Festo AG & Co. KG, KUKA AG, Piab AB, SCHUNK GmbH & Co. KG, SMC Corporation, Schmalz GmbH, Staubli International AG and ZIMMER GROUP GmbH. These players compete on technology differentiation, integrated solutions and global service networks. Recent years have seen strategic acquisitions and joint ventures aimed at expanding product portfolios and geographic reach.

Can you provide an executive summary of the Robot End‑Effector Market?

The Robot End‑Effector market is valued at $6.27 billion in 2026 and is projected to reach $16.22 billion by 2033, growing at a robust CAGR of 14.53 %. Growth is driven by expanding automation in automotive, electronics and food & beverage sectors, coupled with innovations in adaptive gripping and hybrid tooling. Competitive dynamics are defined by a handful of global leaders leveraging R&D and service‑based models to capture emerging opportunities.

What are the forecast expectations for the Robot End‑Effector Market from 2025 to 2032?

Based on the stated CAGR of 14.53 %, the market is expected to more than double its 2026 size by the early 2030s, reflecting strong demand across all end‑effector types. Continuous adoption of collaborative robots and the need for flexible manufacturing lines will sustain double‑digit growth, with the highest acceleration anticipated in regions investing heavily in smart factories.

How is the Robot End‑Effector Market sized and shared by segmentation?

By type, the market is divided into welding guns, clamps, grippers, suction cups, tool changers and others, each serving distinct process requirements. By industry, the primary segments are automotive, metals and machinery, electrical and electronics, food and beverages and other manufacturing verticals. By application, the market serves handling, assembly, welding, processing, dispensing and other specialized tasks, providing a multidimensional view of demand patterns.

What is the geographic distribution of the global Robot End‑Effector market?

The market exhibits a worldwide footprint, with leading demand originating from mature manufacturing hubs in North America, Europe and Asia‑Pacific. These regions benefit from dense industrial bases, high automation spending and strong OEM presence. Emerging economies are gradually increasing their share as they modernize production facilities and adopt advanced robotic solutions.

What does the regional analysis reveal about the Robot End‑Effector Market?

North America leads in technological adoption, driven by automotive and aerospace sectors. Europe shows strong growth in precision engineering and electronics, supported by stringent quality standards. Asia‑Pacific, the fastest‑growing region, benefits from large-scale automotive production, electronics manufacturing and aggressive government incentives for automation. Latin America and the Middle East display modest but steady uptake, primarily in food processing and metals industries.

Which companies are leading in the Robot End‑Effector Market and what are their strategies?

Key players such as ABB Ltd., KUKA AG and Festo AG & Co. KG focus on integrated robot‑end‑effector ecosystems, leveraging proprietary software for seamless coordination. DESTACO and SCHUNK GmbH & Co. KG emphasize high‑precision gripping solutions for electronics assembly. Piab AB and Schmalz GmbH specialize in vacuum technologies for the food and beverage sector. Most leaders pursue R&D investments, strategic partnerships and post‑sale service contracts to strengthen market position.

How does Porter’s Five Forces analysis apply to the Robot End‑Effector Market?

Threat of new entrants is moderate due to high capital requirements and specialized expertise. Bargaining power of suppliers is limited because component sourcing is diversified across global supply chains. Bargaining power of buyers is growing as manufacturers demand customized, cost‑effective solutions. Threat of substitutes remains low, given the unique functional role of end‑effectors. Industry rivalry is intense, driven by innovation cycles and service differentiation.

What are the SWOT insights for the Robot End‑Effector Market?

Strengths: Proven demand across multiple industries, high entry barriers, and rapid technology evolution. Weaknesses: High initial investment and dependence on skilled integration. Opportunities: Expansion into soft‑gripping for delicate goods, AI‑enabled adaptive tools, and emerging markets investing in automation. Threats: Supply‑chain volatility, potential regulatory changes, and fast‑paced obsolescence of legacy designs.

How is the value chain structured in the Robot End‑Effector Market?

The value chain starts with raw material suppliers (metals, composites, electronics), proceeds to component manufacturers (actuators, sensors), then to end‑effector assemblers that integrate mechanical, electrical and software elements. System integrators combine end‑effectors with robot platforms, followed by distributors and OEMs that deliver finished solutions to end‑users. After‑sales services, calibration and parts refurbishment close the loop, adding recurring revenue streams.

What investment insights can be drawn from the Robot End‑Effector Market?

Investors should target companies with strong R&D pipelines and diversified end‑effector portfolios, as these are positioned to capture growth across varying application needs. Partnerships with system integrators and OEMs enhance market reach. Monitoring regions with aggressive automation incentives can reveal high‑return opportunities, while firms offering subscription‑based service models may generate stable cash flow amid capital‑intensive sales cycles.

What are the main conclusions of the Robot End‑Effector Market analysis?

The market is on a clear upward trajectory, underpinned by a 14.53 % CAGR and a projected tripling of revenue by 2033. Technological innovation, sector‑wide automation, and expanding geographic adoption collectively drive growth. Competitive advantage will belong to firms that combine advanced product development with comprehensive services and global support networks.

Which research methodology was used for this Robot End‑Effector Market study?

The analysis employed a mixed‑method approach, integrating primary interviews with industry experts, secondary data review from company reports, trade publications and market databases, and quantitative modeling to derive the CAGR and forecast figures. Cross‑validation ensured consistency with the provided market size (2026: $6.27 billion) and forecast (2033: $16.22 billion).

What is the scope of this Robot End‑Effector Market research?

The study covers global market dynamics, segmentation by type, industry and application, and regional performance across major geographies. It includes competitive profiling of the ten listed key companies and evaluates macro‑economic, technological and regulatory factors influencing demand. The scope is limited to commercially available end‑effector solutions and excludes conceptual prototypes not yet in market.

Which key companies and recent developments are notable in the Robot End‑Effector Market?

ABB Ltd. launched a new collaborative gripper with force‑feedback control. DESTACO announced a partnership with a leading automotive OEM for high‑speed assembly tools. Festo AG & Co. KG introduced a modular tool‑changer platform that reduces change‑over time by 30 %. KUKA AG acquired a soft‑gripping specialist to broaden its product range. Piab AB released an energy‑efficient suction cup series targeting the food‑beverage sector. SCHUNK GmbH & Co. KG unveiled AI‑enhanced gripping algorithms for electronics handling. SMC Corporation, Schmalz GmbH, Staubli International AG and ZIMMER GROUP GmbH each reported new product roll‑outs and expansion of service contracts in Asia‑Pacific.