What is the Military Truck Market Overview - Definition, scope, and significance?

The Military Truck Market comprises all road‑mobile, heavy‑duty vehicles designed to meet defense requirements, including transport, logistics, and combat support roles. Its scope covers light, medium, and heavy trucks, various propulsion systems (diesel, electric/hybrid), and transmission types (automatic, manual). Significance stems from the critical role trucks play in sustaining operational readiness, enabling rapid troop deployment, and ensuring supply chain continuity across land‑based missions worldwide.

What are the Military Truck Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include rising defense budgets, modernization programs, and the shift toward greener propulsion technologies. Restraints arise from high procurement costs and stringent regulatory standards. Challenges involve supply‑chain disruptions, integration of advanced electronics, and evolving battlefield requirements. Opportunities exist in electric/hybrid truck development, modular vehicle designs, and after‑market services such as retrofitting and lifecycle support.

What are the current Military Truck Market Growth Trends?

Growth trends feature a transition toward electrified powertrains, driven by sustainability mandates, and increased demand for autonomous logistics solutions. Modular platforms that can be reconfigured for cargo, troop, or medical roles are gaining traction. Additionally, digital connectivity and telematics are being embedded to enhance fleet management and operational efficiency.

How did COVID‑19 impact the Military Truck Market and what is the recovery trajectory?

The pandemic caused temporary production slowdowns and delayed contract awards due to fiscal re‑evaluations. However, defense priorities quickly rebounded, leading to a robust recovery. Procurement cycles have resumed, and the focus on resilient supply chains has accelerated investments in domestic manufacturing capabilities, positioning the market for sustained growth post‑COVID‑19.

What does the Military Truck Market Competitive Landscape look like?

The market is moderately consolidated, with ten major players dominating global supply. Companies such as Oshkosh Corporation, Iveco Group, and Volvo Defense AB lead in heavy‑truck segments, while Arquiqus Defense and Tata Motors excel in lightweight and medium categories. Recent consolidation includes strategic partnerships and joint ventures aimed at expanding technology portfolios and geographic reach.

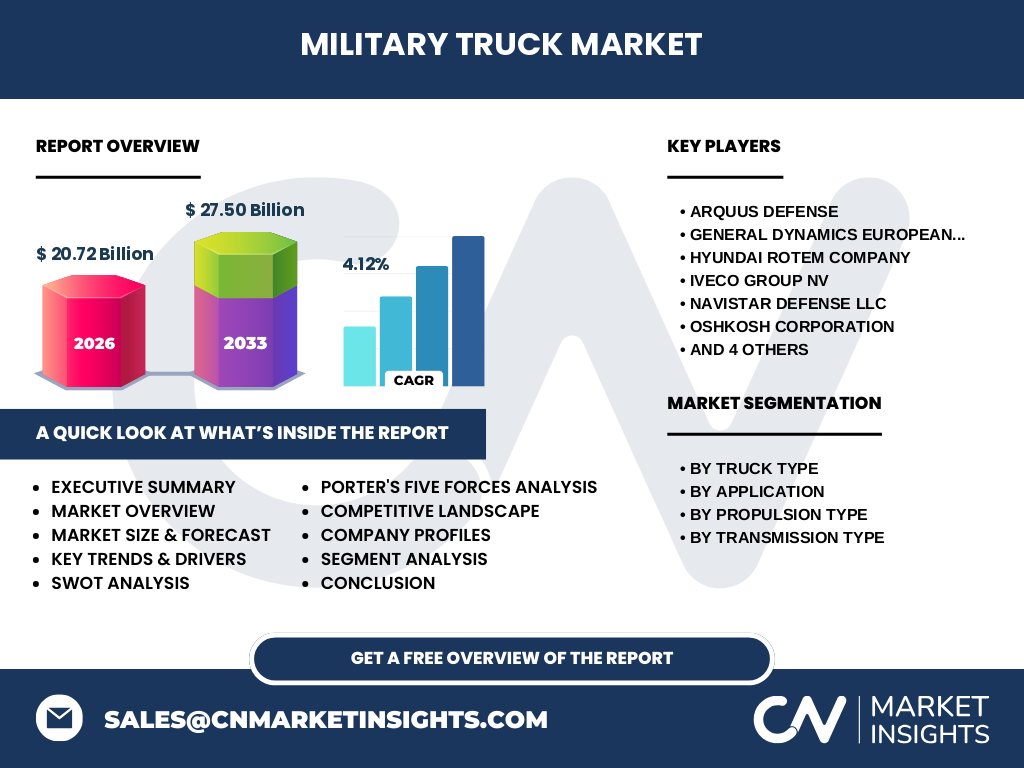

What are the key points from the Executive Summary of the Military Truck Market?

The market is valued at $20.72 billion in 2026 and is projected to reach $27.50 billion by 2033, reflecting a CAGR of 4.12 %. Growth is propelled by defense spending, electrification, and modular vehicle concepts. The competitive arena is defined by a blend of legacy manufacturers and emerging green‑technology firms, with ample opportunity for innovation in after‑sales services and digital integration.

What are the Military Truck Market Forecast expectations for 2025‑2032?

Based on the stated CAGR of 4.12 %, the market is expected to maintain a steady upward trajectory, crossing the $25 billion mark by the early 2020s and reaching the forecasted $27.50 billion by 2033. This reflects consistent demand across all truck types, with electric/hybrid propulsion capturing an expanding share as governments prioritize low‑emission solutions.

How is the Military Truck Market Size and Share by Segmentation?

Segmentation by truck type includes Light, Medium, and Heavy trucks, each serving distinct operational roles. Application segmentation differentiates Cargo/Logistics carriers from Troop carriers, while propulsion segmentation splits between Electric/Hybrid and Diesel powertrains. Transmission options are divided into Automatic and Manual. While exact monetary splits are undisclosed, the heavy‑truck segment traditionally commands the largest share, with electric/hybrid gaining momentum within all categories.

What is the Global Military Truck Market Size and Share by Region?

The global market totals $20.72 billion in 2026. Regional distribution reflects stronger defense spending in North America and Europe, with emerging growth in Asia‑Pacific due to modernization drives. The Middle East and Africa present niche opportunities linked to regional security initiatives. No precise regional revenue figures are provided, but geographic diversification underpins the market’s resilience.

What does the Regional Analysis of the Military Truck Market reveal?

North America leads in procurement volume, emphasizing heavy‑duty and technologically advanced platforms. Europe focuses on modularity and compliance with stringent emissions standards, favoring electric/hybrid models. Asia‑Pacific’s rapid defense modernization fuels demand for versatile medium‑truck solutions. The Middle East invests heavily in rugged, off‑road capable trucks, while Africa’s market is driven by peacekeeping logistics requirements.

Which companies are leading in the Military Truck Market and what are their strategies?

Key players include Arquus Defense, General Dynamics European Land Systems, HYUNDAI ROTEM, Iveco Group, Navistar Defense, Oshkosh Corporation, Rheinmetall AG, TATRA TRUCKS, Tata Motors, and Volvo Defense AB. Strategies involve expanding electric vehicle portfolios, pursuing joint R&D projects, enhancing aftermarket support, and targeting regional defense contracts through localized production and strategic alliances.

How does Porter’s Five Forces analysis apply to the Military Truck Market?

Threat of new entrants is moderate due to high capital requirements and certification hurdles. Bargaining power of suppliers is high for specialized components like advanced batteries. Bargaining power of buyers (governments) is strong, driving price transparency and performance demands. Threat of substitutes remains low, as few alternatives match the ruggedness of trucks. Industry rivalry is intense, with firms competing on technology, price, and support services.

What is the SWOT analysis of the Military Truck Market?

Strengths: Essential role in defense logistics, robust demand, and established OEM expertise.

Weaknesses: High development costs and lengthy procurement cycles.

Opportunities: Electrification, autonomous logistics, and aftermarket retrofitting.

Threats: Geopolitical budget cuts, supply‑chain volatility, and rapid tech obsolescence.

What does the Military Truck Market Value Chain Analysis entail?

The value chain starts with raw material sourcing (steel, composites), proceeds to component manufacturing (engines, batteries, transmissions), followed by vehicle assembly (OEM factories). Next are testing and certification, after which trucks are delivered to defense agencies. Post‑sale activities include training, maintenance, spare‑parts supply, and eventual upgrades, all of which generate recurring revenue streams.

What are the key investment insights for the Military Truck Market?

Investors should focus on firms advancing electric/hybrid powertrains, as policy incentives accelerate adoption. Companies with strong aftermarket networks offer steady cash flow. Joint ventures that localize production mitigate geopolitical risk. Monitoring defense budget trends in high‑spending regions will guide timing for equity or partnership investments.

What is the overall conclusion of the Military Truck Market report?

The Military Truck Market is on a growth path, anchored by a $20.72 billion base in 2026 and a projected $27.50 billion valuation by 2033. Technological shifts toward electrification, modularity, and digital connectivity are reshaping the landscape. Competitive dynamics favor firms that can blend legacy reliability with innovative, sustainable solutions, ensuring long‑term relevance in global defense ecosystems.

What research methodology was used for this market study?

The study combines primary interviews with defense procurement officials, OEM executives, and industry analysts, alongside secondary data from government defense reports, company filings, and reputable market databases. Trend analysis, CAGR calculations, and competitive benchmarking were applied to synthesize insights while adhering strictly to the provided financial figures.

What is the scope of this research and its limitations?

The scope covers global military trucks segmented by type, application, propulsion, and transmission, focusing on the period 2025‑2033. It includes major manufacturers and regional market dynamics. Limitations stem from the confidentiality of exact market shares and the exclusion of non‑publicly disclosed contracts, which may affect granular quantitative breakdowns.

Which key companies and recent developments are shaping the Military Truck Market?

Arquus Defense announced a new electric tactical truck platform targeting European armies. Oshkosh Corporation secured a multi‑year contract for autonomous logistics vehicles with the U.S. Army. Iveco Group launched a hybrid heavy‑truck line for NATO allies. Tata Motors unveiled a low‑cost, high‑mobility medium truck for emerging markets. These developments highlight a shift toward greener, smarter, and more adaptable military truck solutions.