1. Marine Lighting Market Overview – Definition, scope, and significance?

The marine lighting market encompasses all lighting products and solutions installed on vessels, docks, and related marine infrastructure. It includes functional and decorative lighting, serving end‑users such as commercial and passenger ships, and spans technologies from LED to halogen, fluorescent, and xenon. The market’s significance lies in its role in navigation safety, operational efficiency, crew comfort, and aesthetic appeal, directly influencing maritime regulatory compliance and passenger experience.

2. Marine Lighting Market Drivers, Restraints, Challenges, and Opportunities – Key growth factors and obstacles?

Key drivers include stringent international maritime safety standards, the rapid adoption of energy‑efficient LED technology, and growing demand for passenger‑focused cabin ambience on cruise ships. Restraints stem from high upfront costs of advanced lighting systems and the complex certification processes for marine equipment. Challenges involve harsh marine environments that test product durability and the need for skilled installation crews. Opportunities arise from retrofitting aging fleets, integration of smart‑controlled lighting, and expanding offshore wind‑farm support facilities.

3. Marine Lighting Market Growth Trends – Current and emerging trends shaping the market?

Current trends feature a decisive shift toward LED lighting, driven by its low power consumption and long lifespan. Emerging trends include IoT‑enabled lighting that allows remote monitoring and adaptive brightness for energy savings, and the rise of customizable decorative lighting to enhance brand identity on passenger vessels. Additionally, there is a growing emphasis on eco‑friendly, recyclable materials in lighting housings to meet sustainability mandates.

4. COVID-19 Impact on the Marine Lighting Market – Pandemic effects and recovery trajectory?

The pandemic caused a temporary slowdown in new vessel construction and dock upgrades, curtailing demand for marine lighting in 2020‑2021. However, the market displayed resilience as refurbishment projects revived, and health‑oriented lighting solutions (e.g., UV‑C sterilization) gained interest. Recovery accelerated in 2022‑2023, aligning with the broader rebound in global shipping and cruise activities, positioning the market for a robust growth phase.

5. Marine Lighting Market Competitive Landscape – Major competitors and market consolidation?

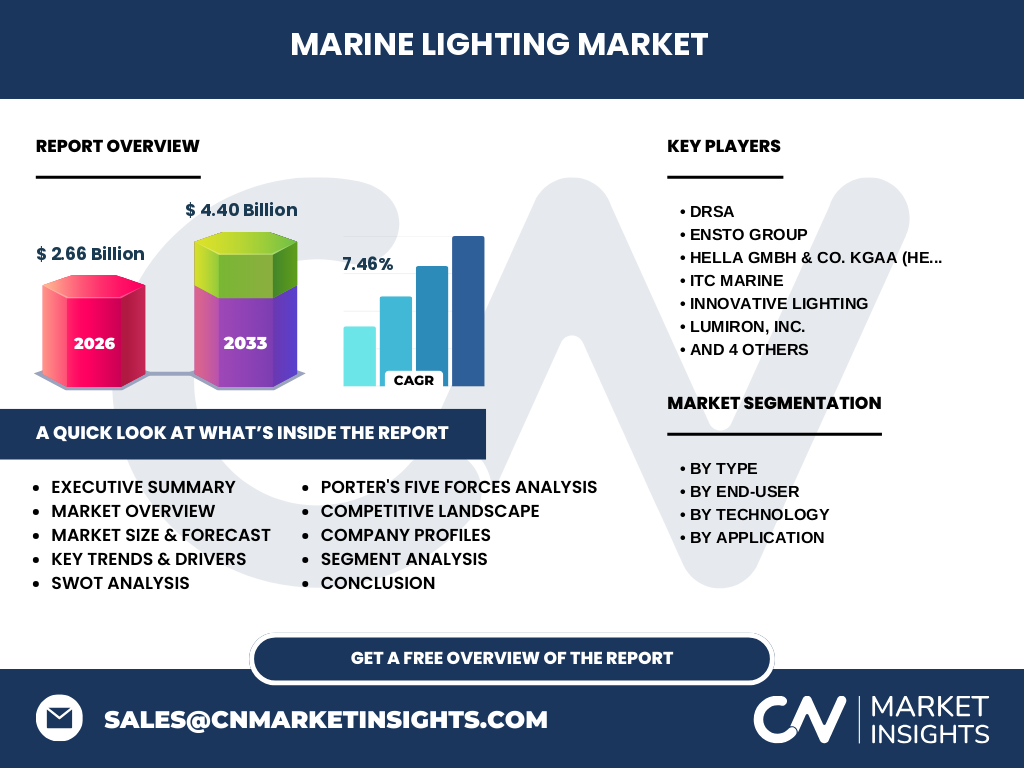

The competitive arena includes established players such as DRSA, Ensto Group, HELLA GmbH & Co. KGaA (Hella Marine), ITC Marine, Innovative Lighting, Lumiron, Inc., Lumitec LLC, NJZ Lighting Technology Co., Ltd., Phoenix Products LLC, and The Carlisle & Finch Co. These firms compete on technology innovation, after‑sales service, and global distribution networks. Recent consolidation trends feature strategic acquisitions aimed at expanding LED portfolios and strengthening presence in high‑growth regions.

6. Executive Summary – High‑level overview and key findings about Marine Lighting Market?

The marine lighting market is projected to grow from a 2026 valuation of $2.66 billion to $4.40 billion by 2033, reflecting a CAGR of 7.46 %. Growth is propelled by safety regulations, LED adoption, and fleet modernization. While cost and certification remain hurdles, opportunities in smart lighting and retrofits dominate the outlook. Leading manufacturers are consolidating capabilities to capture expanding demand across commercial and passenger segments.

7. Marine Lighting Market Forecast – Projections for 2025‑2032 period?

Based on the stated CAGR of 7.46 %, the market is expected to maintain steady expansion throughout 2025‑2032. The forecast underscores a compound increase in LED adoption, heightened investment in energy‑saving technologies, and rising expenditures on decorative lighting for premium cruise experiences. The trajectory suggests that by 2032 the market value will comfortably exceed $4 billion, reinforcing its attractiveness for long‑term investors.

8. Marine Lighting Market Size and Share by Segmentation – Breakdown by segment?

Segmentation by type identifies functional lighting—essential for navigation, safety, and operational tasks—and decorative lighting, which enhances interior aesthetics. By end‑user, commercial ships dominate due to extensive cargo‑handling requirements, while passenger ships drive growth in decorative solutions. Technology segmentation shows LED leading the charge, followed by halogen, fluorescent, and xenon. Application‑wise, navigation lights, dome lights, compartment and utility lights, safety lights, and docking lights each capture distinct niche demands.

9. Global Marine Lighting Market Size and Share by Region – Geographic distribution?

The market exhibits a worldwide footprint, with major consumption in North America, Europe, and the Asia‑Pacific region. North America benefits from a large commercial fleet and stringent safety standards, Europe leverages its historic maritime hubs, and Asia‑Pacific experiences rapid fleet expansion and offshore infrastructure growth, collectively driving the bulk of market revenue.

10. Regional Analysis of the Marine Lighting Market – Detailed regional market performance?

In North America, the focus is on upgrading aging vessels with LED solutions to meet emission targets. Europe’s market is characterized by high regulatory compliance and strong demand for decorative lighting on luxury cruise lines. Asia‑Pacific shows the fastest growth, propelled by shipbuilding powerhouses, expanding container trade, and increasing offshore wind projects that require robust dock lighting. Latin America and the Middle East present niche opportunities linked to emerging ports and tourism‑focused vessels.

11. Leading Company Profiles in the Marine Lighting Market – Industry players and strategies?

DRSA emphasizes modular LED systems for easy retrofitting. Ensto Group leverages its electrical expertise to offer integrated lighting and power solutions. HELLA Marine focuses on high‑performance xenon and LED products for safety-critical applications. ITC Marine pursues aggressive R&D in marine‑grade smart lighting. Innovative Lighting and Lumiron, Inc. target decorative segments with customizable color‑changing fixtures. Lumitec LLC, NJZ Lighting, Phoenix Products, and Carlisle & Finch expand market reach through geographic partnerships and after‑sales service networks.

12. Porter’s Five Forces Analysis of the Marine Lighting Market – Competitive forces assessment?

Threat of new entrants is moderate; high certification costs and technical expertise create barriers. Bargaining power of suppliers is low to moderate, as component suppliers are abundant, especially for LEDs. Bargaining power of buyers is moderate, with ship owners seeking cost‑effective yet compliant solutions. Threat of substitutes is low, given the specialized nature of marine lighting. Industry rivalry is high, driven by technological innovation and price competition among established manufacturers.

13. SWOT Analysis of the Marine Lighting Market – Strengths, weaknesses, opportunities, threats?

Strengths: Strong regulatory demand, rapid LED technology adoption, and a diverse end‑user base. Weaknesses: High initial investment and complex certification processes. Opportunities: Smart, IoT‑enabled lighting, fleet retrofitting programs, and offshore renewable infrastructure. Threats: Economic downturns affecting shipbuilding, potential supply‑chain disruptions for semiconductor components, and evolving environmental regulations.

14. Marine Lighting Market Value Chain Analysis – Industry structure and value flow?

The value chain begins with raw material suppliers (glass, aluminum, semiconductor chips), proceeds to component manufacturers (LED modules, drivers), then to system integrators that assemble functional and decorative units. OEMs and shipyards incorporate these systems into vessels, followed by installation specialists. After‑sales services, maintenance contracts, and end‑of‑life recycling complete the chain, emphasizing the importance of long‑term support.

15. Key Investment Insights in the Marine Lighting Market – Strategic investment recommendations?

Investors should target companies with strong LED R&D pipelines and proven certification capabilities. Capital allocation toward firms expanding smart‑lighting platforms can capture premium pricing. Retro‑fit services present recurring revenue streams, while partnerships with shipbuilders secure long‑term supply contracts. Geographic diversification—especially into the fast‑growing Asia‑Pacific market—enhances portfolio resilience.

16. Marine Lighting Market Conclusion – Summary and key takeaways?

The marine lighting market is on a decisive upward trajectory, underpinned by safety regulations, LED efficiency gains, and aesthetic demand from passenger vessels. Despite cost and certification hurdles, the market’s 7.46 % CAGR and projected $4.40 billion size by 2033 signal robust growth. Companies that innovate in smart, energy‑saving solutions and pursue strategic regional expansions are positioned to lead.

17. Research Methodology – How this research was conducted?

The study combined primary interviews with industry experts, OEMs, and end‑users, alongside secondary data from company reports, maritime regulatory publications, and market databases. Trend analysis, CAGR extrapolation, and competitive benchmarking were applied to derive forecasts and segmentation insights. All figures reflect the provided base year (2026) and forecast horizon (2027‑2033).

18. Research Scope – Coverage and limitations?

The scope covers global marine lighting across functional and decorative categories, all major end‑users, technologies (LED, halogen, fluorescent, xenon), and applications (navigation, dome, compartment, safety, docking). Limitations include the exclusion of ultra‑niche lighting accessories and proprietary pricing data, focusing instead on aggregated market values and publicly disclosed information.

19. Key Companies and Recent Developments in the Marine Lighting Market – Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

DRSA recently launched a modular LED retrofit kit for container ships, reducing installation time by 30 %. Ensto Group announced a partnership with a leading Asian shipyard to supply integrated power‑lighting modules. HELLA Marine introduced a high‑intensity xenon navigation system meeting the latest IMO standards. ITC Marine unveiled a cloud‑based lighting management platform for cruise liners. Innovative Lighting rolled out a customizable RGB decorative line for luxury cabins, while Lumiron, Inc. secured a multi‑year contract to supply safety lights for offshore wind‑farm support vessels. Lumitec LLC expanded its North American distribution network, and NJZ Lighting Technology opened a new R&D center focused on marine‑grade LEDs. Phoenix Products LLC entered a joint venture with a European dock operator to provide energy‑saving docking lights. The Carlisle & Finch Co. released a next‑generation floodlight designed for harsh salt‑water environments.