What is the North America Waste Heat Boiler Market Overview – Definition, scope, and significance?

The North America Waste Heat Boiler Market comprises technologies that capture residual thermal energy from industrial processes and convert it into useful steam or hot water. These boilers are employed across power generation, oil & gas, chemicals, primary metals, and non‑metallic minerals, among other sectors. By recovering waste heat, they improve overall plant efficiency, reduce fuel consumption, and lower greenhouse‑gas emissions, making them critical for meeting both economic and sustainability goals in the region.

What are the North America Waste Heat Boiler Market Drivers, Restraints, Challenges, and Opportunities?

Key drivers include stricter environmental regulations, rising energy costs, and the need for higher plant efficiency. Opportunities arise from increasing investments in renewable integration and retrofitting of aging facilities. Restraints involve high upfront capital requirements and complex integration with existing systems. Challenges encompass a skilled‑labor shortage for installation and maintenance, as well as the variability of waste‑heat characteristics across industries.

What are the North America Waste Heat Boiler Market Growth Trends?

Current trends show a shift toward high‑efficiency, compact designs that can be installed vertically or horizontally, depending on space constraints. There is growing adoption of ultra‑high‑temperature waste‑heat recovery in the petrochemical and primary metals sectors. Digital monitoring and IoT integration are emerging to optimize performance and enable predictive maintenance, driving further market adoption.

How has COVID‑19 impacted the North America Waste Heat Boiler Market and what is the recovery trajectory?

The pandemic caused temporary project delays and reduced capital spending in 2020‑21, particularly in the oil & gas segment. However, the market rebounded quickly as industries prioritized energy‑saving measures to offset rising operational costs. Recovery is now aligned with broader industrial resurgence, and the market is projected to continue expanding at a steady pace.

What does the North America Waste Heat Boiler Market Competitive Landscape look like?

The market is fragmented, with several global and regional players competing on technology, service, and project execution. Major competitors such as Alfa Laval, Bosch Group, General Electric, Siemens AG, and Thyssenkrupp AG dominate the high‑end segment, while companies like Nooter/Eriksen and Viessmann focus on customized solutions. Recent consolidation includes strategic partnerships and joint ventures aimed at expanding service networks across North America.

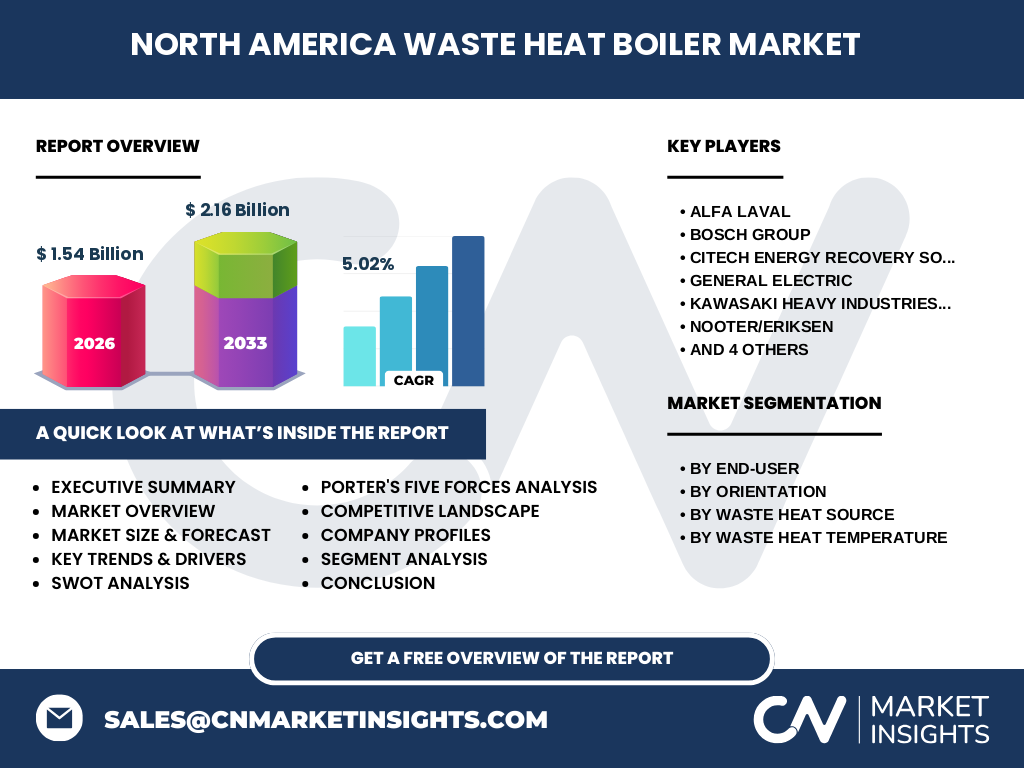

What are the key findings in the Executive Summary of the North America Waste Heat Boiler Market?

The market is valued at US 1.54 billion in 2026 and is projected to reach US 2.16 billion by 2033, reflecting a 5.02 % CAGR. Growth is driven by regulatory pressure, energy‑price volatility, and increasing demand for carbon‑reduction solutions. Horizontal and vertical boiler orientations, as well as medium‑to‑ultra‑high temperature applications, are gaining traction. Leading manufacturers are investing in digitalization and aftermarket services to capture higher margins.

What is the forecast for the North America Waste Heat Boiler Market for 2025‑2032?

Based on the provided CAGR of 5.02 %, the market is expected to expand consistently each year, moving from the 2026 baseline of US 1.54 billion toward the 2033 forecast of US 2.16 billion. This trajectory indicates robust demand across all end‑user segments, with the strongest acceleration anticipated in power‑generation utilities and oil & gas as they pursue stricter emissions compliance.

How is the North America Waste Heat Boiler Market size and share segmented?

Segmentation by end‑user shows a balanced distribution among Power Generation Utilities, Oil & Gas, Chemical, Primary Metals, and Non‑Metallic Minerals. By orientation, both Horizontal and Vertical designs capture significant share, reflecting diverse plant layouts. Waste‑heat source segmentation includes Oil Engine Exhaust, Gas Engine Exhaust, Gas Turbine Exhaust, Incinerator Exit Gases, and Kiln & Furnace Gases, each serving niche applications. Temperature categories—Medium, High, and Ultra‑High—highlight the market’s capability to handle a wide thermal spectrum.

What is the geographic distribution of the Global North America Waste Heat Boiler Market?

The market is concentrated in the United States and Canada, with the United States accounting for the majority of demand due to its extensive industrial base and energy‑intensive sectors. Canada contributes a smaller yet growing share, driven by its focus on renewable integration and emissions reduction in mining and oil‑sand operations.

What does the regional analysis of the North America Waste Heat Boiler Market reveal?

In the United States, the Power Generation and Oil & Gas segments lead installations, supported by federal incentives for energy efficiency. The Midwest and Texas regions show heightened activity in primary metals and chemical processing. Canada’s market growth is anchored in the mining sector, especially non‑metallic minerals, where waste‑heat recovery from kiln and furnace gases is becoming standard practice.

Which companies are leading in the North America Waste Heat Boiler Market and what are their strategies?

Key players include Alfa Laval, Bosch Group, General Electric, Siemens AG, and Thyssenkrupp AG, which focus on advanced high‑temperature designs and digital services. Nooter/Eriksen and Viessmann emphasize customized engineering for niche applications. Companies are expanding service footprints through acquisitions, partnering with engineering firms, and investing in R&D for compact vertical units to address space‑limited retrofits.

How does Porter’s Five Forces analysis apply to the North America Waste Heat Boiler Market?

Threat of new entrants is moderate due to high capital intensity and technical expertise requirements. Bargaining power of suppliers is low, as component sourcing is diversified. Bargaining power of buyers is moderate; large utilities and petrochemical firms can negotiate pricing. Threat of substitutes remains limited, given the unique efficiency gains of waste‑heat boilers. Industry rivalry is high, driven by technological differentiation and service contracts.

What is the SWOT analysis of the North America Waste Heat Boiler Market?

Strengths: Proven energy‑saving technology, regulatory support, and mature supplier base.

Weaknesses: High initial investment and integration complexity.

Opportunities: Expanding retrofits, digital optimization, and growth in ultra‑high‑temperature applications.

Threats: Economic downturns affecting capital projects and potential competing clean‑energy technologies.

How is the value chain structured in the North America Waste Heat Boiler Market?

The value chain starts with raw‑material suppliers (steel, alloys), moves to component manufacturers (heat exchangers, turbines), followed by system integrators who design and assemble the boiler. The next stage involves EPC contractors who install the units, and finally, service providers who offer maintenance, performance monitoring, and aftermarket upgrades.

What are the key investment insights for the North America Waste Heat Boiler Market?

Investors should focus on companies with strong service portfolios and digital monitoring capabilities, as these generate recurring revenue. Funding retrofitting projects, especially in the Power Generation and Oil & Gas sectors, offers attractive returns given the clear ROI from fuel savings. Partnerships with OEMs that specialize in ultra‑high‑temperature recovery can also unlock growth.

What are the main conclusions of the North America Waste Heat Boiler Market report?

The market is on a solid growth path, underpinned by regulatory pressure and the economic benefits of energy recovery. With a 5.02 % CAGR, it will expand to US 2.16 billion by 2033. Diversified applications, advances in vertical and horizontal designs, and increasing digitalization are set to shape the competitive landscape. Companies that combine technical innovation with strong service networks are best positioned to capture market share.

How was the research methodology conducted for this market report?

Primary data were gathered through interviews with industry executives, OEM specialists, and end‑user engineers. Secondary sources included company annual reports, regulatory publications, and reputable market databases. Data triangulation ensured consistency, and quantitative forecasts were derived using the provided CAGR of 5.02 % applied to the 2026 baseline.

What is the scope of the research, including coverage and limitations?

The study covers the North America region, focusing on all major end‑users, boiler orientations, waste‑heat sources, and temperature categories listed. It excludes detailed country‑by‑country financial breakdowns beyond the United States and Canada, and it does not project macro‑economic variables beyond the stated market size and CAGR.

Which key companies and recent developments are highlighted in the North America Waste Heat Boiler Market?

Alfa Laval announced a new line of compact vertical boilers for refinery retrofits. Bosch Group introduced IoT‑enabled monitoring platforms for real‑time efficiency tracking. General Electric launched a high‑temperature turbine‑integrated boiler aimed at gas‑turbine exhaust recovery. Siemens AG announced a partnership with a North American utility to pilot ultra‑high‑temperature waste‑heat recovery. Thyssenkrupp AG released a modular horizontal boiler system designed for quick installation in chemical plants. These developments illustrate the market’s focus on integration, digitalization, and modularity.