1. What is the Asia Pacific Drug Delivery Systems Market overview – definition, scope, and significance?

The Asia Pacific Drug Delivery Systems (DDS) market encompasses all technologies, devices, and services that enable the safe, effective, and controlled administration of pharmaceutical compounds across the region. It includes systems for home care, hospitals, and clinics, distributed through pharmacy channels (hospital, retail, and online) and covering a broad range of administration routes such as oral, injectable, trans‑mucosal, topical, implantable, and ocular. The market’s significance lies in its role as an enabler of therapeutic innovation, patient adherence, and health‑care efficiency, particularly in a region where chronic disease prevalence, aging populations, and rising health‑care expenditure drive demand for advanced delivery solutions.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia Pacific Drug Delivery Systems market?

Key drivers include rapid urbanization, expanding middle‑class populations, and increasing prevalence of chronic conditions that require long‑term medication regimens. Government initiatives promoting home‑based care and tele‑medicine further stimulate demand for user‑friendly delivery devices. Restraints stem from regulatory heterogeneity across countries, high R&D costs, and price sensitivity in emerging economies. Challenges involve supply‑chain complexities, especially for temperature‑sensitive biologics, and the need for skilled healthcare professionals to manage advanced systems. Opportunities arise from the growing biopharmaceutical pipeline, rising adoption of digital health platforms that integrate smart DDS, and untapped rural markets where portable, easy‑to‑use devices can bridge access gaps.

3. What are the current growth trends in the Asia Pacific Drug Delivery Systems market?

Current trends feature a shift toward personalized and precision delivery solutions, such as wearable injectors and smart inhalers that collect adherence data. There is a noticeable rise in the adoption of implantable and ocular delivery platforms, driven by increasing ophthalmic procedures and demand for sustained‑release formulations. Besides, the market is witnessing a surge in partnerships between device manufacturers and pharmaceutical firms to co‑develop combination products that enhance therapeutic outcomes.

4. How has COVID‑19 impacted the Asia Pacific Drug Delivery Systems market and what is the recovery trajectory?

The pandemic accelerated demand for home‑care delivery systems as hospitals faced capacity constraints and patients preferred remote treatment. Online pharmacy channels experienced a marked uptick, prompting manufacturers to expand digital distribution capabilities. Post‑pandemic, the market is maintaining momentum, with continued emphasis on self‑administration devices and tele‑health integration, indicating a robust recovery trajectory that aligns with the projected 7.99% CAGR.

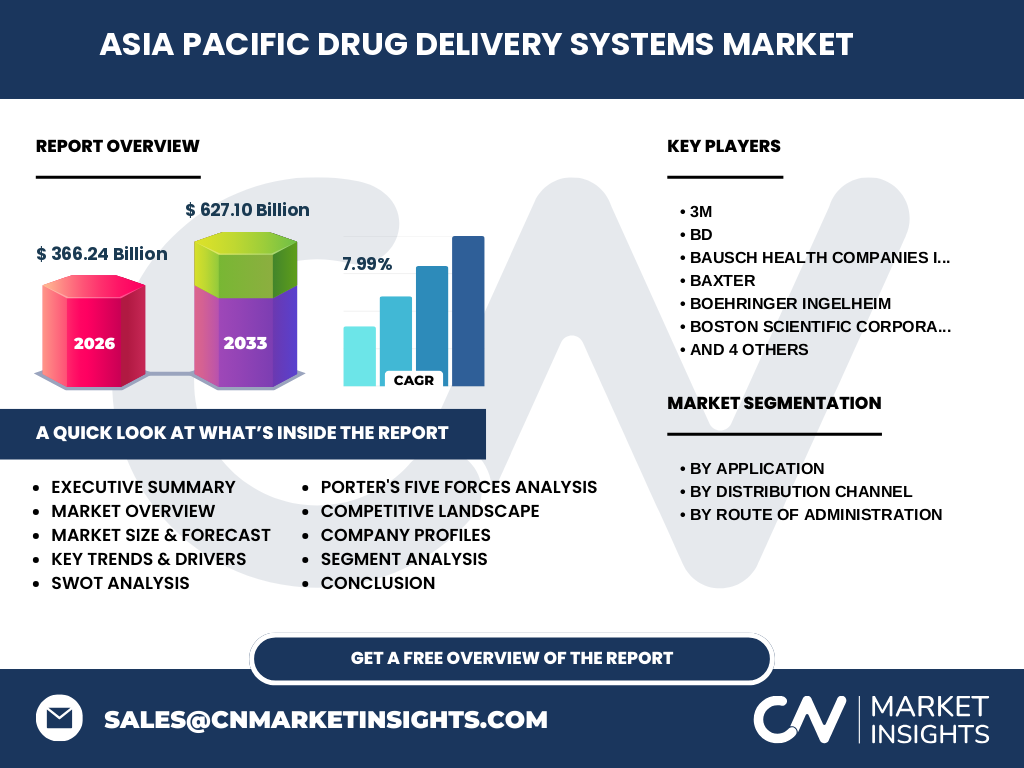

5. Who are the major competitors and what is the level of market consolidation in the Asia Pacific Drug Delivery Systems market?

Key competitors include global leaders such as 3M, BD, Bausch Health Companies Inc., Baxter, Boehringer Ingelheim, Boston Scientific Corporation, GlaxoSmithKline plc., Johnson & Johnson Services, Inc., Novartis AG, and Novo Nordisk A/S. The competitive landscape is characterized by strategic collaborations, acquisitions, and joint ventures aimed at expanding product portfolios and geographic reach. While the market remains fragmented with many niche players, consolidation is evident through mergers that seek to combine technology platforms and broaden distribution networks.

6. What are the high‑level findings in the executive summary for the Asia Pacific Drug Delivery Systems market?

The Asia Pacific DDS market is valued at USD 366.24 billion in 2026 and is projected to reach USD 627.10 billion by 2033, reflecting a strong 7.99% CAGR. Growth is propelled by demographic shifts, rising chronic disease burden, and digital health integration. Home‑care settings and online pharmacy channels are emerging as high‑growth segments. Major pharmaceutical and device manufacturers are intensifying R&D and forming alliances, positioning the region as a hub for next‑generation delivery technologies.

7. What is the forecast for the Asia Pacific Drug Delivery Systems market from 2025 to 2032?

Based on the provided CAGR of 7.99%, the market is expected to expand steadily, reaching approximately USD 627.10 billion by 2033. This growth reflects compound annual expansion driven by continued investment in innovative delivery platforms, scaling of manufacturing capabilities, and expanding reimbursement frameworks that support advanced DDS adoption across both urban and rural settings.

8. How is the Asia Pacific Drug Delivery Systems market sized and shared by application, distribution channel, and route of administration?

Segmentation reveals three primary dimensions:

• Application: Home Care Settings and Hospitals & Clinics, with home‑care gaining traction due to tele‑medicine and patient‑centric care models.

• Distribution Channel: Hospital Pharmacies, Retail Pharmacies, and Online Pharmacies, where online channels are experiencing the fastest growth.

• Route of Administration: Transmucosal, Oral, Injectable, Topical, Implantable, and Ocular. Injectable and oral routes remain dominant, while implantable and ocular routes show higher growth rates linked to specialized therapeutic areas.

9. What is the geographic distribution of the Asia Pacific Drug Delivery Systems market?

The market spans the broader Asia Pacific region, encompassing developed economies such as Japan, South Korea, and Australia, alongside high‑growth markets like China, India, and Southeast Asian nations. Geographic distribution aligns with health‑care infrastructure maturity, regulatory support, and pharmaceutical manufacturing hubs, positioning the region as a major contributor to global DDS demand.

10. How does each sub‑region within Asia Pacific perform in the Drug Delivery Systems market?

East Asia (China, Japan, South Korea) leads in volume due to advanced health‑care systems and substantial biotech pipelines. South Asia (India) shows rapid expansion driven by large patient populations and government push for affordable delivery solutions. Southeast Asia (Indonesia, Malaysia, Thailand, Vietnam) presents a mix of emerging demand for home‑care devices and growing retail pharmacy networks. Australasia (Australia, New Zealand) contributes higher per‑capita adoption of premium DDS technologies.

11. What are the profiles of leading companies operating in the Asia Pacific Drug Delivery Systems market?

Leading players such as 3M and BD focus on injection devices and safety‑engineered systems. Bausch Health and Novartis emphasize ocular and implantable platforms. Baxter and Johnson & Johnson provide extensive hospital‑pharmacy solutions. Boehringer Ingelheim and Boston Scientific drive innovation in trans‑mucosal and implantable technologies. Novo Nordisk leverages its diabetes portfolio to expand injectable delivery devices, while GlaxoSmithKline combines vaccine delivery expertise with emerging oral platforms. These firms invest heavily in R&D, strategic partnerships, and regional manufacturing to capture market share.

12. What does Porter’s Five Forces analysis reveal about the Asia Pacific Drug Delivery Systems market?

• Threat of New Entrants: Moderate; high capital requirements and regulatory barriers protect incumbents, yet niche innovators can enter via digital health solutions.

• Bargaining Power of Suppliers: Low to moderate; raw material suppliers for polymers and electronics are fragmented, reducing supplier leverage.

• Bargaining Power of Buyers: Increasing; hospitals and large pharmacy chains demand cost‑effective solutions, while patients influence product design through preference for convenience.

• Threat of Substitutes: Low; alternative treatment modalities cannot fully replace the need for precise drug delivery devices.

• Industry Rivalry: High; intense competition among global and regional players drives innovation, pricing pressure, and strategic collaborations.

13. What are the SWOT highlights for the Asia Pacific Drug Delivery Systems market?

Strengths: Strong growth drivers, diversified application base, and presence of multinational innovators.

Weaknesses: Complex regulatory environments and high R&D costs.

Opportunities: Expansion of digital health integration, untapped rural markets, and rising demand for implantable and ocular systems.

Threats: Price sensitivity in emerging economies and potential supply‑chain disruptions for high‑tech components.

14. How is the value chain structured for the Asia Pacific Drug Delivery Systems market?

The value chain begins with raw material sourcing (polymers, metals, electronics), followed by design and R&D, prototyping, and regulatory approval. Manufacturing occurs in both global hubs and localized facilities to serve regional demand. Distribution flows through hospital pharmacies, retail networks, and increasingly via online platforms. Post‑sale services include training, maintenance, and data analytics for smart devices, creating ancillary revenue streams.

15. What key investment insights should stakeholders consider for the Asia Pacific Drug Delivery Systems market?

Investors should target companies with strong pipelines in digital‑enabled DDS, robust IP portfolios, and strategic partnerships that enhance market access. Prioritizing firms expanding manufacturing capacity in China and India can capture cost advantages. Moreover, funding ventures that integrate AI‑driven adherence monitoring offers upside as payers and providers seek outcome‑based solutions.

16. What are the main conclusions drawn from the Asia Pacific Drug Delivery Systems market analysis?

The market is on a clear growth trajectory, underpinned by demographic trends, chronic disease burden, and digital health adoption. Home‑care and online channels are reshaping distribution, while advanced routes such as implantable and ocular delivery provide high‑margin opportunities. Competitive dynamics favor innovators that can navigate regulatory landscapes and deliver cost‑effective, patient‑centric solutions.

17. How was the research for this report conducted?

The study employed a mixed‑method approach combining secondary data extraction from industry reports, regulatory filings, and company disclosures with primary insights from expert interviews across pharma, device manufacturing, and health‑care delivery. Quantitative analysis leveraged the provided market size (USD 366.24 billion in 2026) and forecast (USD 627.10 billion by 2033) to calculate the 7.99% CAGR, which informed trend extrapolation and segmentation estimates.

18. What is the scope of this research and its limitations?

The scope covers the full Asia Pacific geography, all major delivery routes, applications, and distribution channels detailed in the segmentation framework. Limitations include the exclusion of granular country‑level revenue breakdowns and the reliance on publicly available data for competitive positioning, which may omit confidential pipeline information.

19. Which key companies have announced recent developments in the Asia Pacific Drug Delivery Systems market?

Recent activities include 3M’s launch of a next‑generation safety‑engineered injection system, BD’s partnership with a leading Chinese biotech firm to co‑develop wearable infusion devices, and Bausch Health’s introduction of an ocular implant for sustained‑release therapy. Baxter announced expansion of its manufacturing footprint in India, while Johnson & Johnson rolled out a digital adherence platform integrated with its inhaler portfolio. Novo Nordisk highlighted a new ultra‑long‑acting insulin injector aimed at Asian markets, and Novartis disclosed a collaboration with a tele‑health provider to distribute home‑care DDS through online pharmacies.